AMZN - Alibaba: Underwater For 1 Year And 2023 Reflections

Summary

- I started accumulating Alibaba Group Holding Limited shares in 2H of 2021 when its price dropped to $140 and below.

- These shares have been underwater for more than 1 year and have suffered drawdowns close to 50% at the worst moment.

- Now, my position is finally above water. And this article reflects on this journey to better shield the future me (hopefully you too) from similar experiences.

- Looking forward, I see the sentiment about Alibaba having turned a corner.

- Alibaba valuation is still cheap. And the possibility of its Ant Group IPO adds another major upside catalyst.

Thesis

As a long-time investor, I learned this key lesson (and am still relearning it over and again). Making a profit for the wrong reason (being lucky is a typical one) is more dangerous than losing money. If I lost money for doing something silly, I am pretty sure I won't do it again. But if I did something wrong and still made money, it could lead me to do it again, at a large scale, and lose more. To paraphrase my son's driving coach, if you drink and drive, you are still a fool even if you make it home safe.

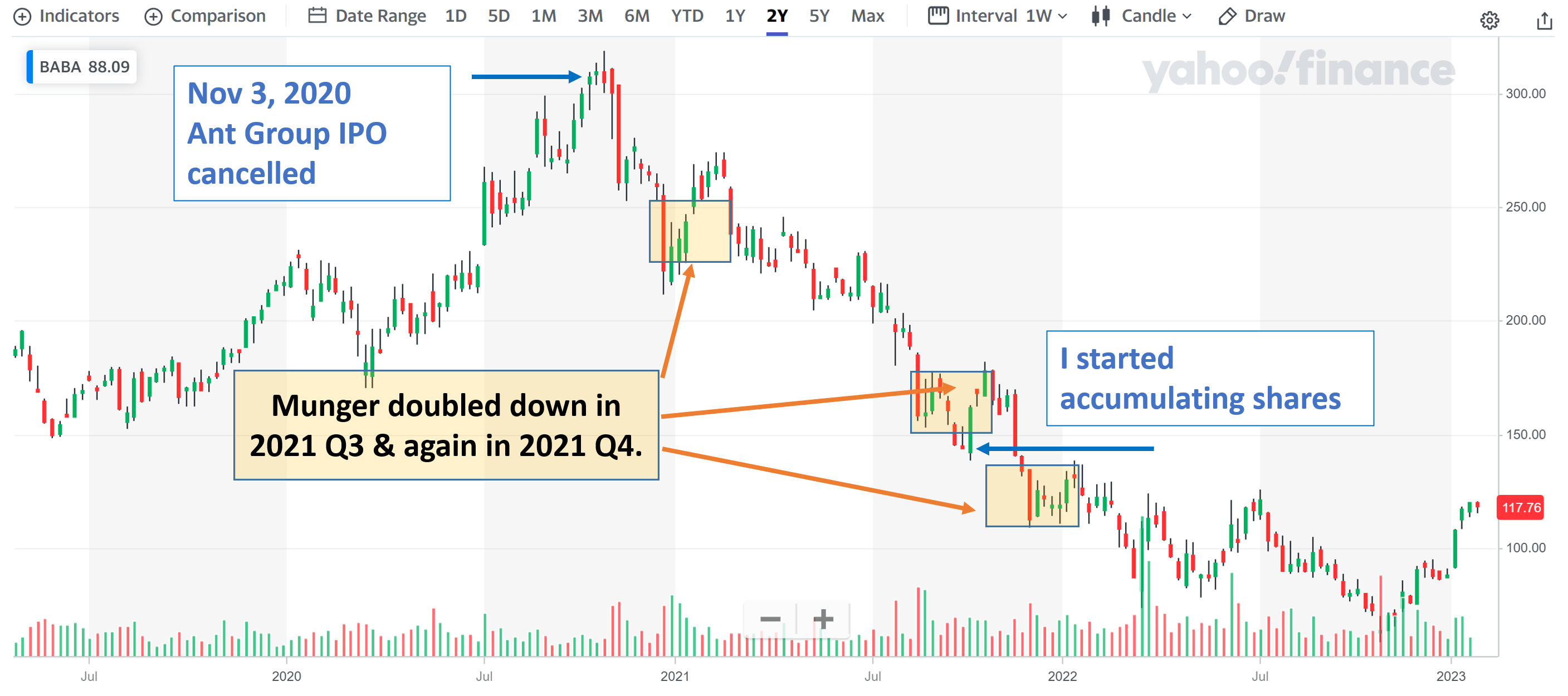

And in this article, I will reflect on my relearning of this lesson again during the past year or so on my Alibaba Group Holding Limited ( BABA ) position. As seen in the chart below, I started accumulating its shares in late 2021 when its price dropped to $140 and below. My average cost basis was about $115 when I built up my full target position in the next few quarters. The rest is history. These shares suffered drawdowns close to 50% when their prices bottomed below $60. the worst moment.

Thanks to the recent rally (its current price of $120 almost doubled from the recent bottom), my position is finally above water. Instead of feeling happy, I feel obliged to reflect on the journey in the hope that an honest reflection could better shield the future me (hopefully you too) from similar painful experiences.

Then after the reflection, I will provide my future plan for my BABA position. In a nutshell, I will keep holding and will explain why I view now as precisely the wrong moment to exit.

