ENBA - Allstate 8% Yielding Debentures: Higher For Longer Vs. A Fed Pivot

2023-04-02 06:00:00 ET

Summary

- Allstate subordinated debentures started paying a floating interest rate.

- The 8% yield looks juicy and comes with a high credit rating.

- We look at what the Fed funds futures are pricing in and whether Allstate will redeem these expensive notes.

Operating via subsidiaries, The Allstate Corporation ( ALL ) is an insurance provider. Be it automobile, home, health, accident, life, or personal property, Allstate can assist with it all. The various insurance products are allocated between five reportable segments in their financial statements, with Allstate Protection bringing home the bulk of bacon.

{kind=link}

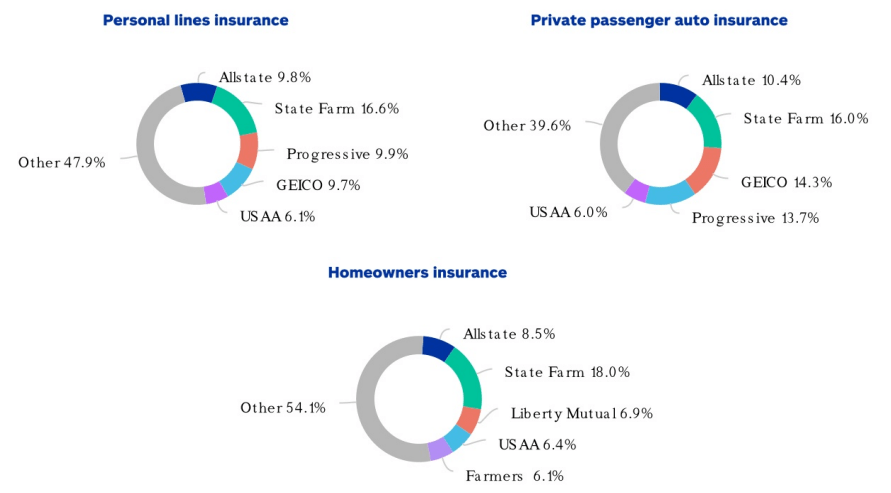

Included in the Allstate protection category is the personal lines insurance. Allstate was kind enough to show their share of this highly competitive segment in the US measured in terms of direct premiums written for the 2022 calendar year.

{kind=link}

Allstate operates primarily in the US and Canada, with four stateside names making up close to 37% of the total direct premium pie in 2022.

2022 10-K

While it has been at the forefront compared to some of its publicly traded peers in the last decade...

...it has lagged since the pandemic. Still, at least the returns have still been in the positive territory.

It is leading again in the last one year, albeit from the bottom.

Allstate seems to taken Ricky Bobby's wisdom to heart; "If you ain't first, you're last."

While the common shares have their merits and certainly at the current valuation we can see a good case for them, we do want to focus on another security in the capital structure. This comes about as our renewed focus in this climate is on fixed income with an emphasis on capital preservation.

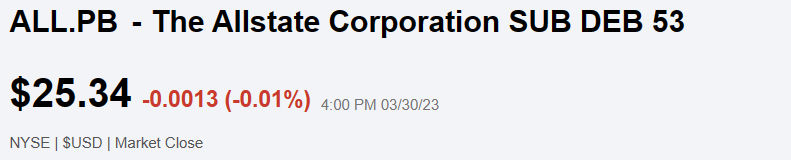

Allstate Corp. Sub Debentures due 1/15/2053 ( ALL.PB )

