EADSY - AerSale Stock: A Disruptive Buy

2023-04-17 11:17:56 ET

Summary

- AerSale Corporation 2022 results were driven by flight equipment sales, not an area where I would like to see earnings growth being achieved.

- The integrated nature of the company gives the company a lot of flexibility.

- AerAware should be a big thing for AerSale Corporation and its stock price even though its P/E ratio of 21 is a bit high.

While demand for airplanes is high as air travel demand is recovering globally, original equipment manufacturers such as The Boeing Company ( BA ), Airbus SE ( EADSF ), and Embraer S.A. ( ERJ ) are struggling to increase production while some airlines such as Transavia, part of Air France-KLM S.A. (AFRAF), are forced to cancel flights due to part shortages for maintenance, repair and overhaul.

For a company such as AerSale Corporation ( ASLE ), this is a double-edged sword, but I would lean towards the current environment being somewhat favorable for a company such as AerSale. In this report, I will briefly discuss the company's business activity, the Q1 2023 forecast, and its most recent earnings.

What Does AerSale Do?

AerSale Corporation is a Florida-based company with several areas of activity, namely aircraft and engine sales, leasing and management, airframe material sales and maintenance, repair and overhaul with commercial as well as government customers.

What AerSale Expects For 2023

For 2023, AerSale expects revenues between $460 million and $490 million, which provides an increase in revenues of 12.5% to 20%. Analysts are currently expecting revenues to come in at $470.8 million, down from a previous estimate of around $495 million. AerSale expects adjusted EBITDA of $70 million to $80 million down from $87.4 million. So, the guidance is down, but it should be noted that it does not assume any AerAware sales.

A Look At The 2022 Results For AerSale

{kind=link}

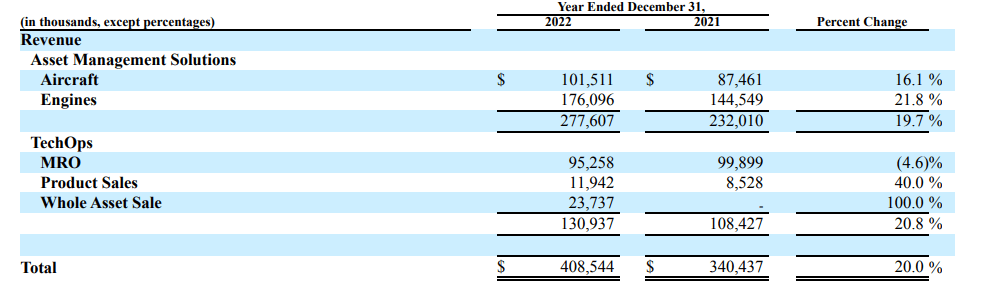

In 2022 , revenues increased by 20% which was driven by roughly the same growth rate in asset management solutions and TechOps. While the growth rate for Asset Management Solution is good it should be noted that the increase is driven by flight equipment sales and not so much in the leasing segment. The lease revenues actually declined due to lease terminations related to the war in Ukraine and the associated sanctions. As an investor, I would like AerSale better with more exposure to the equipment leasing environment but the reality is that there are other players in the market with a better competitive positioning for airplane leasing activities.

TechOps Revenues increased by $22.5 million, but the growth driver there was not quite satisfactory as it was driven by flight equipment sales. Adjusting for the Payroll Support Program, operating profits increased from $41.9 million to $55 million. So, we are seeing a 31% growth in adjusted operating profits on a 20% increase in revenues, which is what I like to see. I'd say that if you are looking for high MRO growth, AerSale is not the name you should look into.

What Are The Growth Drivers For AerSale?

While AerSale is not really showing growth where I'd like to see it, I am not negative on the company for investment but one should keep in mind the risks. The Boeing 757 passenger-to-freighter conversion program or P2F is a growth opportunity for the company. Currently, there are delays in the conversions and there was some headwind in H2 2022 for feedstock availability. With airplane shortages which are not getting much better given the Airbus delivery and program delays and Boeing's most recent problems with the Boeing 737 MAX , acquiring feedstock at attractive prices can be a challenge but this year should be better and with airplane shortages, there are also opportunities for MRO as airlines are keeping airplanes in the fleet longer requiring more maintenance activities than initially planned for.

What I liked about AerSale is that the business provides an integrated solution. With feedstock, the company can either decide to lease the airplane to an operator, part it out or convert it. So, the company always has a solution for its feedstock. The Boeing 757 offers opportunities as an airplane in the express logistics chain for e-commerce growth, but there are also risks. Engine availability could drive up costs and cost of conversion could in the current inflationary environment also be higher while macroeconomic headwinds could reduce demand for the converted airplanes.

So, that is something that should be kept in mind. Either way, even with lower P2F demand in the current environment where airplanes are higher in demand than OEMs can supply AerSale has some flexibility to optimize its on-airport MRO business and let the conversions be done by subcontractors. This basically means that the capacity for conversions is being subcontracted so that the MRO business can focus on servicing in-fleet airplanes.

What makes AerSale a highly interesting name to consider for investment is its AerAware product which consists of some airplane modifications in the radome and a wearable heads-up display for a pilot which improves situational awareness through improved vision in low-visibility conditions. Initially developed for the Boeing 737NG or Boeing 737 MAX, the Enhanced Flight Vision System provides AerSale with a big addressable market for a product that should be high margin. The only drawback is that the commercial roll-out of this product is one that is unknown. AerSale is going through the certification of the product now, but the process of cumulating flight hours has been rather slow. So, it is a project that is promising but its revenue generation depends on certification though I do believe that we are closing in on commercialization. No AerAware sales have been projected for 2023, but that is not because no sales are expected at all but because AerSale does not want to conduct issuing forecasts which include products that are not yet certified.

Conclusion: AerSale Stock Is A Buy, If Only Just For AerAware

The results from AerSale are not something that impresses me, but maybe my expectations are too high because we see operating income growth outpacing revenue growth on an adjusted basis. Furthermore, the company is subcontracting P2F conversions for the Boeing 757 which it is able to do so at better costs while also optimizing its capacity to capitalize on on-airport services demand.

The big thing for AerSale is going to be AerAware without doubt. It will have a high margin and a big addressable market for the Boeing 737, which can be expanded towards other airplane models. AerAware should become the next big thing for AerSale and makes AerSale Corporation stock a buy in my view.

For further details see:

AerSale Stock: A Disruptive Buy