CS - A Swiss CDS Story

2023-03-24 03:33:00 ET

Summary

- The dramatic "takeover" of Credit Suisse by UBS has highlighted Switzerland's rather distinctive approach to bank capital.

- Documentation for Credit Suisse's Sfr16bn AT1 bonds - now worth zero - appear to allow a full write-down of the instruments without shareholders absorbing complete losses.

- European AT1 debt typically do not include such provisions - the Swiss government reinforced the decision by introducing emergency legislation empowering FINMA to write down AT1.

{kind=link}

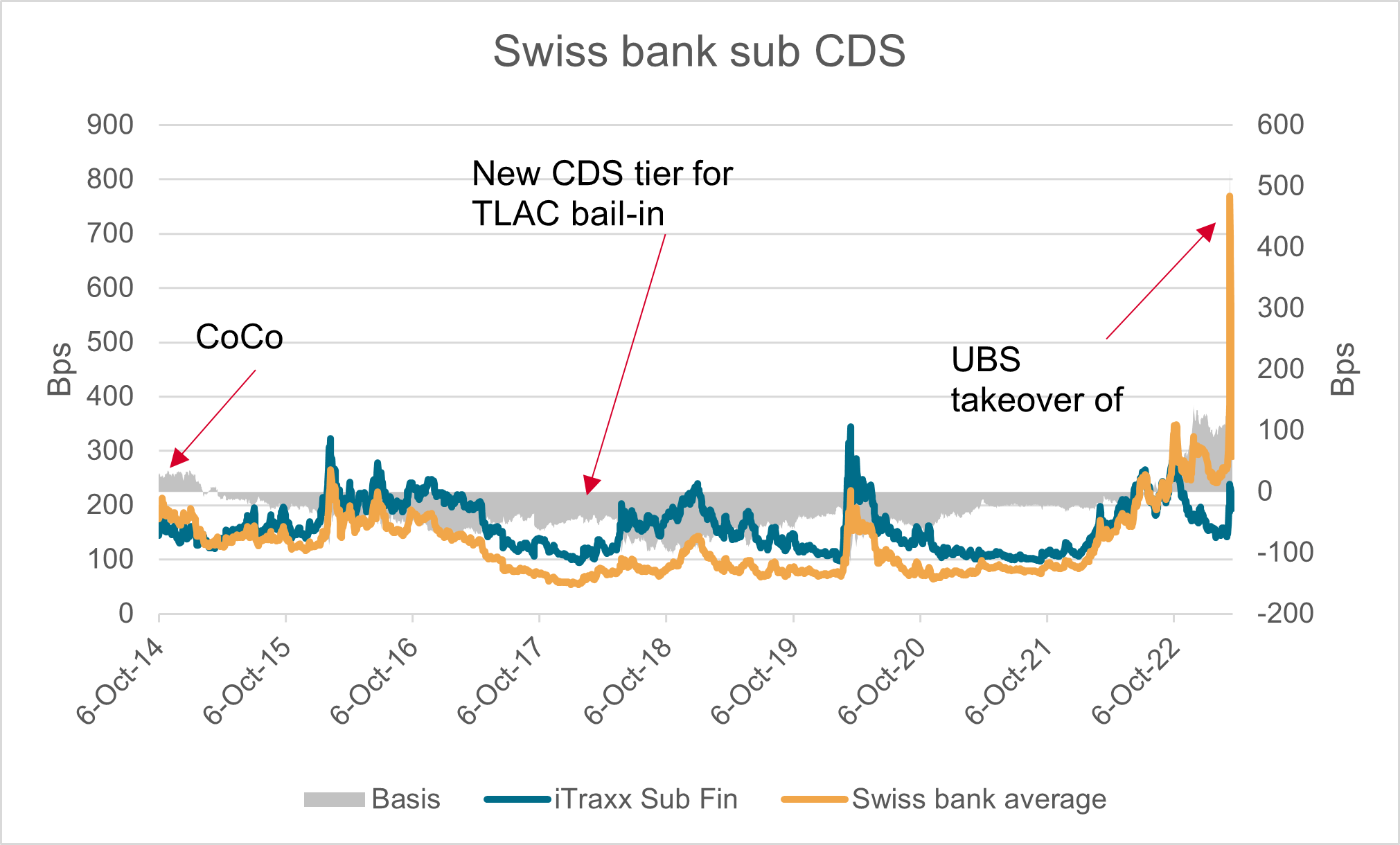

Figure 1. Swiss bank subordinated CDS

The dramatic "takeover" of Credit Suisse ( CS ) by UBS ( UBS ) has highlighted Switzerland's rather distinctive approach to bank capital. Documentation for Credit Suisse's Sfr16bn AT1 bonds - now worth zero - appear to allow a full write-down of the instruments without shareholders absorbing complete losses.

Not only was this idiosyncratic - European AT1 debt typically do not include such provisions - the Swiss government reinforced the decision by introducing emergency legislation empowering FINMA to write down AT1.

No doubt the Swiss government had the stability of its banking system uppermost in its priorities. Some will argue that the creditor hierarchy should always be respected, though it should be noted that the CS/UBS combination is not under the auspices of a formal resolution process. The controversy may rumble on for some time.

Those with longer memories may recall that Swiss banks have a notable history when it comes to Contingent Convertible debt, colloquially known as CoCos. Indeed, for a brief time it changed the way CDS traded.

In 2014, when a new set of ISDA definitions were introduced, an ISDA CoCo supplement was created, along with a new ISDA Transaction type. This was necessary as Swiss banks' tier 2 debt had contingency features, as required by Swiss regulation but not elsewhere in Europe.

From the onset of the new definitions in September 2014, Swiss banks subordinated CDS were quoted "with CoCo" as standard, while other bank sub CDS were without CoCo.

Given that the supplement provided for a Governmental Intervention credit event on tier 2 CoCos, Swiss bank sub CDS traded wider than their European peers. In effect, Swiss bank sub debt had a higher risk of a credit event trigger due to the inclusion of CoCos through the supplement.