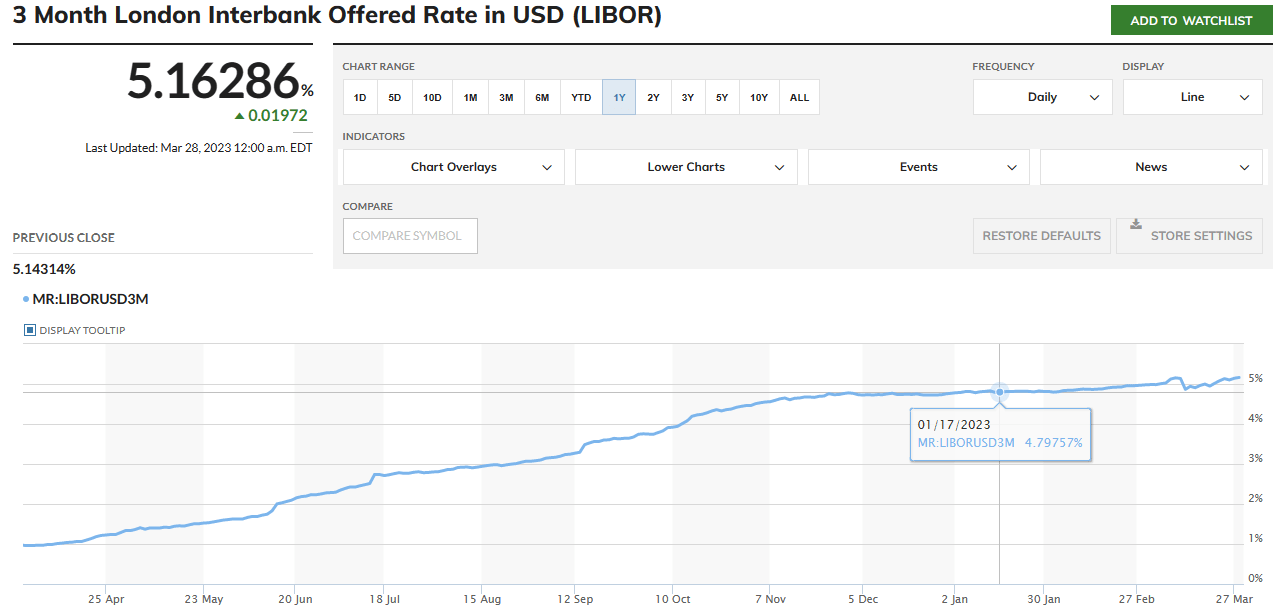

These debentures were fixed rate (5.10%) until January 15 of this year. On January 15, 2023, the rate floated and is set at three month LIBOR plus 3.165%. These $25 par value securities also became callable at the issuer's option effective that date.

{kind=link}

The debentures are subordinated to the senior notes and carry a rating of BBB from S&P. This is two notches below the corporate credit rating of A-.

Its current yield based on the LIBOR rate on the January reset rate is close to 8%, and based on the current rate, the next reset in April should comfortably get it to over 8%.

{kind=link}

With around 41 cents of accrued interest reflected in the current price, the yield to maturity is slightly higher than the current yield since this security currently trades under its par.

{kind=link}

From a fixed 5.10% to almost 8%, in hindsight, Allstate could not have chosen a worse time for the fixed rate training wheels to come off. With regards to the interest payment, provided the debentures are not in default, the company has the right to defer the payments for up to five years, but not beyond the maturity date.

