AL - Air Lease Corporation: I Still Prefer The Preferreds

2023-10-04 05:04:41 ET

Summary

- Air Lease Corporation's metrics continue to lag those of AerCap in the market to the detriment of its equity returns.

- The preferred stock, on the other hand, offers an attractive quarterly dividend and limited interest rate risk.

- Air Lease's refinancing into a higher interest rate environment may lead to increased interest expenses and limited return of capital to shareholders.

I previously wrote twice about Air Lease Corporation ( AL ) in the past year, highlighting my lukewarm views on the common stock and constructive views on the preferred shares. My view remains unchanged, and I highlight why below.

Competitor benchmarking

I've compiled a variety of metrics that compare Air Lease to its largest public competitor, AerCap Holdings ( AER ). On a P/B basis, Air Lease currently trades at a sizable discount to AerCap. However, despite a mountain of evidence demonstrating AerCap's superior operating results, Air Lease still trades at a higher P/E ratio. You could argue, potentially, that the discount between the two should be wider, and a pairs trade (long AER, short AL) could potentially have merit, in particular, if the valuation discrepancy between the two firms were to narrow further.

| Air Lease |

| AerCap |

| Debt / EBITDA |

| 8.6x |

| 7.5x |

| Net Debt / Equity |

| 2.7x |

| 2.8x |

| ROA |

| 1.6% |

| 2.8% |

| ROE |

| 7.1% |

| 12.0% |

| Cost of Debt (incl. amort of discounts and issuance cost) |

| 3.9% |

| 3.7% |

| EBIT Margin |

| 50.0% |

| 52.8% |

| Net Margin |

| 18.1% |

| 25.6% |

| Gain on Sale % |

| ~7.5% |

| ~25% |

| Price / Book |

| 0.62x |

| 0.85x |

| Price / NTM Est Earnings |

| ~9.5-10x |

| ~8-8.5x |

Source: Company filings, author's own calculations - with exception of P/B and P/E, all calculations based on second-quarter results.

Interestingly, for most of Air Lease's existence prior to AerCap's purchase of GECAS, Air Lease traded at least at a modest premium to AerCap based on price-to-book. That regime has shifted significantly since then, and it appears that Air Lease's discount to AerCap on this metric has never been wider. Unfortunately, I do not see the stock as a screaming buy as a result, as the table above indicates, and judging by management's unwillingness to repurchase shares at these valuations, neither do they.

Price-to-Book Value History (Seeking Alpha / YCharts )

Aircraft trading update

I had previously expressed my reservations about the company's ability and willingness to sell aircraft into what appeared to be a strong trading market, and Air Lease at least partially addressed my concerns by selling ~$600 million of assets (eight aircraft) in Q2 alone, with some of those needing to be widebodies given the $75mm per aircraft average value, which is positive from an asset risk perspective. They also indicated that they possessed a backlog of $1.7 billion of additional dispositions and that they expect these to generate gains at the top end of their 8-10% historical range.

For so long as the market remains robust and in particular as the stock declines in value, it would be very encouraging to see management step up its asset sale efforts, and ideally, use those proceeds to buy back its shares at a discount. AerCap has utilized this playbook for years, and the value proposition for Air Lease is the same, it just requires management to adopt this philosophy of capital allocation that they have been unable and/or unwilling to do thus far. In fact, they recently provided a snapshot of their strategy, which can be found below:

Firstly, their existing average fleet age is well under the "first third" of their useful lives, so that would naturally limit how much trading they do. However, I happen to think that this programmatic approach is misguided at best, as it ignores the fact that selling an aircraft is not a function of its age, but a function of a cyclical marketplace that ebbs and flows like the market for other financial assets. It would be nice to see management demonstrate a willingness to be flexible on this age-based approach in lieu of a capital allocation-centered approach. They have previously said that bulk buying of new aircraft from the manufacturers is the best outlay of their cash, but again, in a market that fluctuates, it is extremely hard to believe that (or any one approach) can always be the answer to this question.

Refinancing and interest rate outlook

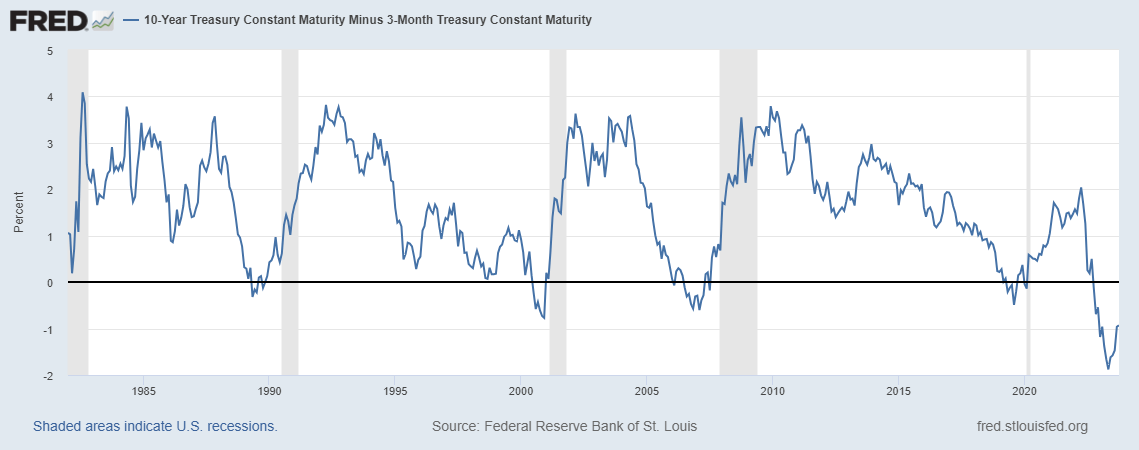

As of 6/30/23, the company had not increased its revolving credit facility borrowings from the $1 billion level, although it extended the maturity a few months ago. They also issued a sukuk at 5.85% in March, but otherwise have not been active in issuing new debt, at least in the public or private placement markets. In recent weeks, bond yields have been rising rapidly, and the yield curve inversion appears to have bottomed, at least for now, as can be seen in the chart below.

