REIT - A Wall Of Worry

2023-05-21 09:00:00 ET

Summary

- U.S. equity markets climbed to nine-month highs this week as investors weighed signs of progress on debt-ceiling negotiations and solid economic data against a continued drumbeat of hawkish Fed commentary.

- Snapping a two-week losing streak and climbing to its highest levels since August, the S&P 500 advanced 1.7% while the tech-heavy Nasdaq 100 rallied 3.5% to fresh 52-week highs.

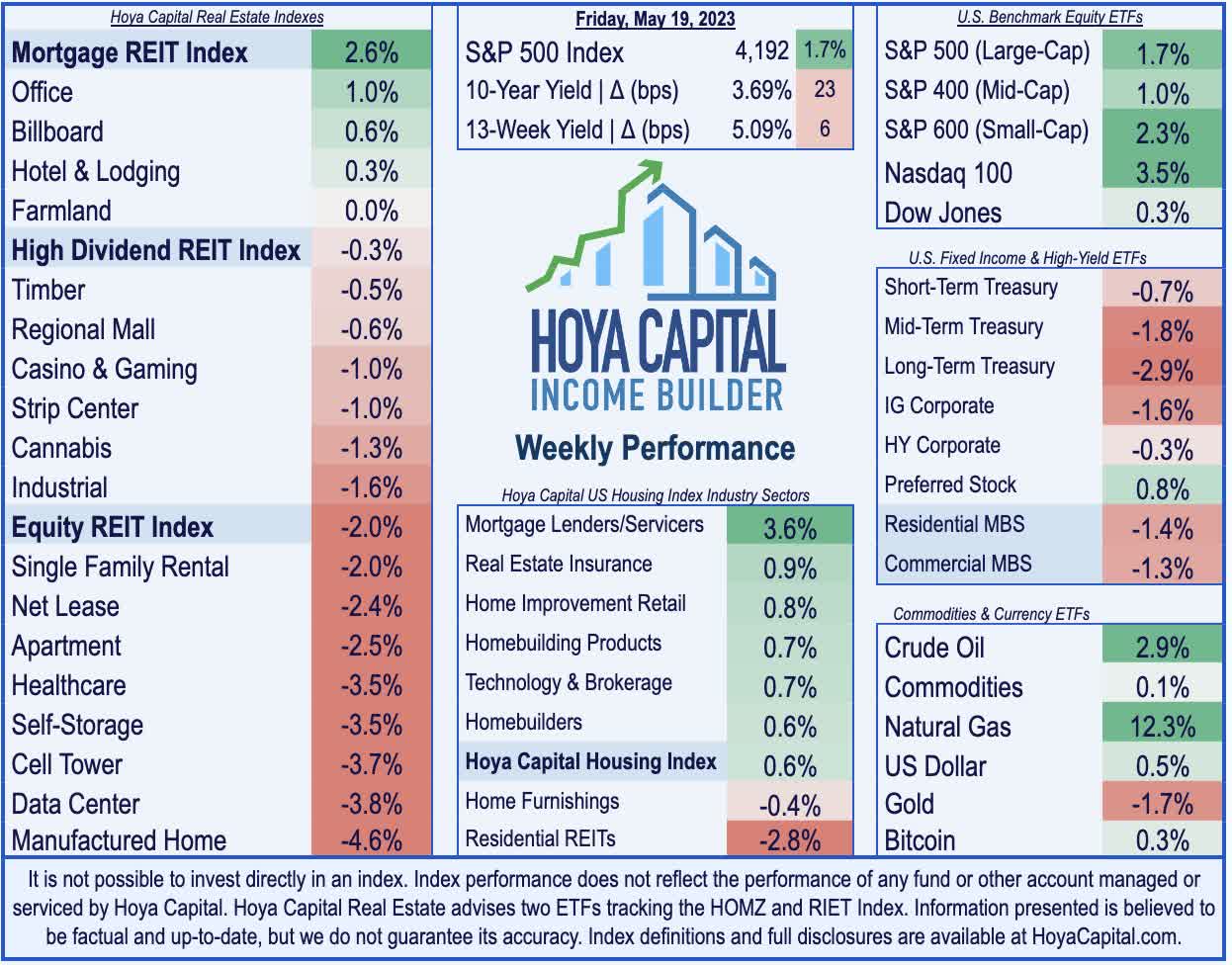

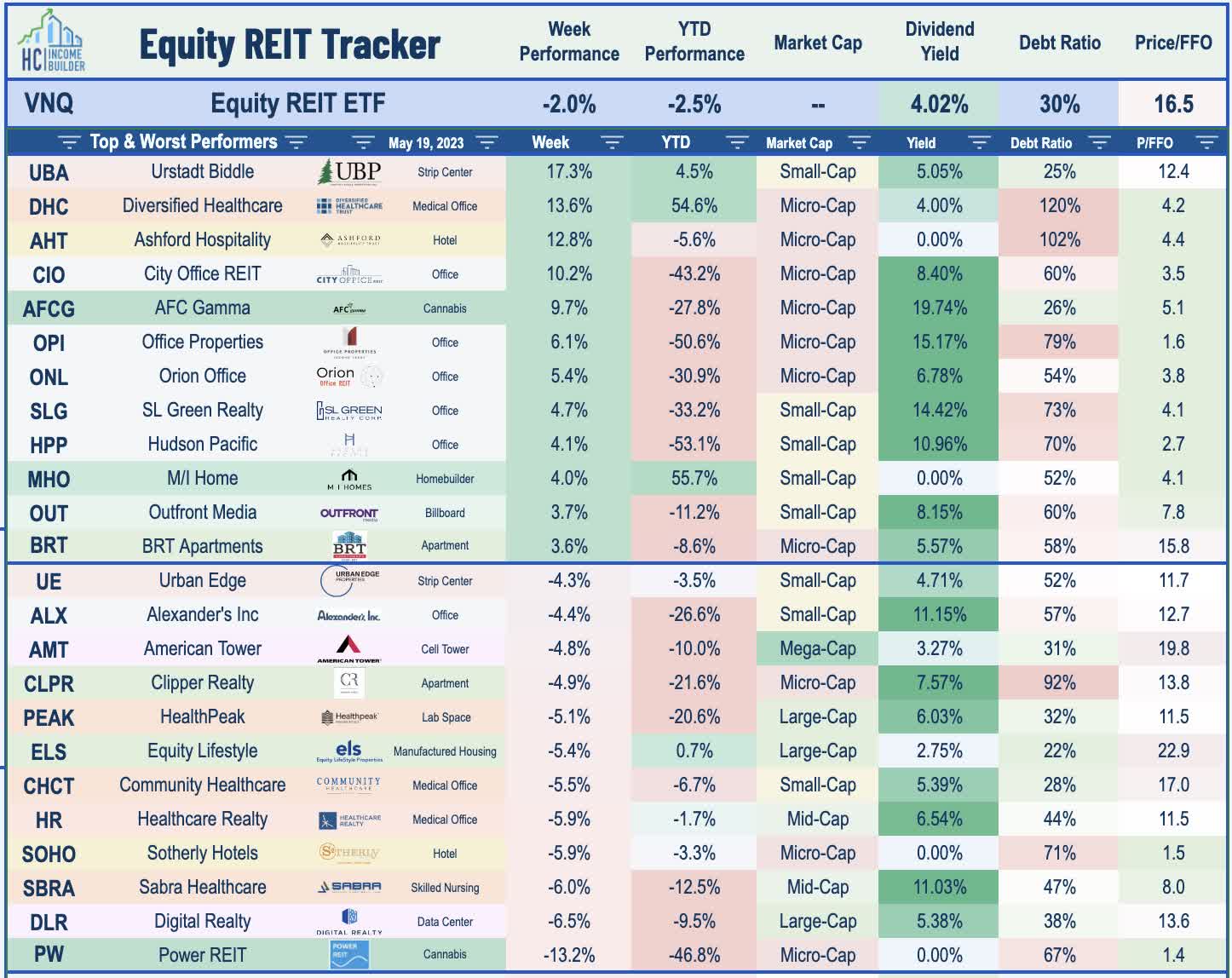

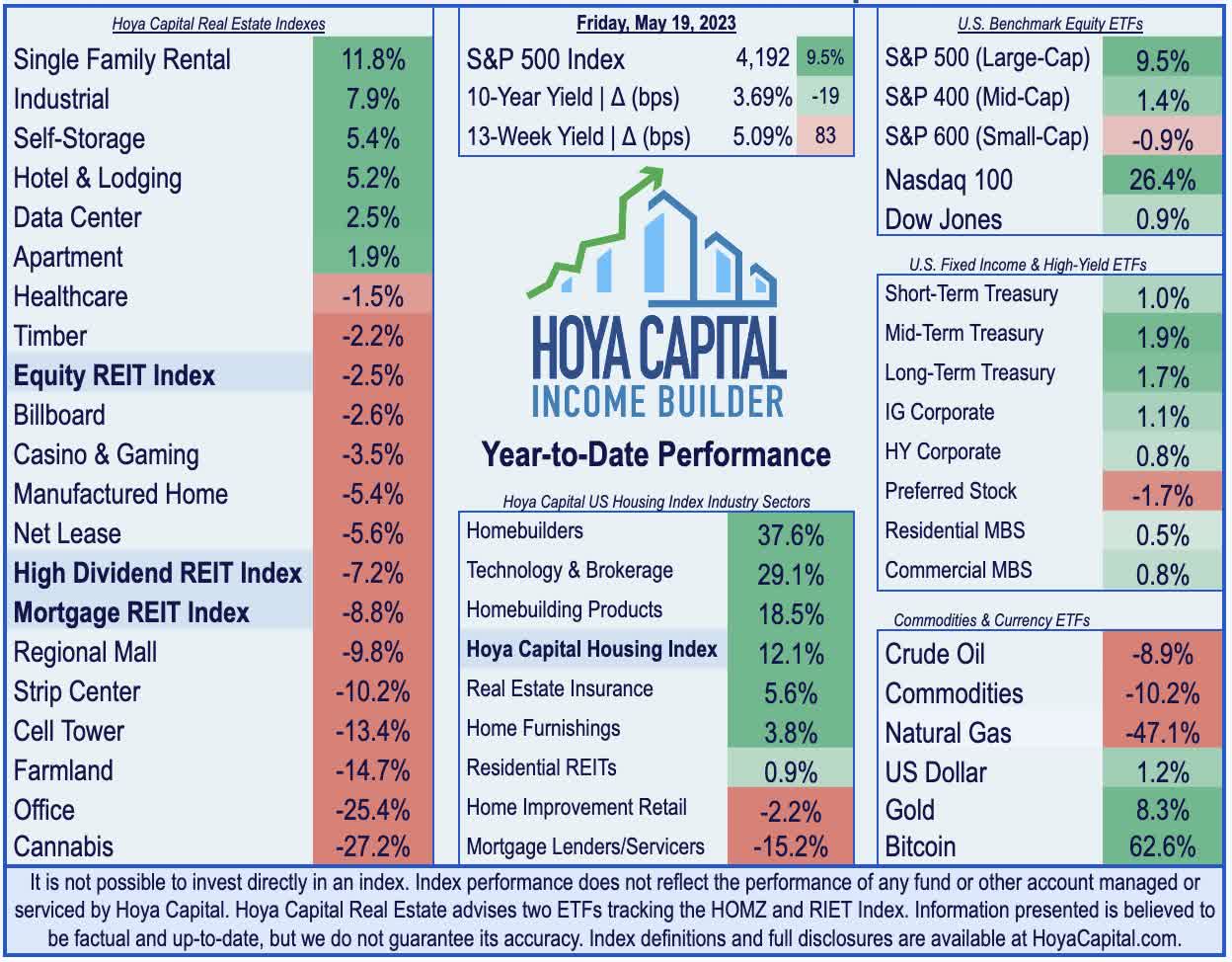

- Real estate equities were laggards this week, pressured by a rebound in benchmark interest rates. The Equity REIT Index dipped 2.0% but Office and Mortgage REITs were among the leaders.

- Homebuilders and the broader Housing Index continued their strong start to 2023 on data indicating that the housing industry is beginning to emerge from its nearly two-year-long recession.

- A flurry of M&A and dealmaking was the theme this week in the REIT space amid a historically slow year of commercial real estate transaction activity. Regency Centers announced a $1.4B deal to acquire Urstadt Biddle Properties. Both Casino REITs also announced major deals.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on May 19th.

U.S. equity markets climbed to nine-month highs this week as investors weighed signs of progress on debt-ceiling negotiations and solid economic data against a continued drumbeat of hawkish central bank commentary. The rebound came despite a surge in benchmark interest rates, which rose to their highest level since March as Fed officials across a dozen public appearances pushed back on calls for a pivot towards less-aggressive monetary tightening.

{kind=link}

