NUE - Algoma Steel: A Potential Winner For The Patient Investor

Summary

- Algoma Steel is on a transformative journey, transitioning from a blast furnace steel producer to one using the more modern, cost effective and environmentally cleaner EAF technology.

- ASTL stock seems to be trading at over a 40% discount to its intrinsic value, making it a great bargain. I assign it a “Buy” at the current price.

- It can be a potential multi-bagger for the patient investor if one has the capacity to stomach short-term variability.

- Risks include structural risks of macroeconomic and pricing uncertainty, as well as specific risk of executing EAF transition successfully (which a few other steel producers have done).

Despite being in traditional and structurally difficult industry, there is plenty to like here about Algoma Steel ( ASTL ). It’s in the process of transitioning to newer, more cost-effective technology while adding capacity at the same time. The market seems to be discounting the stock due to the gyrations of this journey while not fully appreciating the end game here. This makes ASTL a potential winner for the value investor.

Company Overview

Algoma Steel Group Inc. is a Canada based steel producer. It operates 1 manufacturing plant located in Sault Ste. Marie, Ontario, with an annual capacity of 2.8 million tons. Algoma is a fully integrated steelmaker, i.e., it produces coke from coal, converts iron ore into iron, iron to liquid steel and liquid steel into semi-finished and finished steel products. Algoma provides a range of hot and cold steel products including coiled sheet and plate for the North American market (US, Canada, Mexico). Its primary customers segments are automotive, manufacturing & construction, tubular and service/distribution centers. For its most recent fiscal year ended March 31, 2022, the shipment volume by product category, geography and end markets is shown below.

Company's FY2022 Annual Report

{kind=link}

Founded in 1901, Algoma has gone through a number of transitions in its expansive history. Most notably, it was acquired by Essar Group in 2007, went through a bankruptcy, and was taken private in 2018. In October 2021, Legato Merger Corp, a US based Special Purpose Acquisition Company ((SPAC)) went through a merger with Algoma Steel to take it public again.

Currently, major transformations are underway at the company. Algoma is transitioning itself from a Blast Furnace mill to an Electric Arc Furnace ((EAF)) mill. This is a huge undertaking for the company, with the project expected to take over 2 years (completion projected to be mid 2024) at a capital expense of around CAD700-750 million . Secondly, a plate mill modernization project was launched in 2021, focused on improving product quality and productivity of its plate operations. More on these transformations later.

Steel Industry Overview

In my view, steel manufacturing is a relatively tough business to be in. Being a commodity, steel prices are largely dictated by the balance of global supply and demand, general macroeconomic conditions and political forces influencing import/export tariffs and regulations. This causes steel prices to be volatile. Unless a company is producing a propriety or a differentiated product, it has little control over unit prices for its products. Take a look at the US Midwest Domestic Hot Rolled Futures shown below and notice the variation in prices, especially the pronounced cyclicality during and post Covid.

