LHX - AeroVironment: The Market Is Likely Wrong Again

Summary

- Similar to 2018, AVAV trades at 50x EV/EBITDA, with rapid growth expectations. We believe the market is egregiously overvaluing AVAV. Again.

- Similar to 2018, expectations for the AVAV Switchblade are stratospheric. Switchblade sales and profitability are likely to disappoint. Again.

- Similar to 2018, investors are enthusiastic about growth outside the core products. We think AVAV will continue to struggle to grow outside its niche. Again.

- This article covers why we believe the market is unjustly overvaluing AVAV - risk reward is skewed heavily towards the downside. Strong Sell.

Investment Summary

AeroVironment ( AVAV ) (hereto "AVAV", "the company", or "AeroVironment") is a manufacturer of small and medium unmanned aerial systems (UAS). The majority of sales (65%) are to U.S. military customers, the remainder of sales are international militaries and governments. As of FY 2022, small UAS products that perform surveillance make up 40% of sales and tactical missile systems ((TMS)), comprising entirely the Switchblades products, make up 17% of sales. The remainder of the sales are from the larger, medium-sized UAS business recently acquired from Arcturus in 2021 , and high-altitude UAS in conjunction with SoftBank. The small UAS business is the only meaningfully profitable business and is experiencing deteriorating sales over the past three years. This segment recently reported a $32 million EBITDA out of the total $31 million EBITDA for the company in FY 2022. As a pure-play UAS company, AeroVironment suffers from participating in a low-moat, low barrier-to-entry, cyclical segment of military budgets.

First, the recent acquisition of Arcturus (medium-sized UAS) is shaping to become an expensive, value-destructive acquisition. The company's struggle to expand outside of their niche is reminiscent of their marketing to push into the commercial UAS markets in 2018. Investors took this story to heart and drove up share prices. We do not expect the company will deliver on expansion promises.

Second, the TMS line has never been, and remains, unprofitable. It seems that investors are enamored by the stories of Switchblade 300s deployed to Ukraine and are running up the share price, similar to how investors in 2018 hoped the Lethal Miniature Aerial Missile System Program of Record (LMAMS) would lead to substantial Switchblade 300 sales, rather than the ultimately mediocre $60-$80 million annual contract . We believe AVAV will continue experiencing muted demand and limited profitability on Switchblade 300 (and now also Switchblade 600) sales.

Third, AVAV is not a sustainable high-growth business to justify its 26x expected FY 2023 EBITDA. AVAV U.S. based competitors, Textron ( TXT ), Northrop Grumman ( NOC ), and L3Harris ( LHX ) are all trading under expected 20x FY 2023 EBITDA, and in particular, the slam-dunk contract winner TXT is at a modest 11x FY 2023 EBITDA. Outside the U.S., AeroVironment shares intense international competition led by Turkey. Several of the company's products are simply not value-effective or strongly aligned with U.S. DoD priorities. We think AVAV's business is a high-growth facade, and that the market may be wrong to prescribe such a high multiple to the business.

This article will cover each of these points to illustrate to the reader why the bull case for AeroVironment is likely to be based on a fairy tale. The AeroVironment story is playing out like in 2018 and, unfortunately, many sequels to stories are disappointing. Out of the six Wall St. analysts covering AeroVironment , not a single one seems to think AVAV is a poor risk/reward investment. This article takes the contrarian view, explaining why we consider the market may be wrong on AeroVironment. Again.

This article concludes with a Strong Sell rating.

The Struggle for Expansion

In their 2018 Analyst Day , AeroVironment unveiled their push on their high-altitude UAS products and their commercial applications, particularly for agriculture and telecom. A joint venture with Japan's SoftBank in high-altitude UAS was announced and investors were all too eager to associate AVAV's future to the larger, higher-margin commercial sector. None of this panned out, and AVAV has since exited the commercial business as well as the JV with SoftBank.