{kind=link}

Patience

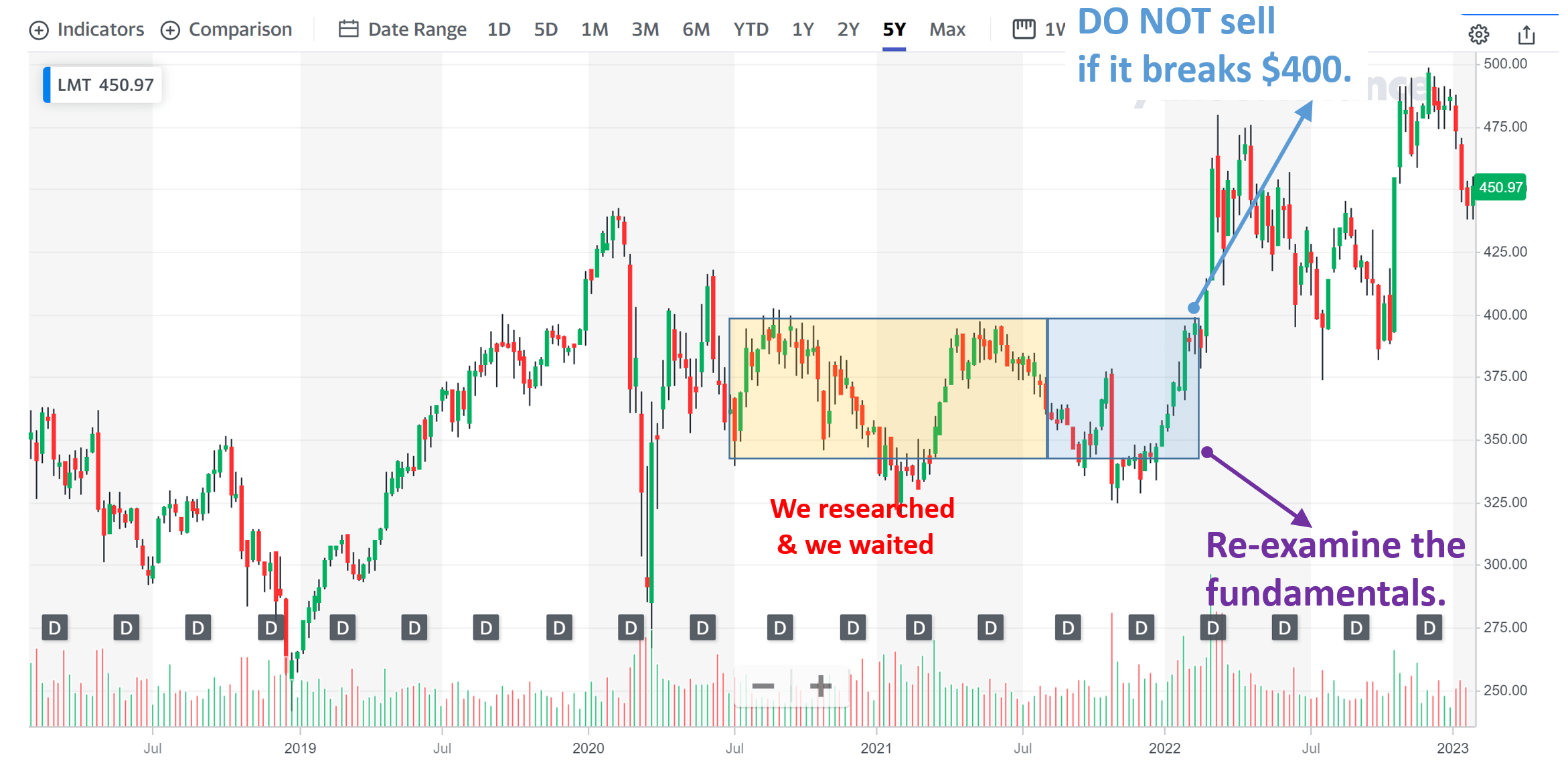

There is simply no way that I could overemphasize the importance of patience in investing. And as I sometimes joke with our marketplace members, they would have already made enough money by only letting me bore them with our "patience rule." Indeed, during the whole of 2022, we only sent a total of ~6 trade alerts (e.g., buy Goldman Sachs at $290 and do not sell Lockheed Martin if its prices break out of $400). You can see these details in our recent blog article here. Through a combination of good research and a LOT of patience, all of these trades turned out to be winners during a very turbulent 2022.

And the lesson of patience works on so many levels.

First, always accumulate shares in a layered fashion. Do not follow the "convicted buy" recommendation no matter where it comes from. The "all-in" strategy is wrong on so many levels - even if it makes a profit. To start with, you won't really know how you feel about the position until you hold some shares. So give yourself a chance to feel it first by accumulating some shares. And in our BABA case, I am glad I followed this rule and accumulated shares layer by layer despite the convicted buy signal from others (including Charlie Munger, as you see from the chart above).

