CA - A Transformative Change For Petrobras Warrants Strong Upside

2023-11-30 16:09:13 ET

Summary

- Petrobras plans to invest $102 billion in various initiatives, primarily in exploration and production operations, over the next few years.

- The company's goal is to capture tremendous cash flow from these initiatives in order to invest in other projects and reward shareholders directly.

- Petrobras will also invest in low carbon initiatives, including renewable energies, carbon capture, and biorefining, as part of its long-term strategy.

- Add in how cheap shares are and the company definitely warrants optimism at this time.

With a market capitalization as of this writing of $97.39 billion, Petrobras ( PBR ) is one of the largest integrated energy companies on the planet. Based in Brazil, the company is a massive player that focuses not only on the exploration and production side of the equation, but also turns the commodities it extracts into finished products for various end uses. With the year coming to an end, management thought it would be a good time to release an updated presentation that shows their current thoughts on the industry, and what investors should likely anticipate for the next few years. Assuming energy prices remain at fairly attractive levels, the company intends to invest around $102 billion in various initiatives. The resulting cash flows should be material and, given how cheap shares are, the upside potential from this point on could be quite nice.

A massive plan

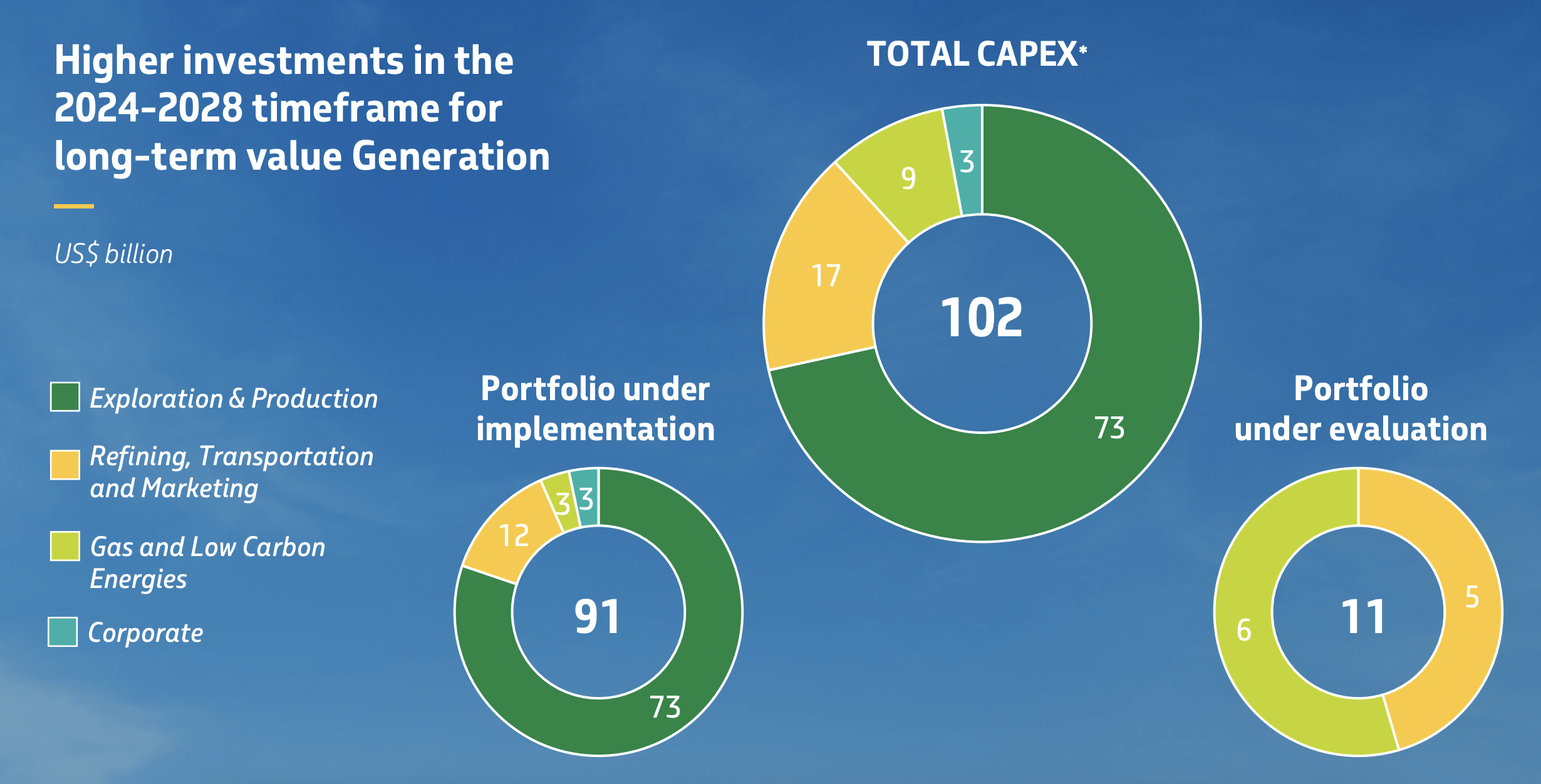

With November practically over, the management team at Petrobras released a plan for what the near term future holds. Or at least it's a plan of what they expect to hold. Many companies in this space are hesitant to forecast out more than a year. But in this case, management has forecasted out five to cover the 2028 fiscal year. From 2024 through 2028, Petrobras expects to allocate around $102 billion toward capital projects. $91 billion worth of this spending is already under implementation by the company. That leaves another $11 billion that is under evaluation.