{kind=link}

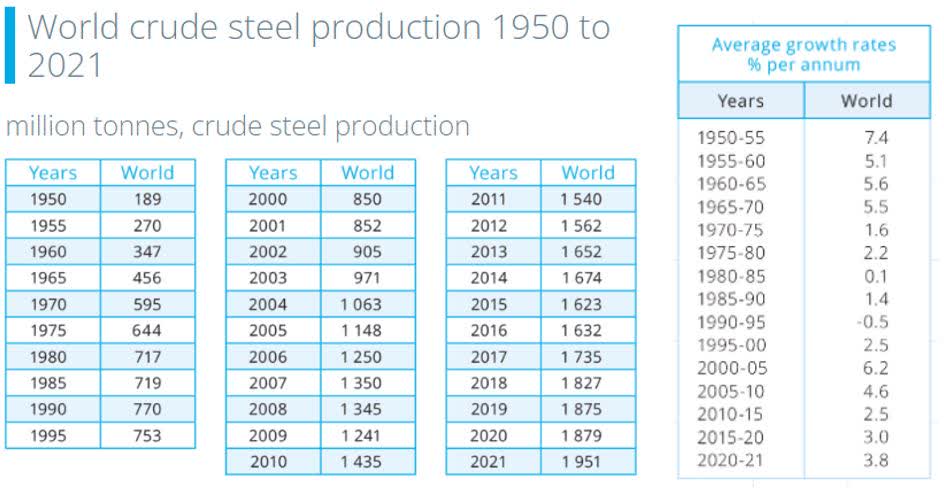

Secondly, similar market forces cause the cost of major raw materials (coke, iron ore for blast furnace steelmaking process and scrap steel for EAF process) to be market driven. A company can certainly get into long-term contracts with its suppliers but typically, the contractual prices are tied to the respective commodity indexes. Finally, steelmaking requires heavy capital expenditure in plant and machinery. Consequently, margins for steel producers tend to exhibit a high degree of variability. On top of this, growth rate of the industry as a whole have been relatively low, probably tracking global GDP growth as shown below.

{kind=link}

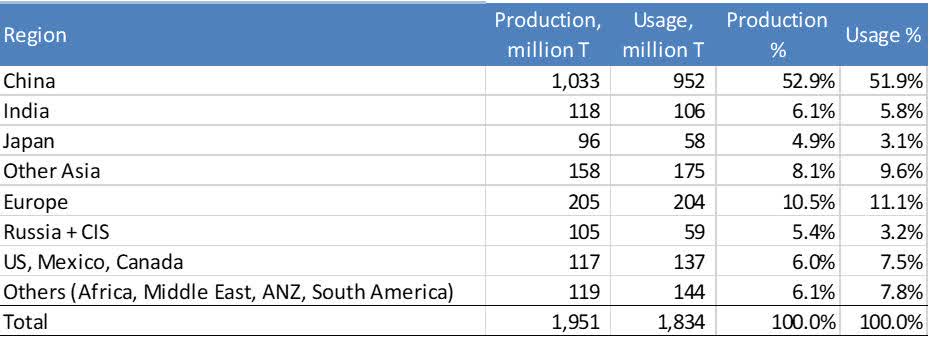

From a geographic standpoint, in 2021, the North American (US, Canada, Mexico) region, produced 117 million tons or 6% of world steel output. From a usage standpoint, it consumed 137 million tons or 7.5% of world steel output . Thus, the region is a net importer of steel.

Crude Steel Production and Usage by region, 2021

{kind=link}

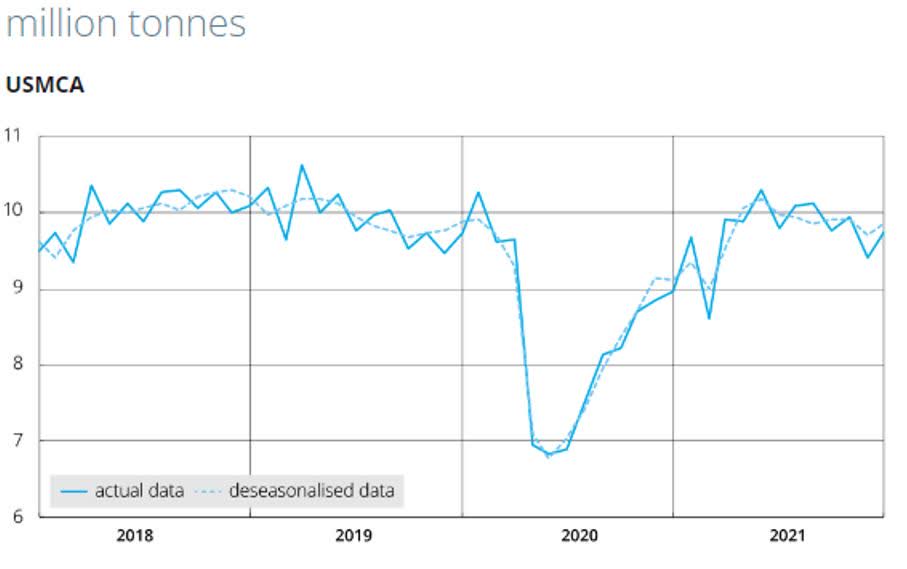

Monthly crude steel production in North America is shown below. Barring the downturn during Covid phase, the production has remained relatively stable. We can, thereby, assume the market in North America in volume terms to remain relatively flat in the future. Together with the fact that the region is a net importer of steel, this bodes well for Algoma’s drive to increase its output capacity via EAF conversion as it can potentially replace some of these imports.