Second, you all heard the caution of "not catching a falling knife." Excellent advice, but not too actionable, though. And my experiences (as detailed in my blog article here ) taught me a more actionable version of it: give a falling knife at least 1 year to fall, then decide if it is time to pick it up or not. This is a rule we've followed closely, shared with our members, and enjoyed great picks (such as Lockheed Martin, and British American Tobacco, as detailed in my blog article). But I deviated from it in the case of BABA and had to relearn this lesson.

And finally, patience also works in the other direction, too. It certainly takes patience to not jump in prematurely due to the fear of missing out. Many of us probably know that it is even harder to resist the urge of exiting (to just get it over with) when your position is finally above water after spending a long time under. Like in my BABA situation here.

And next, I will explain I view now as precisely the wrong moment to exit.

ALIBABA: Sentiment has turned

First, I will argue that there are strong technical signs showing that sentiment has turned. The current situation reminds me of the decisions I made on Lockheed Martin ( LMT ) in earlier 2022. As detailed in a blog article, LMT is a successful case of our patience test applied in both directions. In the buy direction, we researched and waited for more than 1 year. And in the sell direction, we cautioned our readers not to sell if the price breaks out of the $400 consolidation bounds in earlier 2022 because we saw no weakening in its fundamentals. Indeed, the stock climbed to almost $500 per share afterward.

