AHCO - AdaptHealth: Revising To Hold On Economic Fundamental Valuation Grounds

2023-06-20 04:13:08 ET

Summary

- AdaptHealth Corp. faced challenges in its Diabetes division in Q1, along with other hurdles.

- Despite this, it booked growth in its sleep product category and is implementing liquidity preservation measures, which could improve its fundamental picture.

- Despite commendable growth numbers, AHCO's market value is not dislocated from its book value, in my view, due to the lack of economic earnings and poor returns on capital.

- I am revising to hold on these grounds, equity valuation at $10.50.

Summary of investment findings

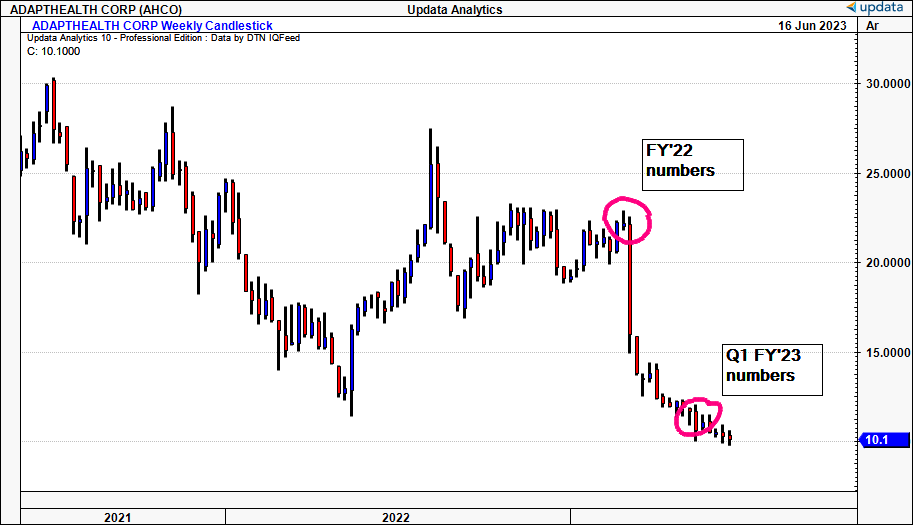

Much has changed in the investment narrative of AdaptHealth Corp. (AHCO) since my last publication in November. The company missed its FY'22 numbers, backed up with another miss in Q1 FY'23 from The Street's estimates.

More extensive findings presented in this report suggest the critical facts are challenging and fraught with pain points. My questions are aimed at the company's business economics, and its ability to produce appreciation in its market value over time. From the capital AHCO has put to work since listing, profits have come back at rates below the market's return on capital. Investors, in my view, have responded to this and priced the company where is should trade, one at a discount to more economically viable peers.

Net-net, challenges in its Diabetes division, combined with the points above, warrant a revised rating to hold for AHCO. I am looking to $10.50 per share in market value for the stock given the findings. Revise to hold.

Figure 1. AHCO weekly showing selloff at key inflection points

{kind=link}

Critical facts to revised thesis

Careful analysis of the company's net revenue, patient census growth, EBITDA, cash flow, and cost-saving initiatives are telling of what's to come for AHCO. However, it still falls short on fundamental, economic and valuation factors in my opinion.

1. Fundamental factors

AHCO reported Q1 net revenue of $744.6mm, a 5.4% increase compared to $706.2mm last year. The company now has a 138,000 patient census, up 8.3% YoY. Thus, average patient census revenue was $5,395.60 at Q1, slightly down from $5,545 the year prior.

Growth stemmed from upsides in the company's sleep product category and pulled to adj. EBITDA margin of 18%, down 150bps YoY with operating cash flow of $140mm. Days sales outstanding also improved 5 days YoY to 42.7 days. It also put another $89mm in CapEx to work and left the quarter with $51.1mm in FCF. By the looks of it, management have set a forecast to clip anywhere between $96–$128mm in free cash by H2 this year.

You'll see the company's growth route since FY'19 has been commendable, adding $625mm in turnover and another $20.8mm in quarterly operating income (using TTM figures).

