AL - AerCap And Air Lease Corporation: The Implications Of A Credit Crunch

2023-03-22 19:29:30 ET

Summary

- Lessors have been able to pass higher interest rates to customers for which the lease has yet to start.

- 98% of the leases is fixed rate, meaning market value changes or interest value changes cannot be passed on once the lease has commenced.

- A credit crunch should not be a huge negative for airplane lessors as airplanes are long-cycle assets with good value retention.

With the turmoil in the banking sector, fears of a credit crunch have been rising . A credit crunch is a tightening in lending standards among banks that can make loans more expensive to finance and in some cases even unavailable due to a change in risk profiling and risk appetite. In 2020, we saw the debt markets becoming inaccessible and the Fed had to intervene with an emergency program to keep the bond market open. I don’t believe the current turmoil in the banking sector is going to be creating a dislocated bond market as we saw previously, but for very cash intensive business that finances purchases with debt even a modest morphing of the risk appetite could have consequences.

One of those businesses is the aircraft financing business with companies such as AerCap ( AER ) and Air Lease Corporation ( AL ). In this report, I will discuss several items regarding the aircraft leasing dynamics, namely:

- The impact of airplane market value on lease rates.

- The impact of interest rates on lease rates.

- The impact of credit tightening on lease rates.

The Lag Effect Of Airplane Lease Rates Catching Up To Market Value

{kind=link}

AerCap

When the pandemic resulted in almost all of the airlines halting their operations, it resulted in 90% of the fleet being grounded. The demand and supply imbalance for commercial airplanes was clear. Airplane leasing companies had a choice to make, further amplify that imbalance by pulling airplanes from airline fleets over non-payment or accept lower payments reflecting the reduced demand for air travel for a short duration. Lessors chose the latter by lowering the lease rates, but extending the lease duration and future lease rates. That way lessors kept receiving money and it was not seeing an even higher pressure on market values.

From 2019 to 2023, the base values of the Airbus A320neo, which will be used as an example, has risen around 1.1% to 1.75%. So, that's nowhere in line with inflation. The base value is the value of the underlying asset in an undisturbed market. Clearly, the past years have not been undisturbed at all, but we're seeing that OEMs have been able to close the gap between the market value and the base value. In 2019, the market value of an Airbus A320neo was around 1.2% lower than the base value. By now, driven by supply chain imbalances, the market value is around 2.9% higher than the base value. Overall, the market value has been better able to track inflation with a 9% increase in prices compared to a 17.7% inflation rate since 2019.

So, higher values of the asset should drive higher lease rate. However, what we do see is that between 2019 and now, lease rates have only risen 7.5% which is in between the base value and market value appreciation of the airplane. However, what should be kept into account is that lease contracts typically are agreed on a year in advance, so it makes sense to look at the market value one year ago. When doing so, the lease rates have increased 13% while the market value has increased by 4%.

The Impact Of Interest Rates On Airplane Lease Rates

{kind=link}

AerCap

Now there's a factor that complicates things further or should at least make us aware that lease rates might just be at the start of going up significantly. Because while only new contracts take into account changes in the market value of the airplane, the contracts also have interest rate escalators.

If you purchase an aircraft directly from the OEM, there are certain escalators involved and the same holds for lease contracts meaning that while a lease rate has been agreed on a year ago that lease rate can still be corrected for changes in interest rates, which is a big difference with changes in market values that are not captured until a new agreement is signed. Only 2% of the lease rate is a variable rate lease in which adjustments can be made when the lease is already in effect. For the remaining 98% this cannot be done, which means there is an interest rate risk to aircraft lessors.

Typically, 70% of the value of the airplane is influenced by the interest rates or said differently 70% of the airplane value is financed with debt. For an airplane like the Airbus A320neo it means around $36.5 million is sensitive to the interest rate environment. That part has to be amortized over a year indicating around $0.25 million per month multiplied by the change in applicable interest rates.

Just giving you an example the rate is currently 4.58% up 4.5 percentage points in a year and it will go another .25 percentage point higher after the most recent Fed meeting but sticking with 4.5% that would mean that there is some impact on for instance the seven-year swap rate which needs to be compensated for, the seven-year swap rate is up 1.27 percentage points in the past indicating that lease rates should have risen at least 12.5% from a year ago.

The actual rise is 12.9% compared to the 12.5% required, but I would attribute that to rounding mostly. So, what we do see is that without issue lessors are able to pass the lease rates on to the customers. What is less reflected is the improved market appeal and value for aircraft, but that will take a while to be translated into the marketplace because a lease agreed on now, with a bit of luck will be delivered next year at the earliest.

The Impact Of Credit Tightening On Airplane Lease Rates

The impact of credit tightening is nearly impossible to quantify. Generally the lessors have strong credit ratings so I would not directly see a reason for risk aversion toward loaning toward lessors. For some airlines, higher interest rates are bad and they might have more struggles to secure funding and that also holds for any credit tightening that might occur but that could make the option of leasing more appealing to them and the added risks that lessors would have with these customers would be absorbed via higher deposits and there is a big pool of lessees who actually are not at risk. So, I don’t see a big risk there.

