AL - Air Lease Corporation: Underappreciation For Airplane Assets Drives Significant Upside

2023-11-06 17:39:26 ET

Summary

- Air Lease Corporation stock prices have decreased by 4.6%.

- The company's revenues increased by 17.5% year-over-year, driven by rental income and aircraft sales.

- Despite higher costs, net income grew by 22% and the company remains undervalued.

Stock prices of Air Lease Corporation ( AL ) have lost around 4.6% of their value since the last time I discussed the company's results and valuation. While there are pressures driven by interest rates, inflation, and insurance costs as I previously discussed, I think the current environment is a very compelling one for lessors.

In this report, I will be discussing the most recent Q3 earnings to assess whether there was any unexpected impact in positive or negative direction, and I will figure the valuation of Air Lease Corporation stock using two valuation methods. The first one will use the shareholder's equity to which a typical price-to-book value will be applied, and the second valuation method uses a combination of balance sheet data and forward projections to which an appropriate EV/EBITDA multiplier will be applied.

Solid Growth For Air Lease Corporation

{kind=link}

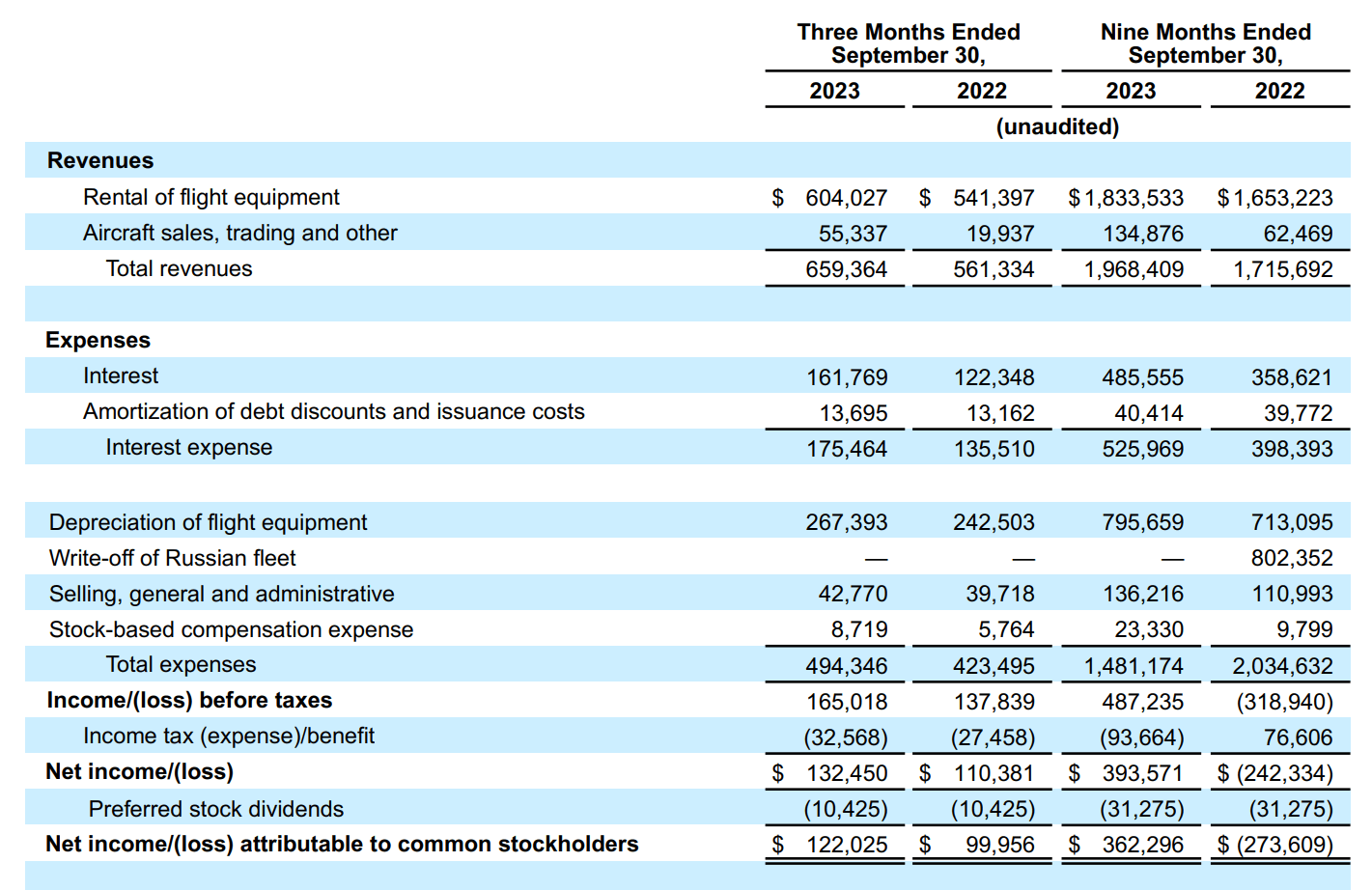

Starting at the top line, rental revenues increased 11.6% to $604 million while aircraft sales increased to $55.3 million for a total revenue of $659.4 million which was 17.5% higher year-over-year. So, we do see a significant increase in revenues which was significantly higher than the 6.6% increase we saw in the previous quarter. However, that was driven by one-off revenue recognition of security and maintenance deposits in connection with the lease terminations for flight equipment placed with lessees in Russia. I adjusted for this in the previous quarter to get a like-for-like comparison and those showed adjusted revenues being 18.4% higher. So, the 17.5% higher revenues year-over-year for the third quarter is not something extraordinary. The 11.6% increase in revenues was driven by a 10.6% growth in flight equipment on lease. So, also there we do not see anything that is highly surprising. It's just the continued growth of flight equipment with value of next-generation airplanes embedded in the lease rates.