{kind=link}

Transformation at Algoma Steel

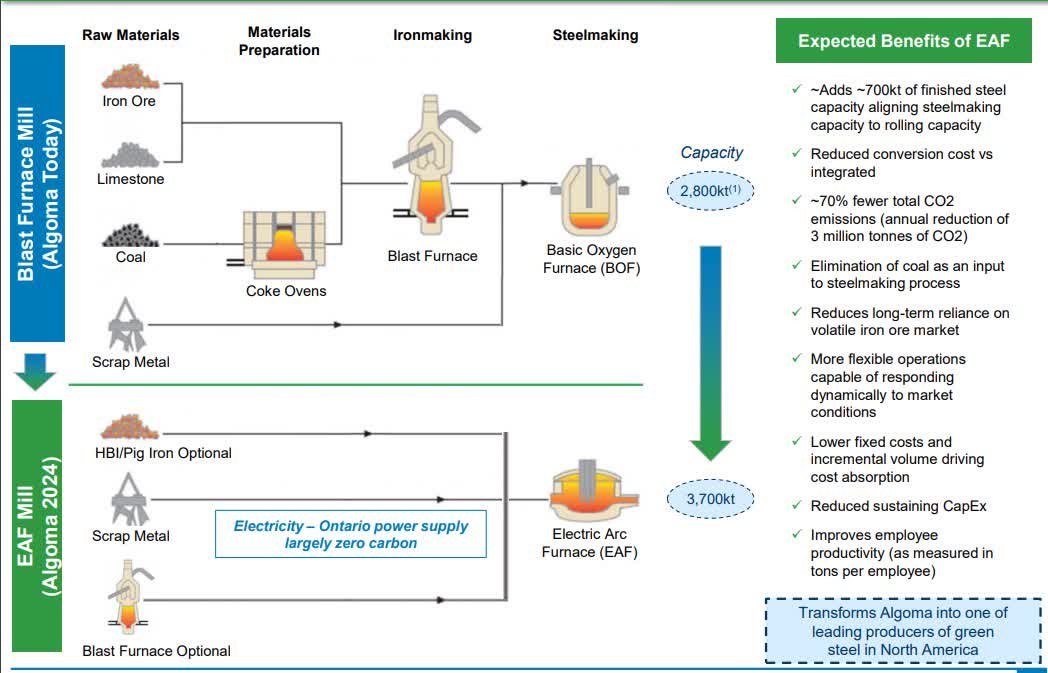

There are two major transformations currently underway at Algoma Steel. The more disruptive one is the conversion from a blast furnace mill to an EAF mill. For those not familiar with the differences in the two processes, the visual below from the company’s quarterly presentation should be helpful.

Company's Q4 FY22 earnings presentation

{kind=link}

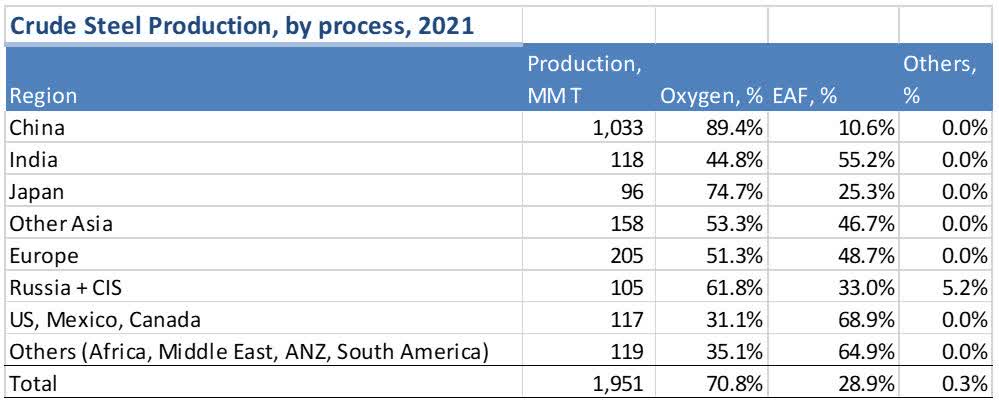

At its very core, the difference between the two processes lies in the use of raw materials and the energy process used for melting. EAF process uses steel scrap as the basic raw material (with other additives) versus iron ore, coke, and limestone used in the blast furnace. The melting process in EAF manufacturing uses electricity versus hot air blast (typically by burning gas) being used in the blast furnace. EAF steelmaking is the modern method for producing steel. Several US manufacturers like Nucor ( NUE ) and Steel Dynamics ( STLD ) have been increasing their EAF steelmaking capacity over the past few years. With 69% of steel produced in North America from the EAF technology, North America is the leader in the use of EAF compared to rest of the world, as seen in the table below.

