CA - Alimentation Couche-Tard: A Fantastic Business Just Too Expensive

2024-01-19 12:11:08 ET

Summary

- Alimentation Couche-Tard is a leading convenience store operator with a strong track record of making successful acquisitions.

- The company plans to target $1.1 billion in additional EBITDA by FY2028.

- Couche-Tard aims to expand its presence in Latin America, Southeast Asia, and Europe, while also focusing on margin expansion through initiatives in food and beverage, fuel, and loyalty programs.

- Despite its track record, balance sheet management, and potential for margin expansion, shares seem expensive at the current price.

Please note all $ figures in , not , unless otherwise stated.

Company Overview

Alimentation Couche-Tard ( ATD:CA ) is a convenience store operator that started in Quebec Canada in 1980. Over the years, the company has carried out a series of successful acquisitions through a roll-up strategy that has enabled the company to take a market-leading position as the second largest convenience store operator in the United States (only second to 7-Elleven). Through its Couche-Tard, Circle K, Ingo, and On the Run banners , the company now has an international presence in over 25 countries through its network of 14,400 stores.

Track Record of Successful Acquisitions

As one of the largest non-financial services companies in Canada, Couche-Tard has been one of the best performers on the TSX. When looking at the historical share price performance of the company, we can see that the company's shares have beaten the TSX by a wide margin, returning 500% over the last ten years compared to the TSX's return of just 49.6% return over the last decade.

Much of this growth has been as a direct result of the company's successful track record of growing by acquisitions, consolidating what is a very fragmented market. At present, about three-quarters of the company's current store network have been sourced as a direct result of M&A. With a market share of about 5%, despite being the second largest player in the United States, there is still ample room to continue consolidating the market. Keep in mind that this is an industry with very few new market entrants and there is more value in owning a chain of convenience stores (eg. buying in bulk, brand name recognition, economies of scale in fuel) than operating a single location.

