AHCO - AdaptHealth: A 4% Return On Capital Doesn't Sing 'Undervalued' At 5x EBITDA

2023-08-30 08:00:00 ET

Summary

- AdaptHealth Corp's Q2 numbers were not well-received by the market, and correspond to an erosion of value for shareholders.

- The company's gross return on assets is only 9%, indicating that its asset base is not pulling its economic weight.

- Economic earnings produced on $4.4Bn in capital don't cut it and are in the negatives for 2023 so far, whereas returns on capital are subpar.

- Net-net, reiterate hold.

Investment updates

Since the June publication, AdaptHealth Corp. (AHCO) has continued to push sideways into congestion despite selling 16% higher at the time of writing. The company's Q2 numbers weren't appreciated by the market, and findings outlined in this analysis support the reasons why. This is a capital intensive business where $4.4Bn in capital deployed into operations returns just $1.36 in TTM NOPAT/share, otherwise 4.1% return on the investments.

Critically, this has translated into an erosion of value for shareholders given cash pays ~4-5%, long-term rates are at the same level, and corporate high yields are offering 8-9% starting yields. Not to mention, if you expect 10-12% from riding the index-same thing. It starts to pile up when the comparisons are made on opportunity costs.

Net-net, given the factors discussed here today, I continue to rate AHCO a hold.

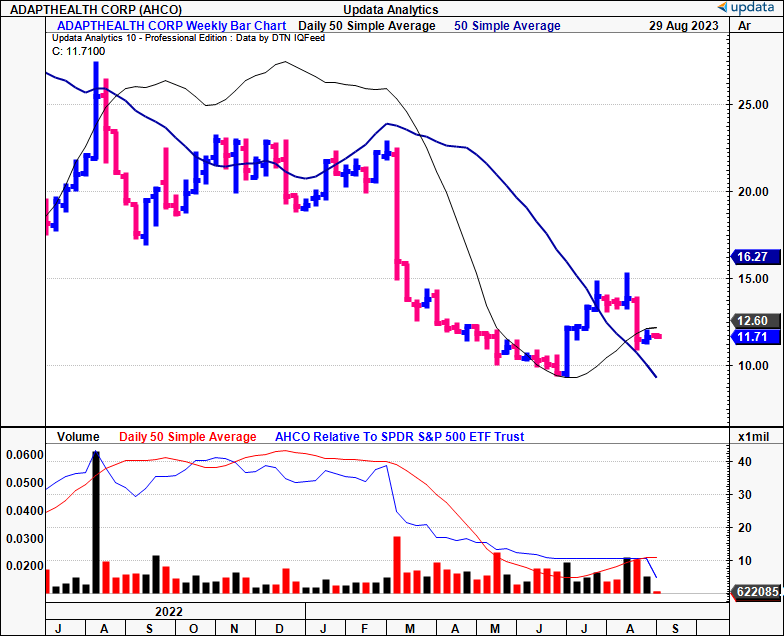

Figure 1. AHCO weekly price evolution, 2022-date

{kind=link}

Critical investment facts to reiterated thesis

1. Q2 FY'23 insights

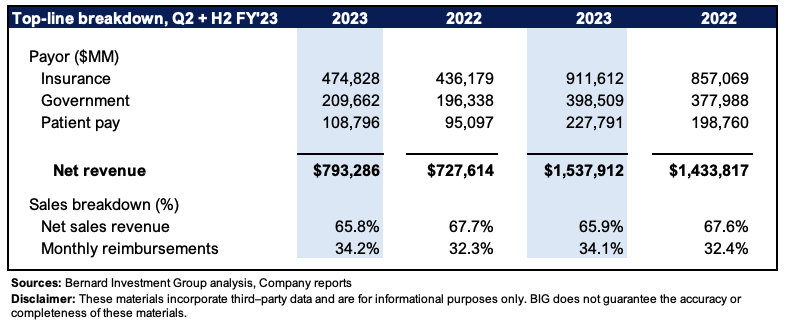

AHCO put up Q2 revenues of $793.3mm , up 9% YoY. This was on core revenue growth was 8.7% on adj. EBITDA of $171mm, up 14%. The margin on this came to 21.6%, with a 100bps decompression resulting from AHCO's liquidity preservation measures instilled over the last few quarters. Critically, the composition of the firm's continuous glucose monitors ("CGM") is shifting towards government sources. Government-sponsored payers now comprise 77% of AHCO's CGM census, growing 9% YoY, and ~200bps sequentially. This trend is projected to continue throughout H2 FY'23.