Gross margins for the company have dropped from a consistently low 40% over the past five years to less than 30% recently. EBITDA margins have dropped from consistently around 15% to less than 10% recently. Return on Capital has dropped from high single digits to negative territory.

These metrics are not indicative of a company with growing competitive advantages. Management has laid the blame on current market conditions regarding shortages on parts and labor, and while this is generally true for most businesses in the defense industry, AVAV's margins have been declining since 2018. The simpler reality is that UAS capabilities are not a high priority for the U.S. DoD.

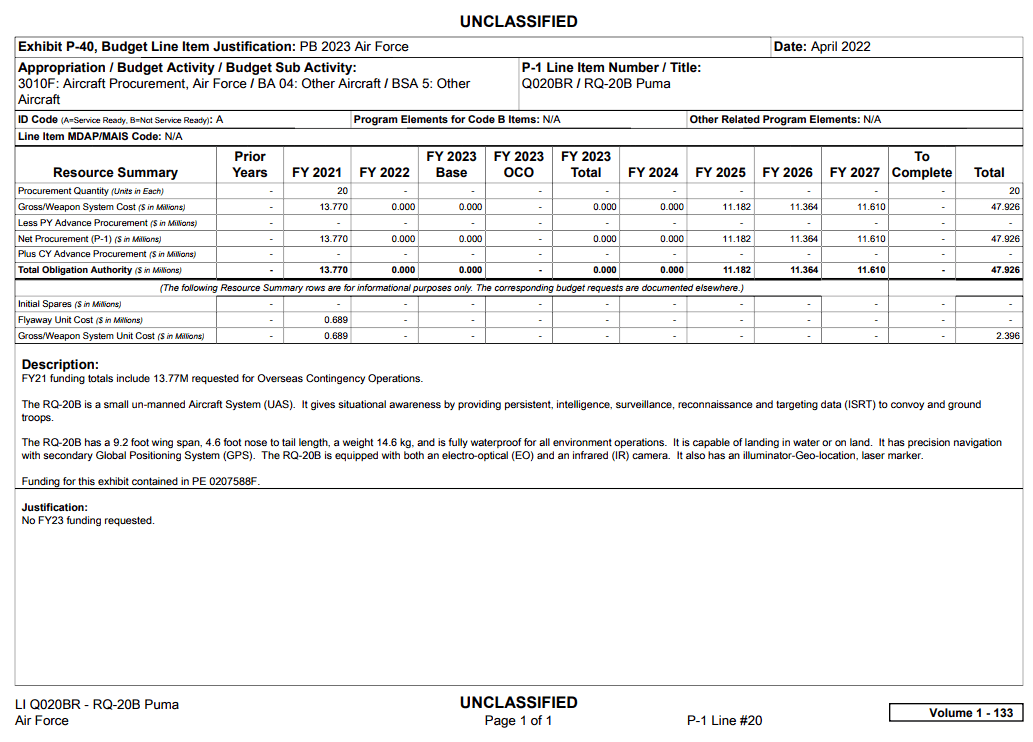

In the FY 2023 U.S. Department of Defense budget, procurement and modifications for aircraft-related systems totals $3.1 billion for UAS . This includes General Atomics MQ-9 Reaper drones and MQ-1B Predator drones, and Northrop Grumman MQ-4C Triton drones. AVAV's small UAS business appears destined to continue its cyclical, bulk delivery nature to replenish U.S. stockpiles without much growth. For example, the U.S. Air Force has budgeted $33 million out to FY 2027 for the AeroVironment RQ-20B Puma.

Air Force Budget Item for Puma (Air Force Budget Comptroller)

{kind=link}

In 2021, AVAV acquired Arcturus to expand their product portfolio. Company management had the foresight, this time, to stay within the defense sector and provide a diversity of products within the company's niche UAS offerings. Unfortunately, management did not have a good pulse on the strategic direction that the U.S. Department of Defense was headed. This is reflected by the accelerated amortization costs of their acquisition: $37 million in FY 2022 to $6.1 million in Q1 FY 2023 and $9.5 million in Q2 FY 2023 as the company has had to write off more than they anticipated upon acquisition due to the U.S. DoD's clear shift away from funding larger, more expensive Group 2 and Group 3 (i.e., larger) UAS solutions. Bullish investors may shrug off such non-cash expenses and focus on the EBITDA numbers, but the larger issue is that this is indicative of management constantly misinterpreting the direction and needs of its primary customer base.