Aircraft sales were up almost 180%, and even this is not a major surprise given the current environment where demand for commercial airplanes is high, but ability of OEMs to fill that demand is limited. Essentially this means that older airplanes can be sold at attractive prices.

Interest expense was up 29.5% and that was primarily driven by the composite interest rate rising from 2.85% to 3.67% as interest rates have been increasing. Depreciation and amortization expenses were up 10.2%, which is also not unexpected given the higher count of flight equipment. Selling, general and administrative expenses were up 7.7% driven by higher leasing expenses. While costs are up, the better way to look at this is in terms of revenues. SG&A measured against revenues was 6.5% compared to 7.1% a year ago, so essentially we are looking at higher costs but better cost amortization. Stock-based compensation expenses were up $3 million which was driven by a reduction last year as performance criteria for the RSU to be vested were improbably to be achieved.

Overall, net income grew to $122 million from $100 million marking a 22% increase. So despite higher interest expenses and depreciation, which are the biggest drivers of cost for a leasing business we saw net income growth outpacing revenue growth with pre-tax margins of 25% compared to 24.6% a year ago and 24.4% in the prior quarter.

So, overall we are seeing stable cost execution on higher rental income and higher aircraft sales.

The Tailwinds For Air Lease Corporation

One can note that the interest expenses are outpacing growth in rental income and that is indeed the case. The reason for this lag effect is that the airplanes that are currently being put on lease have lease rates that were agreed on years ago. The majority of leases have a fixed lease rate with interest rate escalators, but this does not quite track favorably with the higher aircraft values we are seeing today. By that I mean that with the debt piles we are seeing now, more expensive flight equipment is procured as aircraft flight equipment sales from OEM to lessor also consist of cost escalations and it is also not the case that existing leases that are already in effect are seeing any interest rate adjustment to the lease.

So, I wouldn't quite want to make a case that revenues should be in line with interest expense growth because flight equipment values vary over time and lessors are financing growth of their flight equipment portfolio with a big chunk of rental income not having any interest rate sensitivity.