Snapping a two-week losing streak and climbing to its highest levels since August, the S&P 500 advanced 1.7% while the tech-heavy Nasdaq 100 rallied 3.5% to fresh 52-week highs. Real estate equities were laggards this week, however, pressured by the rebound in benchmark interest rates. The Equity REIT Index dipped 2.0% this week, with 13-of-18 property sectors in negative territory, but the Mortgage REIT Index rallied nearly 3%. Homebuilders and the broader Housing Index continued their strong start to 2023 on data indicating that the housing industry is beginning to emerge from its nearly two-year-long recession while housing supply levels remain near historic lows despite a myriad of recent demand headwinds.

{kind=link}

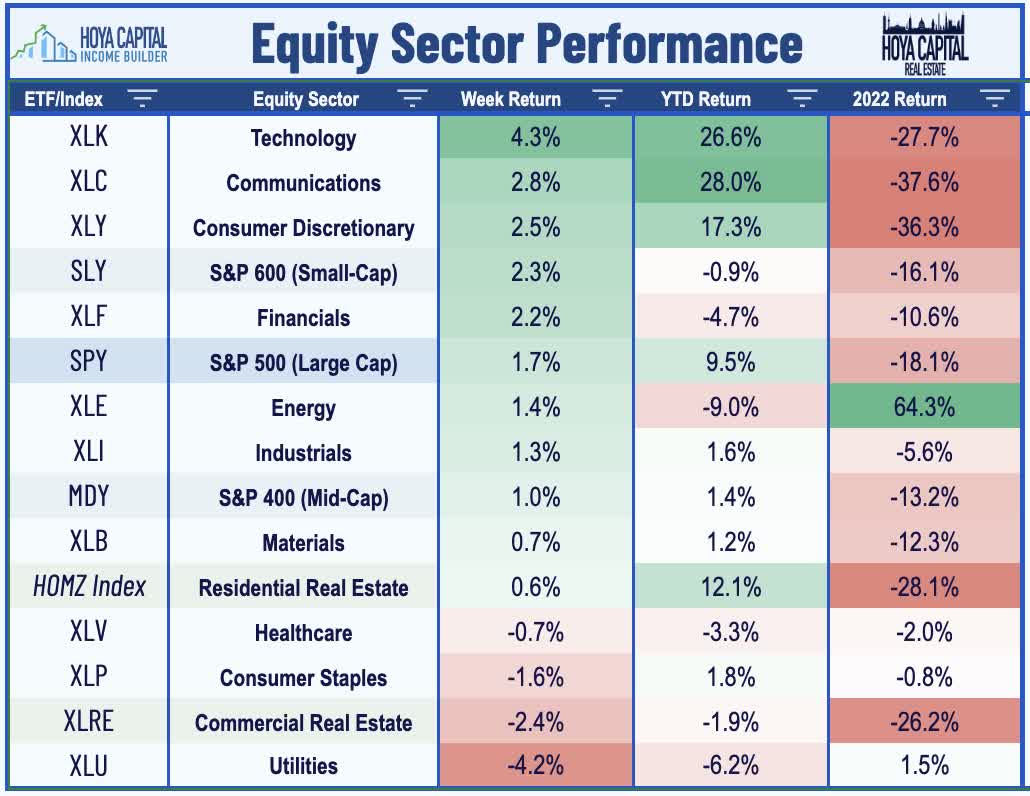

Bonds traded lower this week across the credit and maturity curve, as decent economic data revived the drumbeat for another Fed rate hike in June. Swaps markets now imply a 20% chance of a June hike - down from the mid-week high of over 40% - but up from less than 1% a week ago. The policy-sensitive 2-Year Treasury Yield surged 27 basis points this week to 4.27%, while the 10-Year Yield rose 23 basis points to 3.69% - each at their highest levels since the Silicon Valley Bank collapse in early March. The U.S. dollar, meanwhile, climbed to five-week highs, buoyed by optimism that a debt ceiling deal between Republican and Democrat negotiators will be reached before the June 1 deadline. Six of the eleven GICS equity sectors traded higher on the week, with Technology ( XLK ) and Financials ( XLF ) stocks among the leaders. Regional bank stocks were particularly strong after Western Alliance ( WAL ) - which has dipped more than 40% this year - provided a positive update on deposit growth, calming some concerns that the lender could be the next major bank failure following three major collapses since early March.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

