ABCM - Abcam: Nosebleed Valuations Flat Growth Profile Justify Hold Rating

2023-06-09 09:00:00 ET

Summary

- Abcam plc's outlook remains unchanged after a mixed FY'22, with improvements needed in fundamental, sentiment, and valuation factors to attract buyers.

- Despite a strong FY'22, ABCM's poor returns on capital, economic losses and flat growth outlook hinder its investment potential.

- The company needs to enhance performance across key metrics to create value for shareholders and warrant a buy rating.

Investment summary

After a mixed FY'22, little has changed to the outlook of the equity stock in Abcam plc (ABCM) in my opinion. Importantly, there are three critical avenues in which ABCM needs to shift up in order to attract buyers to the stock. These are made from fundamental, sentiment and valuation factors.

In my last ABCM publication I noted several issues that had plagued the company's market value. The firm's reinvesting patterns was one of these, and findings suggest this may continue going forward. As is shown here today, there is insufficient evidence to suggest a re-rating is warranted in any of these three factors, and with a lack of obvious catalysts on the horizon, market values may remain anchored to the 36x forward P/E investors are currently selling their ABCM stock at.

Net-net, I am reiterating my neutral stance on the company, but it was essential to review the firm's latest numbers and revisit the investment thesis to observe what critical facts may have changed. With ABCM agnostic to such change, reiterate hold.

Figure 1.

{kind=link}

Critical facts of the investment debate

Presenting the critical facts is essential to illustrate ABCM's investment value. Thoughtful analysis reveals key findings on fundamental, sentiment and valuation factors, discussed below.

Fundamental factors

Turning to the FY'22 numbers, ABCM clipped top-line revenues of GBP361.7mm, showcasing a 15% YoY growth [note: the firm reports in GBP, and I will be holding this convention throughout the report for simplicity] . In-house revenue led the way, pumping a remarkable 18% upside from the BioVision acquisition and its custom products & licensing ("CP&L") enterprise in particular. Collectively, these two income streams contributed 67% of turnover for the year. It pulled this to GBP83mm in core EBITDA and a GBP0.249 in earnings.

Two points worth mentioning here-

- The firm is rolling over to implement the Oracle Cloud enterprise resource planning ("ERP") system. This will manage all of the firm's financials, planning, accounting and so forth. Key point is the ERP's implementation curbed revenues in both September and October. So the 15% growth may well be understated on a pro-rated basis. Looking ahead, this could be a tailwind, one investors may not be aware of.

- Management estimates a c.10% headwind to top-line growth from the above-mentioned points. Thankfully, growth was still such that ABCM saw ~330bps gross margin decompression to 75.5%. Hence, the new cloud ERP system would build on this and could play a role in achieving future margin expansion.

Switching to the geographical highlights, results were mixed. Its Americas footprint, constituting ~43% of Catalogue sales, lifted 16% YoY and 20% in constant currency terms, and EMEA sales were up 6%. China, accounting for 18% of sales, reported a decline of 2% at constant exchange rates which is a shame as the nominal growth rates in its China markets are worth noting. These regional variations are the result of a strong dollar and thus may be looked at more positively when excluding the FX impact.

Speaking of positives, ABCM's top-line is relatively hedged against large-sigma events. No revenue stream makes up >3% of turnover. Therefore, revenue is distributed evenly across a large selection customers, reducing the concentration risk in the event of an economic downturn. I've made similar arguments in the Avantor ( AVTR ) investment debate (see the deep dive on this from 2021 here ).

Moving to the divisional takeouts:

- Academic revenues, representing ~43% of catalogue revenue, grew by 4% globally.

- It also booked biopharma revenue growth of 10% on all international sales. Both U.S. and EMEA performed well in biopharma. The company's focus on recombinant antibodies and in-house assay technology, [this includes including BioVision], has resonated strongly with customers, resulting in an 80% growth for the year.

- Distributor sales made up 30% of catalogue sales, experienced a solid growth rate of 12% as well.