{kind=link}

AerCap

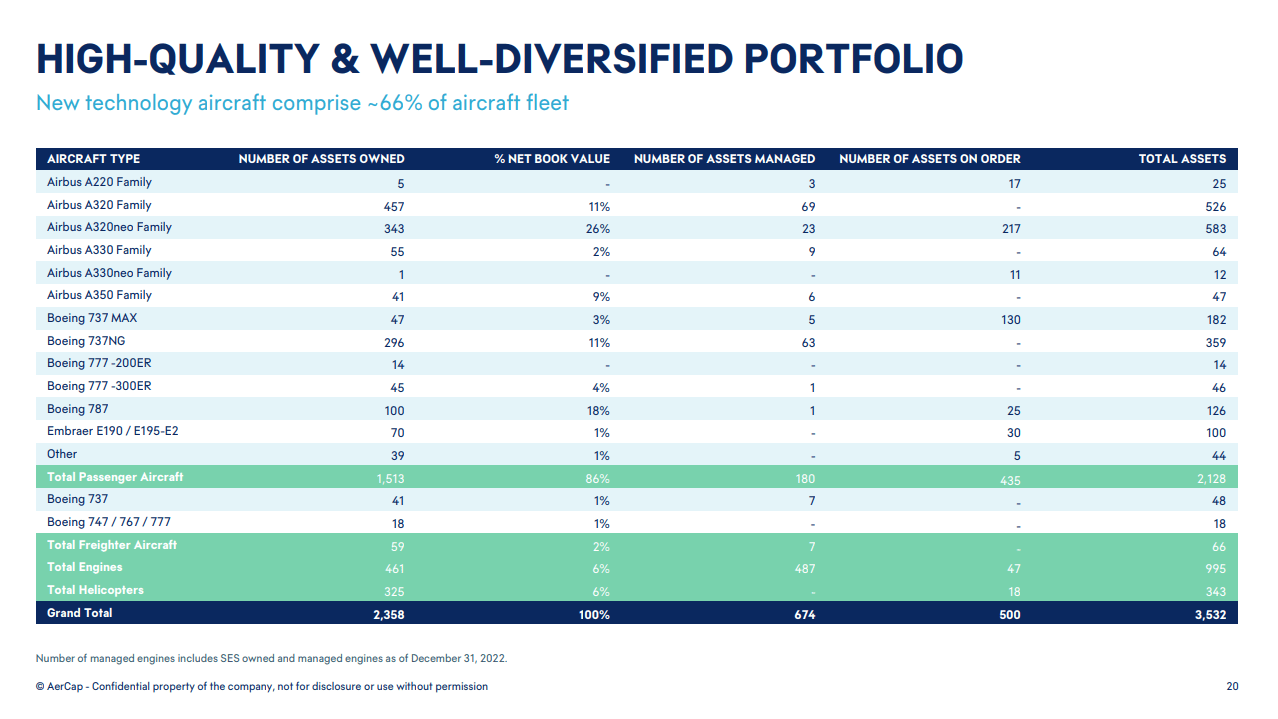

In fact, lessors have a big advantage and that's because they have a huge pool of flight equipment that they are managing well. AerCap says its share of new technology aircraft compromises 66% of the fleet. My definition of new technology might be somewhat different, so I only get to 46% but what is important to consider is that the company does not focus on old-technology aircraft but is focusing on new technology aircraft that have better value retention. That's something we also saw during the pandemic when older technology aircraft saw market value declines up to 45% while this was less than 10% and often even less than half of that for new technology single aisle jets.

Consequently, the focus on new technology assets should mean that financing at relatively attractive terms that can be passed on to the lessee should remain available in times of credit tightening. Even more so since the assets have an economic life cycle of at least 25 years and AerCap can proactively manage the attractiveness of its portfolio by selling older generation jets which it also does with gains of sales realized frequently.

{kind=link}

AerCap

Testimony to the success of the aircraft management strategy is that at the absolute worst moment that we have witnessed for the industry, namely the pandemic, asset impairments were only $1.1 billion or 8.5% of the flight equipment value driven by wide body aircraft impairments for the Boeing 777 and Airbus A330. The risk of impairment is virtually always there, but generally the risk on these long-cycle assets is minor.

How Many Aircraft Does Aercap Own?

At the end of 2022, AerCap owned and managed 2,128 passenger airplanes, 66 freighter airplanes, 343 helicopters and 995 engines.

Conclusion: Credit Tightening Is A Risk, But Lessors Will Manage

I cannot say that credit tightening is no risk for lessors, because simply from higher interest rates they are already experiencing some risks but these can be passed on to the customers who have yet to take delivery of airplanes. An analysis of the lease rates shows that market value appreciation will take a while longer before it is reflected, but interest rate increases have almost 1:1 been reflected in the lease rate when considering the part of the asset value that is impacted by interest rates.

With the long-term nature of the contracts, the long-cycle nature of the asset and the asset retention qualities I don’t think that in a rational assessment lessors should be given a hard time to securing funding to finance commercial airplanes. As a result, I maintain my buy rating for AerCap and Air Lease Corporation stock.

For further details see:

AerCap And Air Lease Corporation: The Implications Of A Credit Crunch