{kind=link}

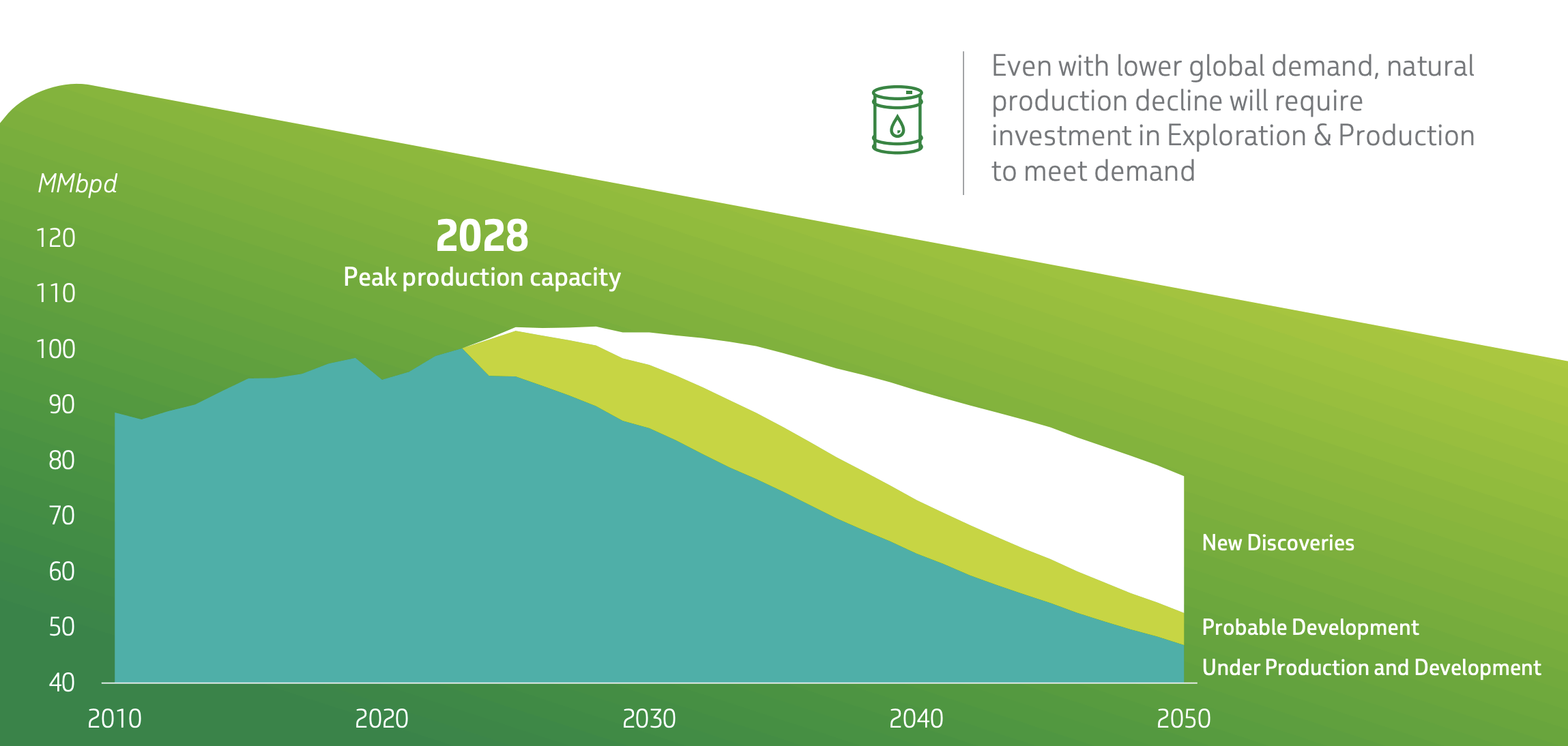

For the purpose of clarity, it might be helpful to first focus our efforts on the largest chunk of spending. The largest, by far, is the $73 billion that management intends to allocate toward its exploration and production operations. As the company has made very clear, its belief is that the days of oil and gas production growth are limited. Total oil production, for instance, should peak sometime around 2028 at less than 110 million barrels of crude per day. It should flat line for about a year or so before starting a permanent descent.

{kind=link}

While this might sound catastrophic if true, it's not the worst thing in the world. And this is because demand for crude is also expected to decline. From 2021 through 2050, for instance, it's believed that light vehicles will go from consuming around 28 million barrels per day worth of oil to 15 million barrels per day. Other types of vehicles on the road should see a decline of about 3 million barrels per day, while the aviation and maritime space combined should see a reduction of 1 million. There will be, of course, some growth areas when it comes to oil consumption. The petrochemical industry, for instance, should continue to see a growth in demand, with demand forecasted to expand from 15 million barrels per day to 22 million barrels per day over this window of time.