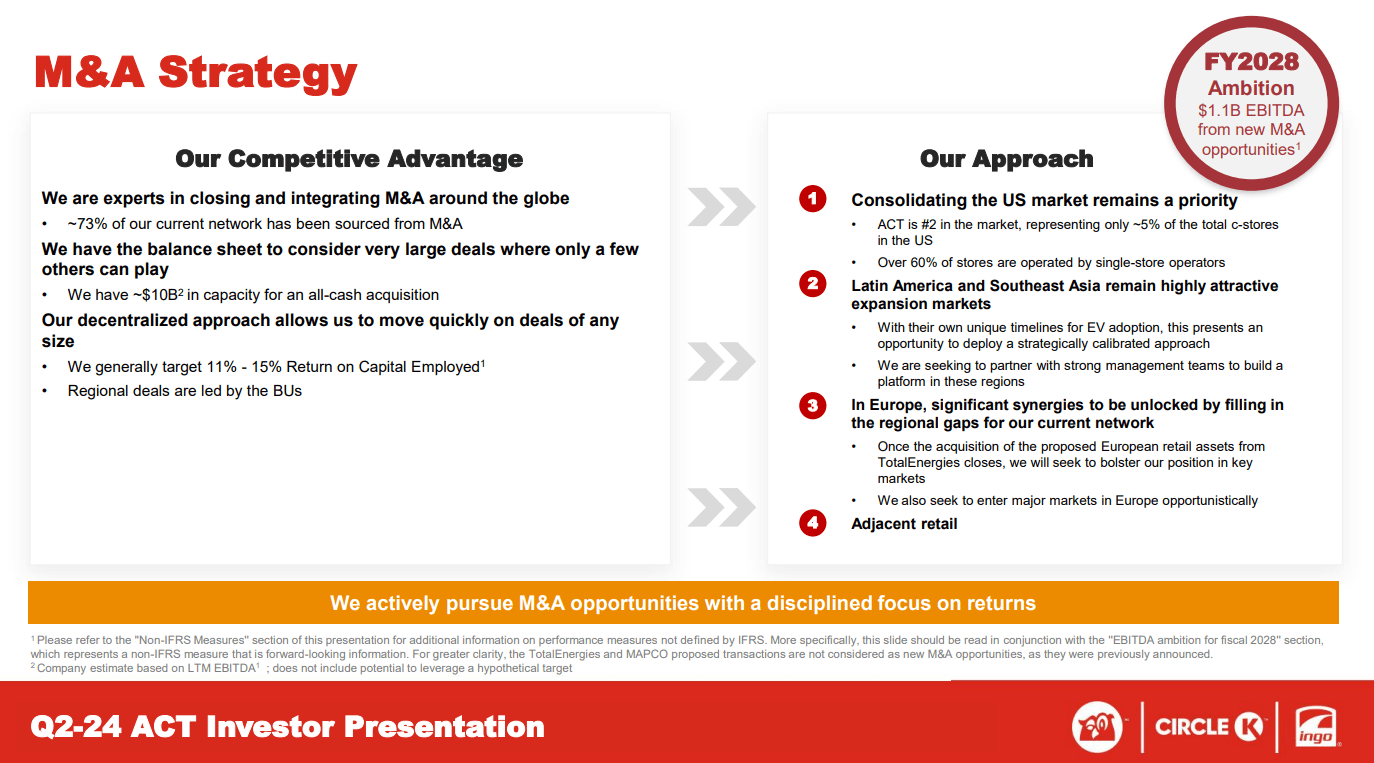

As well, with the vast majority of convenience stores being single-store locations (about 60% not being attached or owned by a brand name like Couche-Tard or 7-Elleven), so Couche-Tard views consolidation as a key priority going forward. They have ambitious plans to target $1.1 billion in additional EBITDA by FY2028 from new M&A opportunities.

M&A Strategy (Investor Presentation)

{kind=link}

In addition to the United States, which represents 66.3% of revenues, Couche-Tard also expects to expand its presence in Latin America and Southeast Asia. Because these markets are higher growth compared to the United States, the market opportunity there is relatively untapped. We're also witnessing acquisitions taking place in Europe with the purchase of key assets from TotalEnergies. So despite the more mature market here, it seems that Couche-Tard is finding no shortage of opportunities to grow internationally.

It can be extremely difficult to execute a successful roll-up strategy. In fact, most roll up strategies, around two-thirds , fail. They often fail because they often pay too much for acquisitions, take on too much debt, fail to integrate acquisitions successfully, fail to merge competing cultures, and can't meaningfully generate synergies or prove out margin expansion.

However, in my view, Couche-Tard has been one of those rare gems who've been able to do it right. Led by CEO Alain Bouchard, the company's founder, the management at Couche-Tard have been exceptional capital allocators , with an impressive track record of not only growing sales at very consistent rates, but also earnings with margin expansion.

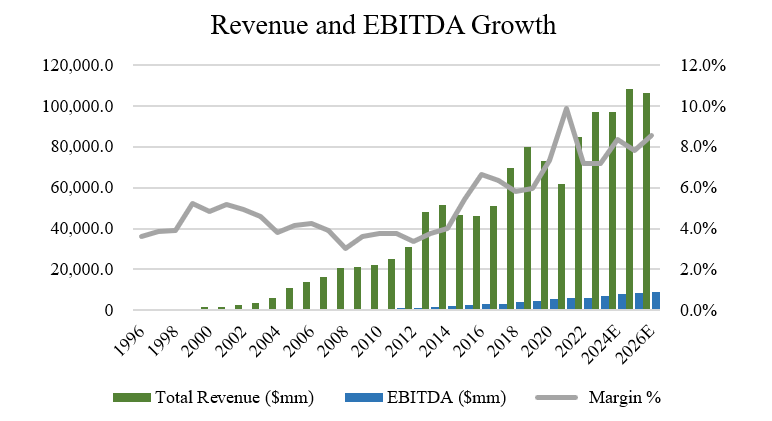

As shown by the graph below, you can see that Couche-Tard has compounded revenues and EBITDA at 7.3% and 14.5% CAGRs over the last decade and 18.4% and 21.1% CAGRs over the last 20 years, respectively (S&P Capital IQ). I believe these growth rates illustrate the track record the company has of integrating acquisitions successfully as well as steadily increasing margins over time.