{kind=link}

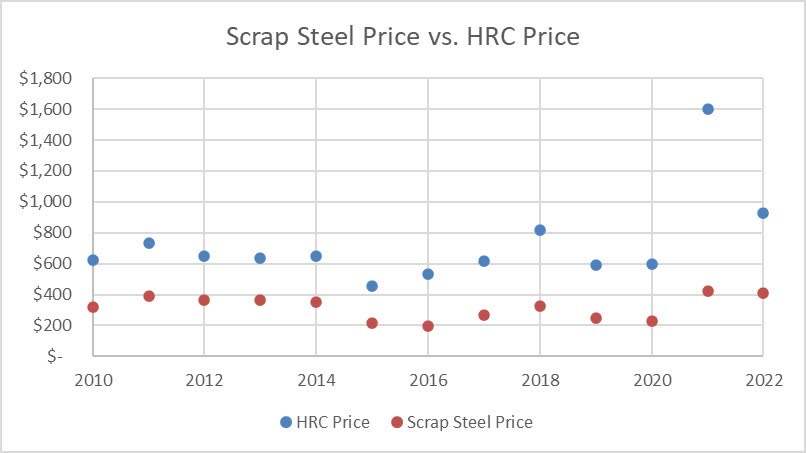

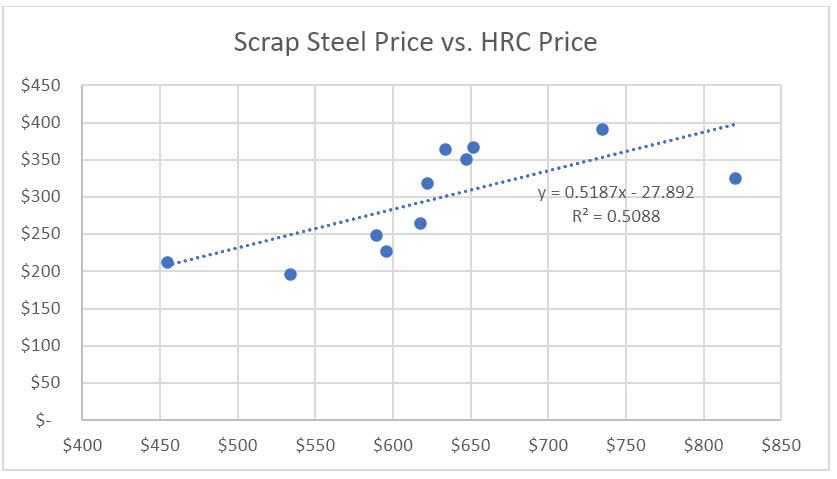

In terms of the benefits of EAF technology, it is a much cleaner technology compared to blast furnace process, yielding a ~70% reduction in CO2 emissions. This could provide Algoma with higher carbon tax savings. Moreover, it would reduce Algoma's reliance on highly volatile iron one prices. Though the price of steel scrap exhibits variance as well, it seems to move somewhat in tandem with the HRC steel prices. In fact, analyzing the price data from 2010 through 2020, I find a covariance of 0.71 between the two (see below). This means that the cost of the major input moves in conjunction with the price of the output, providing some stability on gross margins.

Author's analysis of data from Statistica.com Author's analysis of data from Statistica.com

{kind=link}

{kind=link}

Thirdly, with the addition of 2 EAF furnaces, Algoma increases its installed steel production capacity by ~700k NT or 25%. The new capacity of 3,500k NT better matches its downstream processing capacity. Finally, EAF process is likely to reduce its annual maintenance expenses.