Table 1. AHCO Net revenues, Q1 2019–2023

Data: Author, AHCO 10-Qs

These growth numbers are commendable, for sure, but are not shared equally throughout the company's broad offerings. In Q1 non-acquired sales growth fell short of internal estimates due to headwinds affecting the company's diabetes line. Notable issues impacting margins and asset utilization in the division include:

- Despite an 8.3% growth in continuous glucose monitoring ("CGM") patient census, management report that an increasing number of payers have shifted their diabetes patients out of the durable medical equipment ("DME") channel, onto dual benefit and pharmacy routes instead. As a result, more sales are pushing through pharmacy, whereas some manufacturers are simply holding their DME distribution internally. There is likely a dozen or more reasons for this shift, although none positive for AHCO in my view.

- Subsequently diabetes revenue for pumps and supplies declined by $9mm YoY, which snipped adj. EBITDA by 2.7% YoY to $134mm.

- It is crucial to address the challenges faced by AHCO's diabetes product line.

In spite of the challenges in its diabetes segment, AHCO has advanced in other areas. The company experienced significant growth in its PAP setups, with figures surpassing 50% compared to any time before the Philips recall. The PAP renal patient census nudged to 53% from the lowest point in February 2022 – to a record level – while the resupply patient census grew by 10%. These positive trends indicate the effectiveness of AHCO's strategies and its ability to serve a larger patient population. The surge in demand could be a notable bedrock for the company to set on in FY'23, and thankfully "came to the rescue" of the Diabetes segment.

In view of the analysis above, there are 3 critical facts that need further discussion:

- Upsides in sleep products: The increasing demand for sleep products and the record-high patient rental census is notable, as mentioned. Should AHCO successfully capitalize on this demand, there's a more favourable position for future growth to slot in.

- Not all doom and gloom in the diabetes segment : As mentioned, the shift in patient distribution, and overall lower volumes hurt diabetes growth in Q1. Still, there are investment opportunities for the company in this domain. AHCO's emphasis on a more innovative care model, via the Adapt 2.0 "myApp" platform, which facilitates patient management of chronic diseases, has seen strong adoption– 50,000 downloads, and 7,500 verified orders through the app. Alas, there is still a focus on product diversification, leveraging technology, developing strategic alliances, and so on, and thus not a complete wipe out just from one period's downside.

- New liquidity preservation measures : Management are restructuring the company's operating model, rationalizing some of its fixed capital, and renegotiating its key supplier contracts in an effort to save from 2023. It hopes to book $40mm in total savings this way– $25mm to be realized this year alone, leaving another $15mm ahead of us.

These points shouldn't be discounted and warrant AHCO's rating as a hold in my view, reflecting management's efforts to improve the fundamental picture.

2. Economic factors

Equity investors are entitled to a claim on the residual net profits of a company "at the end of the year" so to speak. Net income presented on the financial statements differs from the residual income just described. Thus, there are both accounting and economic realities to consider. Pinto and co-author's (2010) do a good job for us in terms of definitions: "residual income is net income less a charge (deduction) for common shareholders ’ opportunity cost in generating net income". That charge being one of the capital employed to run and grow the business.

Similarly, in order to grow operations, firms must invest additional money to buy more income-producing assets, launch new products, increase capacity, or make business acquisitions. What post-tax profits the company produces from its investments is an absolutely quintessential data point that influences the market's perception of its future outlook.

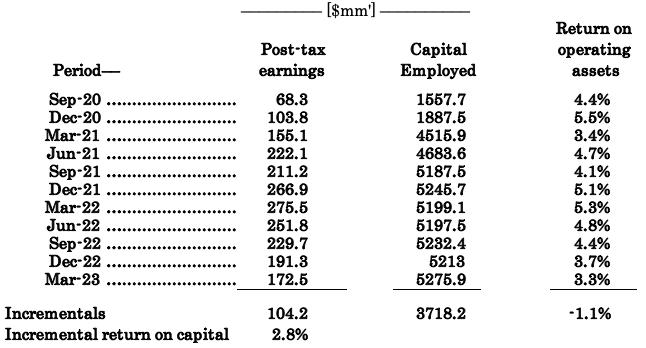

The critical fact– investors will pay higher valuations on companies who produce earnings on capital employed greater than the market's return on capital. I've tabulated AHCO's net return on operating assets since 2020 below. Figures are TTM and represent the after-tax operating earnings produced from the existing capital employed each period. Two immediate observations emerge:

- The return on existing operating capital has hovered between 3-5%, and decreased 110bps over the period. Taking a 12% hurdle rate, the economic loss on this is quite pronounced, 7-9% in fact.