Outlook

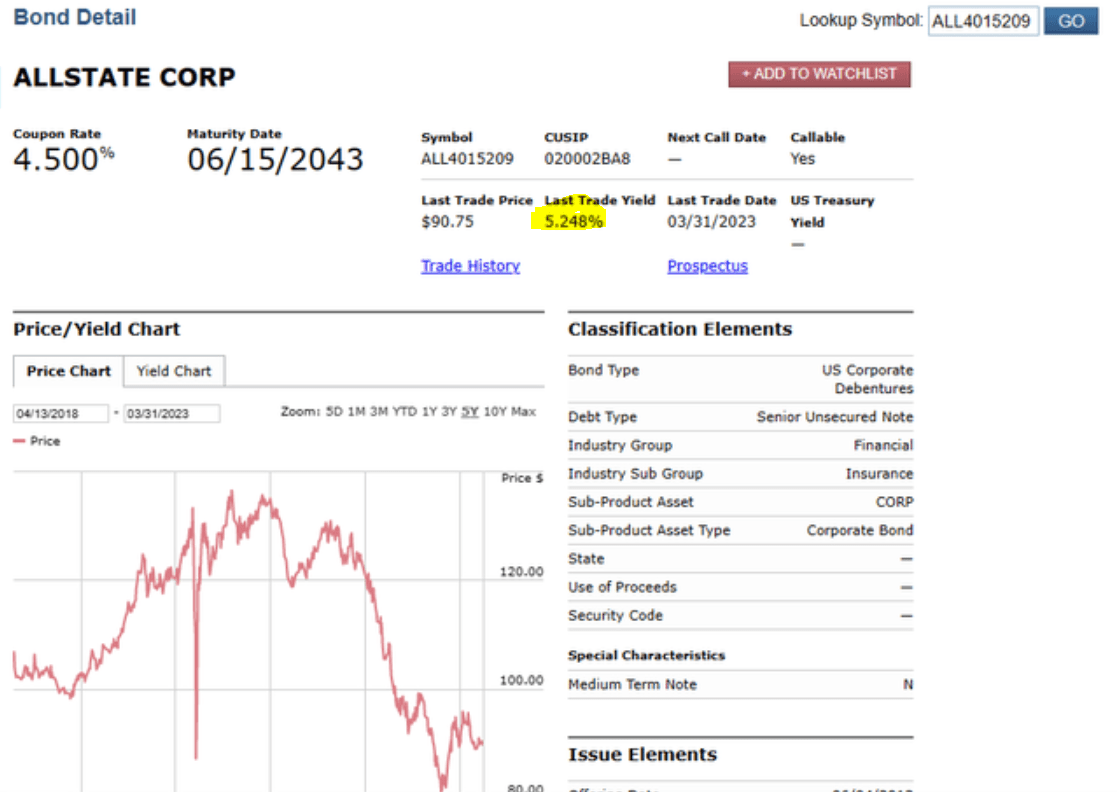

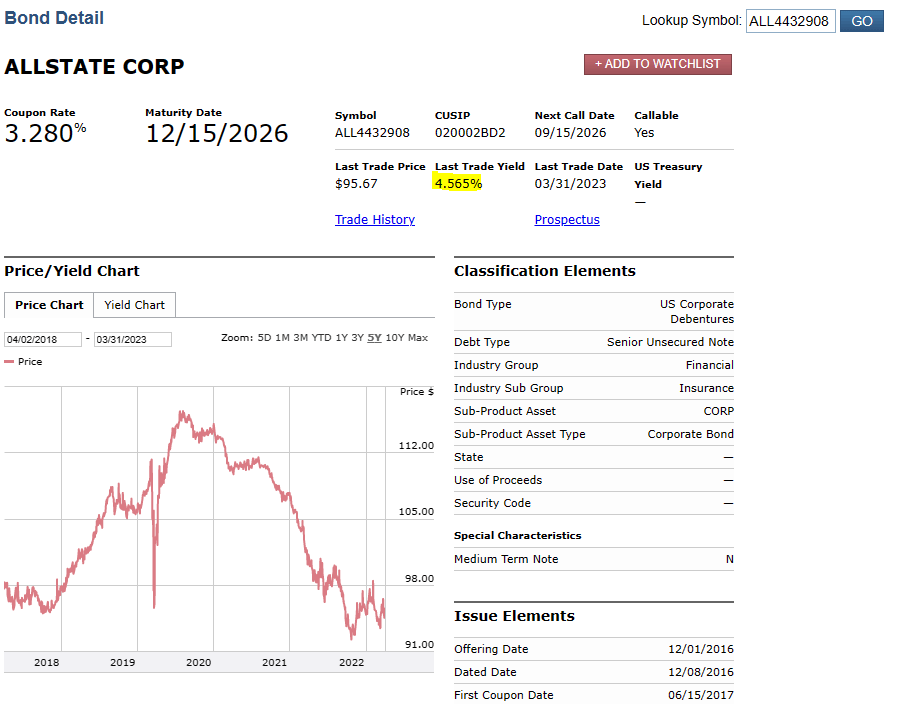

ALL.PB's float puts the company in an extremely interesting situation. The current payout is ridiculously high for ALL.PB. Let us show you exactly what we mean. Currently, Allstate's bonds from 10-20 years out, yield about 5.0%-5.5%. We have shown one below.

{kind=link}

Its near term bonds have an even lower yield with the December 2026 bond yielding just 4.565%.

