EADSY - Air France-KLM Stock Is Undervalued Against Its Earnings

2023-08-03 12:46:18 ET

Summary

- Air France-KLM SA posted strong Q2 results, with revenues increasing by €917 million and margins improving from 5.8% to 9.6%.

- Air France outperforms KLM in revenue growth and profit increase.

- Air France-KLM's debt profile is manageable, with net debt/EBITDA reduced from 1.8x to 1.2x and €7.8 billion in liquidity.

Air France-KLM SA ( AFRAF , AFLYY) is one of the companies that I have adopted a positive view on after being somewhat downbeat on the name in recent years due to the French and Dutch parts of the airline group not working in harmony. Initially, the buy rating paid off, with an 18% return on a flat market. However, those gains have evaporated since.

I don’t want to go too much into detail on what caused the stock price to drop, but there have been some aircraft shortage issues at Transavia due to longer than expected maintenance events, some ground incidents, and delayed paperwork on leased airplanes. Furthermore, the issues with the Pratt & Whitney ( RTX ) geared turbofan has affected the Air France Airbus ( EADSF ) A220 fleet, and the KLM Cityhopper Embraer E-2 ( ERJ ) fleet also have caused some issues for the airline group. All of this layers on top of the growth prospects at Amsterdam Schiphol Airport, where KLM and other airlines are in a legal battle with the government regarding the growth prospect of KLM’s hub.

In this report, I will discuss the second quarter results and revisit my price target and rating for Air France-KLM stock.

