AL - Air Lease: A Strong Quarter But Balance Sheet Repair Delays Upside

2023-11-08 04:40:06 ET

Summary

- Air Lease stock rallied 1% following strong quarterly results, and while shares have lagged, they are cheap.

- The Company's revenue rose by 17% to $659 million as air travel recovered and it grew its flight due to deliveries of new planes.

- The shortage of new planes and strong lease rates provide opportunities for AL to re-lease existing planes and generate strong cash flow.

- Its focus on deleveraging while AerCap buys back stock means its valuation gap is likely to persist next year.

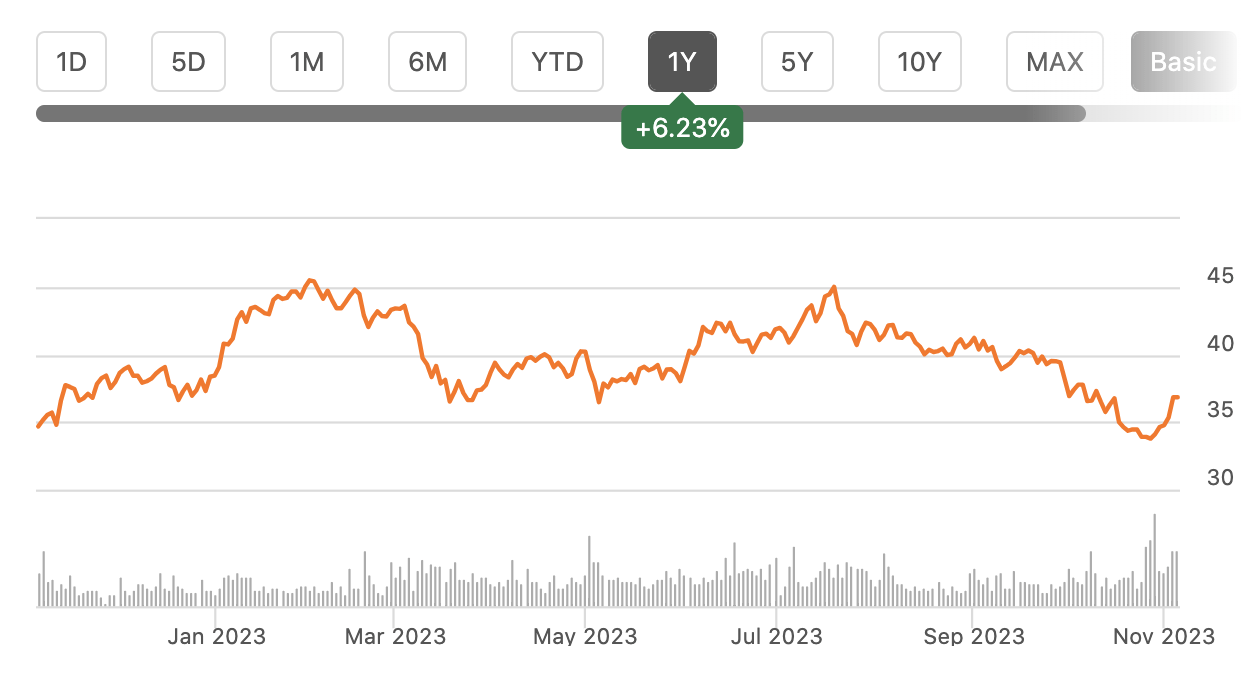

Shares of Air Lease ( AL ) have been a mixed performer over the past year, rising by about 6% but lagging the broader market. On Monday, they rallied 1% following a strong set of quarterly results. I believe the position is favorably positioned, and the stock is cheap. While I see upside in AL, I do think AerCap ( AER ) is likely to prove to be a more attractive investment opportunity.

{kind=link}

In the company's third quarter , Air Lease earned $1.59 in adjusted EPS, which beat consensus by $0.12 as revenue rose by 17% to $659 million. AerCap leases airplanes under long-term contracts to airlines. As air travel has recovered and it has grown its flight due to deliveries of new planes, revenue has been rising substantially. I would note that the air lessors are more exposed to international travel demands than domestic ones.

Some airlines may struggle to get stand-alone financing for planes at an attractive price, which is why they choose to lease from companies like AL. Moreover, Air Lease and AerCap each maintain massive fleets and are among the biggest buyers of planes from Airbus and Boeing (BA). Air Lease owns 448 planes with 351 on order. Because they provide anchor orders, they can negotiate discounts that a smaller airline could not.

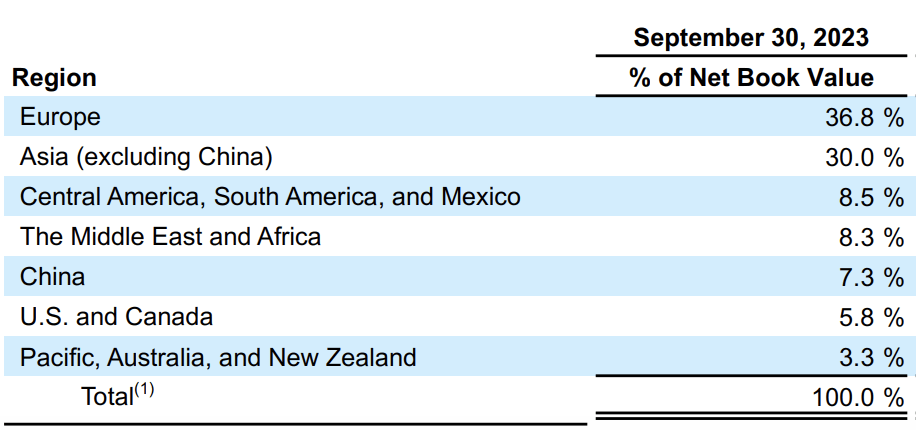

This makes it relatively attractive for them to buy planes and lease them out to carriers. Because companies like Delta (DAL) have large fleets of their own, they can negotiate directly with the manufacturers, making leasing a less attractive proposition. As you can below, the US and Canada account for just 6% of book value with Asia (including China) and Europe over 70%.