EAF transition was approved in November 2021, and is expected to be completed by mid-2024. Including contingency, Algoma estimates the project to cost ~CAD750 million in capital spend. 8% of this was spent in its FY22, 35% is expected to be spent in FY23 and the rest in FY24 and beyond.

Plate Mill Modernization – This project is intended to enhance the quality and productivity of Algoma’s plate product line, which according to the company, could be a source of competitive advantage. The project is undertaken in two phases. Phase 1, which focuses on product quality improvements, was completed recently. Phase 2, which focuses on productivity improvements to increase throughput, is slated to begin later in 2023 based on market conditions. Overall, the capex spend on this project is estimated to be ~CAD135 million , with CAD20 – CAD25 million of this spend remaining.

Valuation Thesis

To value Algoma Steel, I focused on four key factors – revenue growth, margins, capital expenditure needs and cost of capital. This valuation has also been done in Canadian dollars (C$ or CAD) to keep it consistent with the reporting currency for the company. Unless otherwise stated, all references to currency are in Canadian dollars.

Revenue growth

Excluding the impact of Covid, steel usage in North America has been fairly static over the last 4 years. Given its plant location, Algoma is unlikely to expand its geographic market. With the addition of production capacity due to EAF conversion in 2024, I assume that Algoma will be able to sell this additional capacity given the NA region is a net importer of steel. Therefore, I assume that it will be able to ramp up to utilize 80% of its new capacity or 2,800k NT by CY2027. Note that over the last 4 years, its average capacity utilization has been 82% based on its annual reports.

Algoma has recently experienced lower production volumes due to unplanned and planned outages, as well as plate mill modernization project. These disruptions seem to be largely behind them at this point. Therefore, I find it likely that the production volume will ramp slowly over the next 2 years and then, at an increasing pace post EAF conversion in 2024.

I assume HRC steel prices will continue to exhibit high variability and cyclicality as has been observed in the past. Therefore, I find it safe to use a historical average price (converted to today’s $ terms) for HRC steel. From 2012 through 2020 (pre-Covid), this average has been close to USD 752/MT . I further assume that this average will gradually rise over the years (due to inflation) at the risk-free rate. Note that with this assumption, I am forecasting almost a 35% drop in revenues over the next 12 months, given steel prices were much higher than average in the last 12 months.

Margins

Algoma is facing market pressures currently on its raw material supplies. As a conservative estimate, I assume that the gross margin pressure will continue and therefore, I assign miniscule gross margins of 0.8% for the next 2 years. With the conversion to EAF by 2024, I believe the margins will start improving steadily for reasons stated earlier. It is interesting to note that for the 2 US producers with highest % EAF capacity (Nucor and Steel Dynamics), gross margins for the last 4 years have averaged slightly over 20%. I attribute this largely to the structural benefits of using EAF technology. As Algoma transitions to this technology, I expect to them to realize similar margin gains. Hence, I assume gross margins for Algoma will rise starting in 2025 and get to 18% (90% of NUE and STLD’s gross margins) by 2028. Operating expenses are assumed to remain at historic 3.3% of revenues.

Capital investment requirements

Capital requirements for Algoma stem from regular annual maintenance needs and a one-time spend on two major projects underway. On a net capital basis, the annual maintenance spend has been close to 1% of revenues historically and I use the same going forward. On top of this, I have added CAD128 million for CY2023 and CAD428 million for CY2024 for the spend on EAF conversion and the remainder of plate mill modernization project. Both these estimates come from the most recent quarterly report and earnings call. Finally, I assumed a terminal return on capital of 20%, slightly higher than the US industry average but below the average for global steel producers.

Cost of capital

I used a bottoms-up model to estimate the cost of capital. Using a risk-free rate of 3.3%, an implied equity premium of 5.55%, an unlevered beta of 1.18 for steel industry, and the current debt/equity ratio of 9.2%, the cost of equity for ASTL comes out to be 10.2%. Given its relatively small debt currently, its assumed that ASTL will have a stable grade credit rating of BB, which translates to a default spread of 3.1% and a resulting pre-tax cost of debt of 6.4%. Using current weights of its market value of debt and equity, its weighted average cost of capital ((WACC)) comes out to be 9.8%. Being a mature company, I don’t expect its WACC to fluctuate much over the years.

