AESC - AES: A Few Things To Like If You Are Comfortable With The Risk

2023-03-20 14:14:47 ET

Summary

- The AES Corporation is one of the few utilities that operate in multiple countries, but it still enjoys the incredibly stable cash flows that we like to see from the sector.

- The company uses hedging to reduce its exposure to currency fluctuations, which we should be able to appreciate.

- The company is positioned to give investors a 10% to 12% average total return annually over the next three years.

- The company has considerably higher debt than its peers, which is a risk to investors.

- The stock is cheap relative to its peers, which may be because of the risks inherent in the firm's leverage.

The AES Corporation ( AES ) is one of the largest utilities in the world, boasting operations in the United States and fourteen other countries. This makes it one of the only companies that have such a reach, as there are very few that have international operations. The company still has many of the characteristics that have long made utilities popular among more conservative investors, such as retirees. These characteristics include generally stable cash flows and generally high dividend yields. As of the time of writing, The AES Corporation has a 2.96% yield, which is respectable but well below the current rate of inflation.

Unfortunately, The AES Corporation also has substantial amounts of debt that result in it being somewhat riskier than many of its peers. The company has been trying to make up for this by aggressively developing and deploying a renewable energy platform, and admittedly it has been enjoying some success at this as the company does have somewhat better growth prospects than many of its peers coupled with a very attractive valuation. This is similar to the thesis that I presented in the last article that I published about this company a year ago. As such, it may make a somewhat attractive investment today for someone that can stomach the risk created by the company’s tremendous debt load.

About The AES Corporation

As stated in the introduction, The AES Corporation is one of the largest utility companies in the world, boasting operations in fifteen different countries. However, the company is headquartered in Virginia, United States, and the majority of its operations are in this nation:

The AES Corporation

It is quite rare to see a utility operate in multiple nations. This is partly because every country in which the firm operates has its own regulations and utilities tend to be among the most heavily-regulated companies in operation today. However, there are a few characteristics possessed by The AES Corporation that are common to all utilities, no matter where in the world they operate. The first of these is that the company enjoys remarkably stable cash flows over time. This is immediately obvious by looking at the company’s operating cash flows. Here are the annual operating cash flow figures for each of the past ten years:

{kind=link}

As we can clearly see, the company has delivered some growth over the period, but other than that, its cash flow figures did not vary that much over the years. This is a good time period for use for comparison, too, as there was a major global pandemic that resulted in the shutdowns of many national economies, a variety of crude oil and natural gas pricing environments, and the highest level of inflation that has been seen since the early 1980s in numerous developed economies of the Americas and Europe. Yet, The AES Corporation’s operating cash flows did not really vary by much.

The reason for this is that the company provides a product that is generally considered to be a necessity for our modern way of life. After all, how many of us do not have electricity and heating in our homes? That is true even in emerging nations, such as a few of the ones in South America that are included in the company’s footprint. As such, most people will prioritize paying their utility bills ahead of discretionary expenses during times when money gets tight. That is fairly common during recessions. It is something that could be quite important now since the rapidly-rising cost of living has forced many Americans to take on second jobs in order to maintain their lifestyles. I have pointed this out in numerous previous articles and it was noted in a recent Prudential Pulse survey . The point here is that many Americans are strapped for cash and may soon have to make choices about whether to buy the latest smartphone or pay their electric bill. They will almost assuredly opt to pay the electric bill, which means that having a company like The AES Corporation in your portfolio could prove to be a smart play.

One potential risk arises because of the fact that The AES Corporation operates in multiple countries. This is currency risk. After all, currencies fluctuate against each other quite often and it is certainly not unheard of for one to decrease substantially in value against another very quickly in certain cases. For example, the Turkish lira lost 40% of its value in 2021 due to government ineptitude. This would have a very large adverse impact on the profits of a company that operates in Turkey but reports its results in a more stable currency like the U.S. dollar or Euro. The AES Corporation does have some business in Argentina, which has also acquired a reputation for frequently having similar currency devaluations. As this is a risk that investors cannot ignore, it should be somewhat comforting to know that The AES Corporation has limited exposure to fluctuations in currency values:

The AES Corporation

As we can clearly see here, the company only has limited exposure to foreign currency, despite the fact that it collects foreign currency for all of its international operations. The reason for this is that The AES Corporation employs a hedging program through which it essentially transfers its currency risk onto other companies, such as hedge funds and major banks, that are better equipped to deal with such risks. As a result, the company is essentially able to convert the overwhelming majority of the foreign currency that it receives into U.S. dollars at a set rate. This is something that should be comforting to U.S. investors due to the fact that it ensures the company’s relative stability regardless of changes in currency exchange rates. As stability is one of the reasons that we invest in utilities like The AES Corporation, this should be appealing.