- The firm has invested $3.78Bn to produce $104.2mm in earnings, just 2.8% incremental return on capital.

The numbers shown here are telling. The S&P 500 has returned 31.2% incremental capital appreciation since September 2020 to the time of writing. AHCO produced 2.8% of its investments.

This difference isn't at all neglected by the market. Investors are wise enough to know that a firm putting back just 3-5% return on capital to its shareholders, when the benchmark averages 10-12% long-term, is not valuable.

This would directly suggest why the company has produced just 63 cents for every dollar retained from investors, then reinvested back into the business to grow in my view. This is evidenced by the company's market-to-book ratio of 0.63x, below the 8x 3-year average.

Table 2.

{kind=link}

Subsequently, whilst the reported earnings (pre and post-tax) have demonstrated expansive growth, this hasn't transposed to any value-add for shareholders. In fact, the economic earnings, those profits/losses above/below the hurdle rate (12% in my investment criteria, also the same as the capital charge discussed earlier), have been abysmal over this time [Table 3].

AHCO has generated a cumulative $549.3mm in post-tax earnings since FY'20 (TTM basis), whereas at the capital charge of 12%, this translates to a cumulative loss of $968mm. In other words, say the market return on capital is 12%, AHCO underperformed the benchmark by a wide margin.

This says it all for me. The market can't reward a company that isn't creating economic value for its shareholders. The opportunity cost involved is too high and is an unnecessary deviation from a sound course of investment gains.

Of course, these figures are a little less meaningful now that they've already occurred. However, there is reason to believe these trends may continue. My numbers have the company to grow sales 5-6% this year, on earnings growth of 11-13%. However, you'd still be recording the same capital charge, and therefore underperformance from the market's return on capital. Alas a neutral view is warranted.

Table 3. AHCO Economic profitability, 2020–2023 (TTM figures)

Note: EVA = (NOPAT – [Invested capital x hurdle rate]). Cumulative results are sums of each column. (Data: Author, AHCO 10-Qs )

Valuation and conclusion

Investors aren't holding AHCO with strong hands, rather the opposite in fact. Shares are discounted at 13x forward sales versus the sector's 20x, and it is at 0.63x book value as mentioned. Given the lack of economic earnings discussed above, there doesn't appear to be a dislocation in the company's market value of equity versus its book value of equity, in my opinion.

One might argue 13x forward is an attractive discount but you'd be looking for growth on top of that, and there's some value in that regard with the PEG ratio of 0.4x implying you could get the company's projected earnings growth at a discount. But what else would one capture with this? From what's been said thus far, 1) lack of economic earnings, 2) poor returns on capital employed, below the market return on capital, 3) both of these things despite the company's tremendous top-line growth.

Using my FY'23 earnings estimates 13x forward gets me to $10.40 in equity value per share for AHCO, around about the market price as I write (13x0.8 = $10.40). With shares trading in-line with this estimate, again a neutral viewpoint is warranted.

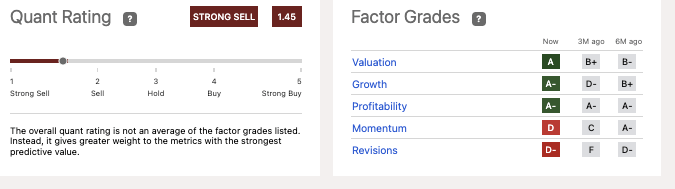

Added to that– the quant grading system has it rated a "strong sell". This shouldn't be ignored in my view, given the system's prowess in obtaining objective insights from rolling, real-time data. I'd say this somewhat supports the revised thesis as well.

Figure 2.

{kind=link}

Net-net, there is substantiative evidence to warrant a revised rating on AHCO. Looking forward, I believe the company is valued fairly at ~$10.50, or 13x EPS estimates of $0.80 in FY'23. However, peeling back the superficial layers of the investment debate reveals deeper issues to consider. Chiefly, the company's ability to create value for shareholders going forward. After this thoughtful analysis, I am revising the company back to a hold.

For further details see:

AdaptHealth: Revising To Hold On Economic, Fundamental, Valuation Grounds