A list of key assumptions used in the valuation model are summarized in the table below.

Key Valuation Assumptions

| Variable |

| Initial |

| Terminal |

| Rationale |

| Sales volume (‘000 NT) |

| 1,978 |

| 2,800 |

| Total EAF capacity of 3,500 kNT. Assuming 80% capacity utilization |

| HRC Steel price (USD/MT) |

| $752 |

| $883 |

| Average HRC price 2012-2020 (exc. Covid period) increasing at risk-free rate annually |

| Gross margin |

| 0.8% |

| 18% |

| Current cost pressures on margins to persist short-term. Terminal gross margins assume at 90% of US EAF producers |

| Capital Expenditure |

| C$147 (Y1) C$480 (Y2) |

| C$56 |

| For next 2 years, capex spend on EAF conversion and plate mill modernization added on top of annual maintenance capex |

| Terminal return on capital |

| -- |

| 20% |

| Slightly better than median US steel companies |

| WACC |

| 9.8% |

| 9.8% |

| Bottoms-up calculation assuming current low debt/equity ratio to stay constant |

Based on these assumptions, a discounted cash flow ((DCF)) valuation was completed for Algoma Steel. The details of the valuation are presented the table below.

DCF Valuation Model (CAD million)

| # of outstanding shares |

| 107 |

| Value of equity/share |

| $18.0 |

| Year --> |

| TTM |

| 2023 |

| 2024 |

| 2025 |

| 2026 |

| 2027 |

| Terminal |

| Volume (kNT) |

| 1,978 |

| 2,077 |

| 2,181 |

| 2,386 |

| 2,660 |

| 2,800 |

| 2,800 |

| Avg. realized price/NT |

| $882 |

| $911 |

| $940 |

| $971 |

| $1,003 |

| $1,036 |

| Net Revenue |

| $3,043 |

| $1,990 |

| $2,158 |

| $2,439 |

| $2,808 |

| $3,053 |

| $3,153 |

| Gross Margins |

| 0.8% |

| 0.8% |

| 6.5% |

| 12.3% |

| 15.1% |

| 18.0% |

| COGS |

| $1,974 |

| $2,141 |

| $2,280 |

| $2,464 |

| $2,591 |

| $2,585 |

| Op. Margin |

| 19.0% |

| -2.5% |

| -2.5% |

| 3.2% |

| 9.0% |

| 11.8% |

| 14.7% |

| EBIT |

| $579 |

| ($50) |

| ($54) |

| $79 |

| $ 252 |

| $ 361 |

| $463 |

| Re-investment |

| $147 |

| $ 480 |

| $74 |

| $90 |

| $72 |

| $56 |

| FCFF |

| ($197) |

| ($534) |

| ($14) |

| $96 |

| $191 |

| $284 |

| Cost of capital |

| 9.8% |

| 9.8% |

| 9.8% |

| 9.8% |

| 9.8% |

| 9.8% |

| PV of operating assets |

| $2,297 |

| ($180) |

| ($444) |

| ($11) |

| $66 |

| $2,864 |

| - MV of debt |

| ($99) |

| + Cash |

| $245 |

| - Value of outstanding options |

| ($82) |

| - Value of underfunded pension plans |

| ($430) |

| Value of equity |

| $1,930 |

Please note that in the model, I have accounted for the long-term investment plan options given to management as well as the outstanding warrants for Algoma. The options were prices using Black-Scholes option pricing model. The warrants are actually exchange traded, and so, I used the current market price for the warrants.

Results from the model yield an intrinsic value of CAD18 per share of Algoma Steel stock. The stock was trading at USD7.74 (CAD10.4) at market close on 2/17/23. Hence, I find this stock being underpriced by over 40%.