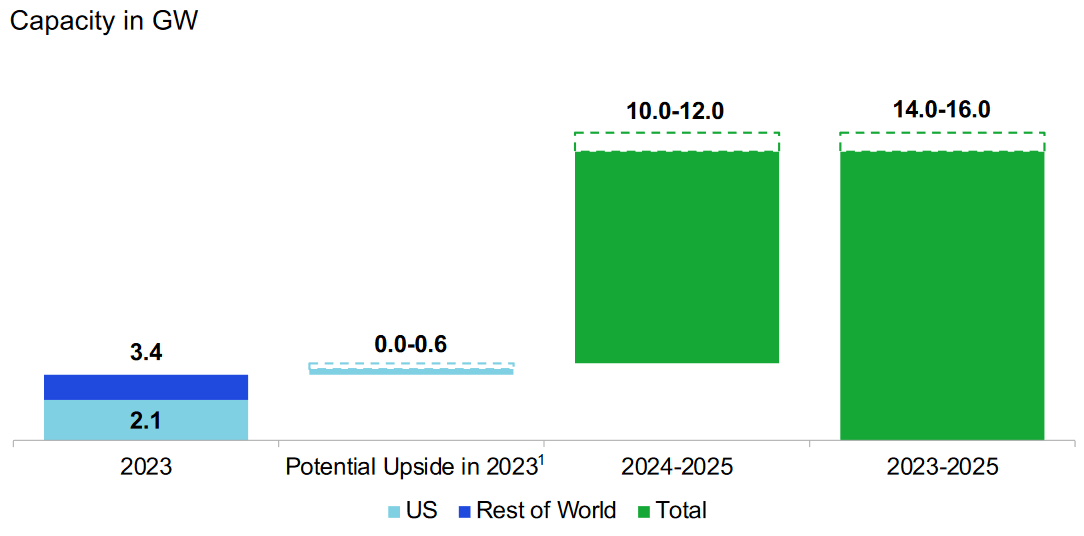

Naturally, as investors, we are unlikely to be satisfied with simple stability. We want to see any company that we are invested in grow and prosper. Fortunately, The AES Corporation is well-positioned to do exactly this. One method that the company is using to accomplish this is constructing renewable energy generation facilities that it then pairs with power purchase agreements with another party. The company plans to bring 3.4 gigawatts of generation capacity online in 2023 alone, with 2.1 gigawatts of that capacity located within the United States. The company plans to bring even more renewable generation capacity online in 2024 and 2025:

{kind=link}

The reason that the power purchase agreements are critical is the intermittent nature of renewable power. The biggest problem with wind and solar generation is that they do not work at all hours of the way as traditional generation sources do. For example, wind power does not work when the air is still and solar power does not work at night. Thus, a solar or wind power generation facility would normally only be able to earn money during certain periods. That is not economical, particularly since there is no guarantee that the periods of time during which it is capable of operating are times that the power is needed. Thus, wind and solar generation is highly uneconomical as cash flows and revenue is unpredictable. A power purchase agreement compensates for this as it ensures that the facility will earn a stable cash flow for The AES Corporation. This allows it to more easily predict its future cash flow and generate an appropriate return from the facility. It also gives us the same stability as we have come to expect from this company.