Air France-KLM Posts Strong Results

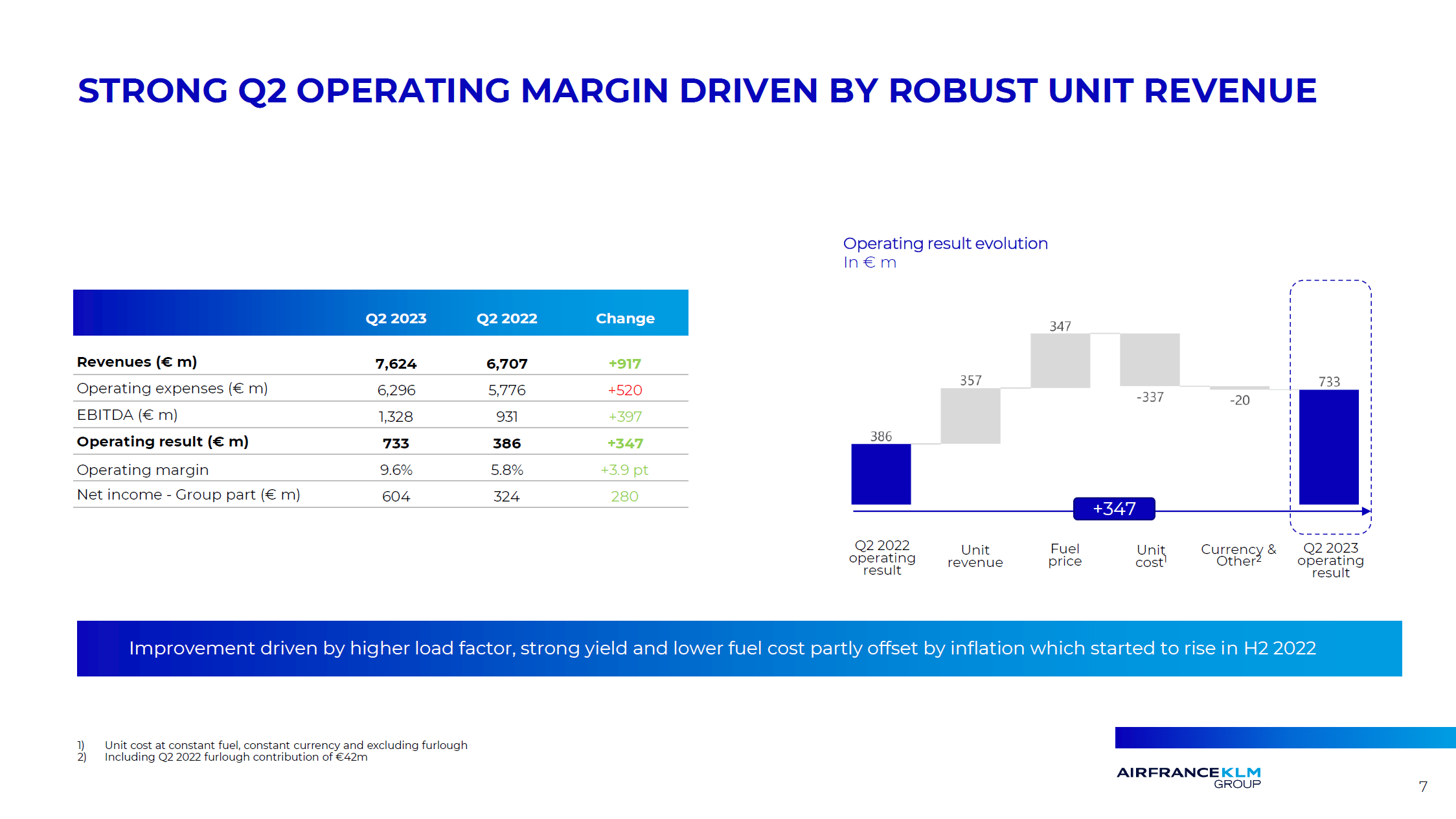

{kind=link}

Year-over-year, revenues increased by €917 million, or 14%, while costs increased 9%. So, we saw margins improve from 5.8% last year to 9.6% this year, which is a good result. €560 million out of the €917 million revenue growth came from 8% higher capacity, around €200 million came from improved load factors and the remainder came from yield expansion. Year-over-year, the expansion in results was driven by unit revenue increases and reduction in fuel costs offset by higher unit costs reflecting inflationary pressures.