Figure 2. Note: H1 FY'23 is shown on the right two columns of the table

{kind=link}

Days sales outstanding ("DSO"), reduced from 45.4 days to 41.2 days YoY and were also down from 42.7 days in Q1 this year. It left the quarter on net leverage of 3.54x adj. EBITDA, down off 3.63x in Q1. Management n ow looks to revenue of $3.16Bn-$3.2Bn on adj. EBITDA of $650mm-$680mm. It also maintains its expectations for total CapEx at 10%-12% of revenue, to produce FCF margin of 3%-4%, calling for $128mm at the upper bound. It generated ~$55mm in FCF for H1, so it needs to spin off another $73mm across H2 to get there.

The divisional breakdown of the quarter is as follows:

- Divisional growth was driven by its sleep and respiratory product lines, both with both segments up double-digits YoY. In the sleep category, total revenue reached $303mm, a 16% YoY increase, driven by PAP setups and a consistent demand for resupply.

- To illustrate, the PAP patient census grew 41% from last year, whereas resupply orders climbed 11%.

- Meanwhile, respiratory products clipped $154mm in sales, a 13% YoY growth schedule. It displayed its highest net patient census since Q4 of '21.

- Finally, diabetes revenue was up just 2% YoY. The flat growth was offset by the 13% increase in CGM patient census.

Thus, the shift in payor composition towards government payors has undoubtedly paid off in my view. Is it sustainable, is the next question. Time will tell.

2. Reconciliation of profits produced on capital/assets deployed

Less concerning to our core investment tenets are the profits as an absolute number. What's more relevant are the economics of what profits are produced on the capital invested and/or assets deployed by the company.

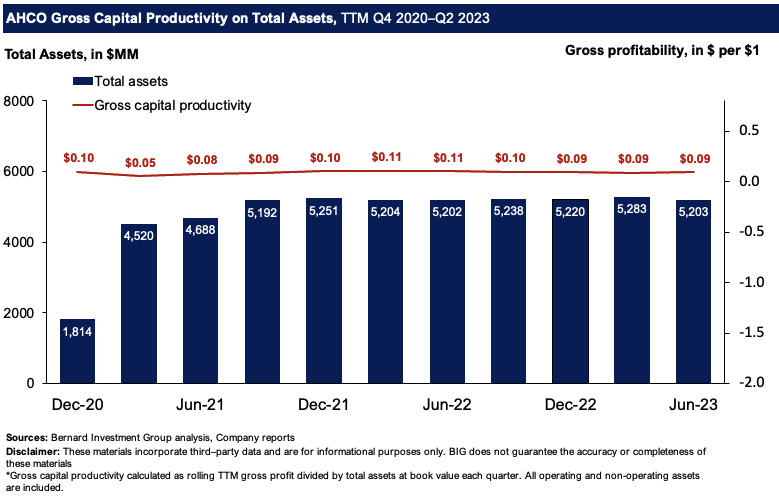

Figure 3 outlines the gross return on assets produced by the company on a rolling TTM basis from 2020-2023. This is also known as gross capital productivity, and shows what amount a corporation returns in gross profit for every $1 employed into the asset side of the balance sheet. All core and non-core assets are included, where the TTM gross profit is taken as a quotient of total assets, which is the denominator. It is relevant because no amount of accounting can adjust the gross profit or total asset number, hence it captures a lot.

Critically, it shows the firm's asset base isn't pulling its economic weight. AHCO brings back just $0.09, or 9%, on every $1 employed into the company's gross assets. This isn't attractive in my view, and suggests why the company's rolling operating margin has hovered ~7-8% since 2021 on a rolling TTM basis. Novy-Marx (2013) suggest gross capital productivity of $0.33 or higher is preferable and suggests a quality business model.

Figure 3.

