EADSY - AerCap: Buy Your Own Airplane And Collect Cash

2023-08-02 10:10:53 ET

Summary

- AerCap Holdings is a strong investment opportunity to capitalize on the recovery in air travel demand.

- The stock has shown outsized returns, up over 125% since the pandemic, outperforming the broader markets.

- AerCap's adjusted net income beat analyst estimates, showing a 28% expansion of profits year-over-year.

AerCap Holdings N.V. ( AER ) is my favourite investment opportunity to capitalize on the recovery in air travel demand. The company is free of some of the pains that airlines face and has streamlined rental collection from long-life assets that are now more in demand than ever.

Since I marked shares a buy during the pandemic, AerCap stock has shown outsized returns for shareholders, validating my buy thesis for the stock. The stock hasn't let me or my portfolio down a single time since I added shares. In this report, I look at the stock price performance as well as the company's most recent results, and I will provide an update to my price target for AerCap.

AerCap Stock: A Strong Outperformer

Seeking Alpha

AerCap stock has not disappointed me one day. I don't regret buying shares of the Ireland-based lessor, and if I had any regret, it is that I did not buy more. Since I wrote about AerCap in 2020, share prices have surged. The stock is up over 125% more than easily outperforming the 56% return for the broader markets, supported by strong long-term demand for air travel and a recovery towards that trendline.

In March, stock prices started weakening somewhat as General Electric ( GE ) started capitalizing on its stake in the lessor. That unwinding process does put some pressure on the stock as more shares come in circulation unless met with a repurchase for AerCap, but the underlying business keeps improving.

AerCap's Adjusted Income Shows Strength

When analyzing companies, one of the things that I do pay attention to is the way the presentation is structured. AerCap generally has a very informative and well-structured presentation. Last quarter, the company chose to put significant emphasis on recycling value for shareholders. While I wasn't a big fan of the way AerCap presented it, the reality is that the company is booking gains on sales and AerCap's presentation does not quite provide a detailed discussion on how the business is performing while there actually is a comparable period for comparison now with the GECAS business included.

| Adjusted Revenues AerCap |

| Q2 2023 |

| Q2 2022 |

| Change |

| Basic Lease Rent |

| $1,602 |

| $1,514 |

| 6% |

| Maintenance Rent |

| $185 |

| $156 |

| 19% |

| Total Lease Revenue |

| $1,787 |

| $1,669 |

| 7% |

| Net gain on sale |

| $166 |

| $35 |

| 372% |

| Other |

| $41 |

| $71 |

| -42% |

| Total |

| $1,994 |

| $1,776 |

| 12% |

When adding back the purchase accounting practices which do deform the reported numbers on top and bottom line but not the actual business operation, we see that year-over-year the basic lease rent increased by 6% up from a 2% decline in the previous quarter while maintenance rent increased by 19% for a 7% higher total lease rent and including gains on sale and other revenues the total top line increase was 12%. The surge in gain on sale can be explained by the strong market for selling flight equipment which boosts the volumes as well as the value of the assets.