{kind=link}

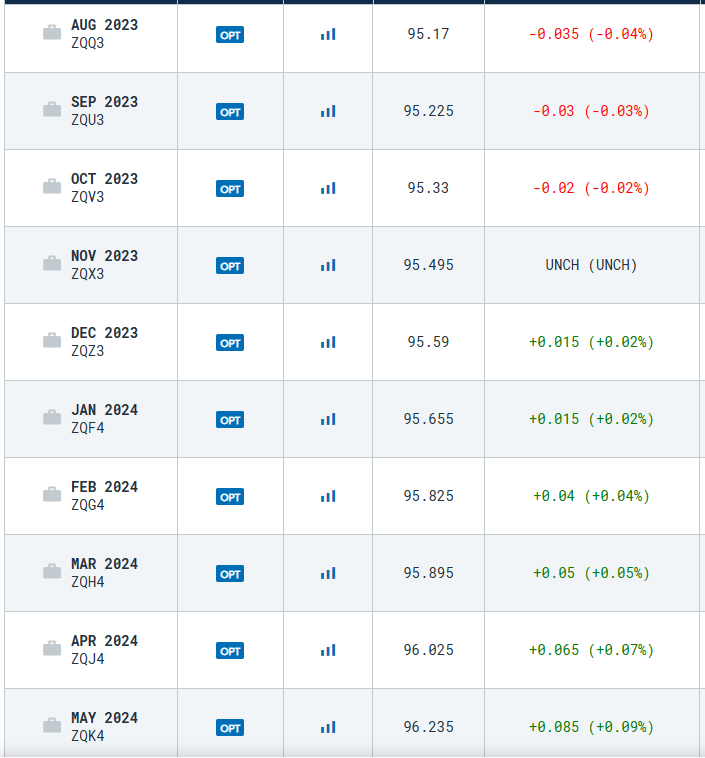

So paying an 8% plus rate is rather unusual. Companies have generally been quick to call these high floaters. Enbridge Inc. 6.375 SNT18 B 78 ( ENBA ) which we wrote about (See, An Easy Way To Play A Hawkish Fed ) was called as soon as possible. Reinsurance Group of America, Incorporated's ( RGA ) fixed to floating baby bond was delayed slightly, but was called piecemeal within 3 months of the floating date. The fascinating aspect is that the yield curve has become even more inverted since then and longer dated financing for corporates is far more appealing than floating rate financing. Perhaps the argument is that Allstate expects the rate to move rapidly lower. Certainly that Fed pivot has been on everyone's mind, but the question remains as to what extent will they cut. The Fed Fund Futures is pricing a 4% Fed Fund rate by April 2024, 1 year from now.

{kind=link}

So cuts yes, but not too many. Even at that rate, Allstate will be paying more than its near term debt.

The other argument may be that Allstate is using this as a "hedge" on its books. Insurance companies of all stripes hold massive amounts of assets (which ironically are actually called a "float").

Those assets are invested in bonds of all maturity lengths but a lot are focused on the short end. Insurance companies need such assets which can be sold rapidly without impacting price to pay large claims. So Allstate's higher interest costs are "internally hedged" to an extent as they also make more interest dollars on a far higher portion.

Verdict

The recent call on The Allstate Corporation DEP 1/1000 PFD G ( ALL.PG ) is interesting as Allstate was not ready to continue paying 5.625% on preferred shares.

{kind=link}

While ALL.PB continues to float, we don't think this will continue for long. Even after the taking into account the potential reasons mentioned above, we think Allstate is better off by calling these, and it will happen, likely on the next Fed Funds Futures move that prices out rate cuts. Investors should view this as a modestly risky security from an interest rate perspective. If we are wrong and the Fed does indeed shower us with an armada of rate cuts, you could be left holding a very poorly yielding security. In an era of ZIRP, ALL.PB would give you close to 3.5% on par. There would be substantial downside in that case and ALL.PB could trade 25-35% lower. For those convinced in the "higher for longer" outlook, this could be an excellent income security with a short maturity.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Allstate 8% Yielding Debentures: Higher For Longer Vs. A Fed Pivot