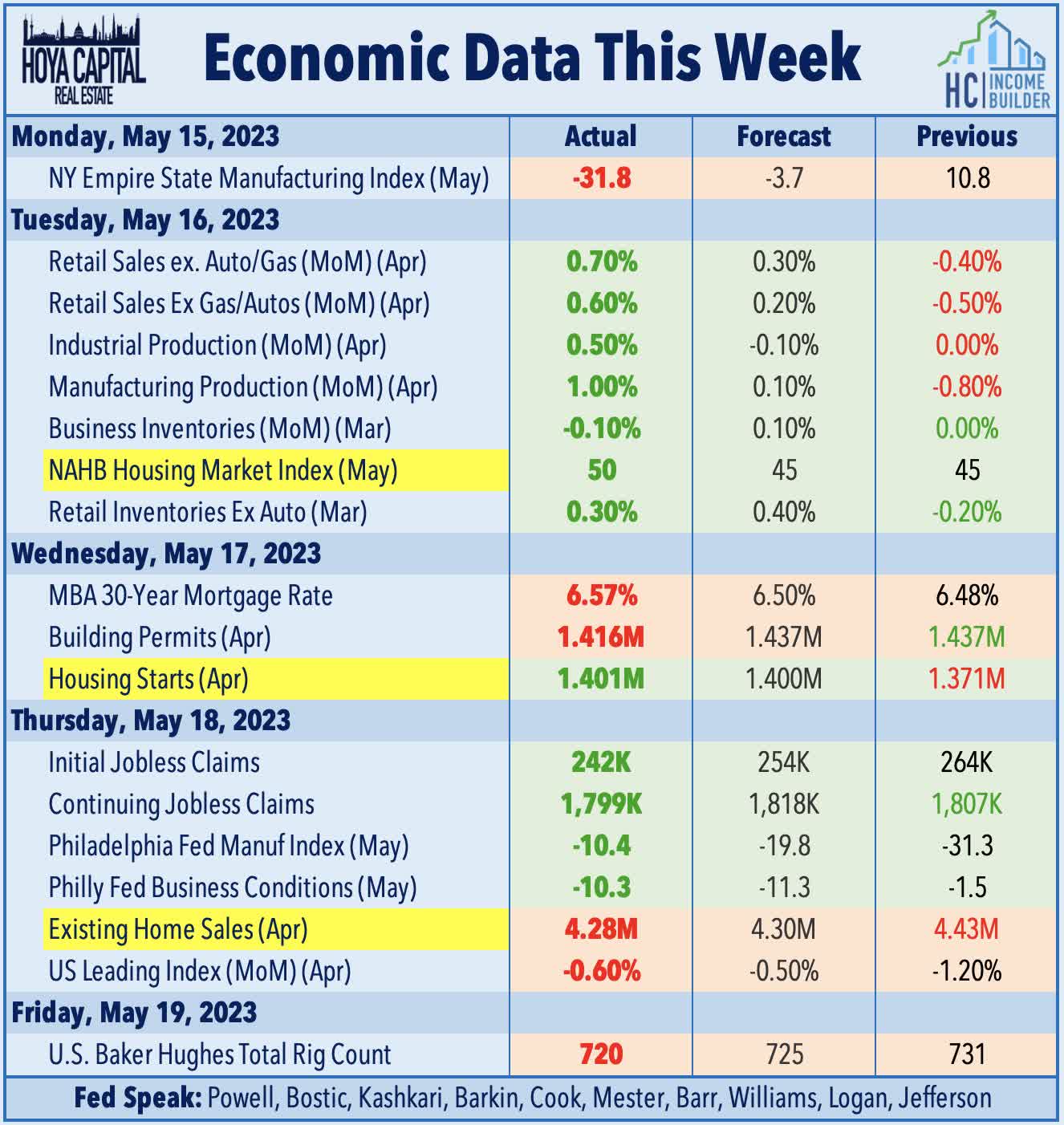

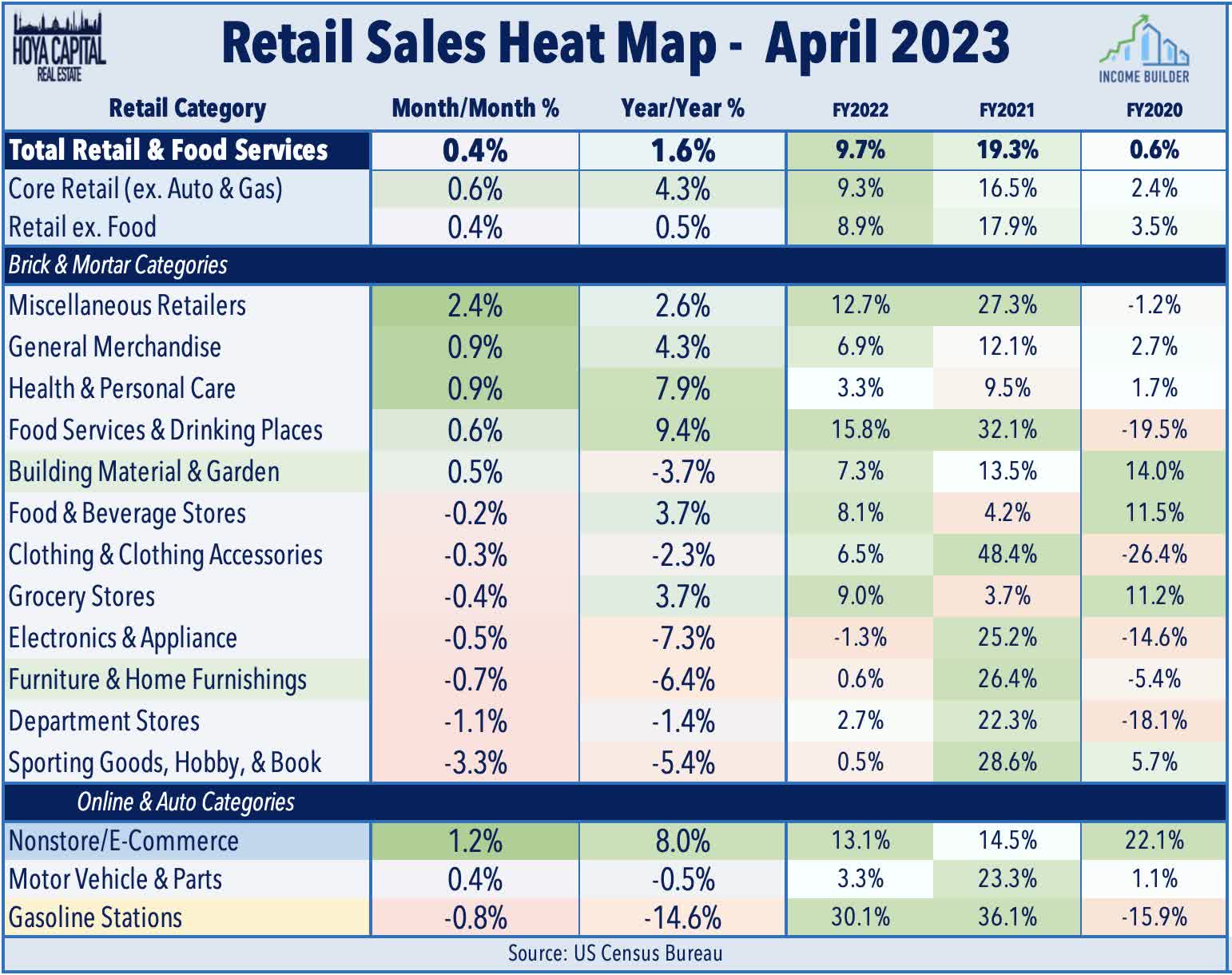

Retail sales data this week provided mixed signals on the state of the U.S. consumer, showing that spending rose at a weaker-than-expected pace in April, but the "miss" was largely driven by reduced spending at gasoline stations. The value of retail purchases rose 0.4% after an upwardly revised 0.7% decrease in March, which was below consensus estimates of 0.8%. Excluding autos and gasoline, however, retail sales increased 0.6%, which was above estimates of 0.2%. Seven out of 13 retail categories rose last month, including advances at general merchandise outlets and online merchants. Total retail sales are now higher by just 0.5% from last year, which is the slowest annual growth rate since the pandemic declines in April and May 2020. As these figures aren’t adjusted for inflation, "real" retail spending is lower by 4.5% from last year after adjustment using the headline CPI Index.