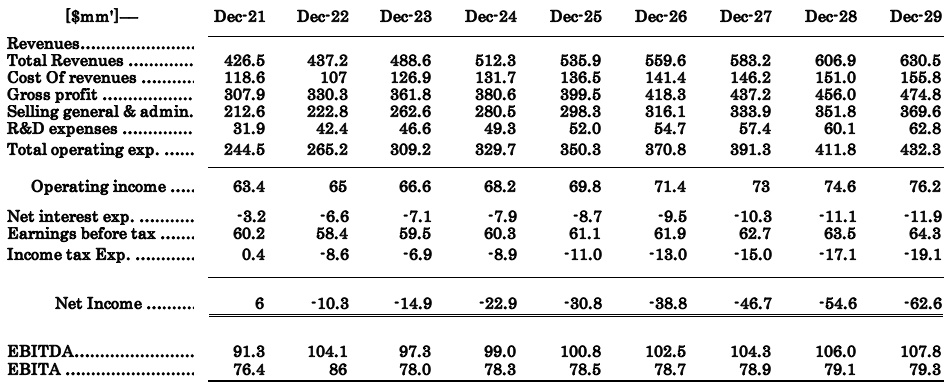

Such was managements happiness with the FY'22 period that it immediately reiterated FY'23 guidance of 15-20% growth in turnover. This calls for GBP420mm-GBP440mm in revenue for the year. Contrasting this to my own growth assumptions [observed in Figure 1], I've got the firm to do GBP512mm in turnover this year on GBP99mm in core EBITDA. This could grow to GBP535mm and GBP100mm respectively by 2025 if my growth assumptions are correct. It wouldn't be unreasonable to expect the firm doing ~GBP400 gross on this either in my view, calling for 21% cumulative increase sine FY'22. Critically, these findings do not support a 36x forward multiple as discussed later. I'd be expecting far more lucrative growth percentages from top-bottom line to pay that price, and that's just not the case from my modelling.

Figure 1. ABCM forward-estimates, [FY'24-'28]