{kind=link}

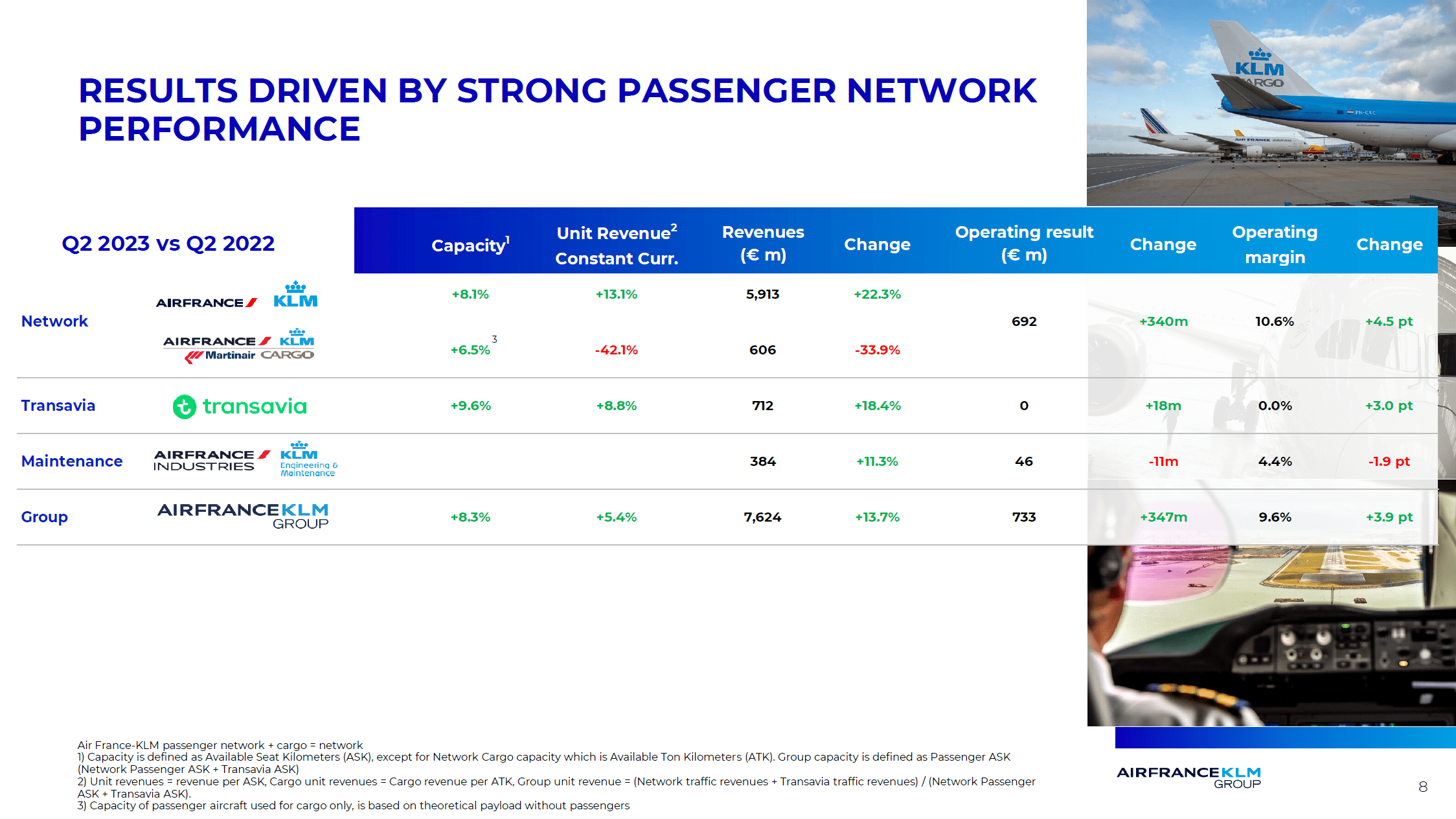

Air France-KLM saw a total increase in unit revenues of 5.4% on 8.3% capacity growth. Transavia saw around 10% capacity growth and 8.8% growth in unit revenues leading do a break-even result in a tough quarter where Transavia suffered from airplane shortages as well as ATC strikes in France. The cargo division is seeing normalization with 6.5% capacity growth and a 42.1% decline in unit revenues leading to a 34% decline in revenues. Air France-KLM is renewing its freighter operations with new airplanes to join the fleet in the years to come as well as logistics partnerships and I would think that this is necessary given the normalization of unit rates and the group’s challenging history in the field of cargo operations. The passenger network, excluding Transavia, saw 8.1% growth in capacity and 13.1% growth in unit revenues, leading to a 4.5 pts expansion in margins.

The maintenance division saw 11% growth in revenues, but margins contracted by 1.9 points. This is driven by higher input costs, which in some cases does not get passed through to the customer and labor shortages in the maintenance division.