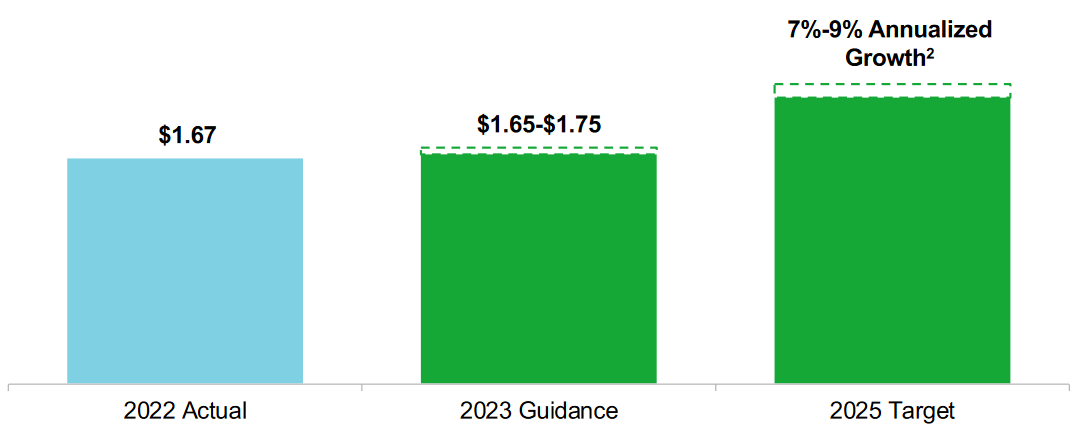

The fact that The AES Corporation is selling its power extensively under power purchase agreements makes it much easier to predict how profitable a project will be before the company begins constructing it. As my regular readers are certainly well aware, this is something that we usually like to see in the midstream sector and in fact these agreements give The AES Corporation a very similar financial profile. The current projects that the company has under construction should allow it to grow its earnings per share at a 7% to 9% rate over the next three years:

{kind=link}

When we combine this with the company’s current 2.96% dividend yield, investors should be positioned to earn a 10% to 12% total average annual return over the period. That is certainly a reasonably attractive return from a conservative utility company. In fact, it is one of the highest potential total returns in the sector. When we consider the company’s focus on renewable power, it could be a reasonable choice for an environmental, social, and governance philosophy.

Financial Considerations

It is always critical to investigate the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. This is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. That can cause a company’s interest expenses to increase following the rollover in certain market conditions. This is especially relevant today as the Federal Reserve has been aggressively hiking interest rates in an effort to combat the incredibly high inflation that is plaguing the economy and there are no signs that it will stop, although it may be forced between saving the banking sector and fighting inflation. In addition to interest-rate risk, a company must also make regular payments on its debt if it is to remain solvent. Thus, an event that causes its cash flows to decline could push it into financial distress if it has too much debt. Although utilities like The AES Corporation tend to have remarkably stable cash flows, bankruptcies have still occurred in the sector so this is a risk that we should not ignore.

One ratio that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio essentially tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. The ratio also tells us how well a company’s equity will cover its debt obligations in the event of a liquidation or bankruptcy event, which is arguably more important.

As of December 31, 2022, The AES Corporation had a net debt of $21.794 billion compared to $5.825 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 3.74 today, which is one of the highest ratios in the utility sector. Here is how that compares to some of the company’s peers:

| Company |

| Net Debt-to-Equity Ratio |

| The AES Corporation |

| 3.74 |

| DTE Energy ( DTE ) |

| 1.85 |

| Eversource Energy ( ES ) |

| 1.45 |

| Exelon Corporation ( EXC ) |

| 1.61 |

| FirstEnergy Corporation ( FE ) |

| 2.05 |

As we can clearly see, The AES Corporation is substantially more leveraged than its peers. This was the case the last time that we looked at the company, although it has gotten a bit better over the past year. However, the company’s debt still poses a very real risk that investors should not ignore as the peer comparison indicates that it may be using an excessive amount of leverage in its financial structure.

Fortunately, the majority of the company’s recourse debt matures after 2025:

The AES Corporation

This gives the company two advantages. The first, and probably most important of these, is that it gives The AES Corporation a bit of time to determine how it is going to handle its debt. This may include paying it off or potentially refinancing it should rates become more favorable. However, the Federal Reserve continues to project that it will keep rates “higher for longer,” so it may be a while before we see rates drop to a level that is anywhere near as low as the interest rates that the company is paying on its debt. That would be concerning as the fact that it will likely have to pay more as it rolls over this debt will strain its cash flow over time and offset some of the promised growth. With that said, a lot can happen over the next several years so it is difficult to make predictions, particularly since something like a severe recession could cause the Federal Reserve to slash interest rates much earlier than it currently expects.

Dividend Analysis

One of the primary reasons why many investors purchase shares of utilities like The AES Corporation is that they usually have a higher yield than most other things in the market. This company is certainly not an exception to this as the stock yields 2.96% at the current price, which is quite a bit above the 1.66% yield of the S&P 500 Index (SPY). With that said though, The AES Corporation’s yield is not particularly impressive for the utility sector as there are several companies whose yields currently exceed 4% today.