{kind=link}

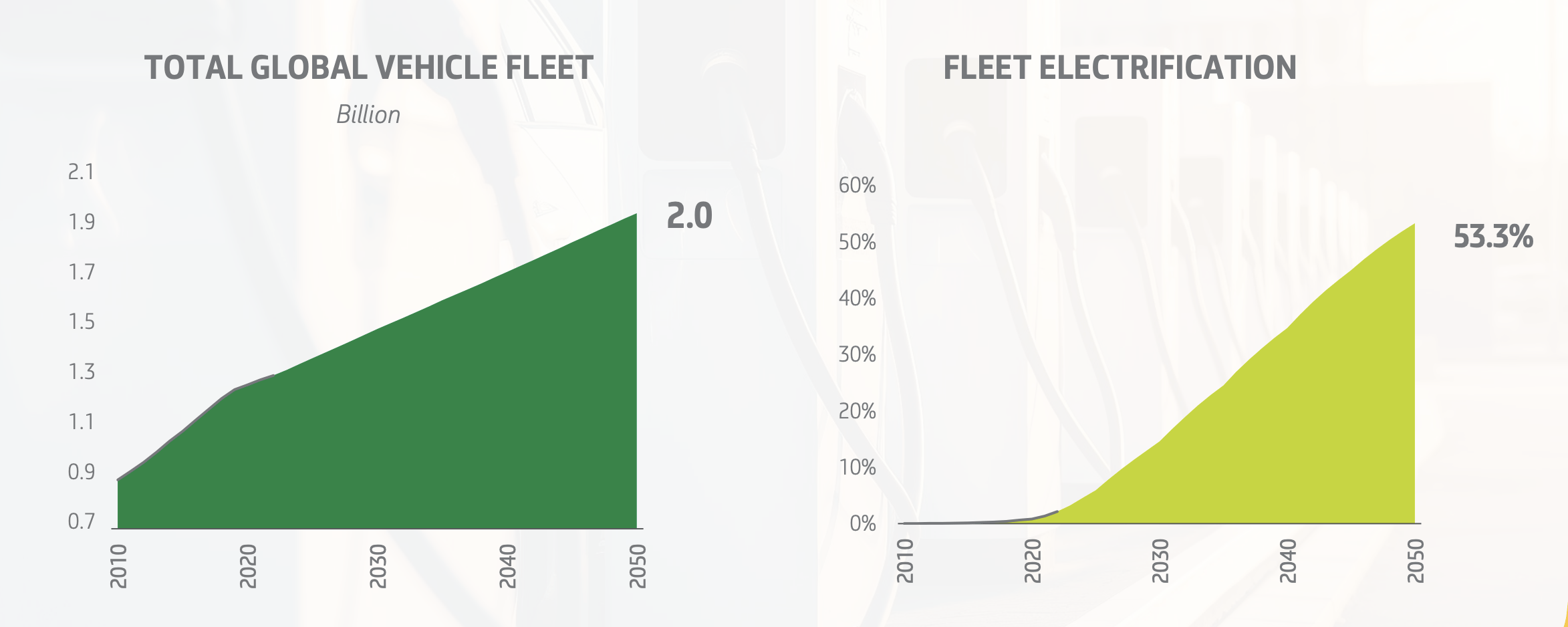

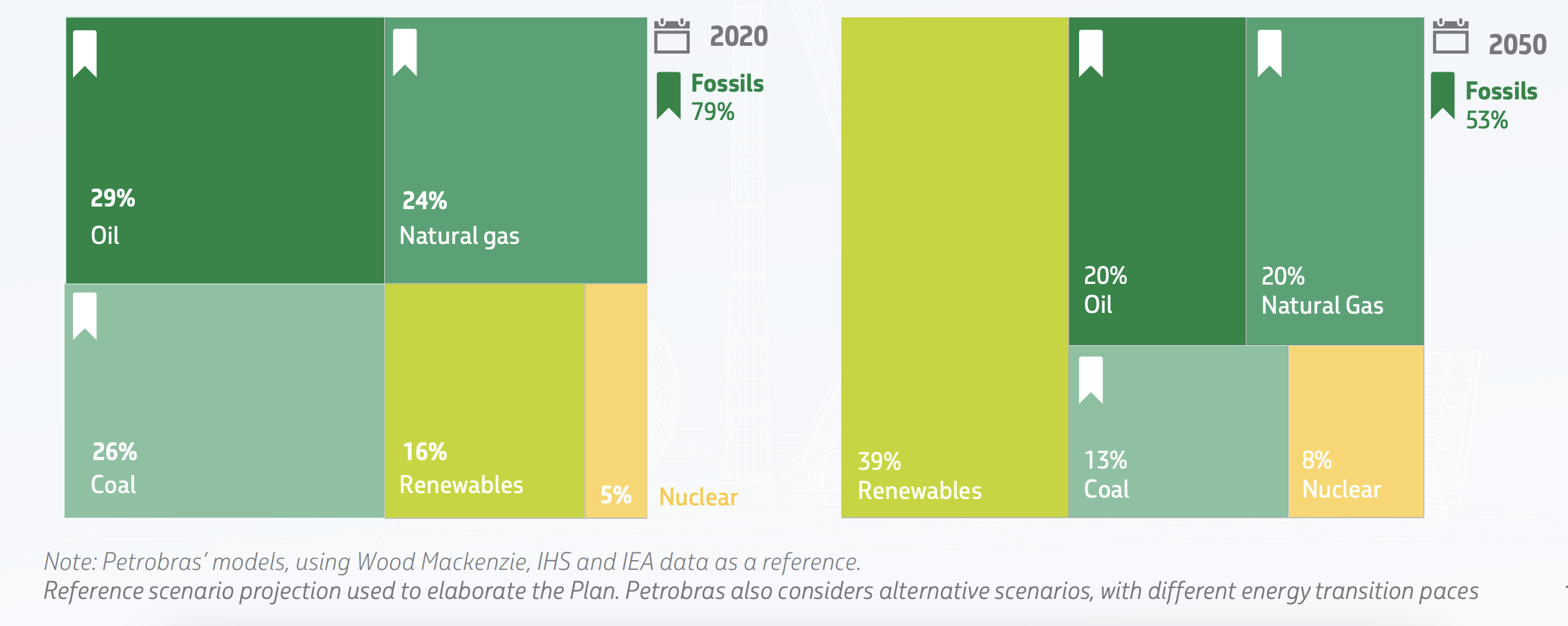

Although it might seem outlandish to expect oil consumption associated with vehicles to drop, this is destined to occur because of the proliferation of electric vehicles. Even as the global vehicle fleet expands from around 1.2 billion vehicles back in 2020 to 2 billion vehicles by 2050, the percentage of those vehicles that will be electric should explode. By 2050, it's estimated that 53.3% of the global fleet of vehicles will be electrified. This, combined with other things moving toward electric, will cause a major shift in demand for different sorts of energy products. For instance, in 2020, only 16% of all energy produced on this planet came from renewable sources. That should balloon to 39% by 2050. Nuclear, meanwhile, should grow from 5% to 8%. On the other hand, we should see oil drop from 29% to 20%, while natural gas drops from 24% to 20% and coal plunges from 26% to 13%.

{kind=link}

It might seem odd, during this window of time, for Petrobras to be investing so heavily into expiration and production activities. But the way I see it and the way that management likely sees it is that current high prices represent one last big hurrah before the eventual decline in demand comes about. And as management revealed in their presentation, the average real internal rate of return on its investments is disproportionately