{kind=link}

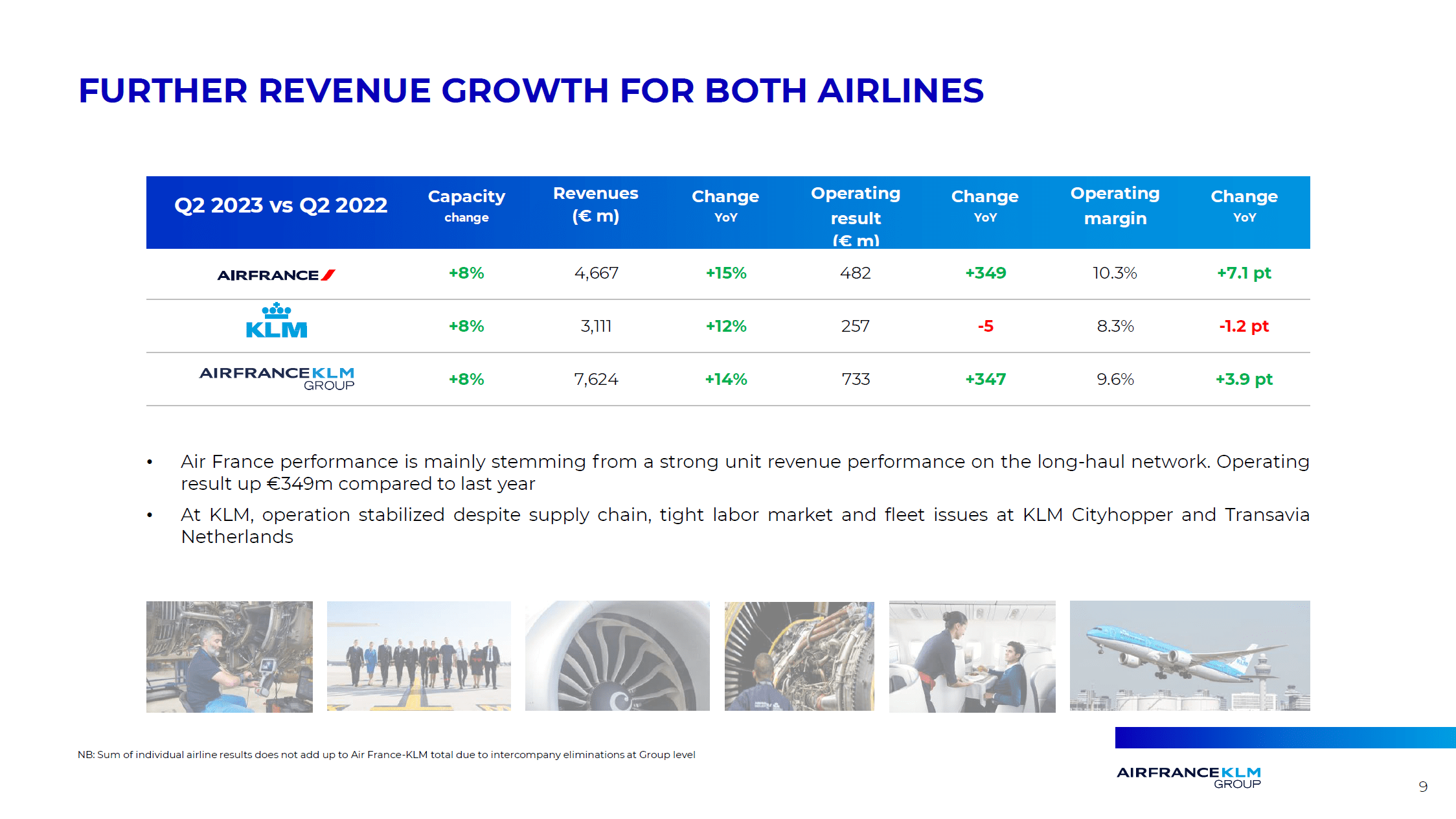

Looking at the Air France and KLM businesses, one thing becomes clear, and that is that after years of KLM outperforming its French partner it is now Air France showing the better growth numbers. Air France revenues increased 15%, resulting in its profits increasing from €133 million to €482 million. The KLM Group did worse with a 12% revenue increase generating €5 million lower profits. So, we see two things. The first is that on similar capacity increases KLM is underperforming on the revenue growth and it is not translating the capacity and revenue growth into higher profits. This is caused by issues at KLM Cityhopper and Transavia, but this underperformance as well as the possibility of future flight caps on Schiphol Airport do give some reason to worry about KLM’s profit prospects.