{kind=link}

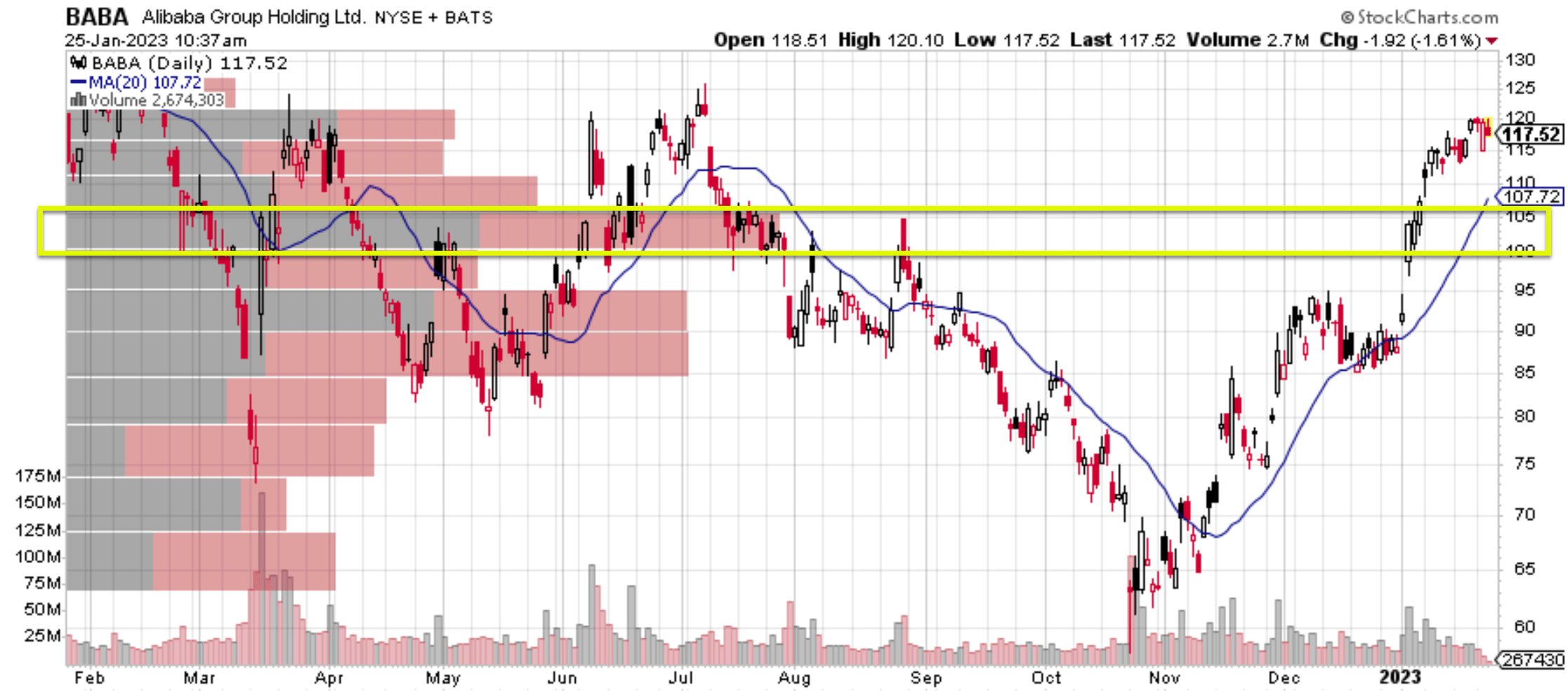

In the case of Alibaba Group Holding Limited, I am seeing essentially the same pattern here. Firstly, the falling knife has been falling for more than one year by now in a consolidation window between ~$75 to ~$120, as you can see from the chart below. And its stock prices have almost doubled recently from a bottom of ~$60 to the current level with strong volumes. The data also show that most of the trading volume in this consolidation window happened in a range between $100 to $105 (as highlighted by the yellow box), quite close to its current price of $117.

And next, I will argue that I am not seeing any weakening in its fundamentals. As such, like in the case of LMT, I'd like caution investors to not to sell if its price breaks out of the $120 consolidation window.