{kind=link}

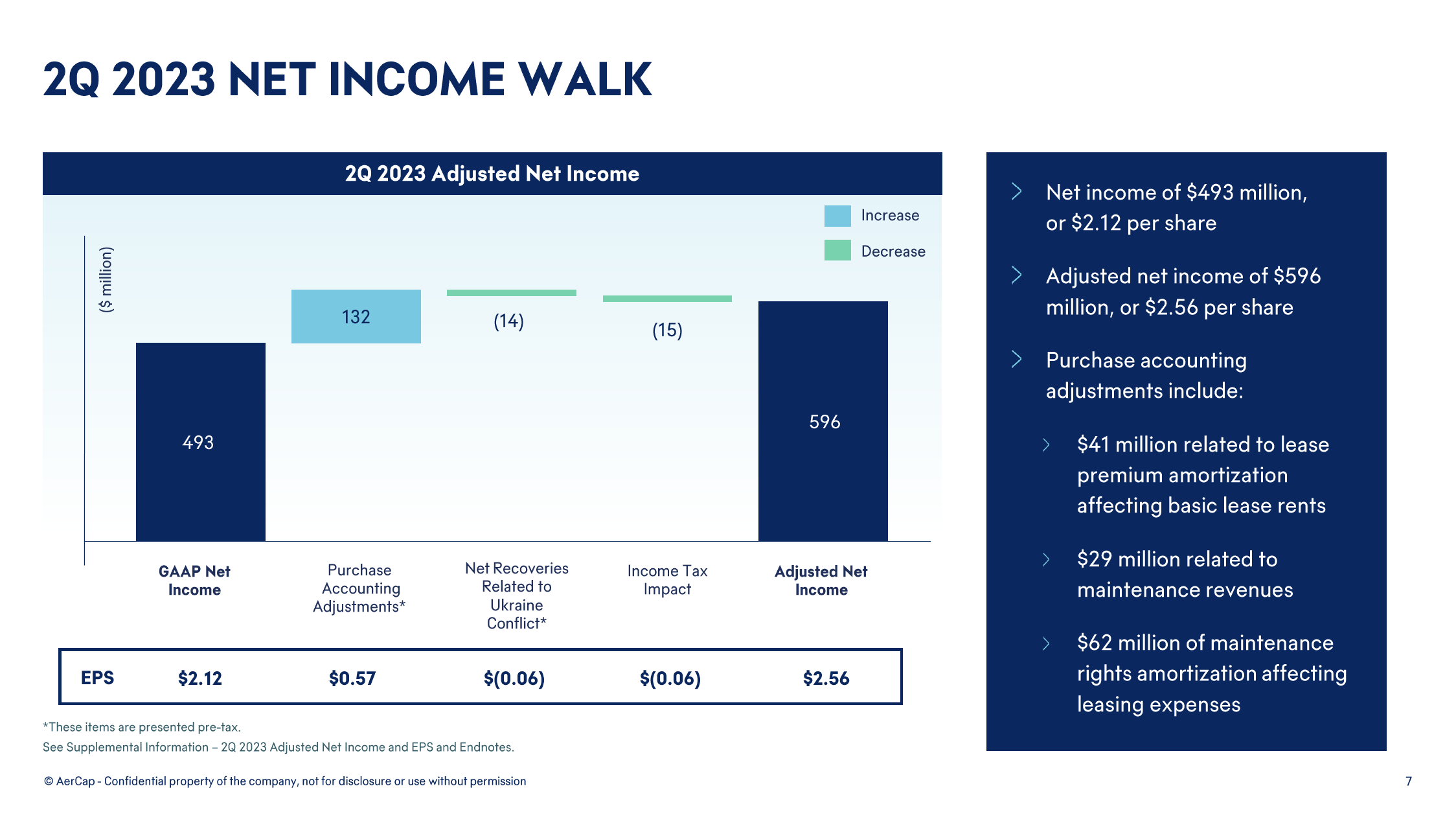

GAAP reporting requires AerCap to amortize certain items related to the acquisition of GECAS at an accelerated pace, which significantly affects the company's income. These are non-cash items that are required but don't really affect the underlying performance of the company. Therefore, looking at the adjusted net income makes a lot of sense. Adjusted net income was $596 million or $2.56 per share, beating analyst estimates by $0.50 which is a strong beat and provides a 28% expansion of profits year-over-year and a 5.3% sequential increase.