{kind=link}

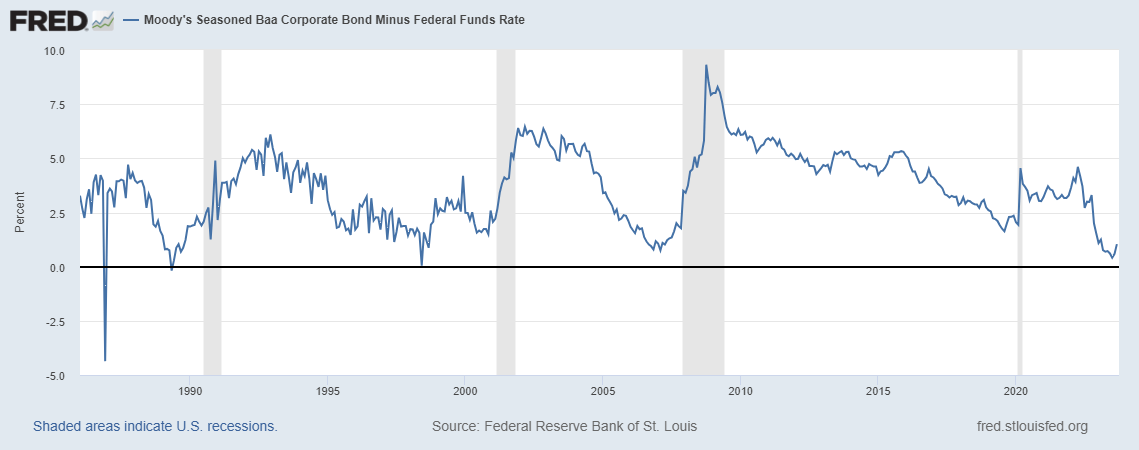

The rise in longer-term yields is alarming as this should at least partially translate into higher-cost borrowing for Air Lease unless spreads tighten further from what are already reasonably low levels, as the following chart demonstrates. This should continue to be monitored, and the company will get some benefit in the form of higher lease rates on certain aircraft, but the impact of those will take time to materialize - likely more than an immediate hike in the company's interest expense line. As it stands, Baa spreads are around the level that coincided with the past few recessions and spread-widening episodes.

Baa Corporate Bond Yields Less Fed Funds Rate (St. Louis Fed)

{kind=link}

Preferred stock update

The preferred stock is little changed since my last publishing. It declined significantly in the wake of the bank failures in March and slowly rebounded to around the same price it was earlier in the year, around ~$24 per share. Meanwhile, it's paid approximately 4.5% in three quarterly dividend payments since then. As the Fed has continued to raise rates, and as the Secured Overnight Financing Rate (SOFR), the likely index rate for the preferreds, has eclipsed 5%, it implies a roughly 9% yield on the preferred stock next year, assuming SOFR holds at current levels. I think the preferred stock offers interesting value and limited interest rate risk, albeit with the limited liquidity I have previously highlighted. It should, in my view, be thought about as a long-term, income-oriented investment, not one for capital gains, or that would need to be sold in the near term. And given that I expect the company's net income to cover the preferred dividend by a factor of 8-9 times, there is plenty of cushion to absorb portfolio deterioration without jeopardizing this payout.

Russia update and portfolio management

On the slightly bright side, the prospects for at least a partial recovery in value on the lessor's claims related to its seized Russian aircraft seem to have improved. AerCap was the first major aircraft lessor to announce a settlement, in the amount of $645 million related to 17 aircraft, and this week SMBC Aviation Capital has followed with its own $710 million settlement covering 16 aircraft which comprises roughly half of its prior Russian exposure by value. Air Lease's total writedown, net of one aircraft it was able to recover, was approximately $771 million.

Meanwhile, the company has prudently, in my view, reduced its exposure to Chinese airlines from ~12% of fleet value down to a level below 8%. While this may ultimately not result in any consequences, the ongoing tensions between China and the United States cannot be taken lightly and should continue to be watched closely. I would not be shocked or disappointed to see them further reduced exposure, particularly where there is a strong appetite from domestic lessors that can efficiently acquire this equipment.

Otherwise, there have not been any major near-term airline failures; however, it appears that the company had two newer A330-900s with restructuring Air Belgium and it would be a shame to see these returned so soon. It is likely to put pressure on the lease rates and/or SG&A line for this aircraft, although probably not enough in isolation to significantly move the needle overall.

Risks to investment thesis

1. Increasing interest rates and "higher for longer" Fed (common stock only)

2. Lack of profitable asset trading and rigidity of management's strategy

3. Potential 2024 recession

4. Limited liquidity (preferred stock only)

Conclusion

There seemingly is potential here for shareholders if management really leaned into share repurchases via asset sales. They say that their order book is a tremendous asset given the delivery delays and sold-out nature of many of Boeing's and Airbus's most popular models, but that "value" has yet to meaningfully materialize in the company's results. The company has shown no indication that it is willing to deviate from its strategy, and I expect its return on equity will continue to be compressed relative to other aircraft leasing peers. However, results should be satisfactory enough to more than enable the existing payment (and higher potential payment) on the preferred shares, which still provide an interesting income-generating opportunity.

For further details see:

Air Lease Corporation: I Still Prefer The Preferreds