{kind=link}

BABA and its role in the eCommerce space

I have written on BABA's specific segments and growth catalysts (like the cloud segment) extensively below. As such, in this article, it might be a good shift to overview the stock from a higher level. And such a 30,000 ft view actually makes my bull thesis really straightforward. The chain of logic is simple: A) I see our world's transition to eCommerce as invertible; B) Alibaba Group Holding Limited will lead the next phase of this transition; and C) it is for sale at a discounted price despite recent price rallies.

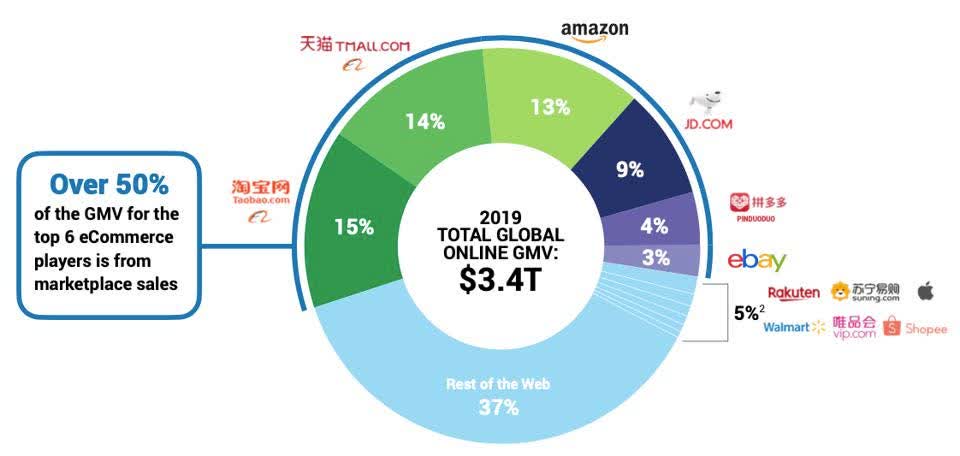

Let me first elaborate on point A. Now, we say "eCommerce" because we need to distinguish "eCommerce" from "traditional commerce." The way I see things, very soon, there would be no need for such distinction anymore. Commerce will be eCommerce by default and vice versa. And BABA is the one best positioned in this mega transition. As reported by this Forbes analysis , current eCommerce is dominated by a total of 6 companies as shown in the chart below. Together, they control 58% of the global eCommerce. Four out of six of them are from China - and there is a good reason for it as the Forbes report pointed out below (the highlights are added by me):

And just four Chinese companies account for almost half of global digital sales. The biggest digital commerce companies, with the percentage of the global e-commerce market that they own are Taobao.com 15%, TMall.com 14%, Amazon 13%, JD.com : 9%, Pinduoduo 4%, and eBay: 3%. One key reason: retail in China is simply much more digital than it is in Europe or North America.

I share with Forbes' above view. I view the China market, or more broadly the Asian-Pacific region, as more ready to embrace the everything-digital future. And BABA, as the leader in this space, is best positioned to capitalize on such a transition. Yet, it is still trading at a heavily discounted valuation, as we will see next.