{kind=link}

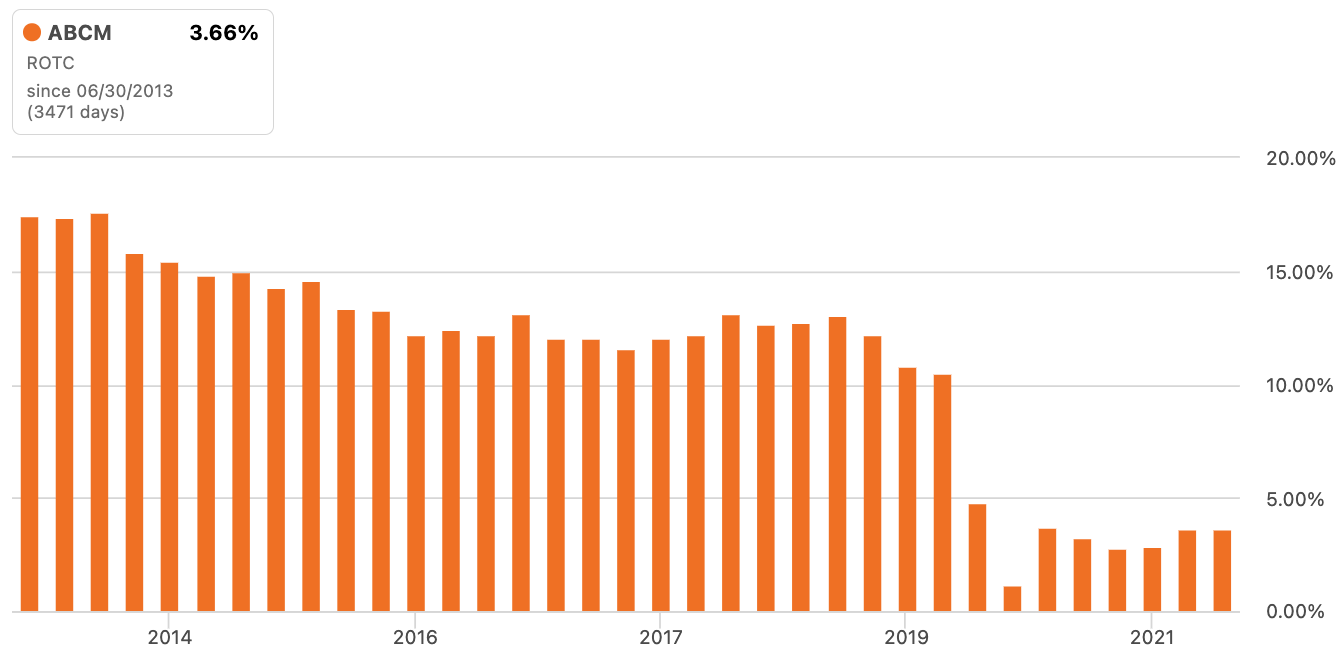

As to what this might look like for investors going forward, my assumptions on the company's profit growth are observed below. I'm looking for ABMC to do GBP60.1mm in post-tax earnings for FY'23, stretching to GBP63mm by FY'24. The 'cliff' ABMC's returns on capital have fallen off is steep, jagged and resulted in a large thud to hit the firm's lowest capital productivity in more than a decade [Figure 2]. We have data ranging back this far for the company thanks to Seeking Alpha's databases .

Figure 2.

{kind=link}

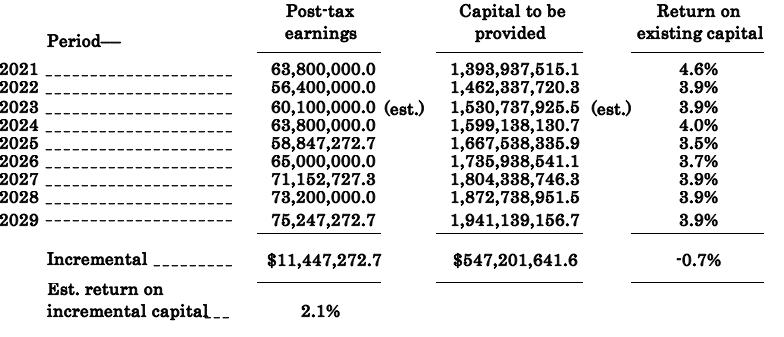

This paints a sombre picture moving forward for any investor thinking of buying ABMC today. A gargantuan effort is required from ABCM with the strictest capital budgeting to reverse course here. Note, at the current trajectory, my numbers have the firm to retain a 3-4% return on existing and new capital going forward- hardly attractive investment criteria [Table 1]. Given this doesn't meet my criteria of capital productivity above a 12% hurdle rate, I cannot advocate ABCM a buy. I'd be looking more in the 15-20% range to warrant a buy rating.

Table 1.

{kind=link}

In that vein, despite a reasonably strong period in FY'22, on fundamental grounds, there's little to bite into for us as investors.

