APO - Alternative Asset Managers Getting Into Insurance: Beware Of The Changing Risk Profile

2023-04-29 01:24:20 ET

Summary

- Alternative asset managers seem to have fallen in love with another way to access other people's money - buying insurance companies.

- They tend to market this as simply another way to get access to permanent capital.

- I will try to show that the insurance industry is fundamentally different from the alt asset management business.

- Investors need to be aware that being in insurance substantially changes the risk profile.

Introduction

Being an asset manager is great: You risk other people's money and get paid for it (management fees).

Being an alternative asset manager is even better: You risk other people's money and get paid a lot for it. Plus, if you are successful, you get paid even more by keeping a part of the gains (carry/performance fees).

Being an insurance company must surely be best: You get to invest other people's money, get paid for it and keep all of its excess returns instead of just the usual 20% cut with carry. In the end, wasn't that how Warren Buffett became one of the richest persons of the world?

No wonder many alternative asset managers have recently started purchasing insurance companies and have big growth targets. And they are more than happy to communicate this to their investors touting it as accessing "permanent capital". But do they have the right mind set and discipline to succeed?

In this article I want to highlight the motivations as well as the dangers of alternative asset managers moving strongly into insurance. I intend to show that this fundamentally changes the risk profile of the business depending on the structure of the deals. Insurance is much more than just another pool of permanent capital to manage. Investors in that space should understand this.

Alternative asset managers move into insurance full speed

There has been a lot of deals recently with leading alternative asset managers acquiring insurance franchises or stakes in them in the past few years. Here are some examples:

Brookfield acquires American National Group for $5.1bn. Apollo buys/merges with Athene Holding for $11bn. ARES (re)insurance subsidiary Aspida acquired Global Bankers Insurance Group for an undisclosed sum. KKR acquires a majority stake in Global Atlantic valuing the company at $4.7bn. Blackstone entities acquire the former Allstate Life which is now called Everlake Life for $4.0bn. Carlyle Group and partners acquired a majority stake in Fortitude Re from AIG in 2019 for $1.8bn and invested another $2.1bn growth capital in 2022.

Therefore, clearly, insurance is hot for alternative asset managers. And it is not only that they buy them in their funds but many take them on their own balance sheet or as owned subsidiaries and intend to own those insurance companies for good. They do this to differing degrees.

What is the attraction of insurance to alternative asset managers?

For asset managers it is all about assets under management (AuM). On this they earn fees and in the alternative space also take a cut on returns if they are successful. While typical private equity funds lock in capital for up to a decade there is something even more alluring: permanent capital! Some companies like Brookfield do this by listing subsidiaries like BIP or BEP, others go for business development companies, closed end funds. etc. But alternative asset managers also view insurance as permanent capital (at least they do in their presentations) although of course it isn't - it just tends to be very long duration. Insurance companies collect premiums to eventually pay out their policyholders. The time span from collecting those premiums to payout can be decades. Even in the so called short tail businesses like auto or home insurance companies regard the so called float as kind of permanent as it constantly renews with new premiums. This is a concept popularized by Warren Buffett.

And unlike other investors in permanent capital vehicles policyholders either do not have specific or generally fairly low return expectations. This means you can invest other people's money ("OPM"), give them a pittance and keep the rest! Amazing! No wonder alternative asset managers get drawn to this like moths to the flame! It's just surprising it took them so long. Hedge fund managers have been doing this for a long time already (and often messed it up like e.g. GLRE or SPNT ).

Why insurance isn't asset management

However, insurance is not asset management! In fact there are four main differences:

1. Assets and investment risk

2. Liabilities

3. Asset-Liability mismatch

4. Regulation

I now want to shed some light on those issues and why insurance is not just another pool of permanent capital for asset managers but a fundamentally different business.

1. Asset and investment risk in insurance

When investors give their money to alternative asset managers they know they are investing at their own risk in hopes of high returns. And because of this they are also willing to accept losses should they occur. A buyer of insurance on the other hand wants to offload risk. They will expect to be made whole on what they were promised - be it a certain crediting rate or the repair costs of a car.