Given the supply and demand imbalance that currently exists it is also not the case that we should be seeing an immediate upward pressure on rental income. That is because the lease rates without escalation have been agreed on years ago, the higher variable part of the lease rate via escalators merely is a cost offset. The real uptick in rental income will come gradually as airplanes are coming off lease and in that case Air Lease Corporation has a big advantage. During the quarter, $450 million worth of flight equipment from the OEMs was received whereas $700 million to $800 million was expected putting on display the constraints from supply side that can drive significant value for Air Lease Corporation besides the negative effect of not having the associated lease revenues for missed deliveries.

The supply side constraints drive up values of airplanes in all brackets whether it is next-generation or previous-generation airplanes and have airlines looking for solutions to execute existing capacity plans. Those solutions include extending leases on existing aircraft but at higher values supported by the improved underlying value of the equipment as compared to an undisturbed market or acquiring the airplanes from lessors. Generally, Air Lease Corporation sells airplanes to lessors and financial institutions but the higher gains on sale are still driven by the shortage of airplanes. So, Air Lease Corporation is seeing better returns on its airplane sales as other parties see a better business case for the older airplanes as well. The company is also fully placed on its deliveries through 2025 which provides significant negotiation strength with lessees going forward.

Some analysts, including ones on this platform, have questioned the continued strength of demand for airplanes, but it should be noted that it is not an easy thing to walk away from existing lease agreements even if a delivery has yet to occur. So, until 2025 at least that risk is somewhat mitigated and we are still looking at airplane delivery shortages of hundreds of airplanes while the long-term trend for air travel will require more airplanes.

Assessing Air Lease Corporation Stock Value Based On Book Value

| Valuation Air Lease Corporation |

| Common shareholder's equity in $ millions |

| $ 6,111.05 |

| Common shares outstanding in millions |

| 111.03 |

| Book value per share |

| $ 55.04 |

| Implied share price (5-year price-to-book) |

| $ 39.64 |

| Upside |

| 6% |

| Implied share price (5-year price-to-book (pre-pandemic)) |

| $ 52.32 |

| Upside |

| 40% |

The book value per share would provide 47% upside in which Air Lease would be fairly valued. However, the company like many other lessors tends to trade below its book value. Using the 5-year price-to-book value, there is around 6% upside, but one can question whether this 5-year trailing figure can be fully justified as it includes two years of pandemic which is not an event I would project forward while using the 5-year trailing figure does exactly that. I deem it more appropriate to use the 5-year pre-pandemic figure which would imply 40% upside to $52.32 closely matching the Wall Street target of around $53.