in favor of allocating capital toward these types of initiatives. The IRR for exploration and production investments is about 23%. That's better than the 14% involving refining, transportation, and marketing. And it dwarfs the slightly higher than 8% associated with gas and low carbon energy projects.

{kind=link}

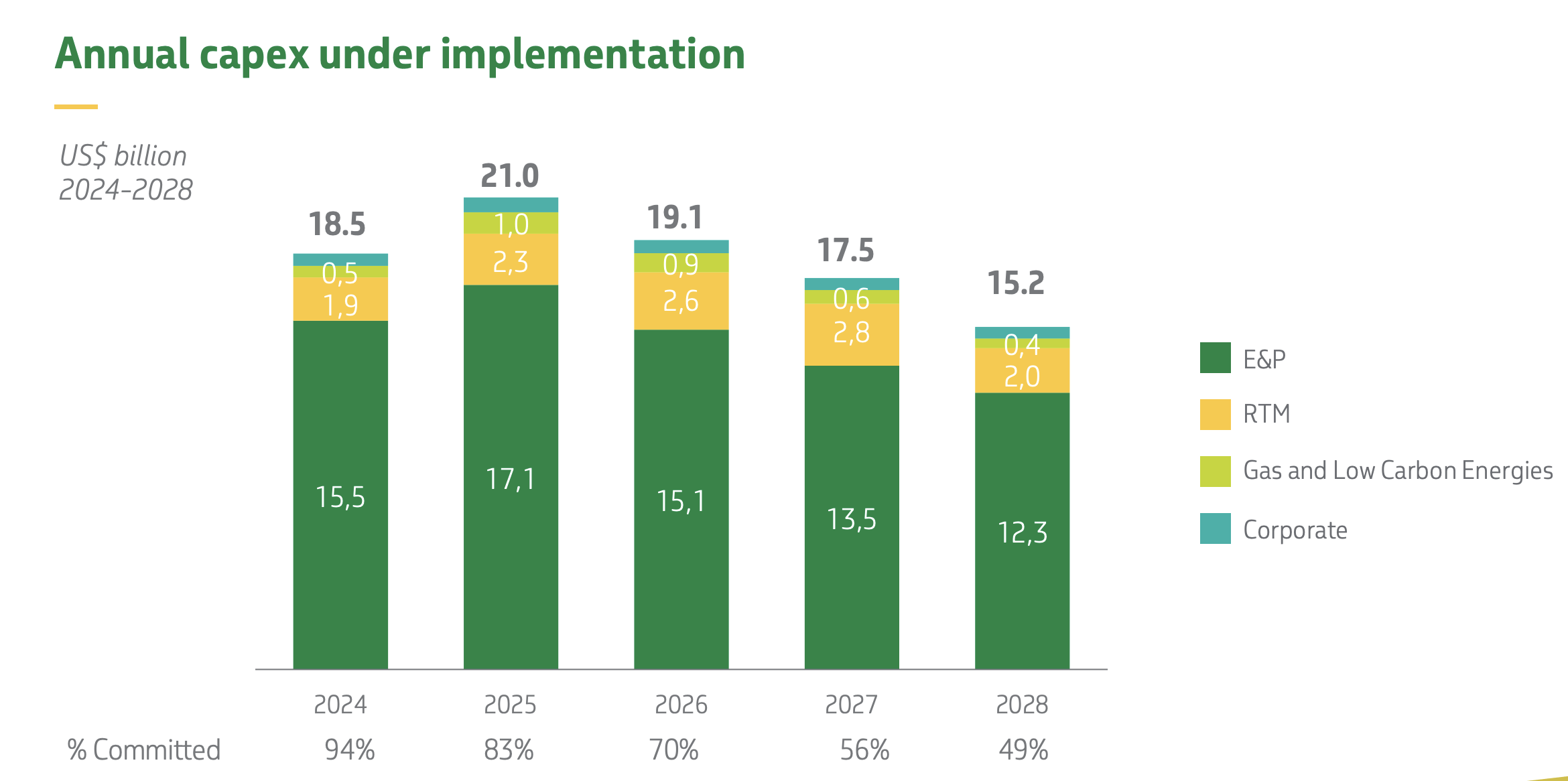

Even though management intends to allocate so much toward exploration and production activities, the amount allocated is expected to decline each year. In 2025, for instance, it's expected for the company to spend a record $21 billion on capital expenditures, with $17.1 billion of that in the form of exploration and production activities. By 2028, total capital expenditures projects should drop to $15.2 billion, with $12.3 billion of that amount in the form of exploration and production activities. Much of this spending would involve significant offshore projects such as the Campos Basin and the Santos Basin. Combined, these two areas offer up an estimated $63 billion worth of investment opportunities. The end result from these investments should be a growth in total daily production for the company from 2.8 million boe (barrels of oil equivalent) per day next year to 3.2 million boe per day in 2028. The vast majority of this output, about 78% in all, would be in the form of oil, with another 9% or so in the form of oil and natural gas commercial output.