Figure 1 shows that the average of Swiss bank 5-year sub CDS (UBS and Credit Suisse) traded around 30bps wider than the iTraxx Subordinated Financials index for the first few months, reflecting the higher risk due to documentation.

But the chart also shows that this basis was transient - by February 2015, the Swiss banks were trading tighter than their counterparts without the CoCo provision. A little over three years later, the negative basis had reached 100bps.

Why was it short lived? Regulation was again responsible for the shift. In 2015, FINMA announced new rules on loss-absorbing capital that increased the amount of Common Equity Tier 1 capital (CET1) in the leverage ratio to 3.5% and, crucially, the remaining 1.5% was to be met with high trigger AT1 instruments.

This was a strengthening of capital requirements compared to the previous regime and on the use of CoCos brought Switzerland more into line with the rest of Europe.

AT1 issuance increased and over time tier 2 debt was called, its use as a capital instrument defunct (though there was an allowance for grandfathering of existing bonds).

The TLAC regulation (Total Loss Absorbing Capacity) for Global Systemically Important Banks (G-SIBs), coming into force in 2019, accelerated the issuance of "bail-in" instruments and a new tier for CDS was created to cover senior-non-preferred bond issuance. In the case of Switzerland, senior unsecured debt issued by the HoldCos was eligible for bail-in.

All of these measures were established to bolster resilience and enable an orderly resolution of banks. But recent events demonstrate there are several methods to rescue a bank - formal resolution is but one.

Figure 1 shows the positive CDS basis ballooning to nearly 500bps prior to the takeover announcement. It has since settled back to 95bps due to Sub tier 2 debt escaping the bail-in and AT1 bearing the burden.

The whole episode is a reminder that credit investors in bank debt need to understand the risk in capital instruments, as well as governments' overriding priority to ensure financial stability.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

A Swiss CDS Story