{kind=link}

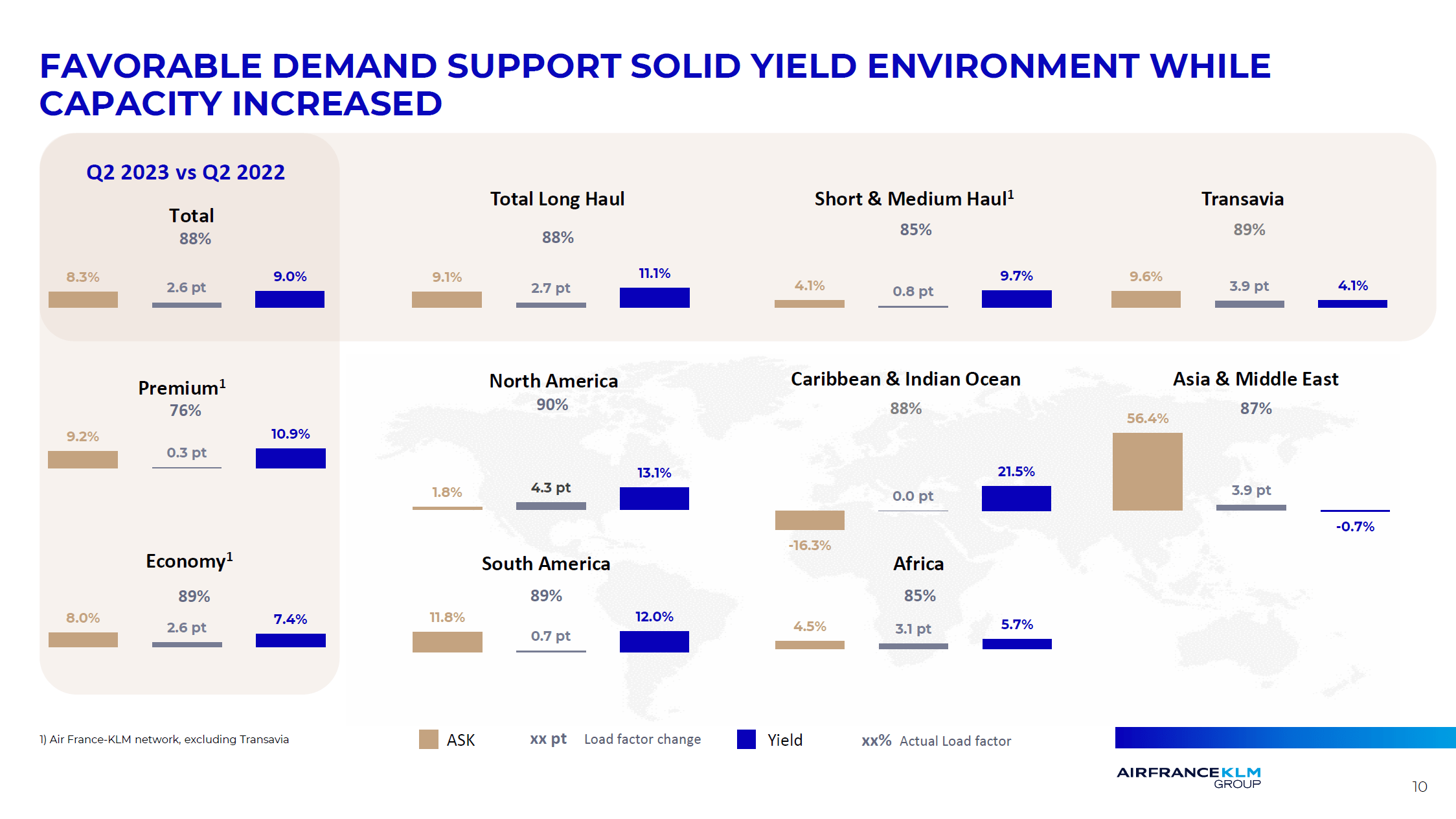

Viewed by segment class, we see that premium is leading the capacity growth. It is not quite leading the load factor change but we do see higher yields compared to last year which somewhat suggests that a focus on the premium product and possible changes to travel habits feather in positively for the premium cabin. Viewed by geographic region, the growth is in Asia with 56.4% capacity growth and a 3.9 pts increase in load factors. The yields softened slightly, but that was to be expected given the limited capacity last year that drove up the yields. In North America, the capacity was kept constant and better load factors and unit revenues drove the improvement. In the Indian Ocean and Caribbean capacity was recued but in return we did see better yields. This likely relates to capacity shifting into Asia and the Middle East while the results in South America and Africa also looked good.

Short and Medium Haul is were Air France-KLM is less focused on growth. That is also not where the airline is most eager to deploy capacity due to competition with low-cost carriers. In that segment, the growth of Transavia can provide more competitive expansion for the airline group while the easier buck is to be earned on long haul expansion with expansion opportunities in Asia & Middle East.

