SLQT - Advanced Emissions Solutions Inc.: Why I've Tripled Down In The $1s

2023-06-21 20:06:29 ET

Summary

- At $1.25, ADES shares are trading at a $41.25 million market capitalization. The company has $79 million in cash and $20 million in debt.

- The company competes in an oligopoly market structure and has $600 million of capital invested in its business, with another $95 million of CAPEX earmarked.

- I explain why the sentiment is so negative towards the stock and why I've tripled down on my position sizing, in the low to mid $1s.

Small cap (micro-cap) investing has always been a conviction game. In many instances, due to the lack of liquidity and inherently small market capitalizations there is very limited buy side / institutional support. When you have limited buy side sponsorship you are subject to amplified volatility as the vast majority of owners don't know what they own. Far too often, in small cap stocks, the share count float turns over quickly, sometimes rapidly, and sadly you have mostly have a shareholder base of renters as opposed to owners. In the Wild West that is the small cap frontier, the momentum works in both directions, and momentum tends to follow the aesthetics of a particular stock chart, at a moment in time, including the good, bad, and the ugly. Given this volatility, you can experience crazy drawdowns and simply bizarre stock price reactions that seem completely untethered to what logical fundamental analysts might consider fair value.

Because most people can't stomach the inherent volatility associated with small caps, there is a limited captive audience for this narrow/ niche segment of the market. Notwithstanding the brutal 2022, the vast majority of the time, it is far more fashionable, for the majority of people to just buy the Nasdaq 100 ( QQQ ) or Mega Cap technology stocks.

As someone that exclusively plays in the small cap patch of garden, notwithstanding a few select special situations names, where I venture outside of this theatre (see my April 21, 2022: As Bill Ackman Liquidated, Netflix Is Now My Largest Sized Position ), I embrace the heightened volatility and relish my high frequency encounters with mis-priced small cap/ micro-cap stocks.

As a quick aside, before we get into the main course of the article, Mr. Market has been most generous to small cap investors that embrace extreme mis-pricings. For example, thus far in 2023, the vast majority of my robust returns have been bolstered by aggressively adding to four of my twenty plus current stock portfolio. This includes adding to my TravelCenters of America ( BP ), in the high $40s, as it was later bought by BP plc for $86 per share. This includes loading up on Kopin Corp. ( KOPN ), at $1.07, on May 11, 2023, after listening to Michael Murray's Q1 FY 2023 conference call. Kopin goes on to trade up to $2.50, on June 1, 2023, so less than one month later. It also includes loading up on Mesa Air Group, Inc. ( MESA ), on May 10th and 11th, in the $1.40s. Mesa shares rebounded smartly, to $2.65, on June 16th. And lastly, while traveling to San Diego (La Jolla and San Clemente), for a conference, I took advantage of the Citigroup-induced downgrade /sell-off in eHealth, Inc. ( EHTH ), and its publicly trade peers (GoHealth, Inc. ( GOCO ) and SelectQuote, Inc. ( SLQT )) by loading up, on EHTH, at $6, on April 26th and more so, at $5, on April 28th. EHTH shares rebounded smartly to $10 on June 8th and 9th.

Therefore today, perhaps aptly, I write to share I've recently tripled down on Advanced Emissions Solutions, Inc. ( ADES ). If Mr. Market affords me the opportunity to aggressively add to my long-standing core position, I'm certainly not going to look a gift horse in the mouth. And during calendar Q2 2023, including just yesterday, between $1.24 and $1.30 per share, I've aggressively loaded up on ADES shares, as I would argue the stock is ridiculously mis-priced, closing just yesterday, at $1.25.

First, A Brief History

On May 10, 2021, after the bell, ADES announced a strategic review process to maximize shareholder value. ADES shares were then trading at $4.63 per share. The next day, shares shot up to $5.46, closing at $5.20, with nearly 7% of the entire share count changing hands. A formal strategic review process is often a major catalyst and special situations event. It attracts a lot of attention and new pools of capital. By June 2, 2021, ADES share hit a new 52-week high, of $8.41. However, this special situations money tends to be 'fast money' and event-driven only. These pools of capital aren't interested in investing in the underlying businesses per se, rather they are only along for the ride, if they can get in on an event or buyout, such that they generate a tidy profit, and in a short period of time.