{kind=link}

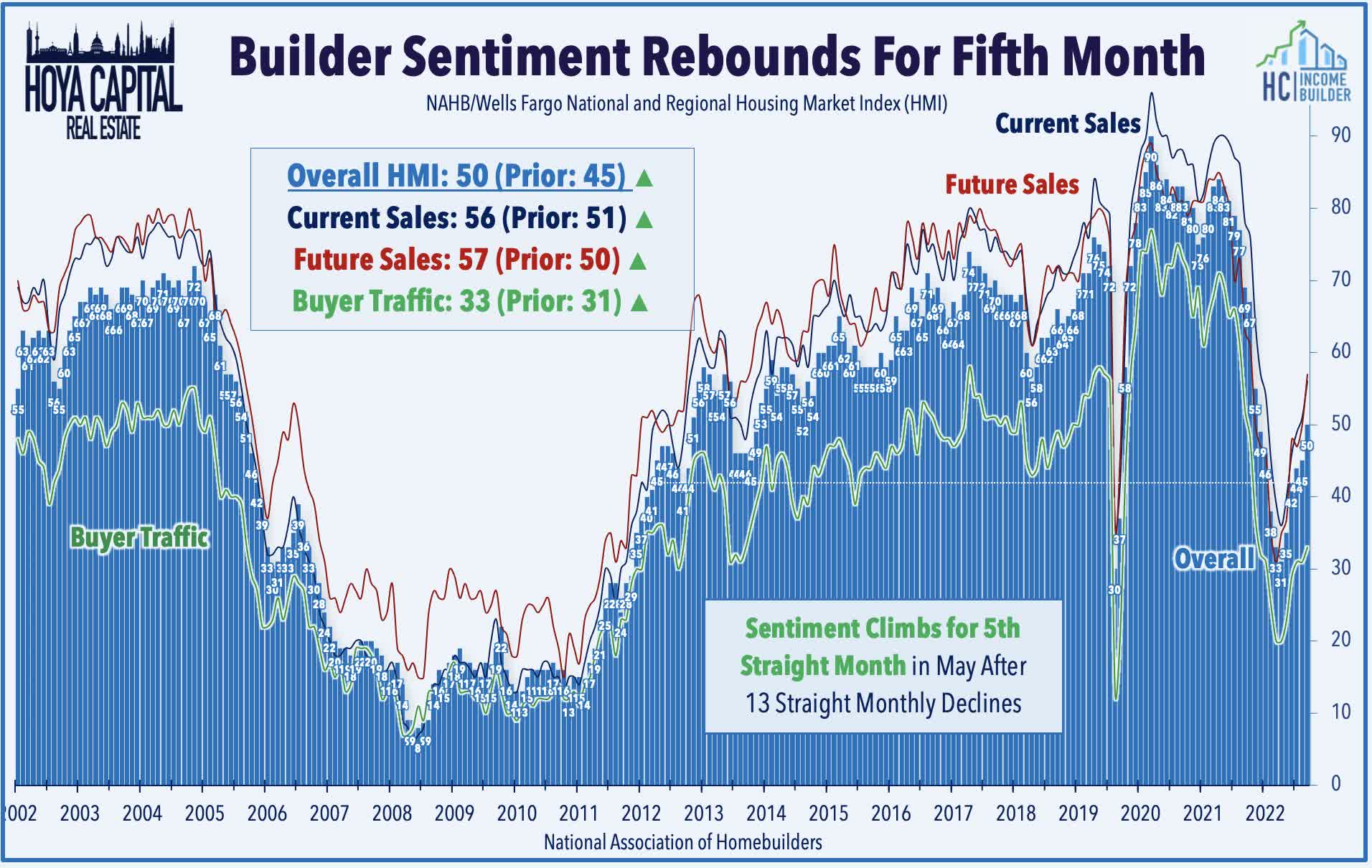

Consistent with the countercyclical performance trends it exhibited early in the pandemic, the previously-sluggish U.S. housing sector has again emerged as a bright spot in recent months. Data this week showed that NAHB Homebuilder Sentiment - a leading indicator of housing market activity - rose for a fifth-straight month in May, which follows a stretch of thirteen straight monthly declines. Rising to 50 on the headline index with gains in the current sales and future sales sub-indexes, builders attributed improving sentiment to low inventory levels and a moderation in mortgage rates. Measures of current sales and sales expectations rose to the highest level since the summer. A gauge of prospective buyer traffic also edged up to a 10-month high.

{kind=link}

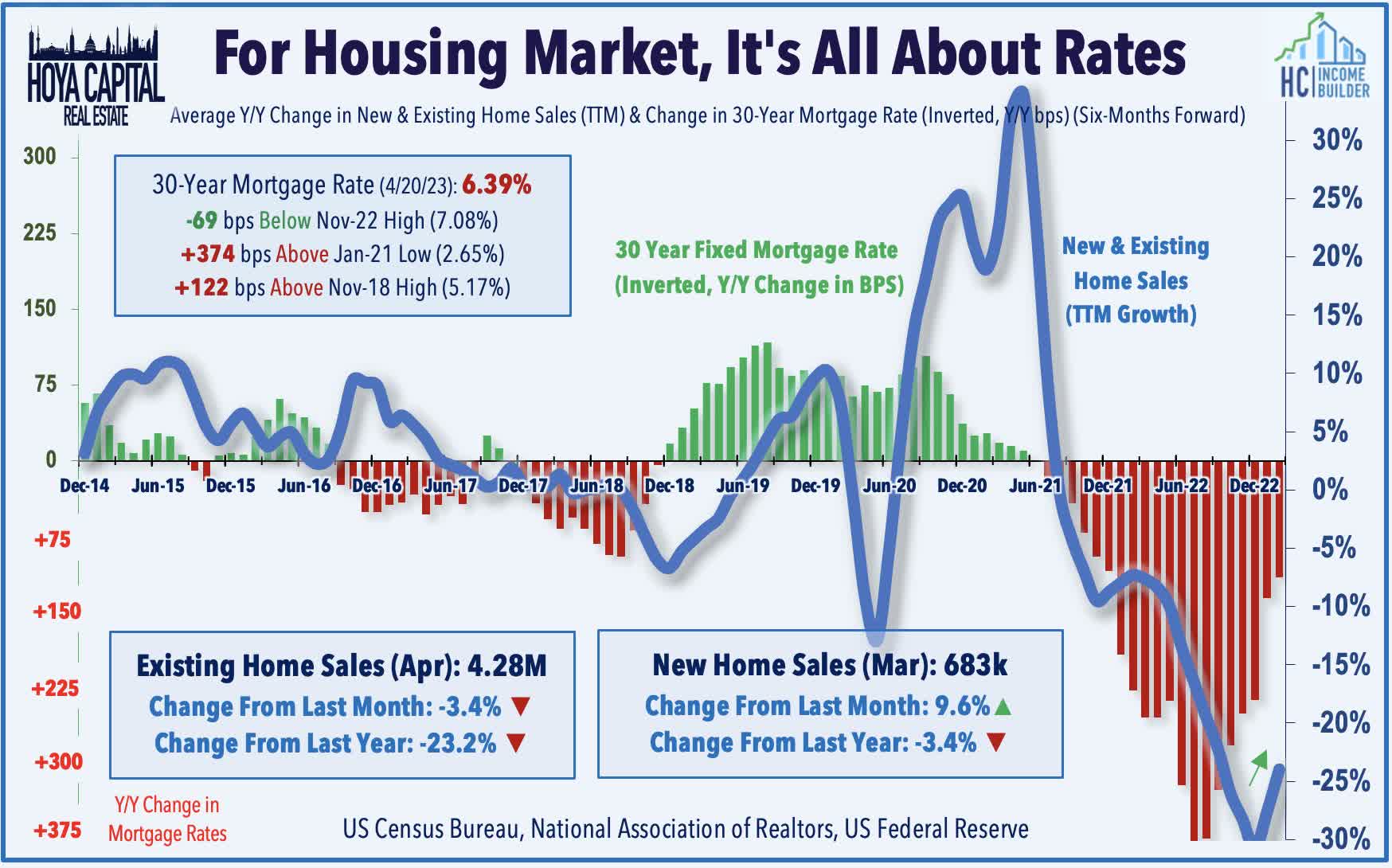

Existing Home Sales data this week, meanwhile, showed that sales of previously-owned homes declined slightly in April from the prior month, but historically low inventory levels were the primary culprit behind the weakness. Despite headwinds on demand resulting from elevated mortgage rates, potential homebuyers are facing an increasingly competitive market, with properties selling in an average of 22 days in April - down from 29 days in March. Nearly three-quarters of homes were on the market for less than a month. There was good news for potential homebuyers, however, as home prices declined 1.7% in April - the steepest price decline in more than a decade - following double-digit annual gains in home prices in 2021 and 2022.