{kind=link}

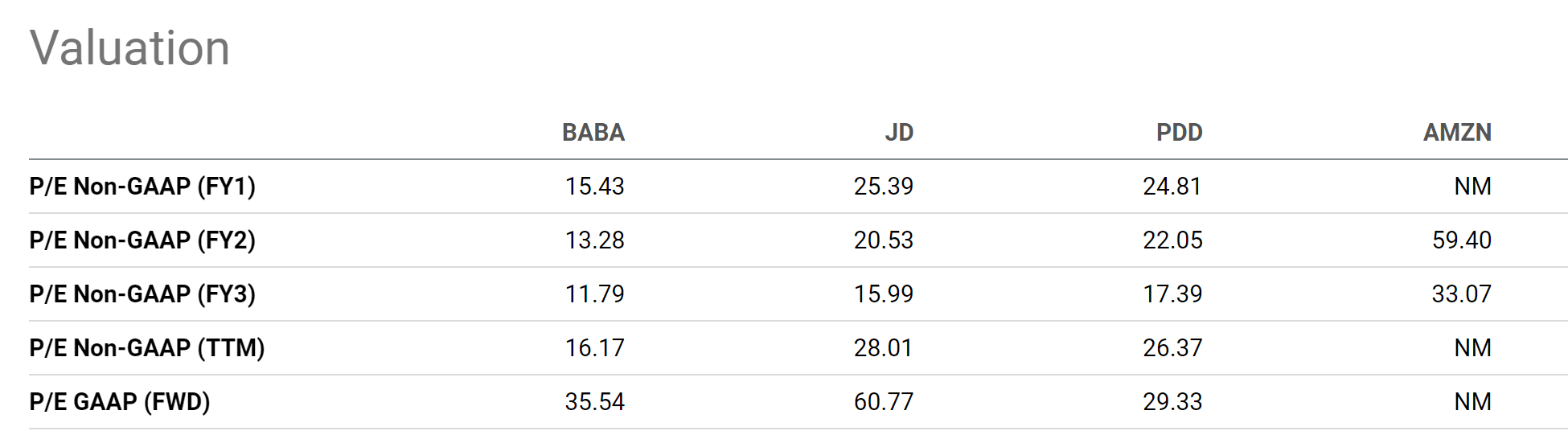

Valuation is still too cheap

The chart below compares BABA's valuation metrics against its closest peers mentioned above, including JD.com ( JD ), Pinduoduo Inc ( PDD ), and also Amazon.com ( AMZN ).

As seen, its P/E multiples are only a fraction of these peers across the board. To cite a few examples, its P/E is 15.4x on an FY1 basis and 16.1x on a TTM basis. Its FY1 P/E of 15.4x is about 40% discounted from JD's 25.4x and PDD's 24.8x. At the same time, keep in mind that BABA has a sizable net cash position ($11.07 per share as of this writing). The cash position is about 10% of its current share price and if the cash position is adjusted for, its P/E multiple would be even lower. There are some profitability differences between BABA and its peers, both in China and overseas as detailed in my other BABA articles. However, I see such valuation discounts as severely overdone and difficult to justify.

{kind=link}

Risks, Ant Group IPO, and final thoughts

There are still risks surrounding BABA in the near future, ranging from the macroscopic economic condition in China after it lifted its zero COVID policies to operational risks specific to BABA. Here I wanted to focus on its Ant Group IPO a bit more, the issue that got my interest in the first place.

Recently (earlier this month), Jack Ma ceded his control of the Ant Group . With this development, he is estimated to own about 6% of Ant only. And I view this development as a key catalyst for another IPO attempt. And if the IPO does revive and proceed, BABA's current valuation would represent a further discount. Actually, in that case, it would be a good investment purely as an asset purchase with all its future earnings ignored, as detailed in this article I wrote earlier. Of course, there is always the possibility that the IPO won't get revived and hence representing a major uncertainty.

All told, with my Alibaba Group Holding Limited position resurfacing above water, rather than feeling lucky or glad, I feel timely to reflect on the journey. I am glad I accumulate shares layer by layer despite the "convicted buy" signals. But I deviated from my patience test and relearn the lesson of letting the knife fall for at least 1 year. At this point, I want to caution myself that patience also works in the other direction too. It certainly takes patience to not jump in prematurely (which was a mistake I made). At the same time, it also takes patience to resist the urge to exit and "just get over with it" when my position just begins to see light from the other end of the tunnel. And, in the case of Alibaba Group Holding Limited, I feel now is precisely the wrong moment to exit considering both the technical and fundamental signals.

For further details see:

Alibaba: Underwater For 1 Year And 2023 Reflections