Air France-KLM Debt Profile Is Manageable

{kind=link}

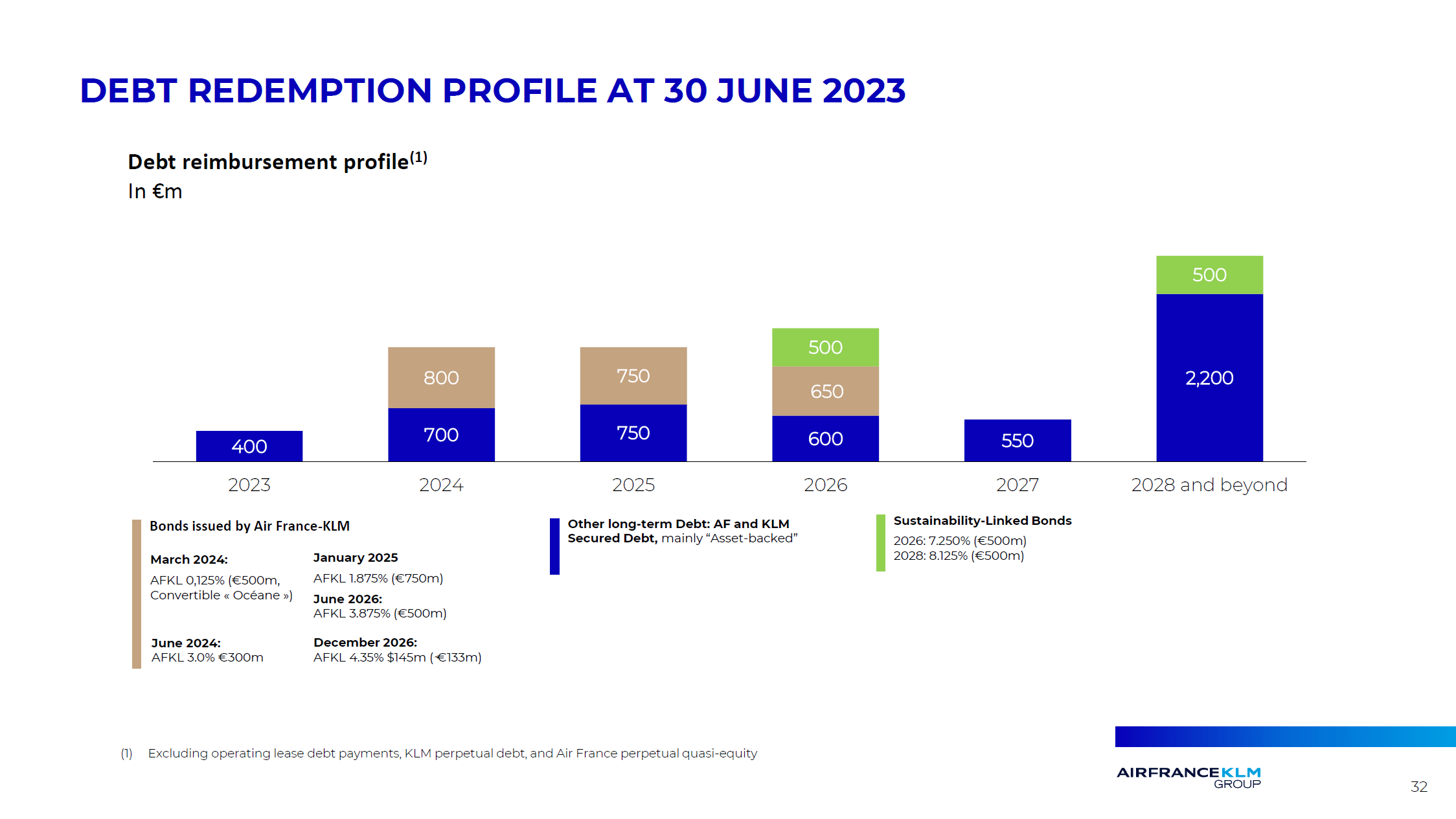

When airlines started taking on debt to survive, the big question is how effective and efficient they would be in the process of deleveraging. I think Air France-KLM did a pretty good job. They completely exited the Dutch and French state aid packages by issuing sustainability-linked bonds. Whether these bonds are just an ideal debt financing tool or will actually make material impact on “going green” remains to be seen, but it is nice to see an airline link its debt to sustainability. The company has now reduced its net debt/EBITDA from 1.8x at the start of the year to 1.2x reducing its net debt by €1.4 billion. With €7.8 billion in liquidity, the airline group can easily service its debt through 2027.