{kind=link}

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

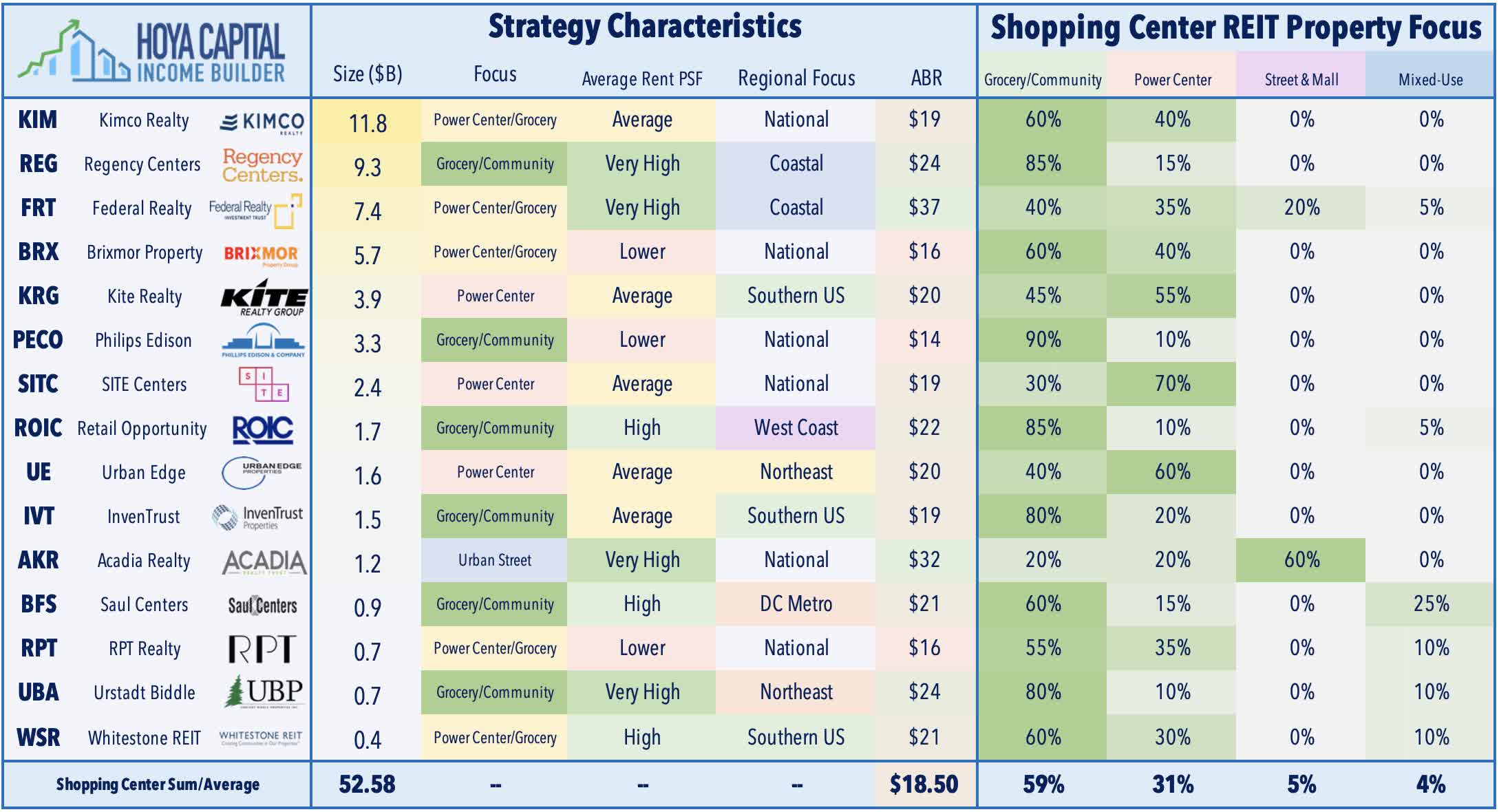

Strip Center : A flurry of M&A and dealmaking was the theme this week in the REIT space amid a historically slow year of commercial real estate transaction activity. Regency Centers ( REG ) - the second largest strip center REIT - announced a $1.4B all-stock deal to acquire Urstadt Biddle Properties ( UBP ) at $20.40/share, a roughly 33% premium to UBP's prior closing price. Urstadt Biddle is a small-cap grocery-focused REIT that owns 77 retail properties concentrated around suburban New York City - of which roughly 85% are grocery-anchored - with the highest average base rent among the pure-play strip center REITs. The combined company - which will have a pro forma equity market capitalization of roughly $11 billion and a total enterprise value of $16 billion - will be comprised of 481 total properties encompassing 56 million square feet of gross leasable area. The transaction is expected to close late by Q4. Regency expects the deal to be immediately accretive to Operating Earnings. Regency has arguably the strongest balance sheet of any retail REIT with a Debt Ratio below 30% - (only UBP has a lower debt ratio at 25%) and trades with the highest P/FFO valuations in the sector - two attributes that put the company in the "drivers-seat" for opportunistic acquisitions.

{kind=link}

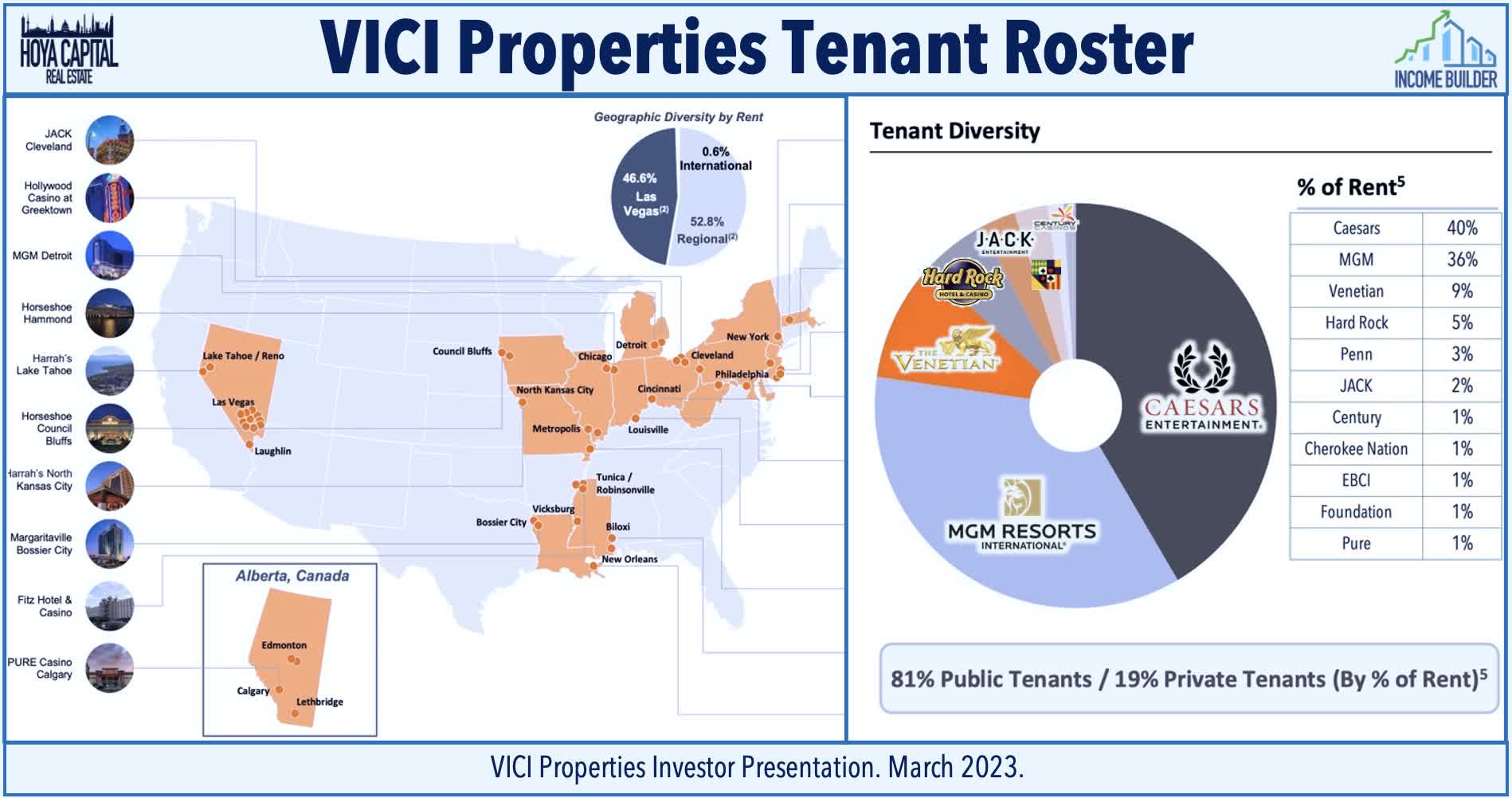

Casino : The most active property sector on the external growth front in recent quarters, both casino REITs announced deals this week. VICI Properties ( VICI ) traded roughly flat this week after it announced that it will acquire the real estate assets of four casinos in Canada from Century Casinos ( CNTY ) for $165M in cash, representing an implied acquisition cap rate of 7.8%. The four casinos are Century Casino Edmonton, Century Casino St. Albert, Century Mile Casino, and Century Downs Casino. The deal is the second major portfolio acquisition in Canada for VICI, following a $202M deal to acquire four casinos from PURE Entertainment in January. The Century Canadian Portfolio will be added to the existing triple-net master lease agreement between VICI and Century with an additional annual rent of $12.8 million. The transaction is expected to close in the second half of 2023.