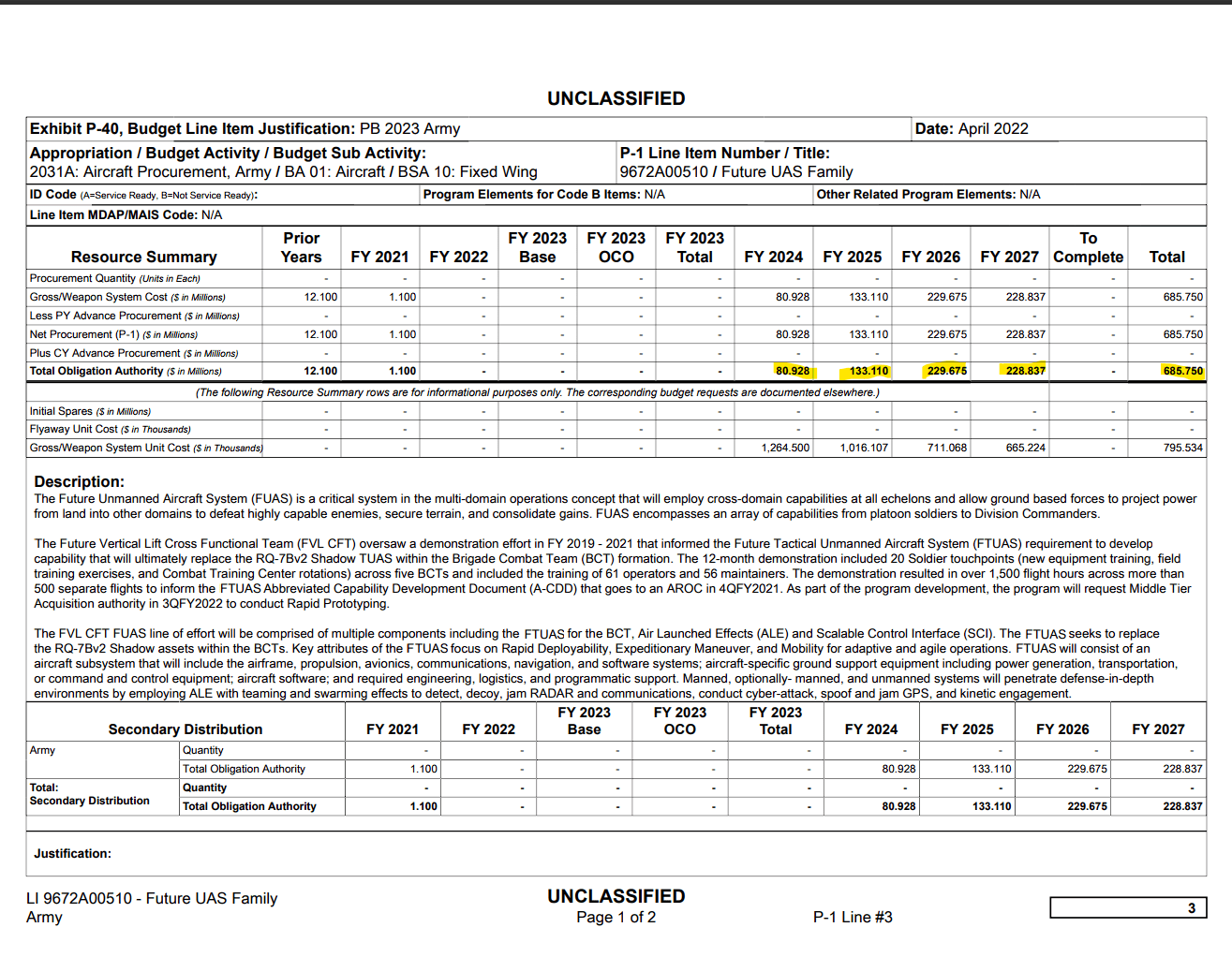

The Arcturus acquisition was motivated largely in part by competition for the Army's Future Tactical Unmanned Aircraft Systems (FTUAS) program. The purchase was done for $405 million , which the company stated was at a trailing twelve-month 11.6x EBITDA multiple on $84 million of revenue, or $35 million of EBITDA. In FY 2021, AVAV delivered $70 million in EBITDA and has guided for $74 - $82 million in EBITDA in FY 2022. This suggests that the acquisition's incremental growth of $4 - $12 million in EBITDA came at closer to a >50x EBITDA multiple. Most of the drop is due to the Arcturus's interim revenue from their FTUAS phase 1 win, which included one-off services on top of delivered goods, phasing out as the Army prepares its final phase 2 competition. The phase 1 competition included Arcturus (now AeroVironment), L3Harris, Textron (the incumbents), and Northrop Grumman. The phase 2 competition pool expanded to include several private companies, with a winner expected to be declared in mid-FY 2025 and production expected in FY 2026.

With a price tag of $405 million, AeroVironment's acquisition will prove to be extremely expensive if they do not win this contract. However, even if they win, FTUAS will provide incremental value at best. The selection timeline coincides with the 2022 Army budget line item for the FTUAS, which indicates a total of $686 million by the end of FY 2027 (i.e., October 2028).

Army Budget Line Item for FTUAS (Army Comptroller Budget Material)

{kind=link}

The production revenue awarded to the winner begins in FY 2025, thus $460 million over two years would be awarded solely to AVAV should they win. Generously prescribing a 20% EBITDA margin - which would be a company record - to this contract amount provides AVAV with $96 million in incremental EBITDA over two years, or $48 million a year. Using the company's record EBITDA from FY 2021 of $70 million, the company would generate $108 million in of EBITDA in FY 2026 and 2027, or about 20x EBITDA multiple to arrive at the current market cap of $2.15 billion - or $86 per share, around the current stock price. Assigning a multiple of 30x EBITDA, which I think is an egregious level, would lead to a value $130 per share.

