EADSY - AerSale: AerAware Is The Reason Why I Bought Back

2023-12-01 10:38:14 ET

Summary

- AerSale Corporation's Q3 financial results show significant growth in flight equipment sales, driving total revenues up from $51 million to $92.5 million.

- The demand for Boeing 757 converted freighters remains soft, with only one sale in Q3 and uncertainty surrounding leases.

- The main growth driver for AerSale is its AerAware system, which enhances flight safety and efficiency, but certification and rollout have been delayed.

The last time I covered AerSale Corporation (ASLE) was in August 2023 . Back then, I reiterated my Buy rating, and that is one that has worked out quite well, as the stock has climbed 32% compared to a 2.3% increase for the broader markets. I also pointed out that I would be interested in restarting my position in AerSale, which I ended up doing as well. In this report, I will have a look at the most recent quarterly results and provide an updated price target on the stock.

AerSale Q3 Financial Results Driven By Flight Equipment Sales

{kind=link}

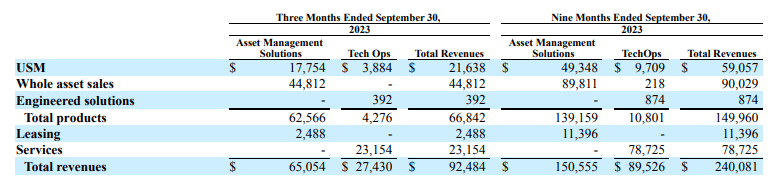

Total revenues increased from $51 million in Q3 2022 to $92.5 million in Q3 2023 driven by $44.8 million in equipment sales compared to $2.7 million in equipment sales in the comparable period last year. So, revenues increased by $41.5 million while flight equipment sales grew by $42.1 million. It is quite clear where the growth came from. Asset Management Solutions revenues climbed from $20.6 million to $65 million reflecting the flight equipment sales as well as higher USM part sales driven by demand and ability to service demand while leasing revenues declined from $7.8 million to $2.5 million. I don't consider the leasing business a major contributor to AerSale's results, but I do like the fact that the company can use its feedstock to drive the USM segment for part sales, generate whole asset sales, or put feedstock on lease. So, for each piece of equipment, AerSale can see which flow provides the highest value for the company.

TechOps results shrunk almost 10% to $27.4 million, which was driven by lower revenue from servicing aircraft in storage as the number of aircraft in storage is declining and the aerostructures and landing gear business finalized a project before starting a new larger project in Q4. While not visible on top line for TechOps, the company had some additional headspace in MRO due to the outsourcing of some of the conversion capacity for the Boeing 757 which was discussed in prior quarters.

Driven by flight equipment sales, adjusted EBITDA was $1.9 million compared to a $0.5 million loss a year ago. Overall, I like the value circulation principle used by AerSale, but an adjusted EBITDA margin of 2% is not something that gets me excited.

Boeing 757 Converted Freighter Demand Remains Soft

{kind=link}

AerSale has a feedstock of Boeing 757 airplanes that were initially intended to be sold or leased as freighter-converted airplanes. However, with softness in the end-market that has become more challenging, and the company had projected three sales and three leases. In the third quarter, one P2F Boeing 757 was sold compared to none in Q2 and one in Q1. There is one airplane contracted for sale in 2023 which would bring the company to the three anticipated sales. On the three leases of airplanes, there is no clarity, and from the earnings transcript - it seems that the company is still actively looking for buyers and lessees. So, it is just a very challenging market to bring converted freighters to the market.

In Q2, the lowered guidance for flight equipment sales sparked a decrease in revenue and EBITDA guidance, and the third quarter included some trimming on the high end of the ranges as well as revenue is now expected to be between $400 and $420 million, which is $20 million lower on the high end and EBITDA is expected to be between $40 million and $45 million, which is $10 million lower on the high end.

What Are The Growth Drivers For AerSale?