{kind=link}

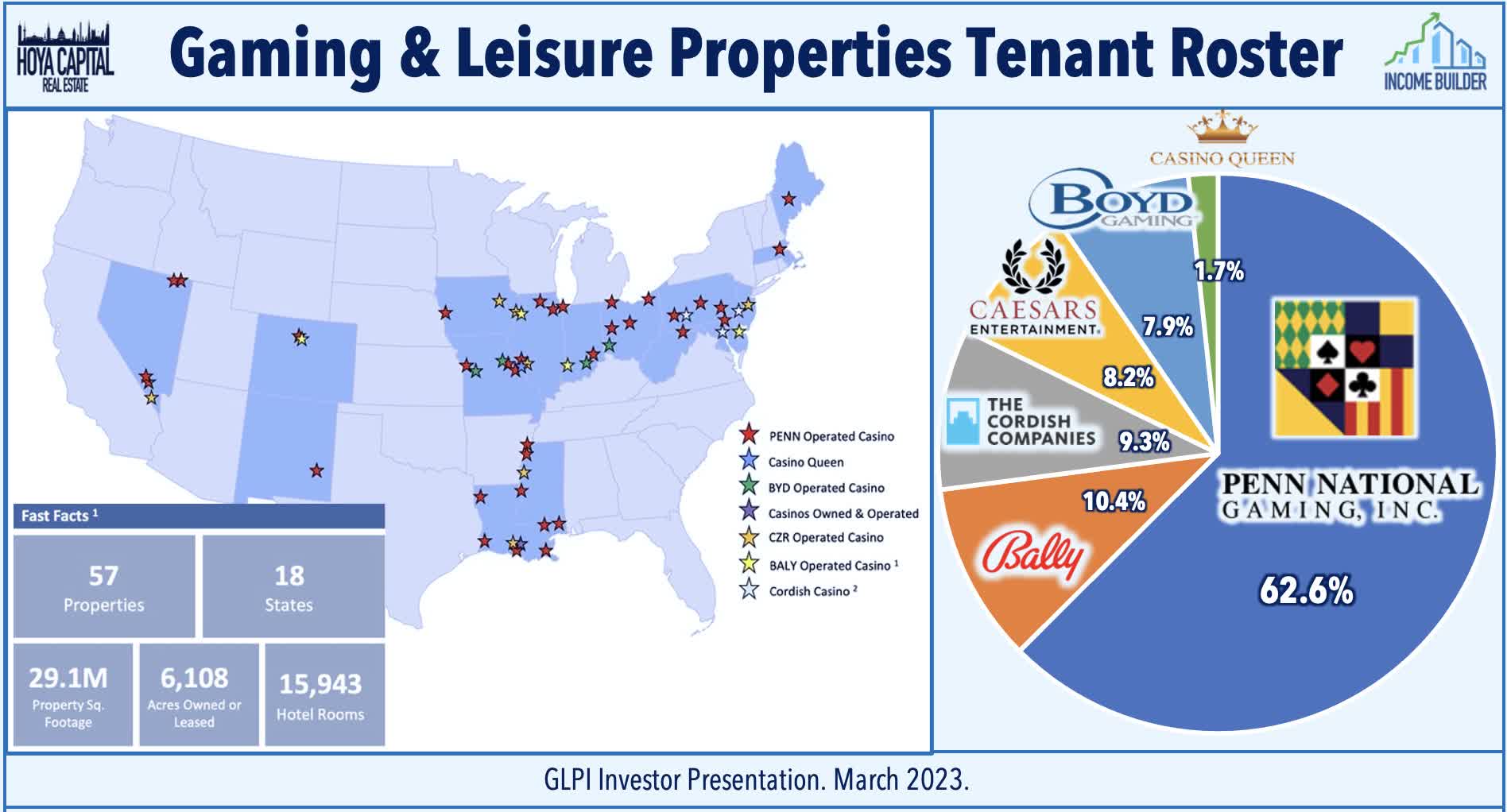

Gaming & Leisure Properties ( GLPI ) reached a binding agreement with the Oakland Athletics to site their new ballpark on a portion of the current Tropicana Las Vegas hotel-casino property. Under the terms of the deal, Bally's ( BALY ) and GLPI will assign approximately nine acres of the 35-acre site located on Las Vegas Boulevard and Tropicana Avenue to the Oakland Athletics. GLPI has agreed to fund up to $175M towards certain shared improvements within the future development in exchange for a commensurate rent increase. The new ballpark will accommodate approximately 30K fans. The agreement is still subject to the passing of legislation for public financing and approval of relocation by Major League Baseball. Nevada state legislators will decide as early as this week if $395M in public assistance will go toward building the baseball stadium. As part of the agreement struck, Bally's retains the ability to assign the rights to all aspects of the development. If built, the ballpark is expected to welcome more than 2.5M fans and visitors annually.

{kind=link}

Office : Providing some hope that long-depressed office utilization rates may recover as labor market conditions loosen, Office REITs were the top-performers this week, buoyed by several new "return to the office" mandates from major corporations including BlackRock ( BLK ) and AT&T ( T ), This week, we published Office REITs: Just How Bad Is It? The new pariah of the commercial real estate sector, Office REITs have plunged nearly 70% over the past eighteen months. Just how bad is it? The surge in interest rates has turned a weak-but-manageable situation into a bleak one, but there is more nuance than the prevailing narrative would suggest. Debt service expenses have been the primary culprit behind the wave of recent loan defaults from private equity firms Brookfield, Blackstone, and Pimco. Much like the e-commerce impact on malls, supply/demand conditions will eventually normalize as properties get repurposed or outright abandoned. We remain bearish on coastal REITs with transit-heavy commutes - the new "Class C/D malls" - but we're calling a bottom for the handful of Sunbelt-focused REITs.

{kind=link}

Sticking with the M&A theme and in more somber news, Sam Zell - a titan of the U.S. real estate industry and one of the pioneers of the 'Modern REIT Era' - died this week at 81 from complications from a recent illness. The legendary real estate investor founded Equity Group Investments, which ultimately formed several of the most highly respected public REITs, including apartment REIT Equity Residential ( EQR ), manufactured housing REIT Equity LifeStyle ( ELS ), and office REIT Equity Commonwealth ( EQC ), which Zell was serving as Chairman until his death. Zell also founded Equity Office Properties Trust, the largest office REIT until its 2007 sale for $39 billion to Blackstone ( BX ) - one of several well-timed deals that earned his reputation as an industry visionary. Arguably his most important contributions to the industry came through his austere approach to corporate governance and emphasis on operating and overhead efficiency, which helped to transform the reputation of the REIT industry from an 'executive-first' structure often riddled with conflicts into a far more 'shareholder-first' governance structure.

{kind=link}

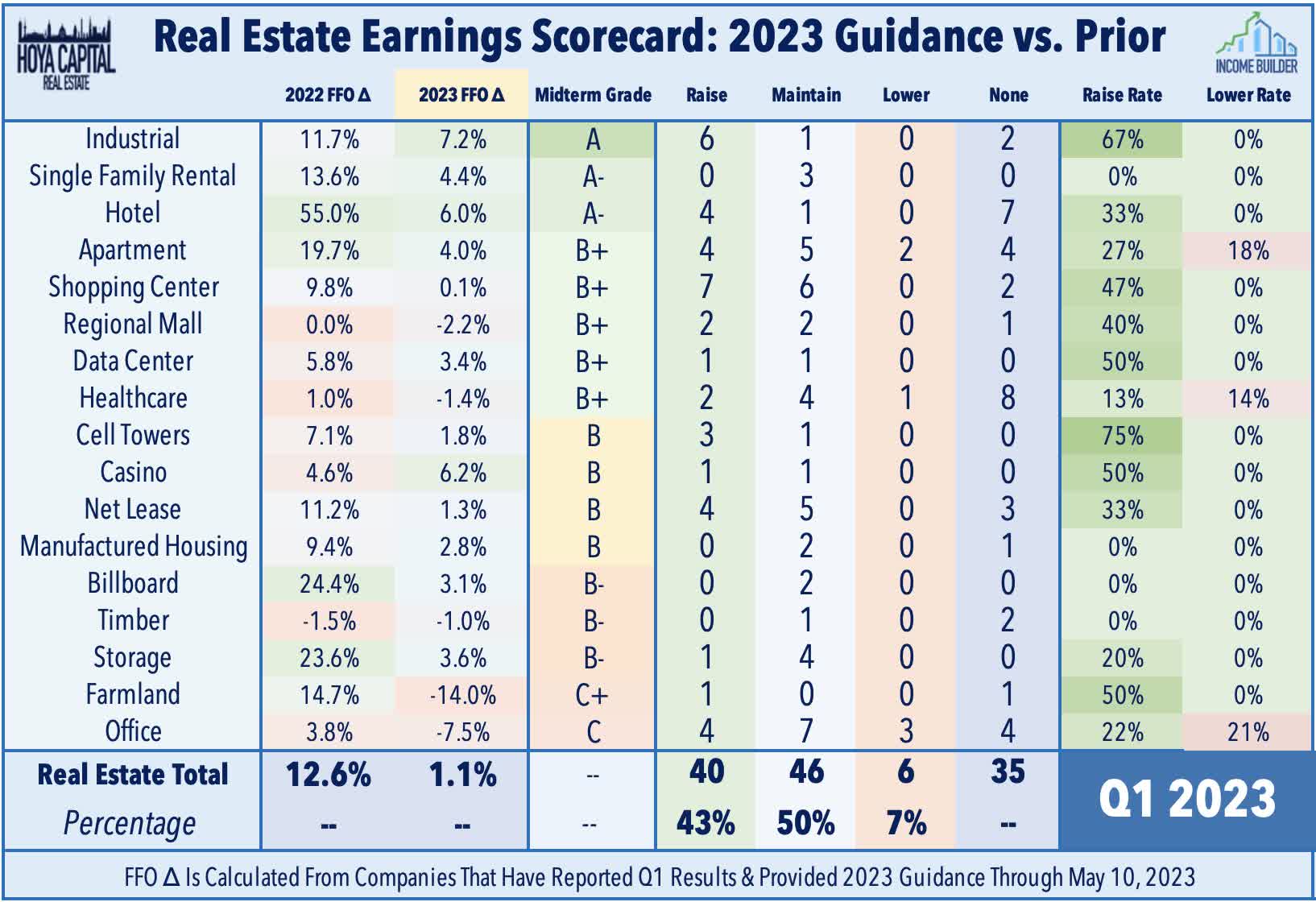

REIT earnings season wrapped up last week with the final two dozen reports, which we discussed in our two-part Earnings Recap series - Winners of REIT Earnings Season and Losers of REIT Earnings Season. Obscured by continued office pain, REITs delivered surprisingly strong first-quarter results. Of the 92 equity REITs that provide full-year Funds from Operations ("FFO") guidance, 40 (43%) raised their full-year earnings outlook, while 6 (7%) lowered guidance - an FFO beat rate that exceeded the historical REIT average of 40% for the first quarter. The "beat rate" for the critical property-level metric - same-store Net Operating Income ("NOI") - was actually slightly better, with over 50% of REITs providing upward revisions. Surprisingly buoyant rent growth - particularly across the residential, industrial, hospitality, technology, and retail sectors - was the prevailing theme of these upward revisions.