{kind=link}

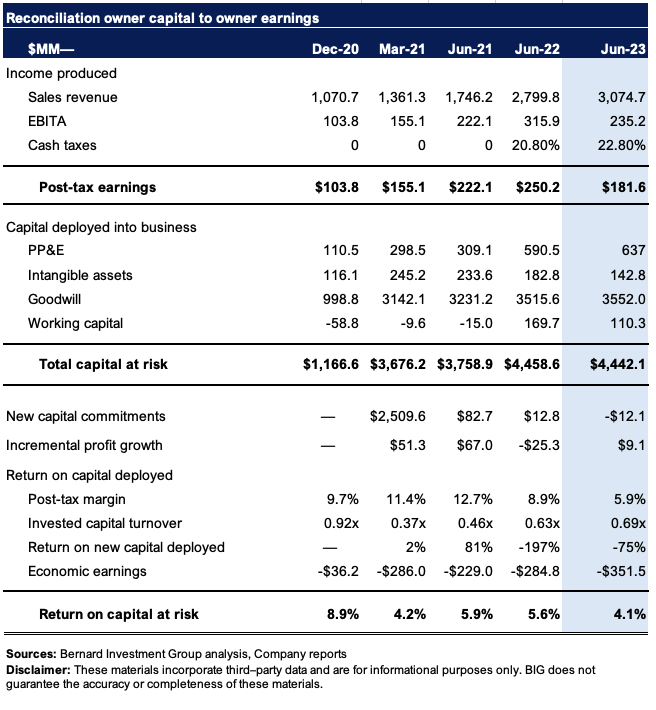

Figure 4 provides a more granular depiction of the flow of revenues and post-tax earnings produced on the capital deployed into AHCO's business. It, too, takes a rolling TTM approach. AHCO has put 103% of the capital provided by investors (debt, equity) at risk as of Q2 FY'23. Accounting goodwill, whilst not an 'operating asset', is considered capital deployed. Post-tax earnings are equal to the net operating profit after tax.

Around $4.44Bn of capital produces $181.6mm in earnings after-tax, otherwise just 4.1% return on investment. This is marginally down on earlier periods, but below the required rate of return nonetheless. The required rate of return is considered 12% here, in line with long-term market returns on capital. Hence, the economic loss produced on the $4.4Bn of capital at risk came to $351.5mm last period (TTM values). If AHCO were the manager of a portfolio of investment securities, you would call into question its investment decisions. AHCO is instead in charge of a portfolio of home medical supplies. The capital it has tied up in the business isn't more profitable than what investors can achieve elsewhere in my opinion. This is relevant because market returns closely track business returns over the long-term.

Figure 4.

{kind=link}

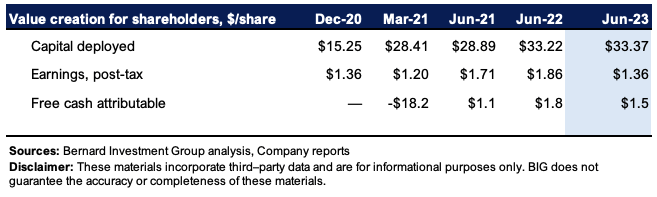

The value erosion for shareholders is fairly clear in Figure 5. Here, the key data form Figure 4 is consolidated to a per-share basis. More than $33/share of capital deployed produces just $1.36/share post-tax. It's no wonder to see FCF/share compound up to just $1.50/share from $1.10 from 2021.

Figure 5.

{kind=link}

Valuation and price structure

Several critical points feed in to the talk on valuation.

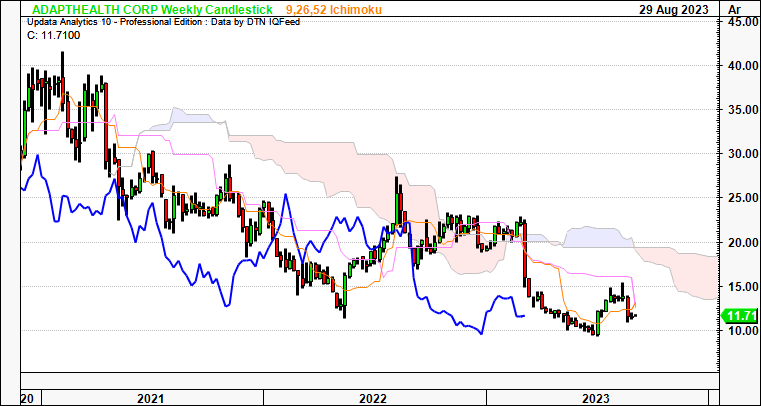

One, price structure has broken down for AHCO these past few months. Taking a long-term view and looking at the weekly cloud chart below, it's obvious both price and lagging lines are below the cloud. Both turning lines are as well. As far as downtrends go, this is as classic as it gets. The downside isn't unwarranted either in my opinion-you saw just earlier the lack of economic value created by AHCO these past 2.5 years. Investors aren't unwise-they expect their companies to at least beat the hurdle if allocating their hard-earned money. Thus, price action is soft and there appears to be a lack of demand even at these levels.