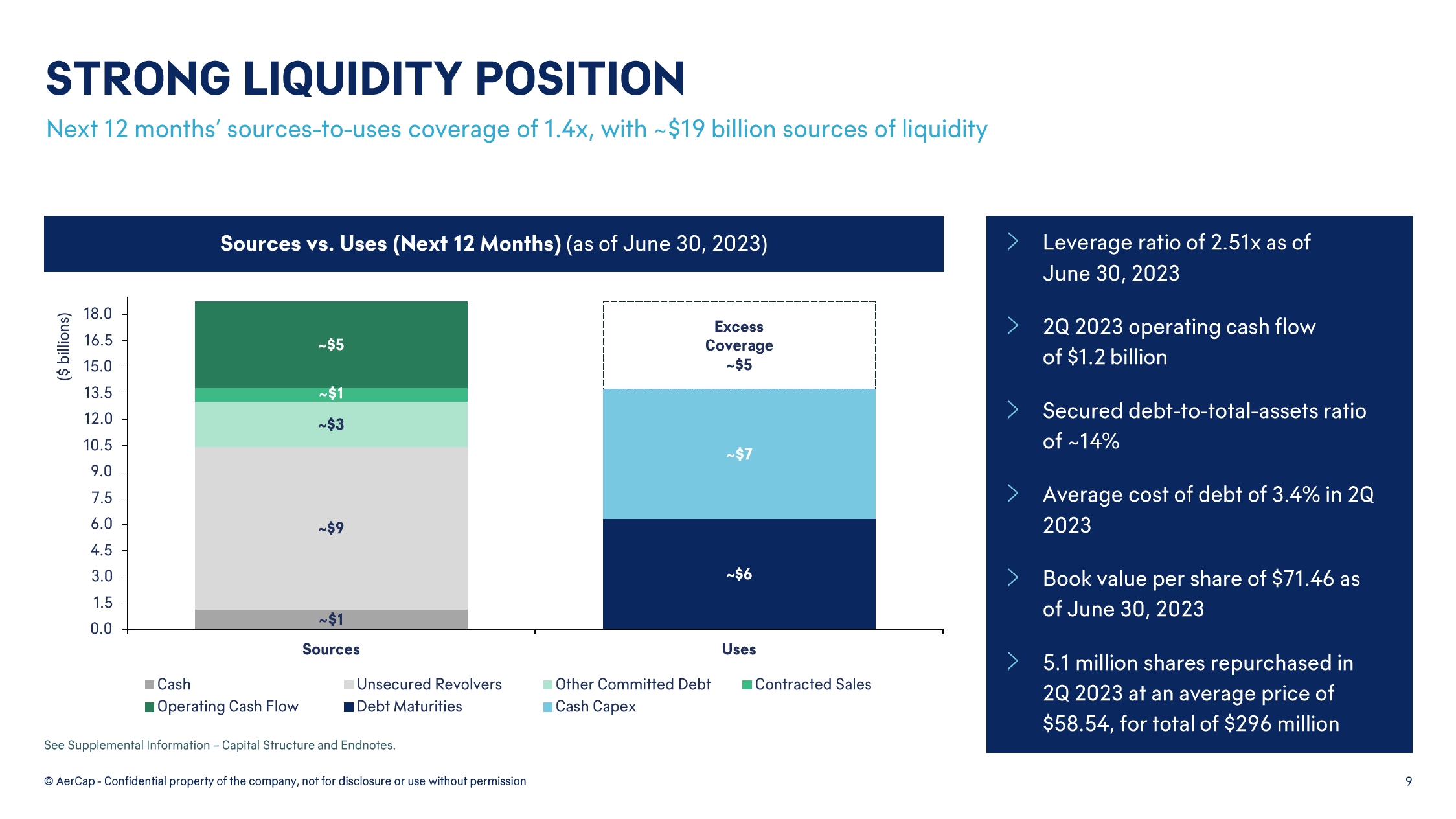

AerCap's Liquidity Position Remains Strong

{kind=link}

Sequentially, the excess overage increased by $1 billion driven by an increase in committed debt in the coming 12 months and lower debt maturities. The sources-to-uses ratio contracted slightly from 1.4x from 1.3x while cost of debt increased to 3.4% compared to 3% a year ago, but that is to be expected in a high interest rate environment.