{kind=link}

Mortgage REIT Week In Review

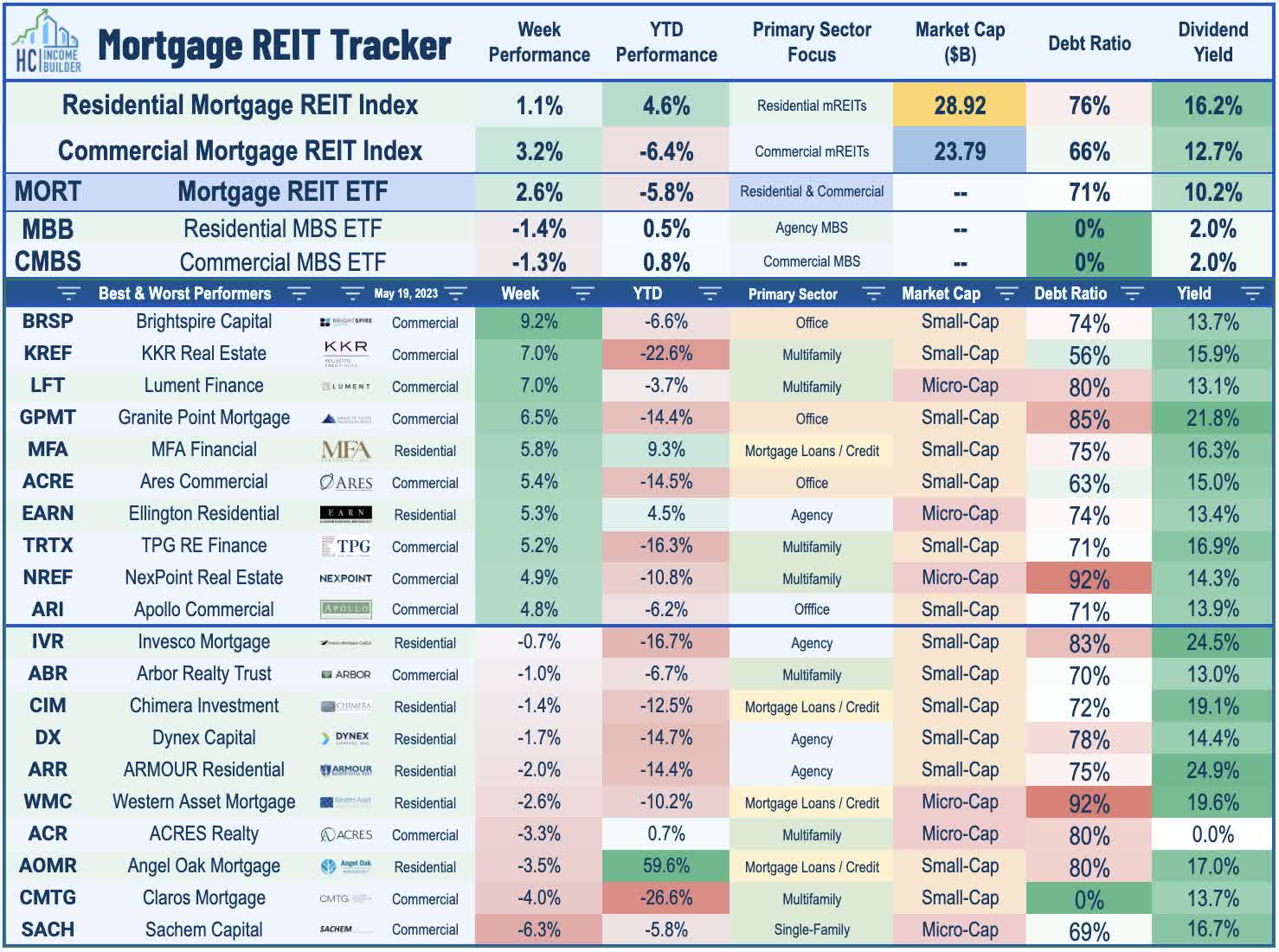

Mortgage REITs finished broadly higher on the week, led by a rebound from office-focused lenders, including BrightSpire Capital ( BRSP ), Granite Point ( GPMT ), and Ares Commercial ( ACRE ). Wrapping up earnings season, Sachem Capital ( SACH ) - which focuses primarily on short-term residential construction lending - declined about 6% on the week after reporting adjusted EPS of $0.10/share in Q1 - short of its $0.13/share dividend - and noted that it now has about 19% of its loan book ($90.1M) is on non-accrual status, up from 8.8% in Q4. SACH commented, "There could be some pressure on our dividends. Let's not sugarcoat them. We're very proud of what done with our dividend, we will defend it, as long as we can. As we build cash to be protective, we can see a little bit of a slip in the dividend."

{kind=link}

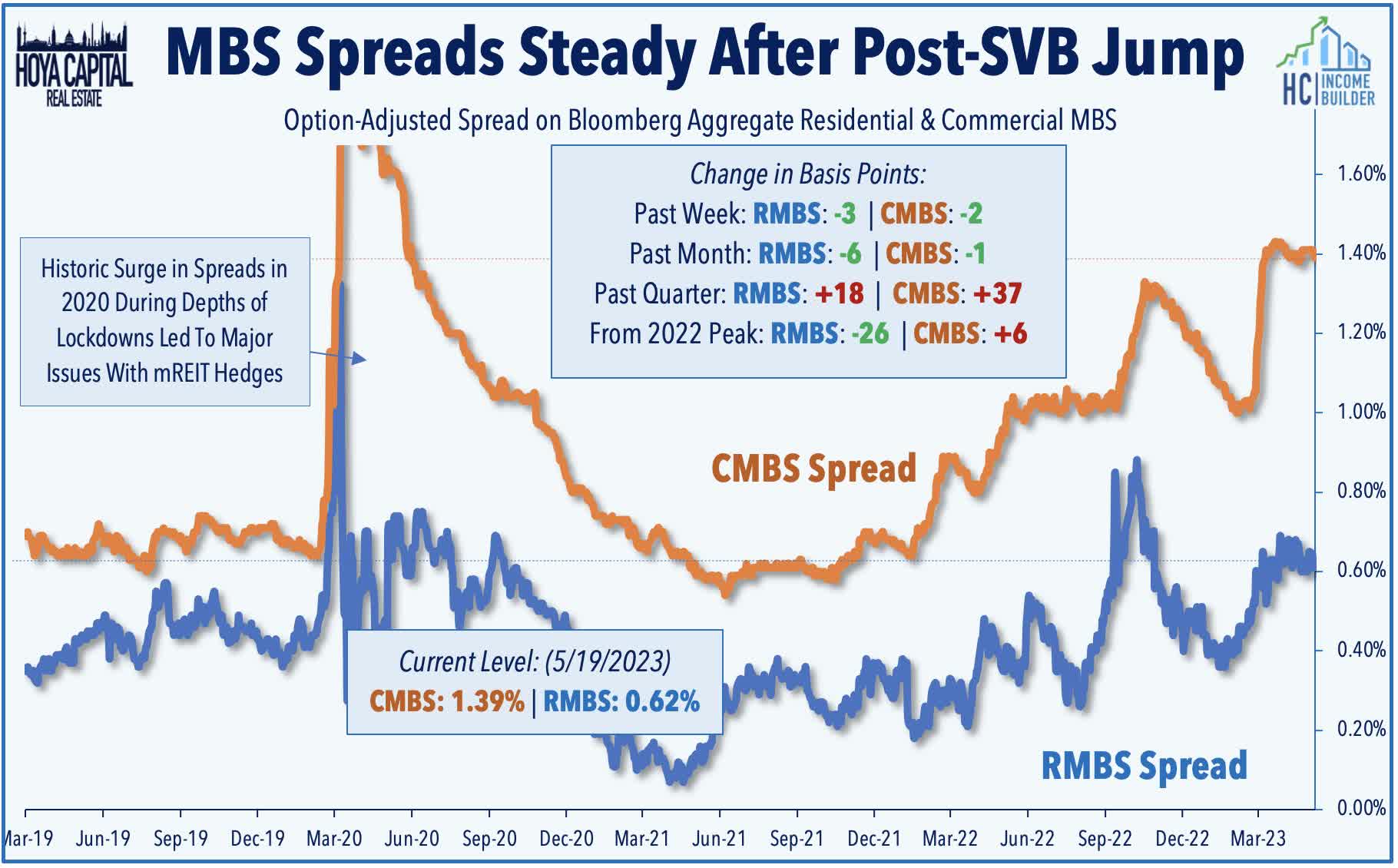

As noted in our Earnings Recap , residential mREITs reported an average decline in BVPS of 1.9% in Q1, while commercial mREITs reported a 1.8% average decline. Within the residential mREIT sector, credit-focused mREITs fared better in Q1 - reporting a slight increase in their Book Value Per Share ("BVPS") while agency-focused REITs reported an average decline in their BVPS of about 5% in Q1. Dividend coverage was stronger for commercial mREITs with about 75% of commercial mREITs covering their dividend with Q1 adjusted EPS while just 50% of residential mREITs covered their dividend. Commercial and residential mortgage-backed bond spreads have tightened a bit in recent weeks after a jump in the wake of the Silicon Valley Bank collapse in early March. Last week, Fitch reported that CMBS delinquency rate decreased six bps to 1.70% in April from 1.76% in March as higher resolution volume outpaced a lower volume of new delinquencies.