The prospective investor would be betting on 1) winning a heavily competed contract and 2) rerating the valuation multiple even higher to 30x in order to justify a 53% increase in their investment at the current price of $86 a share. Should the market come to its senses, and/or the company loses out on the FTUAS contract, AVAV stock could rerate down to 15x of $70 - $80 million EBITDA, dropping over 40% in value to around $45 per share. The 15x EBITDA multiple would put it closer to its peers that are direct competitors to the FTUAS program. These competitors also have additional business lines with strong moats targeted to different facets of U.S. Department of Defense priorities

| Company |

| AVAV |

| TXT |

| NOC |

| LHX |

| FWD EV/EBITDA |

| 26 |

| 11 |

| 20 |

| 15 |

One could argue that AVAV deserves an even lower multiple given the business ex-FTUAS opportunity, and while we would agree, this just further demonstrates - in our opinion - the ridiculous valuation given to AVAV.

Switchblade is Not the Answer

In 2018, AeroVironment was awarded their first significant order for the Switchblade 300 , due to the LMAMS program. Shortly afterward, the share price soared from $55 to $120, or high 40x LTM EBITDA, similar to current valuations. Since then, the TMS business line sales amounted to $64 million in FY 2020 to $76 million in FY 2022, unprofitable both on an EBIT and EBITDA basis each of those years. Contrary to what media coverage of the Russo-Ukraine war might suggest, the bulk of AVAV's expected FY 2023 EBITDA growth is due to an $86 million contract order from the U.S. Navy for AeroVironment's small UAS Puma product, not Switchblade products. This is because the LMAMS program is the only real purchaser for the Switchblade, and the company has not been able to substantially expand their customer base domestically for these products. Management admitted as much, indicating their heightened focus to broaden their marketing efforts internationally .