Figure 6.

{kind=link}

Two, to further hammer in the above point, removing the noise of time, and the intra-trend volatilities to observe pure directional movements only, we have downside targets to $8.10. The point and figure chart below exemplifies this well. These use mathematical formulae to discern directional moves in a cleaner fashion. We also have downsides to $7.70 that have been in situ for some time now. Hence, whilst it tried to stage a rally around 1-2 months ago, AHCO didn't catch a bid and there's probability for future downside from here.

Figure 7.

Data: Updata

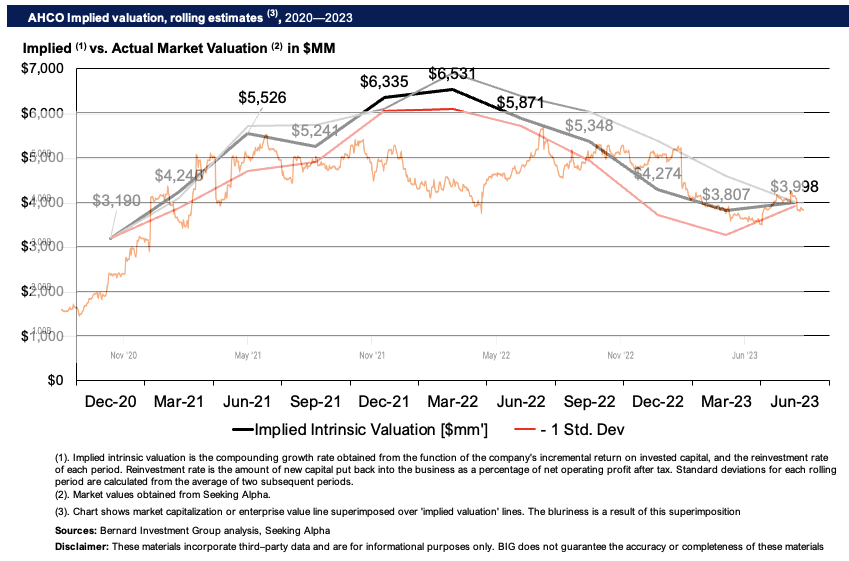

Three, a firm can compound its intrinsic valuation at the function of its ROIC and the amount it reinvests at these rates. A higher return on capital at risk promotes a higher compounding growth rate to intrinsic value, provided there are opportunities for the company to deploy cash at these rates. Those with below-par rates don't enjoy the same luxury. Figure 8 shows this calculus to AHCO's equity line since 2020. There was a period where it arguably sold at a discount, but, in true market fashion, the market priced AHCO at what appears to be a fair level moving into H2.

I've got AHCO at $3.99Bn in EV, a shade above where it sells at the time of writing. Hence, the company doesn't appear overvalued, nor does there appear to be any asymmetrical risk/reward on offer in my view.

Figure 8.

{kind=link}

Finally, we see more explicit evidence in the data outlined in Figure 9. It shows the ratio of EV to invested capital, in other words, what the market sees its capital producing in terms of earnings power and value-creation. It is priced at EV/IC of 0.87x. In my view, the market doesn't see further upside generated from the firm's capital above long-term market rates (12%). In fact, considering 1) the current EV, 2) the capital invested, 3) the returns produced on this, and 4) the hurdle rate; it would appear the company's stock sells at >2.6x the growth potential that's already priced in. The stock sells at compressed multiples of 15x P/E and just 5.8x forward EBITDA-potentially attractive for naive 'value' investors. But I'd urge, very strongly, that in my opinion, these multiples are justified and reflect a poor stream of cash produced on the capital AHCO has employed. This supports a neutral view in my opinion.

Figure 9.

BIG Insights

In short

Despite continued financial growth from AHCO this isn't translating into added value for shareholders. The profits earned on the capital it has at risk in the business is sub-par to what investors can achieve elsewhere. If you're looking for quality compounders that can recycle capital back into the business at above-market rates, I'm not sure AHCO offers this. Findings uncovered in this report corroborate a neutral view in my opinion, supported by 1) soft economic growth levers, 2) price structure in the market, and 3) valuations. Net-net, reiterate hold.

For further details see:

AdaptHealth: A 4% Return On Capital Doesn't Sing 'Undervalued' At 5x EBITDA