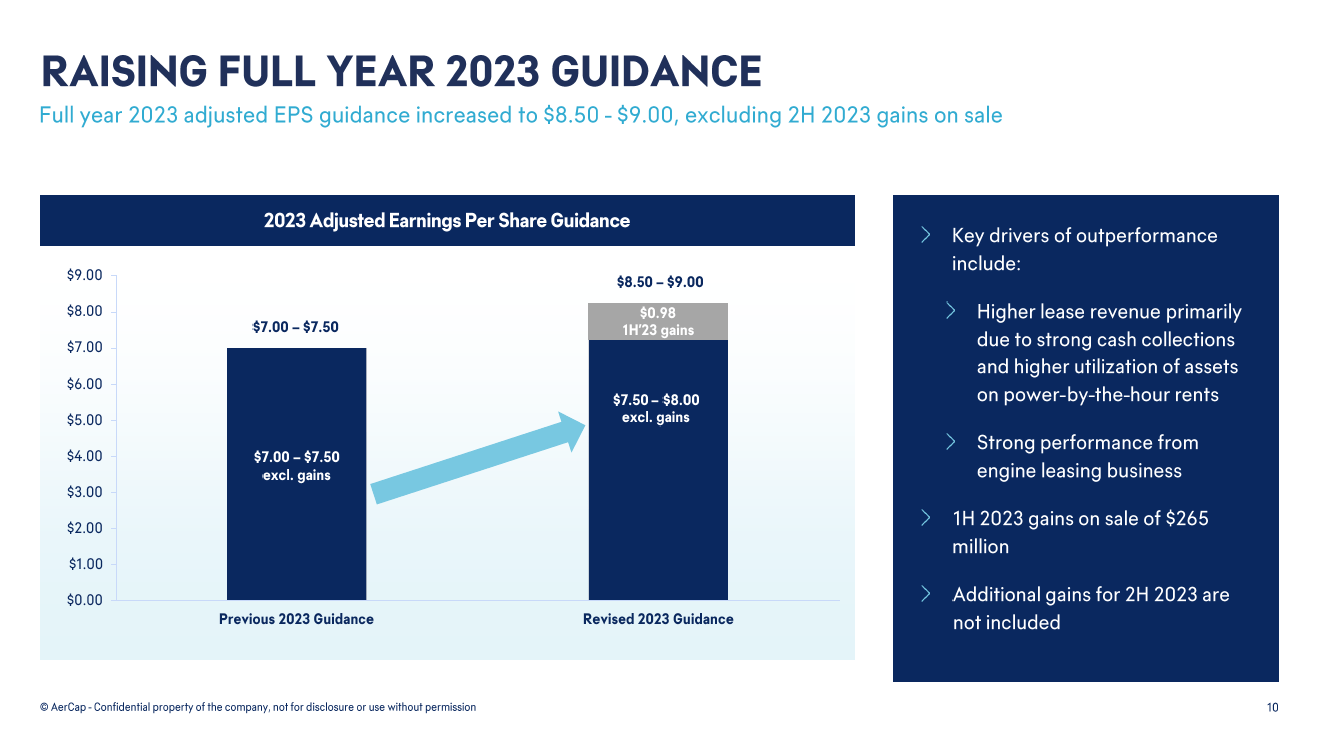

AerCap Guides For A More Bullish 2023

{kind=link}

During the second quarter, AerCap beat expectations by $0.50 per share which looks like a strong beat, but it should also be kept in mind that around $0.72 of earnings per share came from gains on sale which AerCap does not guide for. I previously already estimated that around $1.60 per share to $2.15 per share could be added to the EPS by the inclusion of gains on sale. While analysts likely include some gains on sale, the lack of guidance on this item line makes beating the estimates somewhat easier. However, we also see that the guidance excluding gains has been stretched by $0.50 per share on higher lease revenues and asset utilization as well as the engine leasing business performing well. So, there is strength in the underlying leasing business as well as strength in the disposal of flight equipment held for sale.

Is AER A Good Stock To Buy?