{kind=link}

REIT Capital Raising & REIT Preferreds

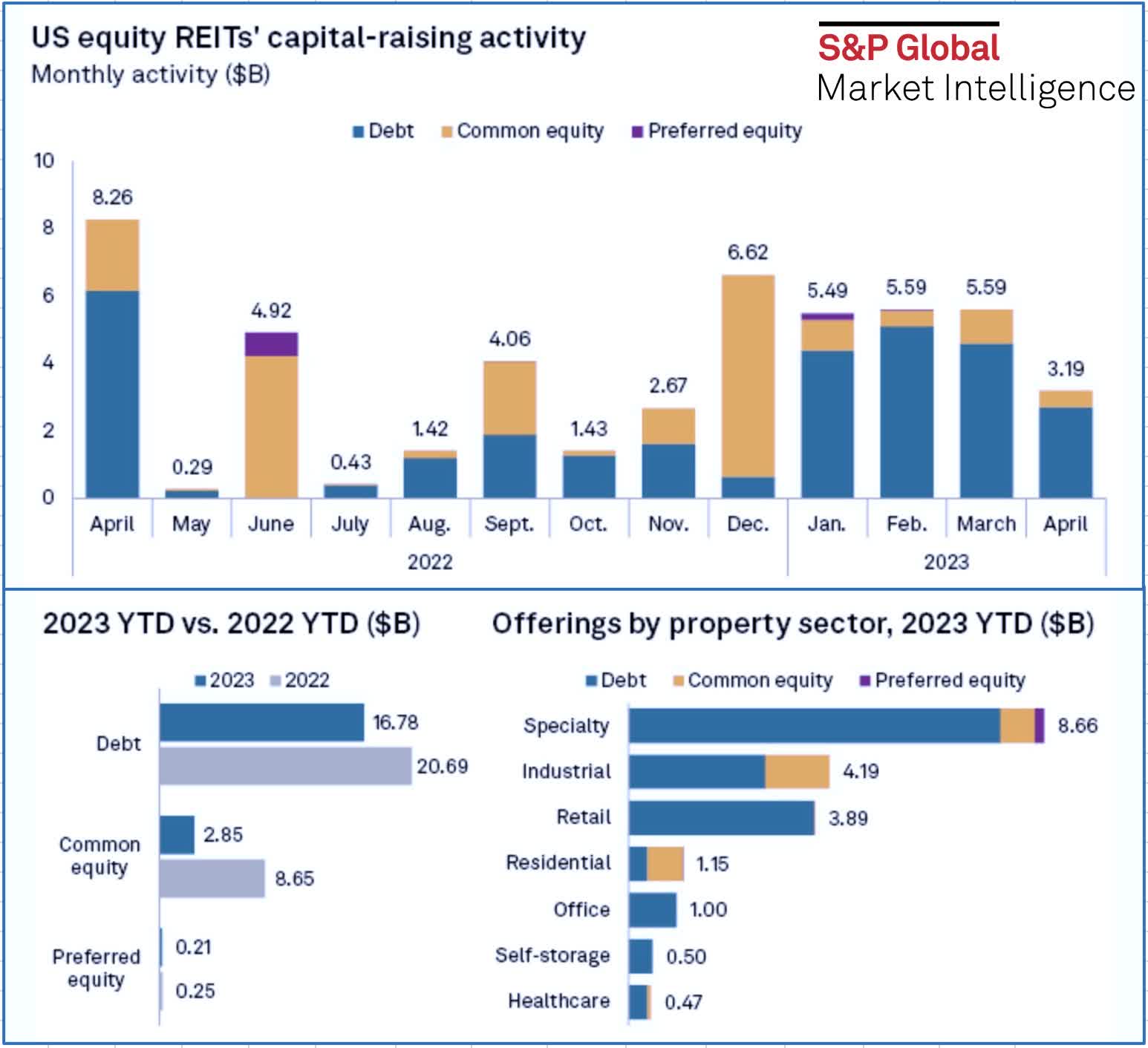

REITs were quiet on the capital raising front this week after a busy prior week. S&P Global Market Intelligence reported this week that U.S. equity REITs raised a total of $3.2 billion in April - below the $5.6 billion raised in March - and well below the $8.3 billion raised in April 2022. The offerings in April brought the year-to-date total to $19.85 billion, about 32.9% lower than the capital raised during the same period last year as REITs have significantly curtailed external growth activity since mid-2022. The slow twelve months of fundraising, however, comes after two record hauls from mid-2020 through mid-2022. Debt accounted for the majority of the funds raised in April at $2.7 billion as some REITs took advantage of a slight pull-back in benchmark interest rates, while common equity offerings accounted for the remaining $500 million. REITs have been reluctant to launch secondary equity offerings, given their relatively low stock prices. Cell tower REIT Crown Castle ( CCI ) raised the most capital during the month at $1.35 billion through two debt offerings, followed by net lease REIT Realty Income ( O ), which raised $1 billion via offerings of $600 million in unsecured notes due 2033 and another set of unsecured notes worth $400 million due in 2028.

{kind=link}

2023 Performance Recap & 2022 Review

Through twenty weeks of 2023, the Equity REIT Index is now lower by 2.5% on a price return basis for the year, while the Mortgage REIT Index is lower by 8.8%. This compares with the 9.5% gain on the S&P 500 and the 1.4% advance for the S&P Mid-Cap 400 . Within the real estate sector, 6-of-18 property sectors are in positive territory on the year, led by Single-Family Rental, Industrial, and Self-Storage REITs, while Office REITs have lagged on the downside. At 3.69%, the 10-Year Treasury Yield has declined by 19 basis points since the start of the year - well below its 2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 1.9% this year.

{kind=link}

Economic Calendar In The Week Ahead

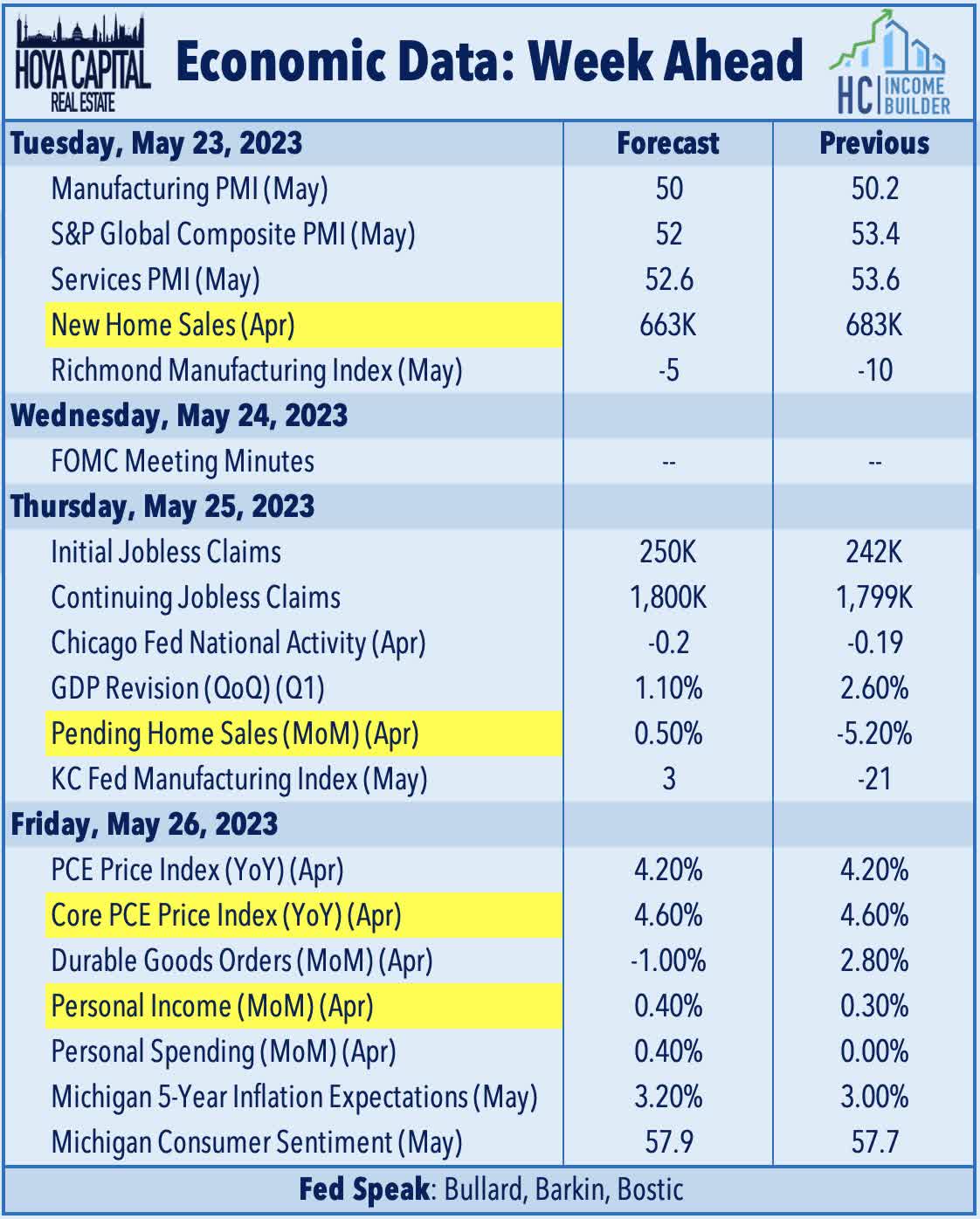

We'll see another fairly busy week of economic data in the week ahead. The state of the U.S. housing market remains in focus early in the week. On Tuesday, we'll see New Home Sales data for April, which is expected to show that sales were higher on a year-over-year basis for the first time in over a year as the housing industry emerges from a nearly two-year recession dating back to late 2021. We'll see some more housing data on Thursday with Pending Home Sales data, which is expected to increase for the fourth month out of the past five, following a stretch of thirteen straight monthly declines. The most important report of the week comes on Friday with the PCE Price Index - the Fed's preferred gauge of inflation - which is expected to show a continued moderation in price pressures. In the same report, we'll also be looking at Personal Income and Personal Spending data for April, a key read on the state of the U.S. consumer.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

A Wall Of Worry