As the sand in the hourglass continue to move through the narrow section, event-driven investors slowly left the ADES party. As the event-driven investors did their Irish goodbyes, ADES shares drift lower, finding a new equilibrium between the mid $4s and lower $5s, depending on the physical supply and demand, of the stock's ebbs and flows. On August 15, 2022, we heard news that the Strategic Review was rapidly careening towards a conclusion. ADES shares go on to move from $4.91 (its August 15, 2022 closing price) to $6.41 (its August 19, 2022 closing price).

Then all hell broke loose.

On a Friday afternoon, after the bell, ADES announced a merger with a very promising privately held company, Arq. However, management very badly read the temperature of the room and its entire ADES shareholders base. This shareholder was anticipating, positioned for, and expecting a buyout.

Again, all hell broke loose and ADES shares cascaded lower.

Candidly, with a then projected $4.75 per share in cash (prior to the recent merger with Arq), the well-signaled sunsetting of ADES's lucrative tax credit business, by the end of 2022, and ownership of its Red River plant, most market participants, myself included, thought selling Red River, even for $50 million to $75 million plus the balance sheet net cash, which would result in shareholders receiving potential net proceeds of say $7.50 to $9 per share, as the most logical outcome of a Strategic Review.

The market reaction was swift and punitive as the event-driven investors base rushed for the exits, and quite frankly, from a physical supply and demand perspective, there weren't close to enough new buyers on the other side, willing to take the other side of the trade. Therefore, the way markets work is the stock price goes lower, a lot lower, in order for new holders (mostly renters in this case) to take the shares off the hands of the thundering herding of ADES sellers, stampeding for the exits.

On December 30, 2022, ADES shares closed the year, at $2.43.

The next hurdle was the long-awaited shareholders vote, on the Arq merger. A majority vote was required for the passage of the merger and it was crystal clear that market participants strongly disliked the terms of the deal.

Lo and behold, a second time, the narrative of the Principal-Agent problem arose. To make a long story short, ADES's management restructured the terms of the Arq merger such that they were more favorable to the original terms, for ADES shareholders, however, in doing so, they cleverly circumvented the shareholder vote. I don't want to waste too much bandwidth on the legal maneuvering that took place, all of which was 100% legal.

However, by circumventing the vote, this further enhanced the narrative and perception that management had an Agency problem.

Lastly, on May 9, 2023, given the crash in calendar Q1 2023 spot natural gas prices, driven over production, production that was chasing $6 and $7 MMBtu gas prices, after the Ukraine war scarcity premium, and a very warm winter, ADES reported a very poor Q1 2023 quarter. Specifically, ADES reported a Q1 FY 2023 Adj. EBITDA loss, of $7.7 million. That said, $4.4 million out of the $7.7 million of Adj. EBITDA loss was from one-time "transaction and integration costs incurred related to the Arq Acquisition".

Here is the issue, though. The current shareholder base is highly fragmented, and the marginal holder is mostly a 'renter' and not an 'owner'. With the stock at an all-time low, very few holders are inclined to trust management. This negative sentiment is very powerful and the entire shareholder base needs to turnover, to a new base, that wants to invest in this business for FY 2025 (and beyond positive Adj. EBITDA).

In the near term, it is a very tall order, given the sequence of events, and perception of Agency Bias. Candidly, this cynical perspective has been well reflected by SA Contributor, Henrik Alex, on February 1, 2023 and most recently, on June 15, 2023.

Seeking Alpha

Although, I completely disagree with Henrik's June 15, 2023 article, and I'm aggressively betting against his view, by loading up on ADES shares, I acknowledge the negative sentiment, which is well reflected in ADES's current share price. Further, I recognize ADES's management hasn't done a good job of telling the story and courting a new buy and hold buy side base, as the go-forward story is actually highly compelling, notably more so in light of this ridiculously low valuation, at $1.25 per share.

The Go Forward Story

As we've reached the 1,500-word mark, I appreciate the readership's patience and I thank them for letting me provide the necessary backstory and context. However, given my long pre-ample, I'm going to cut to the chase on the ridiculously compelling opportunity, at $1.25 per share.