Revenue and EBITDA Growth (Author, based on data from S&P Capital IQ)

{kind=link}

Importantly, Couche-Tard has been able to carry out its M&A strategy with minimal debt on its books. At the end of its most recent quarter , the company had $5.98 billion of long-term debt on its balance sheet against its cash position of $1.40 billion for a Net Debt figure of $4.58 billion. With LTM EBITDA clocking in at $7.08 billion the company has a Net Debt to EBITDA ratio of 0.65x, which is pretty healthy for a highly acquisitive company like Couche-Tard.

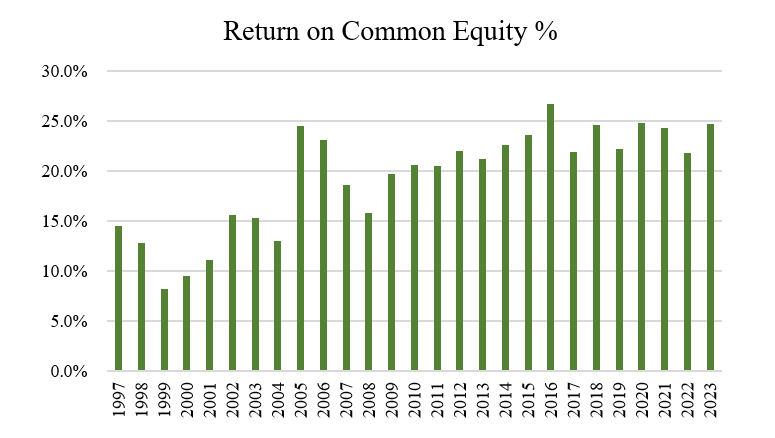

Because Couche-Tard generally targets an 11-15% return on capital employed figure, the company is very disciplined in the price it pays for targets. While most purchase price multiples are not disclosed, we can infer from the consistently high return on equity figures (20%+) over the last decade that the company doesn't over pay and can achieve consistently high returns on capital without over leveraging itself with excess this. To me, this track record speaks volumes about Couche-Tard's ability to create shareholder value for investors over the long-term.

Return on Common Equity (Author, based on data from S&P Capital IQ)

{kind=link}

Potential For Margin Expansion

Couche-Tard has undoubtedly been successful in its roll-up strategy and has improved margins at the corporate level over time. Going forward, I think there's still reasons to be optimistic on how the company can continue to improve its profitability over the next few years.

On the company's latest earnings call , management discussed its 10 for the Win plan, which is the company's 5-year strategy to enhance value for shareholders. By fiscal 2028, the company expects to achieve $10 billion in EBITDA, which is 60% derived from a 7.5% organic EBITDA CAGR and the other 40% coming from $1.8 billion in acquisitions and synergies (about half of which are expected to come out of the TotalEnergies purchase).

The organic growth portion is expected to come from five key initiatives, but to summarize, the primary ones include focusing on food and beverage, outperforming and gaining share in fuel, and enhancing loyalty and digital capabilities.

On the food and beverage front, the company wants to beef up the sales penetration rate of 11% for the company's Fresh Food, Fast and prove out the organic growth of this initiative. Fresh food is a key area of growth for Couche-Tard and is an area where the company has already seen 500 basis points of margin expansion. Going forward, the company expects to drive gross profit in the mid to high teens CAGR, so there's a real opportunity here in both fresh food and private label to steadily increase margins. It also helps them depend less on large manufacturers and other national brands and develop customer loyalty with their own products. In beverages, the company wants to expand cooler space from 3000 locations to 5800 by fiscal 2025. I believe this could be pretty accretive to both margins and return on capital so in my view this is an initiative that requires little capex or investment to meaningfully improve margins.