Air France-KLM Softens Capacity Outlook Further

{kind=link}

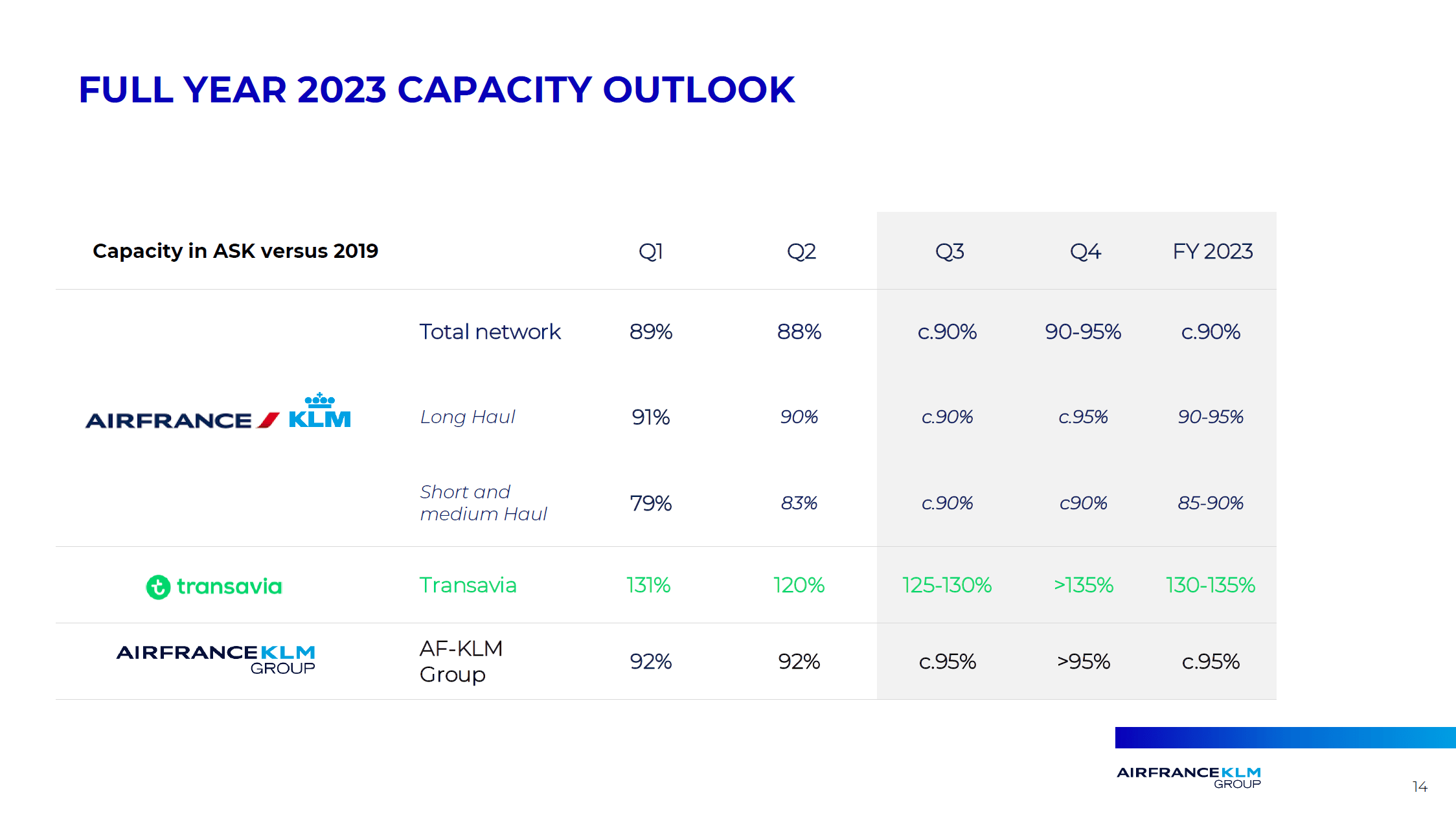

The outlook for Air France-KLM has not changed much other than guiding for a softer full year capacity restoration for the Air France-KLM network. This is driven by Q4 capacity being 90% recovered for medium and short haul compared to a 90%-95% recovery expected earlier. This brings the network recovery for Air France-KLM to 90% compared to 90%-95% expected earlier. Furthermore, Q3 guidance has been narrowed by roughly 5 percentage points for Transavia and the same for the full year.

But the bigger dent to the recovery outlook this year comes from short and medium haul, which is now expected to be 80-85 percent recovered by Q2, bringing the group total 5 percentage points below a full recovery. My best guess is that capacity challenges at Schiphol continue to be problematic.

Is Air France-KLM Stock A Buy?

The reason why I do like KLM has remained unchanged. Air France-KLM SA is seeing the benefits of its rethink on the France domestic network and associated slots, and it has improved its working rules, implementing changes that would have seen fierce resistance years ago. So, the airline used the pandemic to push through necessary changes to better position the airline. Beyond that, the cabin product and ancillary revenues have been optimized to provide more value and drive down unit costs. Air France-KLM SA has also reduced its leverage significantly.

I believe that this actually is just the start, as the airline will begin absorbing more new single aisle jets such as the Airbus A321neo. This will allow further growth from Schiphol without adding flight movements. Part of the bright prospects are dampened by the aircraft shortage at Transavia and KLM Cityhopper and the continued challenges on Schiphol regarding long-term growth.