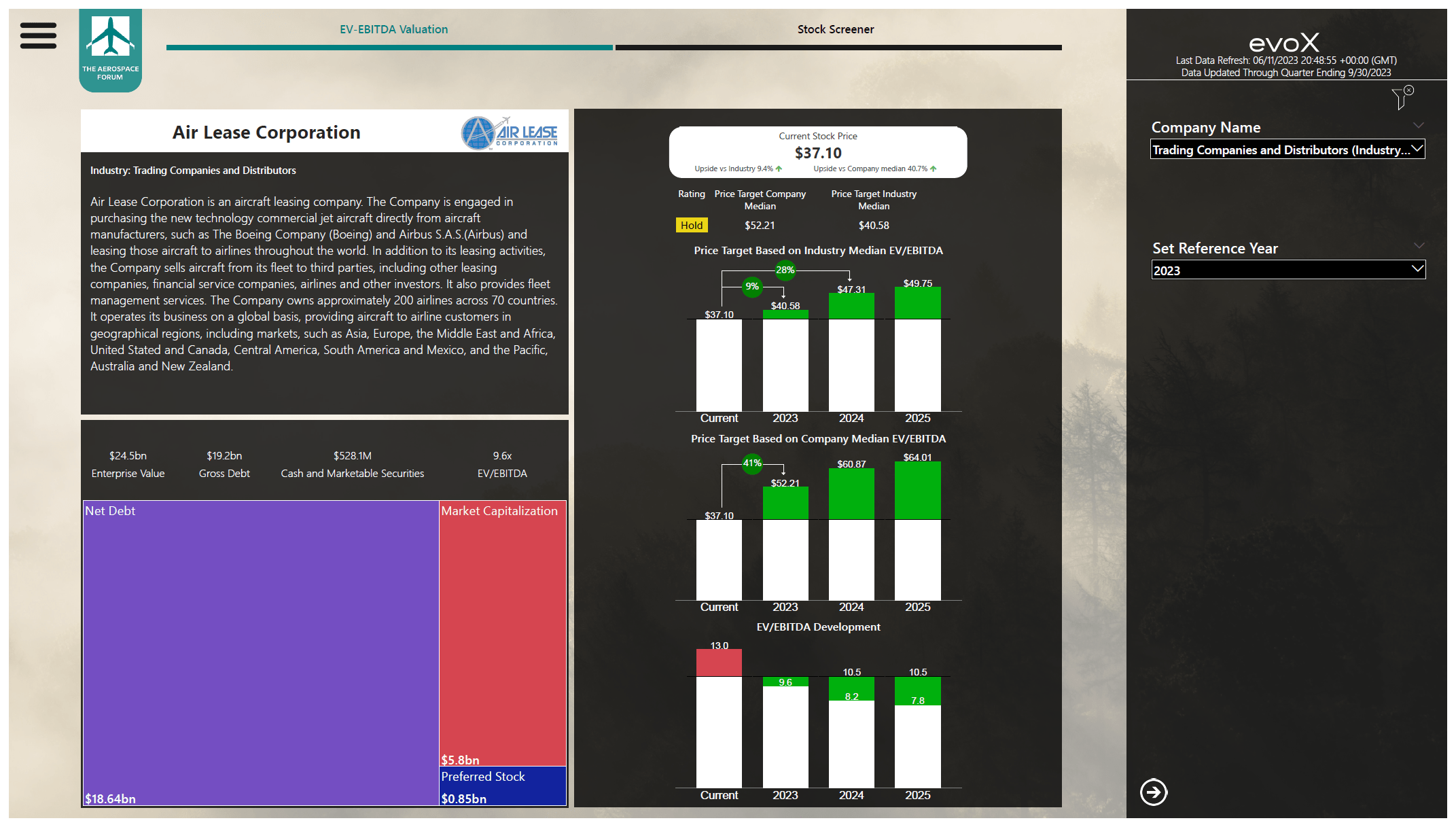

Assessing Air Lease Corporation Stock Value Based On EV/EBITDA

{kind=link}

I analyzed Air Lease Corporation stock based on its fundamentals and the growth expectations going forward and those growth expectations have become more positive with cumulative EBITDA expected to be 6.7% higher towards 2025. What might be somewhat unexpected is that the rating system I use ends up with a Hold rating while the upside is almost undeniable. The reason for that is that even though lessors such as Air Lease Corporation have significant upside, the stock tends to underperform.

So, the hold rating is not so much related to a lack of upside but due to a lack of market appreciation for the airplane leasing business and that is not something that I would discount the stock's appeal for. So, while the stock screener shows a hold rating and there could indeed be a case for that assuming that historical underperformance will continue to exist, I am maintain my strong buy rating for the stock because the appropriate book value computation as well as the processing of the balance sheet data and forward projections show significant upside in the stock price ahead. Furthermore, it should also be considered that that risk-adjustment also includes an alpha-factor that was impacted by the loss of flight equipment in Russia, which I think just like the pandemic is not an event that should be projected forward.

Conclusion: A Strong Buy Despite Underperformance

The quarterly results were not extremely interesting for investors, I would say, and that is not a bad thing because the airplane leasing business is focused on the longer-term and mid to long-term significant growth drivers continue to exist. The pandemic has shown that airplanes retain value rather well and with the current strength in aircraft demand and continued long-term demand for airplanes, I believe the stock is currently significantly undervalued.

For further details see:

Air Lease Corporation: Underappreciation For Airplane Assets Drives Significant Upside