{kind=link}

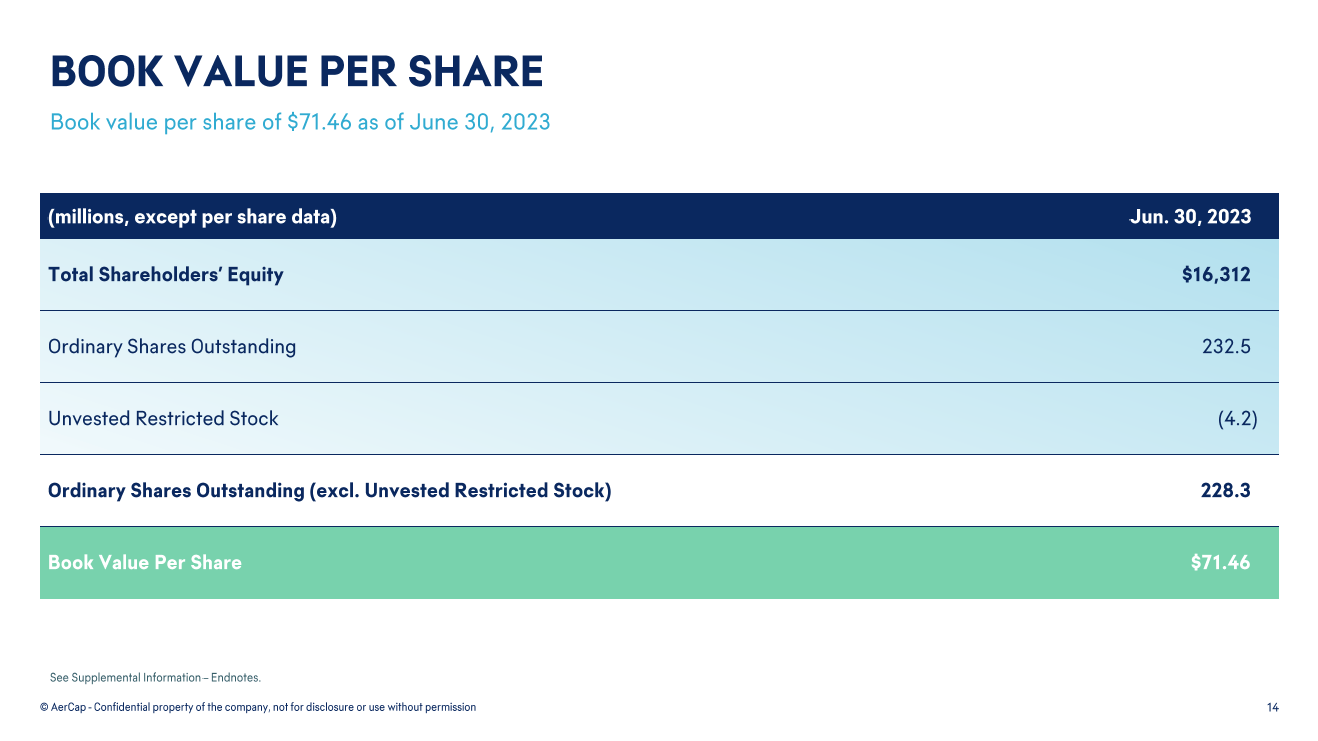

Compared to its book value per share, AerCap is trading at an .90 price-to-book value. However, the $3.3 billion discount that AerCap received when acquiring GECAS is not reflected in this. To adjust for this, we add the $3.3 billion back and apply depreciation to this. By doing so, we get an adjusted book value of $84.70. Normally, I apply a discount to the book value of around 14%, which was in line with the discount to book value that we saw prior to the acquisition of GECAS. With that in mind, I believe AerCap shares should be trading at $72.84 at this moment providing 12% upside. Interestingly, AerCap's price-to-book has normalized from elevated levels of 1 to around .9 more recently. However, with that, the market does not appreciate the discount to NAV that the lessor negotiated with GECAS as this discount is not reflected in the book value. If AerCap were to trade at elevated book values again reflecting the full book value, the price target would increase to $84.70 representing 31% upside.

Furthermore, AerCap's share repurchase program also adds upside to the stock which could boost the book value per share to $85.60 and the stock price target to $73.62. I would consider the lower of both values to be the value that AerCap should be trading at right now and the high value to be the longer-term target.

The Risks Of Adding The GECAS Acquisition Discount Back

While adding the discount to NAV that AerCap secured when acquiring GECAS does make sense, a few things should be kept in mind. Adding the full $3.3 billion discount back is the easy way to do things, but I believe that in the same flight, equipment is depreciated, the value of the discount to NAV should be "depreciated" as well which introduces some uncertainty as assumptions need to be made. At the same time, we don't know when GECAS flight equipment is being sold and at what price point. When that happens, we should remove that part from the discount as well, and with the information that the lessor provides, we cannot do this with certainty. So, we should keep in mind that while adding the discount to NAV back, there are some risks and uncertainty involved.

AerCap Announces New Share Repurchase Program… Another One

The good news that AerCap brought is that it has put in place a new $500 million share repurchase program. AerCap's stock tanked earlier this year as GECAS started unwinding its stake. General Electric received 111.5 million in shares when it sold GECAS to AerCap. In March 2023, AerCap announced a $500 million share repurchase program which was fully used to buy back shares from General Electric which brought back 23 million shares to the open marked. In April 2023, another $500 million repurchase program had been announced which of which $143 million remains unused at present and another $500 million program has been announced on the day the Ireland-based lessor shared its second quarter results. While AerCap made a big deal about buying back shares at a discount which actually was the typical discount, as long as the price-to-book ratio is lower than zero, buybacks are extremely effective in buying back shares especially when that happens with cash gained on asset sales.

Conclusion: AerCap Stock Remains A Buy

I maintain my view on AerCap as a strong buy, driven by strong gains on sales and the positive aircraft lease environment coupled with share repurchases I do believe that at present shares should be trading at $73.60 with a longer-term target of $85.60 which includes share repurchases and AerCap stock being valued in line with its book value.

For the second quarter, we saw a 12% increase in adjusted revenues and a 28% jump in adjusted earnings. Those are results that were not quite highlighted in the presentations but show the strong execution and demand environment.

The business remains strong, and while rental revenue growth might be somewhat soft as Boeing ( BA ) and Airbus ( EADSF ) struggle to deliver airplanes, the flight equipment on the books is worth more these days allowing for higher gains on sales and better lease terms for new lease contracts which has been a tailwind and lifted the 2023 outlook and likely will also be a growth driver towards mid-decade when we should see more normalized production rates.

For further details see:

AerCap: Buy Your Own Airplane And Collect Cash