{kind=link}

International travel grew consistently in the mid to upper single digits in the 2010s before COVID disrupted it. Even with an explosive recovery, travel is 12% below pre-COVID levels. While we may never return to the prior trend, especially given Russia's isolation from the global market, I expect ongoing travel growth, which should support Air Lease's business.

Statista

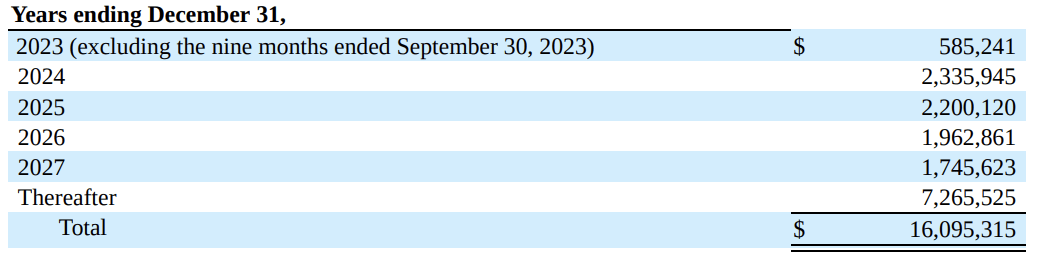

Thanks to strong lease rates and utilization, its adjusted margins rose 70bp from last year to 26.8%. As noted above, AL has 350 planes on order. As these are delivered, they should drive further growth. Critically, every plane that AL is slated to receive between now and 2025 is already leased out. On average, its leases have a remaining life of 7 years. This provides strong cash flow visibility. Last quarter, rental revenue was $604 million, or $2.4 billion annualized. As you can see below, AL has leases amounting to 97% of this amount signed next year and over 90% in 2025. Even by 2027, its lease rate is over 70% of its current revenue rate.

{kind=link}

It is critical to emphasize that this is the floor for revenue, not the ceiling, or even an accurate estimate of where revenue will be. Many contracts have options where the airline can extend. Additionally, Air Lease is always trying to sign new leases. From a year ago, its average remaining lease life has moved from just 7.1 to 7.0 years, even as a year has passed as it signs new contracts. Given the strong travel environment, re-leasing should remain strong.

This should be aided further by the shortage of new planes. It is not news to aviation investors that new plane deliveries have been low, between COVID and Boeing's 737-MAX debacle. As such, hundreds fewer planes have been delivered than trend. On top of this, RTX ( RTX ) has grounded hundreds of planes with engine issues, exacerbating the shortage. With an inability to get new planes, it should be easy to re-lease existing ones, particularly as Air Lease has a young fleet of just 4.6 years.

AerCap

Air Lease maintains such a young fleet because it is constantly selling older planes after leases mature. This part of the business has also been aided by the new plane shortage. Just as used car prices rose after COVID, used plane valuations have been really strong. Last quarter, it sold eight planes for $350 million and generated a $44 million gain, or about 0.40/share. It has $1.8 billion for sale, and I would expect similar quarterly gains over the next year as the plane shortage dynamic should persist for some time.

This is also an important way in which Air Lease can deleverage its balance sheet as well as fund new plane purchases. These sales funded about 80% of its $450 million in new purchases. Air Lease carries $18.6 billion in debt, which is flat year to date. 85% of that debt is fixed rate with a total average interest rate of 3.67%, up from 3.07% last year due to higher refinancing rates and increased rates on the floating portion of its debt.

Debt to equity is 2.68 vs the company's 2.5x target. This is largely due to the Russia write-off of $800 million last year. Essentially after the war in Ukraine began, these planes became stranded in Russia, which stopped paying for them. Frankly, the planes basically were stolen. Air Lease does have insurance claims, which it is pursuing, but there have been no settlements yet. AerCap received a payment last quarter but also has substantial remaining claims.

Because Air Lease relies on debt to finance its plane purchases, investment grade ratings are "sacrosanct" and will come before buybacks. That said, management did raise the dividend 5% to $0.21. Given AL has about $7 billion of book equity. Today, it is carrying over $1 billion of excess debt. Within about 12 months as book equity rises and it sells planes for a gain, it should get back to target. As such, I do not expect material buybacks next year but would expect them in 2025.

AL's book value is over $60. Given it is selling planes for a gain and earning a double digit return on equity, I do think shares should be trading much closer to book value. Because depreciation schedules are conservative, it structurally sells planes at a gain. Even if we discounted half of these gains as one-time, AL has about $5.20-$5.30 in earnings power. It is a capital-intensive business, but it has long-term contracts.

I view fair value as about 10x earnings or about $52-54/share, representing significant upside. It is disappointing buybacks will be some time away as buying back shares so far below book value would be very accretive for investors. That is why I prefer AerCap. While its fleet is older, its financial position is allowing meaningful share repurchases today. Until AL pivots to shareholder returns, I suspect the valuation gap is likely to be persistent. AL is likely to prove a sound investment for patient, long-term investors, but over the next year, I expect it to lag AER within this sector.

For further details see:

Air Lease: A Strong Quarter But Balance Sheet Repair Delays Upside