In a time when drone warfare is front and center, and the stars aligned for AeroVironment during the highly covered catastrophe of the Russo-Ukraine War, it was instead Turkey (a NATO ally) that came through for Ukraine with deliveries of the popular Bayraktar TB2 drones . The Switchblade 300 has been ineffective against tanks , though it was never intended to be; and, after the first batch of 400 Switchblade 300s, no additional munitions were sent to the front lines. President Zelensky has instead pressed the U.S. for heavier anti-tank munitions, such as Javelins, of which over 17000 have been sent . Bulls may argue that the Switchblades win on cost, with some reports stating the cost of each unit at $6000 , though others have estimated them to be around $70000 ; ultimately, it does not matter, since the Switchblade 300 is simply not the solution for war beyond non-state actor insurgent engagements like in Afghanistan of years past.

Enter the Switchblade 600 , a UAS that is ten times the size of the Switchblade 300, with a Javelin-like warhead capable of destroying tanks. These drones have yet to be deployed on the battlefield, but in September the Pentagon awarded AeroVironment a $2.2 million contract for 10 Switchblade 600s to send to Ukraine - implying a $220K price tag per unit. The Javelin missile, a staple armament produced by Raytheon ( RTX ) and Lockheed Martin ( LMT ), is priced at $176K per unit, which would dispel the advantages of Switchblade being a cheaper alternative solution against Russian tanks.

The primary issue with Switchblade, but broadly speaking all of AeroVironment's products, is the intense competition, especially internationally. To drive the point home, Turkey's defense ministry in December reported a record $4 billion in defense exports , helped in large part by Baykar and their popular TB2 drones (of which exports make up 98% of their revenue) following their demonstrated success in the Russo-Ukraine War. Apart from international drone-maker competition, AeroVironment also competes with conventional weaponry, such as the Javelin, without substantially differentiated cost/value to militaries.

Conclusion

The great thing about investing in the U.S. defense industry is that the U.S. customer publicly discloses what its primary goals are, and more importantly to an investor, how much it is willing to pay for procurements. Unfortunately, AeroVironment seems to be unable to grow out of their small UAS business corner.

Winning the FTUAS contract is of paramount importance, but the company's current price makes this uncertainty extremely - and unnecessarily - risky for the prospective investor. Furthermore, AeroVironment has not demonstrated the ability to expand out of its niche, leaving no way to cushion the fall should they fail to win this pivotal contract. To that end, AVAV paid $405 million for a shot on goal for the FTUAS program; and there's no other opportunity available, making this a very risky and expensive bet. Additionally, the Switchblade is a solution that still has not proven to be profitable several years after being unveiled, nor has it shown game-changing efficacy on the battlefield. Finally, growth abroad is hampered with intense, cheaper competition.

At a multiple of 26x FWD EBITDA, AeroVironment is simply far too expensive given its traditional place operating in the extremely niche, low-growth, small UAS segment of the defense industry. It is entirely possible that the market stretches AeroVironment's valuation to $120 - $130 a share, but this reward based on outstretched valuations is not worth the risk of the company value instead falling by half to more reasonable valuations on the back of a binary FTUAS competition award outcome, continued low growth, and poor profitability. There are easier companies to invest in without asking the world of them.

For investors interested in companies with drone capabilities, readers are encouraged to investigate Textron, who recently displaced Lockheed Martin for the important $1.3 billion Army attack helicopter program and has a similar shot on goal as AVAV for the FTUAS contract, but with much more reasonable valuations. For another idea, consider Northrop Grumman as another strong player in the UAS space.

Contrary to other analysts, this article concludes with a Strong Sell/Very Bearish rating on AVAV, in line with our opinion that the market is likely wrong on AVAV. Again.

For further details see:

AeroVironment: The Market Is Likely Wrong, Again