Putting it simply, the only reason why I am invested in AerSale is because of AerAware. On MRO, there does not seem a whole lot of upside to revenues in terms of capacity as AerSale is outsourcing conversion capacity to service MRO demand, and the conversion program is currently in a rather weak market environment, so I would also not look at that as a solid growth opportunity. What I do like about AerSale is that the company bought quite a few CFM56-5Bs turbofans that power the Airbus A320, and those were initially expected to be fueling the USM part sales, but those engines have service life left and have been in demand for purchase and lease. The current shortage of new engine technology airplanes provides a positive backdrop for value optimization across AerSale's channels for the legacy CFM56 engines.

The News On AerAware

The main reason - and only reason - why I am invested in AerSale is AerAware. AerAware is an EFVS or Enhanced Flight Vision System that allows pilots to look through low visibility conditions. I can see the value of this system, as it enhances safety, but also results in fewer airplanes diverting due to fog, which saves on costs. Even not having to perform a go-around - aborting a landing and climbing out for the next landing attempt - would make AerAware worth its money.

AerAware is expected to be a rather expensive piece of equipment with high margins, as AerSale tends to have very high margins on engineered products. In due time, I will be providing some estimates on the impact that AerAware could have, but I am more interested in the process of approval and initial rollout. While I am bullish on AerSale due to AerAware, the certification of that product has been something I have been hearing about for three years, and even now in the final innings, we see that while flight testing is complete getting the approval is taking longer than anticipated. Previously, from management calls, I was given the impression that once the flight tests would be completed, it was a matter of 30 days before the STC (Supplemental Type Certificate) could be obtained.

What I found interesting is that AerSale for a long time has not provided intermediate updates on the progress of AerAware certification and reserved the updates for the earnings call, and it deviated from that line in October, when it sent out a press release in which the company detailed that flight tests were completed by August 19th. The company is now engaged in a back-and-forth on paperwork with the FAA, which is taking more time than anticipated. Once that is complete, getting the STC which would allow AerAware to be rolled out could take another 30 days. In optimistic scenarios, it was expected that there could be some AerAware sales in 2023 which were not included in guidance, but that timeline seems to have slipped.

I am not too worried about that, but at this point, I would have hoped to see some details on the planned roll out. We know there were around 150-160 kits instructed to be manufactured and that bringing AerAware to the market is not just a matter of putting on the EVFS and fly the airplane, so I would like to have seen some detail on how they see the modification path ahead for AerAware installation.