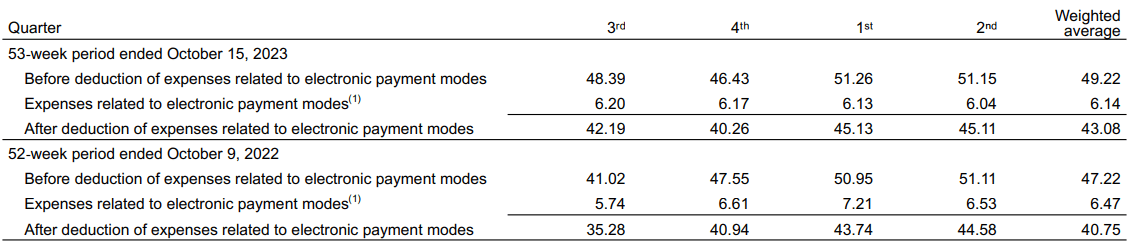

In fuel, the company sees $400 to $600 million of additional EBITDA growth that should come from leveraging scale advantages. Many of its North American sites have been in the process of being rebranded to Circle K fuel (73% to 81% in fiscal 2025). In my view, with better performance coming from fuel margins quarter over quarter, the company is seeing growth in both volume and margins as Couche-Tard drives traffic through "reoccurring promotional fuel days".

Fuel Margins Expanding (Company Filings)

{kind=link}

While there is a risk that fuel margins could contract (ethanol, natural gas, and fuel prices can be highly volatile and uncertain), I believe the company's scale and promotional initiatives should mitigate any potential headwinds to margins. In addition, the company often situates its gas stations in truck-friendly locations and really focuses on the driver's experience in store, so the risk seems to be mitigated by the company the best it can.

Finally, on the loyalty and digital side, Couche-Tard is focused on accelerating its Inner Circle initiative, a loyalty program that was designed to reward frequent customers to Circle K and enhance brand loyalty. Given that this is now seeing traction, with 8 million members up from 2.7 million in June, the company is experiencing strong adoption of this loyalty program. Furthermore, as we're still in the early days of smart checkouts for the company (only 3250 stores), I believe labor costs could come down as smart checkouts eliminate the need for excess employees (thereby increasing profitability for Couche-Tard).

Valuation and Wrap-Up

No question about it; Couche-Tard is a fantastic business with a history of successful M&A and a balance sheet well-equipped to support it. Despite my optimism for margin expansion going forward and the defensive nature of the business that make it a good hold in almost all market conditions, the issue I have with Couche-Tard is that its valuation is a little over stretched right now.

Based on the 11 sell-side analysts with one-year target prices on Couche-Tard's stock, the average price is $86.90, with a high estimate of $94.00 and a low estimate of $80.00. From the current price to the average price one-year out, this implies potential upside of 10.3%, not including the current dividend yield of 0.9%, suggesting analysts are moderately bullish on the company's near-term outlook.

But when I look at the historical valuation range of Couche-Tard and the comparable companies, I can't help but feel like the price one is paying today is quite high at 11.1x EV/EBITDA and 18.7x P/E. At 11.1x EBITDA, above the five-year average multiple of 9.8x, the multiple seems a little stretched.

Comparing the company to peers like Parkland Corp. ( PKI:CA ), Murphy USA ( MUSA ), Arko Corp. ( ARKO ), and Casey's General Stores ( CASY ), these companies have EV/EBITDA ratios of 7.6x, 9.4x, 8.0x, and 11.8x EBITDA. With an average for the peer group around 9.2x, Couche-Tard's valuation is about 2 turns higher at 11.1x EBITDA.

In my view, this valuation would be justified if Couche-Tard had the ability to grow faster than the peer group. But this isn't the case, with an expected revenue CAGR three years out to 2026 of 3.4%. Compared to Casey's General Stores, a company I recently covered and gave a 'buy' rating, Casey's has a slightly higher valuation but is expected to grow at nearly twice this rate.

So in my view, shares of Couche-Tard are a bit overvalued for now. If we got to around 8.0-9.0x EBITDA, closer to the rest of the peer group, I would strongly consider taking a position in the company, given its track record of making great acquisitions, disciplined capital allocation and balance sheet management, and potential for margin expansion. For now, however, I'll be waiting on the sidelines.

For further details see:

Alimentation Couche-Tard: A Fantastic Business, Just Too Expensive