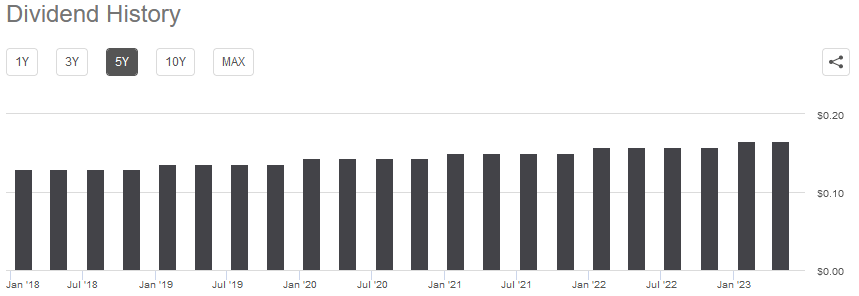

One thing that is quite nice to see is that The AES Corporation has a long history of increasing its dividend yield annually:

{kind=link}

This is something that is quite nice to see, particularly during inflationary periods such as the one that we are currently experiencing all across the developed world. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. As a result, it may feel as though we are getting poorer and poorer with the passage of time. The fact that The AES Corporation increases the amount that it pays out every year helps to offset this effect and maintains the purchasing power of the dividend.

Naturally, though, we need to ensure that the company can actually afford the dividend that it pays out. After all, we do not want to find ourselves the victims of a dividend cut since that would both reduce our incomes and almost certainly cause the stock price to decrease.

The usual way that we judge a company’s ability to pay its dividend is by looking at its free cash flow. A company’s free cash flow is the amount of cash that it generated through its ordinary operations that is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that the company can use to reduce its debt, buy back its stock, or pay a dividend. In the full-year 2022 period, The AES Corporation reported a negative levered free cash flow of $2.6869 billion. That is obviously not enough to pay any dividends, but the company still paid out $422.0 million in dividends over the period. This could be concerning as the company is not generating sufficient free cash flow to cover its dividend.

However, it is not uncommon for utilities to finance their capital expenditures through the issuance of equity and debt while paying their dividends out of operating cash flow. This is due to the incredibly high costs that are involved with constructing and maintaining utility-grade infrastructure over a wide geographic area. If it were to do otherwise, it would be very difficult for these companies to ever pay a dividend since these costs are usually higher than operating cash flows. During the full-year period ending on December 31, 2022, The AES Corporation reported an operating cash flow of $2.715 billion, which was more than enough to cover the $422.0 million dividend with a substantial amount of money left over for other tasks. Overall, the company should have little to no difficulty maintaining its dividend at the current level.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to generate a suboptimal return on that asset. In the case of a utility like The AES Corporation, the usual way to value it is by looking at the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued at the current price and vice versa. However, there are remarkably few companies that have such a low price-to-earnings growth ratio in the current richly valued market . Thus, the best way to use this ratio is to compare the company’s ratio to its peers in order to determine which has the most attractive relative valuation.

According to Zacks Investment Research , The AES Corporation will grow its earnings at an 8.53% rate over the next three to five years. That is reasonably in line with the figure that we used earlier in this article to calculate the company’s projected total return so it seems pretty solid. That gives The AES Corporation a price-to-earnings growth ratio of 1.52 at the current stock price. Here is how that compares to the company’s peers:

| Company |

| PEG Ratio |

| The AES Corporation |

| 1.52 |

| DTE Energy |

| 2.87 |

| Eversource Energy |

| 2.67 |

| Exelon Corporation |

| 2.69 |

| FirstEnergy Corporation |

| 2.49 |

This reinforces the statement that I made in the introduction to this article that The AES Corporation appears very cheap relative to its peers. The reason for this is probably the added risk that the company’s relatively high level of debt imparts upon it. Thus, we have a situation in which an investor that is willing to take on the extra risk may be able to earn a higher return by investing in The AES Corporation as opposed to one of its peers.

Conclusion

In conclusion, The AES Corporation is one of the few utilities that operate in many different countries around the world. The company still enjoys the generally stable finances that we expect from a utility, however. It is heavily focused on the renewable energy sector, which provides it with a few opportunities considering the fact that renewables are being heavily promoted and subsidized by many governments.

The AES Corporation should be able to give investors a better total return than many of its peers as a result. However, the company’s relatively high level of debt presents risks that should not be ignored. Overall, an investor that is comfortable with the risk may find some things to like here.

For further details see:

AES: A Few Things To Like If You Are Comfortable With The Risk