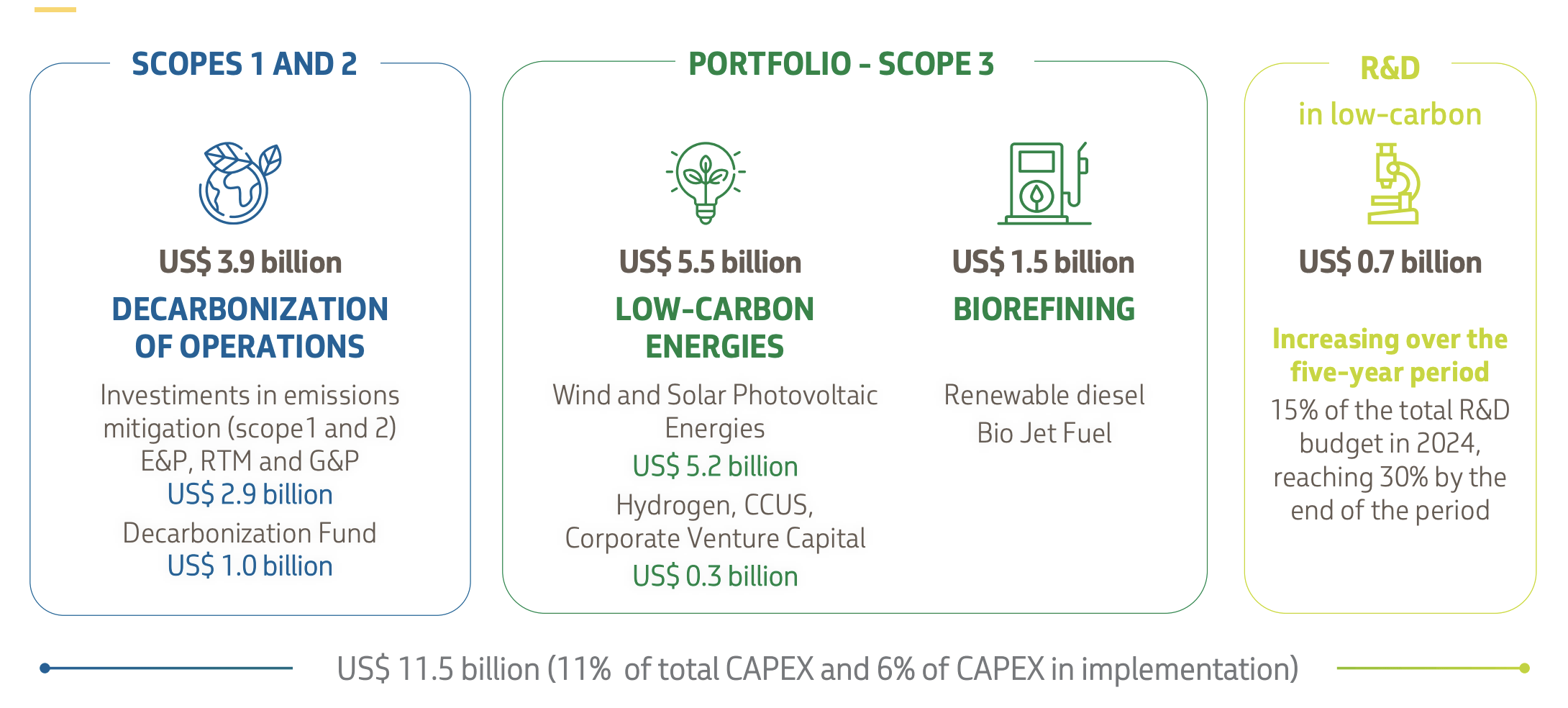

There are other initiatives the company is going to be investing in as well. For instance, around $16.7 billion of its spending between 2024 and 2028 involve refining and logistics operations, with the largest share of this dedicated to refining adaptation and upgrading initiatives. But this doesn't mean that management is not interested in greener technologies. In fact, the company currently plans to spend around $11.5 billion over this five year window of time on various low carbon investments. I have noticed and written about similarly large commitments from other major players such as Exxon Mobil ( XOM ) here and Chevron ( CVX ) here . $5.5 billion of this would involve low carbon renewable energies like wind and solar power, as well as hydrogen, venture capital investments in various prospects, and even carbon capture. This is on top of $1.5 billion that the company wants to invest in biorefining initiatives such as renewable diesel and bio jet fuel. About $3.9 billion of the company's investments will include focusing on reducing carbon emissions from its own operations. And the rest, about $0.7 billion, will involve research and development in low carbon opportunities that are not really defined as of today.