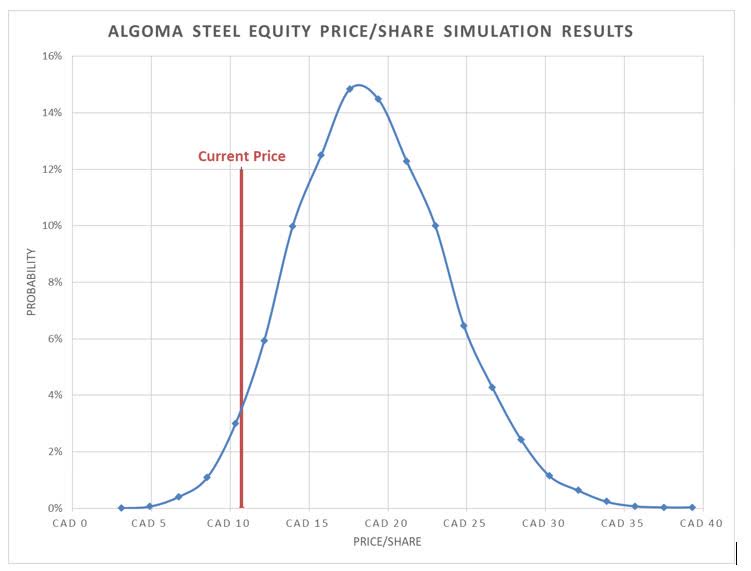

Simulation Results

Results from the DCF model are highly dependent on the key assumptions outlined earlier. Terminal sales volume, price of HRC steel, and terminal gross margins are the key inputs that drive this valuation. Hence, it is prudent to observe the variance in the value per share as a function of these variables.

Monte Carlo simulations were run on the DCF model with these three inputs as variables, with their values being picked from distributions shown in the table below. A set of 10,000 random iterations were performed and the results from this simulation are shown in the figures below.

Input Variables for Simulation

| Variable |

| Distribution |

| Baseline |

| Min |

| Max |

| Std. Dev. |

| Terminal sales volume (kNT) |

| Triangular |

| 2,800 |

| 2,625 |

| 2,975 |

| HRC Steel price (USD/MT) |

| Normal |

| $752 |

| $100 |

| Terminal Gross margin |

| Normal |

| 18% |

| 1.67% |

Frequency Plot of Intrinsic Valuation from Monte Carlo Simulation

{kind=link}

Cumulative Frequency Plot of Intrinsic Valuation from Monte Carlo Simulation

{kind=link}

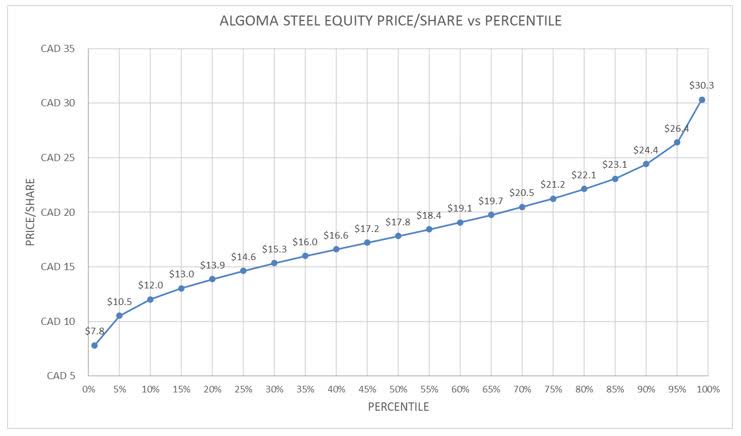

As evident from these plots, the range for intrinsic value goes from the 20th percentile of CAD13.9 to the 80th percentile of CAD22.1. The current price of CAD10.4 lies at around the 5th percentile, translating into a 95% chance that the stock is underpriced currently.

Risks

Algoma faces a number of risks, both market and company specific, which I believe are material and deserve some thought.

Macroeconomic and regional uncertainty – Being a steel producer, Algoma Steel will continue to be exposed to macroeconomic uncertainties. Steel consumption tends to ebb and fall with global economic output. Specifically, since Algoma caters to the North American market only, it is further subjected to the changes in infrastructural, manufacturing and automotive spending in the region. Any loss from manufacturing capacity moving out of this region could be detrimental to its sales volume.

Steel pricing variability and tariffs – Steel gets priced as a global commodity. Overproduction in any region of the world could cause global pricing to fall. China, which produces ~53% of the world’s steel, is the behemoth here. Any overproduction or decrease in domestic consumption in China will have a material impact on global steel pricing.