{kind=link}

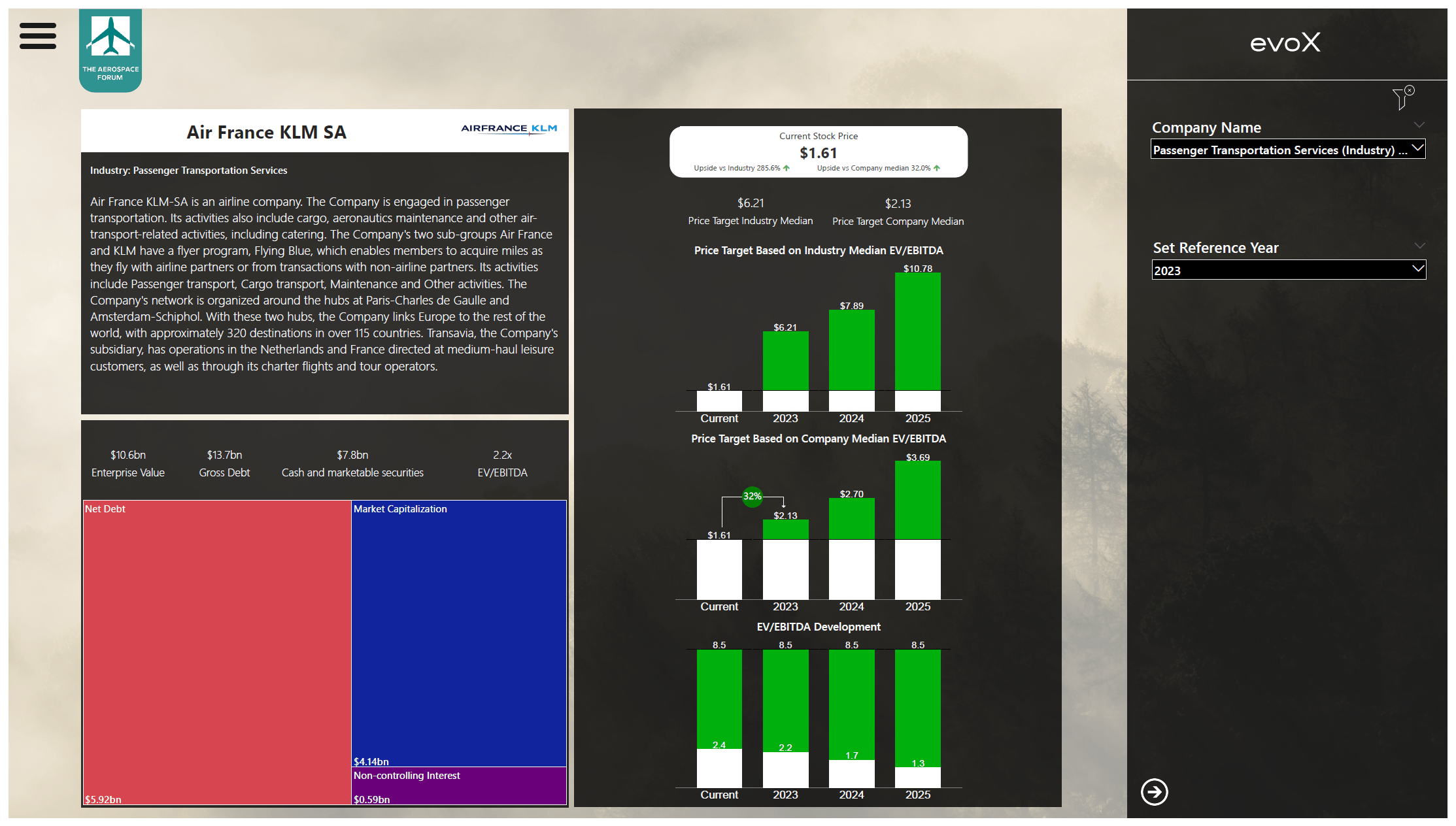

From a fundamental perspective, significant upside remains. With an enterprise value of $10.6 billion and $4.8 billion in 2023(e) EBITDA, the EV/EBITDA is 2.2x which is below the 2.9x median for Air France-KLM and significantly below the industry median of the industry at 8.25x. So, while there is some uncertainty on the exact recovery trajectory, I do believe that the current share prices offer around 32% upside.

Conclusion: Short-Term Challenges, But The Stock Is Priced Way Too Low

The second quarter results show strong improvement on the financial performance including lower net debt and strong EBITDA to net debt. At the same time, we also see that KLM is the relative underperformed driven by challenges for Transavia, KLM Cityhopper and a tight labor market which also affects the group’s maintenance division. However, I do think that Air France-KLM is finally implementing cost efficiency measures that were not possible years ago and primarily Air France is performing significantly better than during pre-pandemic times. Coupled with a focus on premium cabin product upgrades and next generation airplanes entering the fleet I do think that the group could see efficient growth ahead that is not reflected in the stock price. Therefore, I am maintaining my buy rating on Air France-KLM SA stock.

For further details see:

Air France-KLM Stock Is Undervalued Against Its Earnings