{kind=link}

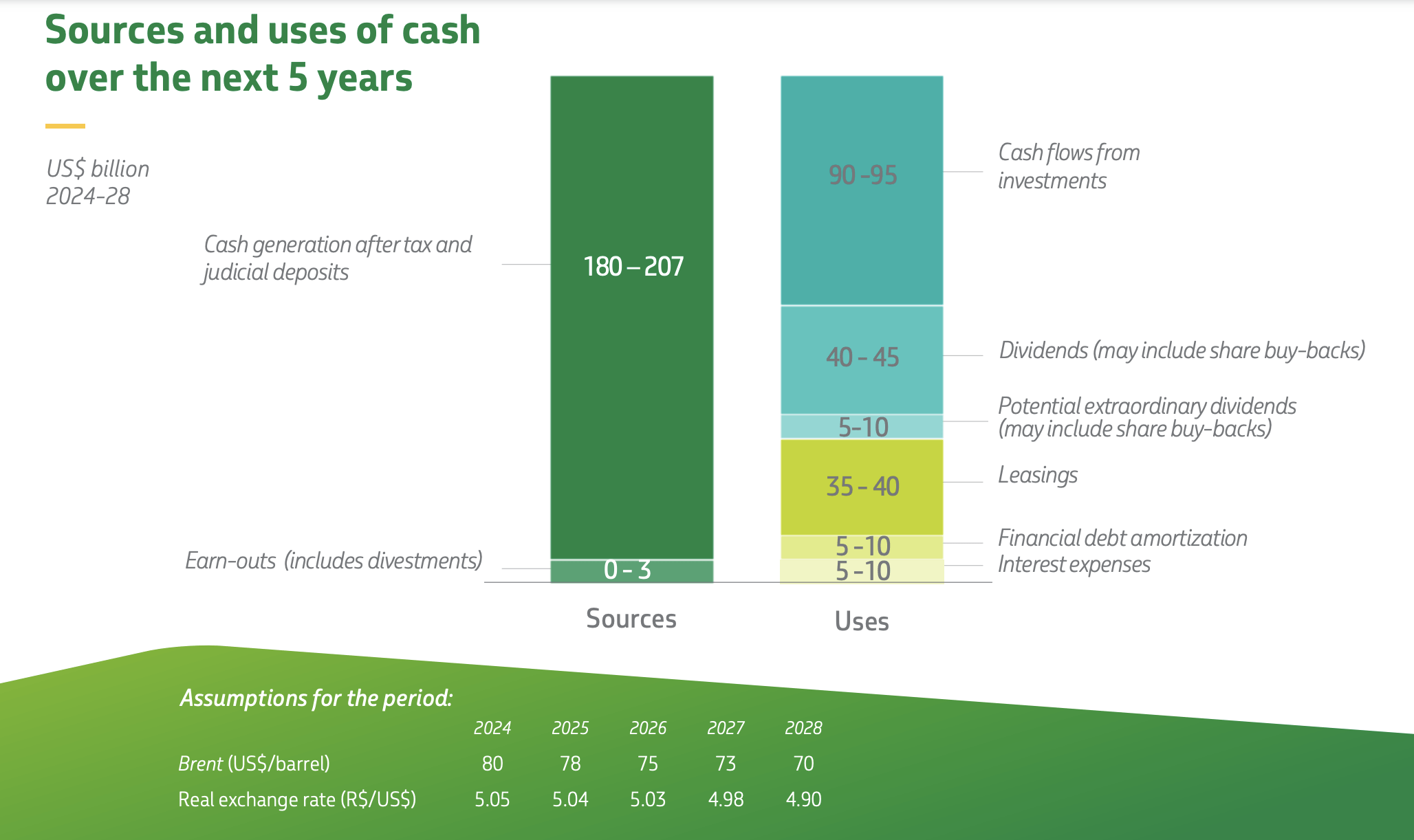

If everything goes according to plan, the company expects to generate between $180 billion and $207 billion from its core operations over the next five years. Between $90 billion and $95 billion of this will go into investments on a net basis. But this won't stop the company from allocating between $45 billion and $55 billion toward a combination of dividends and share buybacks. Generally speaking, I am not a fan of either way of rewarding shareholders. I would prefer capital be allocated toward additional growth initiatives. But given how cheap the stock is, I could imagine share buybacks being a good avenue for management to explore.

{kind=link}

I would encourage those who have doubt in the company's plans to look at just how strong financial performance has been in recent years. From 2020 through 2022, the company has seen its revenue more than double from $53.68 billion to $124.47 billion. Now to be fair, the vast majority of this upside was driven by a surge in Brent crude pricing from $41.67 per barrel to $101.19 per barrel. But even so, energy prices remain elevated and so long as OPEC+ doesn't make any bad decisions, I can't imagine prices dropping much below $70 per barrel for an extended period of time.