AerSale: Strong Buy On AerAware Upside

{kind=link}

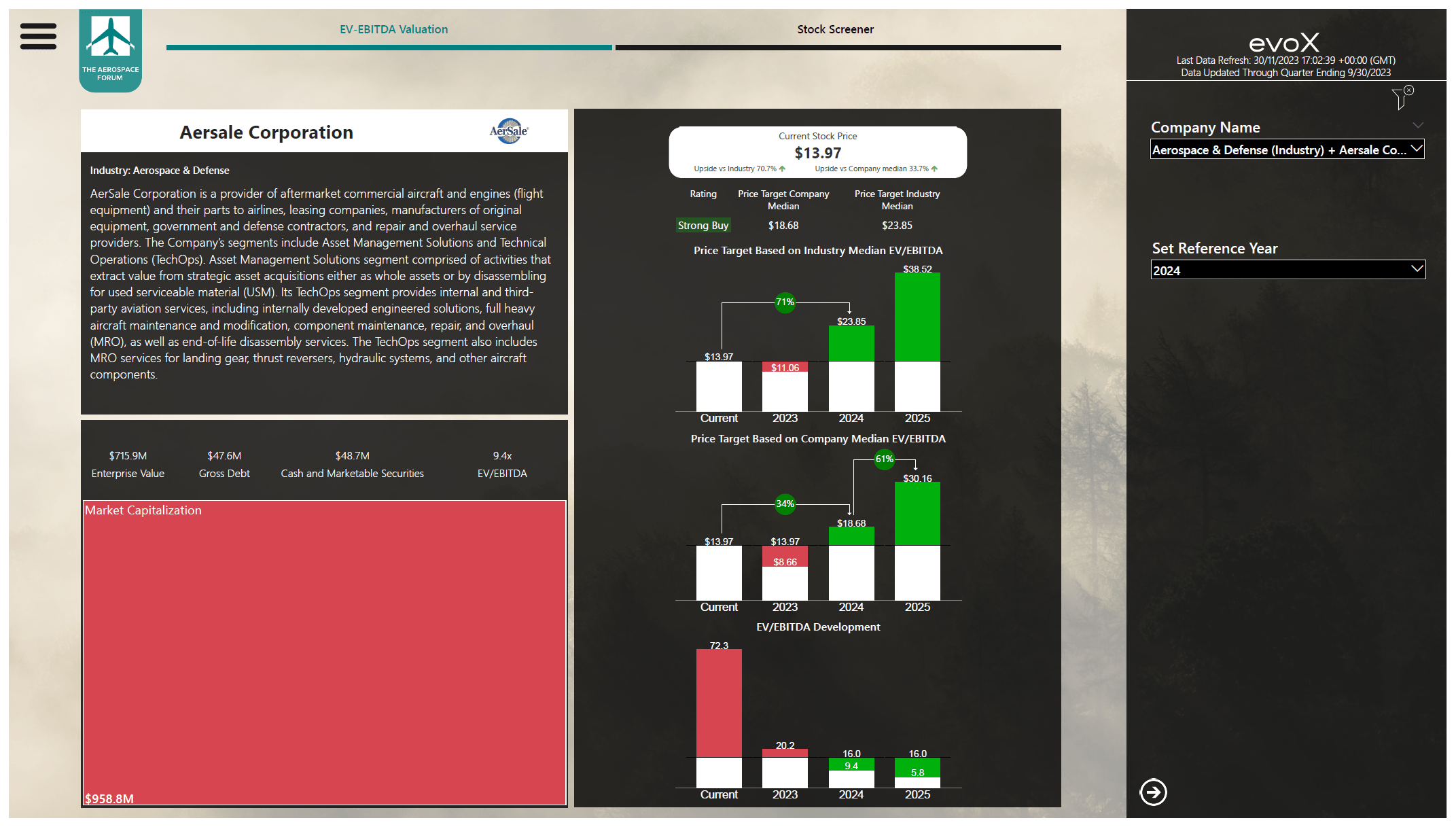

Before I repurchased the shares I initially sold, I processed the numbers for AerSale in my stock screener, which holds names for close to 100 companies in the aerospace, defense, and airline industries. Based on crunching the numbers which sees some 2023 and 2024 EBITDA sliding into 2025 and free cash flow to remain negative cumulated from 2023 to 2025, I still do see an upside of at least 34% with a price target of $18.68 and a strong buy rating. If AerSale were to trade in line with peers, that upside would be even bigger. My price target for 2024 has been reduced by $4.90, driven by a combination of lower results projected and an increase in level of detail for the modeling method used, while for 2025 the price target has been reduced by $3.05 to roughly $30.15.

The 12-month price target of $18.68 more or less coincides with the $19 per share price target that Wall Street analysts have on the higher bound of the range.

Conclusion: AerSale Is A Strong Buy, But Only For AerAware

One thing I cannot stress enough is that AerSale to me only is interesting due to AerAware. I like their business with a value circulation principle, but actually consistently generating value has been a challenge due to the lumpiness of equipment sales while MRO capacity seems to be limited and the freighter market provides a soft backdrop for converted freighter sales campaigns. While the business lines are tied together by the value circulation method, it is just not attractive to me absent of AerAware. However, I still do believe in AerAware and think it is a powerful enhancement to safety as well as operational efficiency for airlines with a significant potential to equip the world's Boeing 737NG fleet and, in the future, other airplanes as well.

For further details see:

AerSale: AerAware Is The Reason Why I Bought Back