Recently, different countries have enacted or tightened regulations to arrest the import of steel. This helps with the so-called steel “dumping” by leading global producers in these markets. As such, any North American steel producer will continue to remain exposed to the changes in these regulations and tariffs measures, which make the cost of imported steel costlier or cheaper than domestically produced steel. Though currently such regulations and tariffs are serving as a deterrent against dumping, there could be unfavorable changes in the future. As mentioned before, EAF transition will provide Algoma with some shielding against this risk.

EAF Conversion derailment or delays – Algoma is paving its way into the future with its transition to EAF technology. This is a pivotal change for the company. As such, a derailment of this project could be catastrophic for Algoma’s survival at the very extreme. Any delays in timeline and/or additional capital requirements beyond the CAD750 million anticipated would have a material negative impact on its valuation. While this transition is new for Algoma, several other North American steel producers have made this transition before. Therefore, it has an industry template to follow.

Reliance on single blast furnace – Though Algoma has two blast furnaces (No. 6 and No.7), only one is functional. Historically, this single point of failure has been detrimental for Algoma, wherein failures of this furnace has resulted in long lasting shutdowns and material loss of production capacity. As a contingency, the other furnace can be made operational but it requires a 6 month timespan and at a CAD60 million expense. Again, this risk will be mitigated with the transition to EAF, wherein they will be operating 2 EAF furnaces.

Capital needs & taxation issues – Algoma has gone through a few bankruptcies and changes in ownership in its long history. With some of these being relatively recent, the future possibility of such events cannot be ignored. Having said that, I think Algoma’s capital situation has much improved, with its current outstanding debt at CAD 99 million. Its current debt/equity ratio of 9.2% is much lower than global industry average of 32%. As long as it maintains the financial discipline it has shown recently, this risk will stay muted.

From a taxation standpoint, Canada Revenue Agency is conducting tax investigation for 2018 and 2019. Furthermore, management calls out a risk of US IRS classifying Algoma as a US company for taxation purposes. This reclassification, if enacted, is likely to increase the effective tax rate for Algoma along with some restrictive consequences. To account for this possibility, I have increased the terminal tax rate to 28% from current 25% in the valuation.

Conclusion

I believe Algoma Steel is making the right investments to transform its future. If it can successfully execute the transition to EAF technology, it can improve its gross margins substantially. Moreover, this transition will increase its output capacity by 25% as well as yield secondary benefits of lower carbon taxes and lower maintenance costs. Macroeconomic and steel pricing risks will remain as structural risks for the industry.

Based on my valuation, I find ASTL to be trading at ~40% discount to its intrinsic value of CAD18. I also completed a relative valuation for ASTL using various multiples across global steel producers. In doing so, I adjusted for differences in their fundamentals by running regressions against the fundamental drivers for each multiple. My relative valuation range for ASTL came out to be from a low of CAD10.4 (using EV/Invested Capital multiple) to a high of CAD41.2 (using forward P/E multiple). Currently, ASTL is trading at the low end of this range. This increases my confidence in my valuation thesis that ASTL is underpriced currently. With the 80th percentile of my simulation yielding a value of CAD22.1, I believe this stock has the potential to increase by 100%+. My optimistic scenario predicts a value of CAD34.8, which is over 3.3x current price. However, the stock’s journey to these levels is likely to be bumpy given the challenges Algoma faces for the next couple of years. If an investor can stomach these short-term gyrations (and maybe even use these as opportunistic entry points), I believe this stock has the potential to reward the patient investor handsomely by being a multi-bagger.

One last point to note here is that there are public traded warrants on this stock ( ASTLW ). These have a strike price of USD11.50 with expiration in October 2026. The expiration is about 2 years post the projected transition to EAF, which provides enough time for my thesis to play out. A 3.5X increase in ASTL’s stock price will provide over 10X increase in ASTLW’s price. For the investor who likes to limit the capital exposure but still partake in potential returns, using these warrants may be an attractive proposition. Please note that warrants, like options, carry the inherent risk a 100% loss of investment if the stock fails to reach the strike price by expiration. In this case, I find the risk/reward to be very favorable and personally, this is approach I have chosen to invest in Algoma’s future.

For further details see:

Algoma Steel: A Potential Winner For The Patient Investor