{kind=link}

{kind=link}

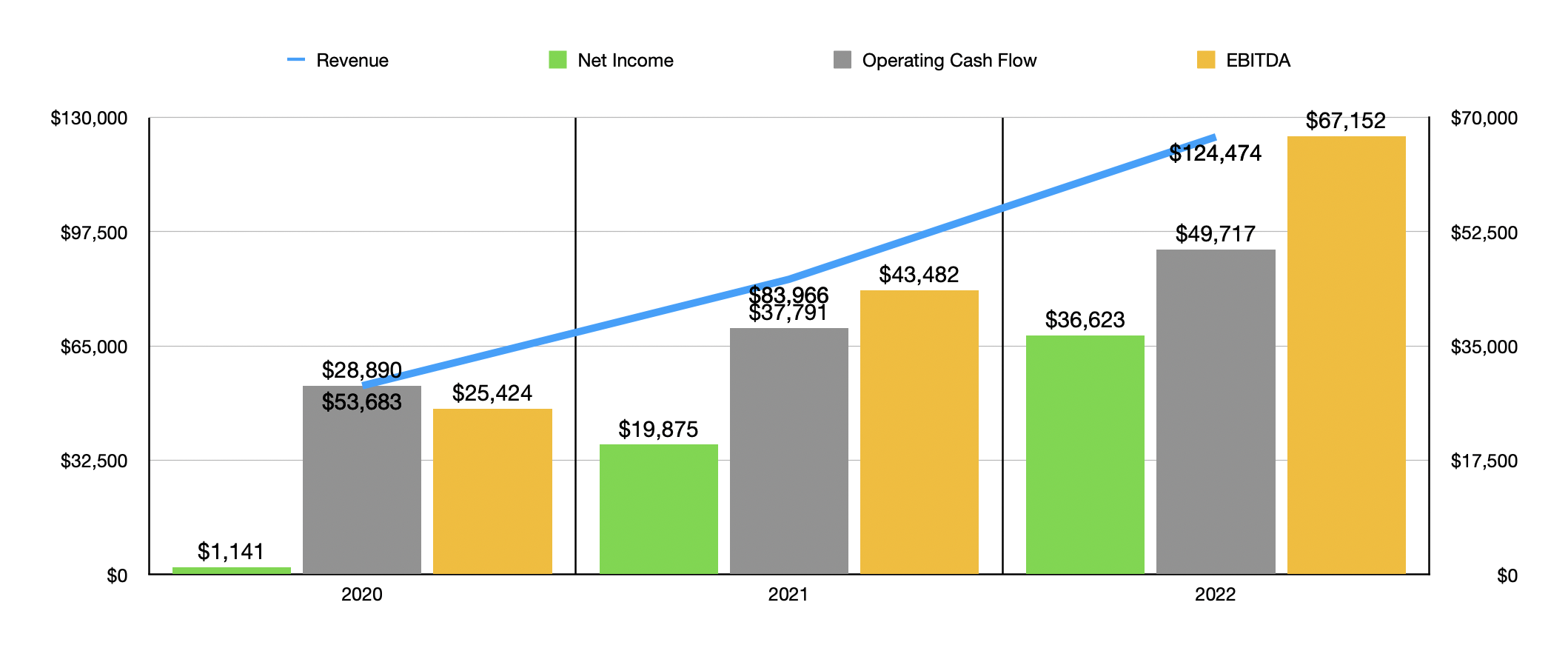

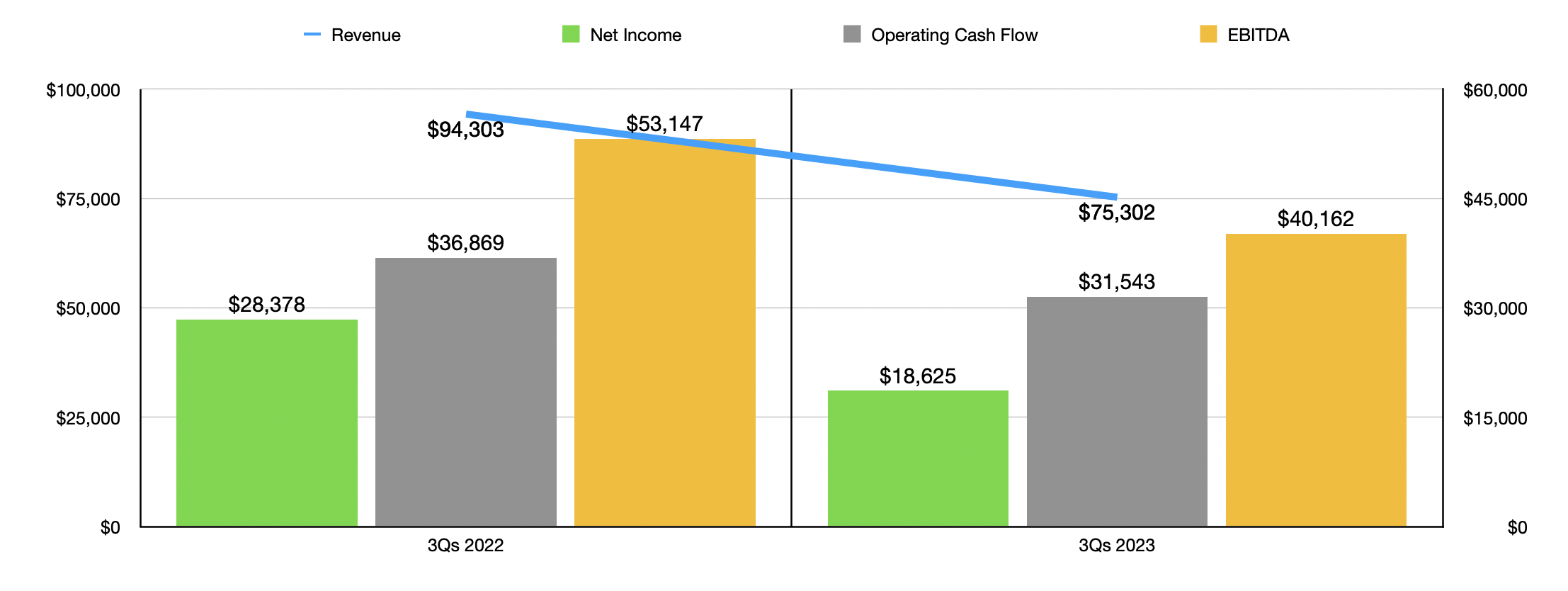

With the rise in revenue also came a surge in profits. The company went from generating $1.14 billion in net income in 2020 to $36.62 billion in 2022. As the first chart above illustrates, cash flow figures for the company also grew nicely during that window of time. Now, to be perfectly clear, this year is looking a bit worse. As you can see in the second chart above, revenue, profits, and cash flows, are all down year over year . This is not surprising to me given the weakness that we have seen in energy pricing. But even so, the cash flows generated so far this year are significant.