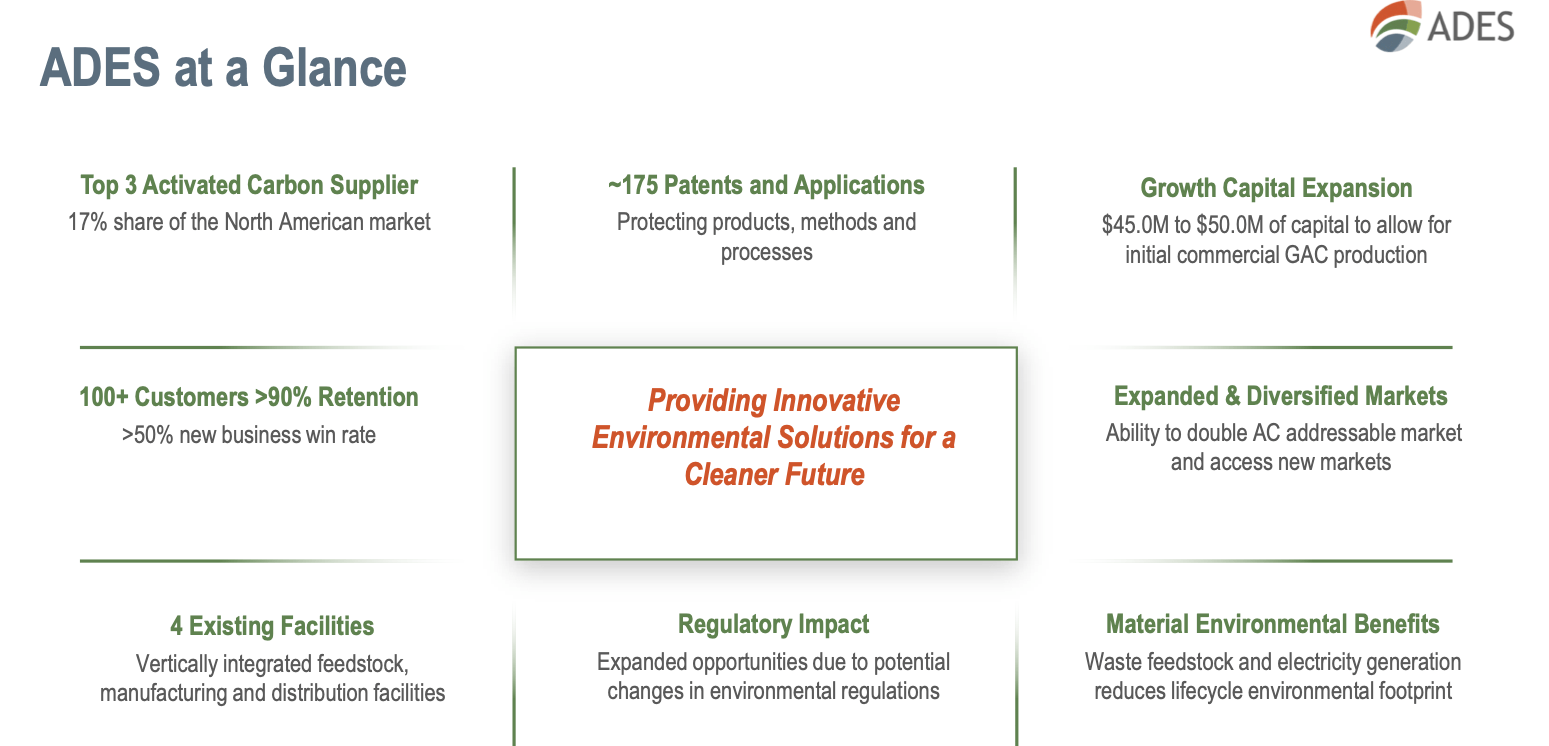

Let's start with valuation. There are 33 million fully diluted shares. $1.25 per share x 33 million shares equals a market capitalization of $41.25 million. As of March 31, 2023, ADES has $68 million of cash, plus $11 million of restricted cash, and $20 million of long-term debt. The company's net working capital is positive, to the tune of $85 million.