Sentiment factors

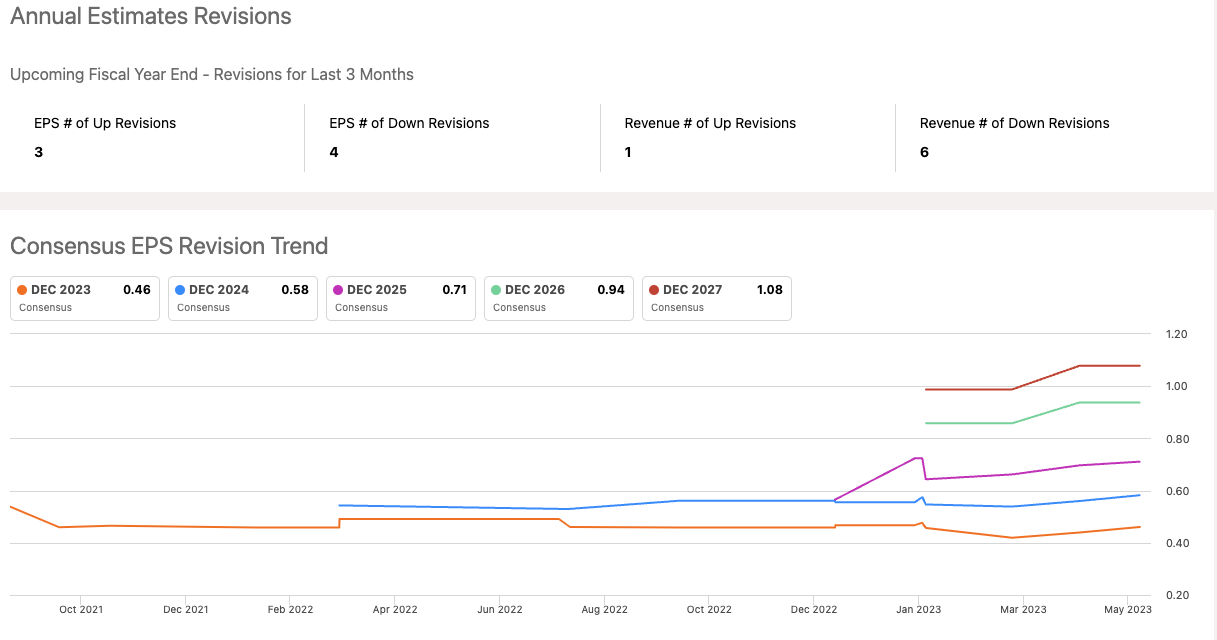

You might accept the potentially laggard capital returns from ABCM is sentiment and valuation factors ironed out the case. Notably, this isn't the case. There has been no less than 4 and 6 down revisions to earnings and revenue in the last 3 months, respectively. Just 1 change upward. But there's an interesting dichotomy here- despite the revisions to the downside, the sell-side still expects 50% growth in earnings from ABMC in FY'23, clipping back to 2% earnings growth in FY'24.

In my view, the growth is less meaningful without ABMC turning an economic profit instead of an accounting one (where the return on capital is above the 12% hurdle rate). In fact, any growth without the economic earnings underneath it is actually destructive to shareholder value, as it detracts from the cash ABMC can spin off for its owners. In other words, the firm cannot grow without jeopardising value to its shareholders, and vice versa. Not unless it bumps up those returns on capital.

Second, there is little to no options positioning for contracts expiring in June, therefore no speculative or hedging activity to see where investors are parked. If sentiment was high, I'd expect to see tremendous open interest at strike depths well above the current share price. Sadly, that's not the case, again suggestive of the low sentiment in ABCM's case.

Figure 3.

{kind=link}

Valuation and conclusion

Any hope of a wide valuation disconnect to salvage the buy thesis is left at the door when you look to see investors trying to sell at 36x forward P/E, and ~30x forward EBIT. I can't get there, nor advocate 'other people's money' to enter wayward in ABCM either. This is 83.5% and 81% above the sector, respectively. In order to re-rate above a 30x forward EBIT, you'd need ABCM to be pushing >25% growth over the next 3-years straight on my rudimentary calculus. It would appear this cannot be done, not without some anomaly or wipeout of the firm's competitors.

I'd have ABCM priced at the sector multiple at least and the reasons are clearly outlined in this report: 1) poor returns on capital, 2) economic losses on accounting profits 3) earnings revisions to the downside and 4) flat growth outlook. This would see it trade at ~20x forward earnings and 16x EBIT, still not cheap. At these multiples I'm getting to roughly $13/share in equity stock value based on my FY'23 and FY'24 growth assumptions. This confirms neutral rating.

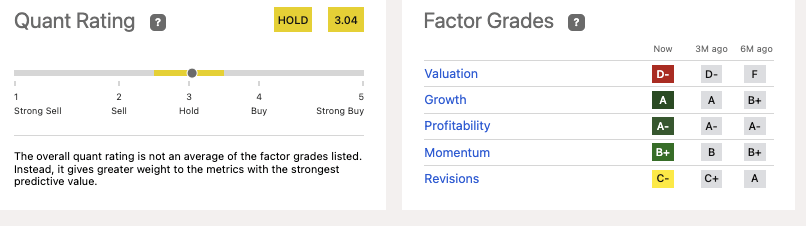

These findings are supported objectively with data from the quant system, that also suggests ABCM is rated poorly on valuation. In my view, this adds a layer of confidence around the hold thesis, and I am aligned with the quant system's output.

Figure 4.

{kind=link}

Net-net, for ABCM to qualify as an investment-grade company, it would need to improve performance across a number of key metrics. Chief amongst these, are its returns on existing and new capital. These dovetail to fundamental, sentiment and valuation factors. Without the ability to produce additional profit growth from its capital base above the market's return, there is little chance of the company creating value for shareholders in my opinion. In that vein, the growth outlook looks quite benign, whilst sentiment and valuation factors are equally unsupportive- especially with the company priced at 36x forward earnings. Collectively, a hold call is well supported here in my view.

For further details see:

Abcam: Nosebleed Valuations, Flat Growth Profile Justify Hold Rating