{kind=link}

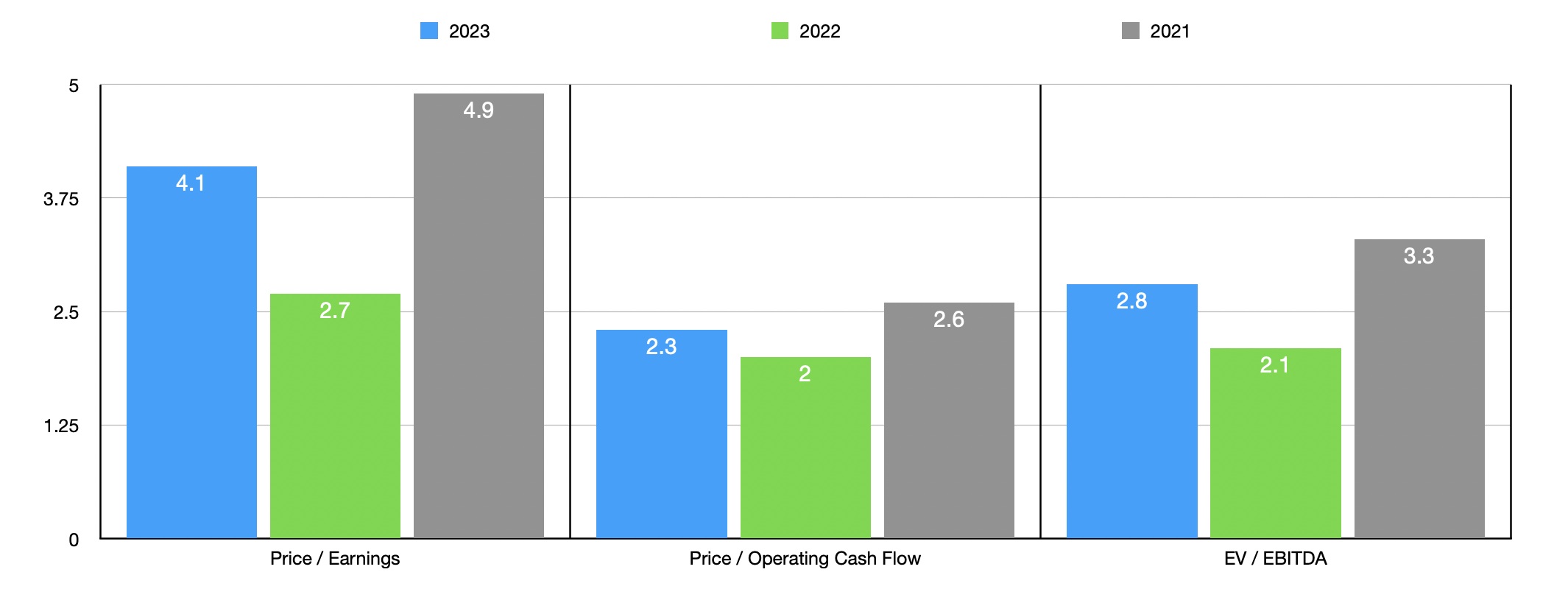

If we annualize the results experienced so far for the first nine months of this year, we would anticipate net income of $24.04 billion for the year. Operating cash flow would come in at around $42.54 billion, while EBITDA would be somewhere around $50.75 billion. Using these figures, I then valued the company as shown in the chart above. Even though financial performance is worse on a forward basis than if we were to use data from last year, the stock is still trading in the low single digit range. As part of my analysis, I also compared the company to five similar firms as shown in the table below. These companies are also quite cheap. But on a price to earnings basis and a price to operating cash flow basis, Petrobras ended up being the cheapest of the group. It's already closer to fair value on a relative basis if we use the EV to EBITDA approach. In that scenario, three of the five companies ended up being cheaper than our prospect.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Petrobras |

| 4.1 |

| 2.3 |

| 2.8 |

| Equinor ASA ( EQNR ) |

| 5.9 |

| 3.8 |

| 1.6 |

| BP p.l.c. ( BP ) |

| 4.3 |

| 3.0 |

| 2.3 |

| Eni S.p.A. ( E ) |

| 9.9 |

| 3.2 |

| 2.3 |

| Occidental Petroleum ( OXY ) |

| 13.1 |

| 4.5 |

| 5.2 |

| Suncor Energy ( SU ) |

| 7.1 |

| 4.7 |

| 3.7 |

Takeaway

Based on the data provided, Petrobras is doing quite well for itself. This initiative launched by management is definitely encouraging, though we will have to see if energy prices stick in the appropriate range to make this happen. In the grand scheme of things, shares of the business are attractively priced and it is refreshing to see investments made in initiatives that will allow the firm to generate returns in the distant future. Personally, I would prefer more of an emphasis on those investments and less on dividends. But with how cheap the stock is, that does not stop me from rating the company a ‘buy’

For further details see:

A Transformative Change For Petrobras Warrants Strong Upside