The company is in the process of upgrading its Red River Plant, Louisiana as well as enhancing its Arq's Corbin, Kentucky plant with the express goal of enabling Red River to produce granular activated carbon. Red River currently has a nameplate capacity to run 150 million pounds of powder-activated carbon. The Capex investments are phrased over the next two years, and total CAPEX is estimated to be roughly $95 million.

For perspective, when it was originally built, in 2009, it is estimated that the total cost of construction, for Red River, was upwards of $400 million. Given the dramatic increases in commodity prices and specialized labor, arguably new green field production would cost upwards of $3.50 to $4 per lb. of capacity. Moreover, it is estimated that Arq's state-of-the-art facility and patented portfolio has $200 million of capital and R&D dollars invested.

So if you take a step back, we are talking about an oligopoly industry structure (powder and granular activated carbon) and a company that has upwards of $600 million of capital invested in it. Moreover, with the $95 million of phrased CAPEX investments, we're looking at almost $700 million of replacement cost capital.

As an ADES shareholder, you're an indirect owner in this enterprise, at a $41 million market capitalization!

Further, if you spent a few hours reading and understanding what management is doing, they are moving up the value stream, into granular activated carbon, with has a much larger addressable market, has very stable municipal water customers, and has a 50% to 75% higher average selling price profile, depending on the quality and specifications of the contract/ end product. Also, one of the major advantages ADES has, by acquiring Arq was accessing a 30-year supply of bituminous coal feedstock, at its Corbin, KY facility. ADES will become a vertically integrated producer once it completes its upgrades to Red River and Corbin, KY. This is a huge strategic and cost advantage to its peer group, in that they now control one of the largest inputs to the overall cost of production.

{kind=link}

Risks

The biggest risks are trying to handicap the near-term Adj. EBITDA losses in light of the super-low natural gas prices. Admittedly, Q1 FY 2023 Adj. EBITDA losses were ugly, at negative $7.7 million. However, $4.4 million of those losses are from one-time merger-related costs. Secondly, natural gas prices have rebounded, off the low of $2 MMBtu with near-term spot prices back to $2.50-ish and winter months natural gas prices firmly trading in the $3s.

Therefore, the ADES bears can't have it both ways here, as very few natural gas producers can make money at $2.50 MMBtu. Further, the well decline rates in shale are super high. Therefore, albeit with the lag, production responds to incentives and you get less drilling at lower prices. Moreover, with oil prices in the low $70s, we aren't getting unbridled oil production and don't risk major casing head gas supply.

In other words, there will be coal burn, notably during the summer months. In fact, just yesterday, there are reports of blackout threats, in Texas, and it is only late June 2023.

{kind=link}

Secondly, ADES's management team needs to prove they are on point, on time, and on budget with the CAPEX upgrades. The market will be keenly attuned to this element of the story, as the earmarked cash needs to be stewarded such that valuing enhancing upgrades get across the finish line. CAPEX cost overruns and delays need to be avoided.

Putting It All Together

At $1.25 per share, you are a shareholder in a business, at a $41.25 million valuation. This is now a vertically integrated company that controls a very valuable bituminous coal feedback, has over $600 million of invested capital, that is patented protected, and they compete in an oligopoly market structure (Calgon and Norit are its two major peers). Moreover, the company has most of the required capital, already on the balance sheet, in the form of cash, that will be earmarked to upgrade Red River to move production into higher value and higher ASP granular activated carbon, from powder activated carbon.

I would love anyone else to please show me a business that competes in an oligopoly market structure, that is patent protected, that is vertically integrated, that has cash on hand to fund the CAPEX, and that has a projection for robust FY 2026 Adj. EBITDA that exceeds its current market capitalization by a factor of 1.5X.

To make a long story short, I've taken advantage of the climatic fear currently embedded in ADES's stock price and I've loaded up on my sizing here, by tripling down on my position. I would argue the risk/ reward is super skewed here and there are multiple pathways to generating strong shareholder returns, from this very diminished low current valuation.

For further details see:

Advanced Emissions Solutions, Inc.: Why I've Tripled Down In The $1s