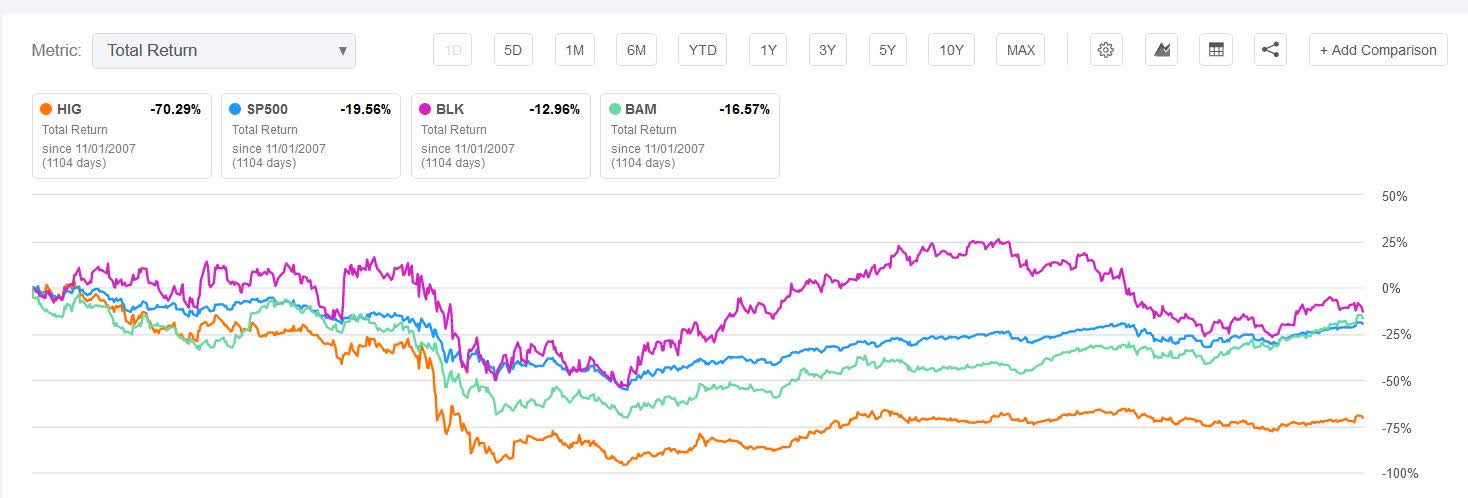

Therefore, while the insurance company gets to keep all the upside they also have to take on all of the downside. This is fundamentally different from being purely an investment manager. While positive investment performance is at the core of both business models in cases like the great financial crisis 2008 as an asset manager you can always try and convince your investors that those were black swans and impossible to foresee so that they stay invested with you. They will bear the losses but your business model is not destroyed and can recover in calmer periods of the market. If you however carry the investment risk an even only temporary poor investment result might necessitate a highly dilutive capital raise or even government bailout. An example would be The Hartford ( HIG ). In Q3/2008 they faced massive investment losses which first led to a capital injection by Allianz SE (ALIZY) and eventually a $3.4bn government bailout in June 2009.

HIG performance Nov. 2007- Nov 2011 (Seeking Alpha)

{kind=link}

HIG's share price dropped by over 95% during the financial crisis and hardly recovered with the markets due to dilutive equity issuances and bailouts (see regulatory risk below). As one can see BlackRock and Brookfield recovered with the overall market.

If you now think: well, then it is just like investing on their own balance sheet with a lot of leverage like e.g. Brookfield does with their real estate portfolio you are still (partly) wrong. Because insurance liabilities are very different from debt.

2. Liability risk in insurance

If companies take on debt to lever up they normally know how much they will have to pay back and when. This is not the case with insurance liabilities. Both amount and timing can be uncertain. Insurance liabilities also known as "reserves" are generally just best estimates of what it will eventually cost to satisfy the contractual obligations to policyholders.

Life insurance companies tend to cover two basic mortality risks: Either they sell pensions products which provide a life-long income stream in retirement. Or they sell protection products which will pay out a certain amount to the beneficiary if the insured person dies. Therefore, for insurance companies the basic risk is that people either live longer or die earlier than what they anticipated in their respective pricing (it is always about what happens in reality vs. what they expected when they priced the products). Unfortunately, those two risks do not cancel each other out. Improvements in life expectancy often tend to happen due to medical progress that is especially impactful for elderly people which no longer have protection products but will benefit from longer pension payments.

The "risk" of people living longer is called longevity risk and is generally a good thing for everyone but the pension provider. Because if people live longer they need to pay out income for longer as well. Actuaries got this wrong for decades! They constantly underestimated the improvements to longevity which lead to strong reserve increases in the past. That said, it finally seems to level out which implies there is very limited risk from that side for the time being. Unless you go to Seeking Alpha's biotech section and learn about all the cures for cancer and similar diseases that the companies there promise. Or if you believe Dr. Aubrey de Grey who thinks "...that the first person that will live to be 1,000 years-old has already been born."

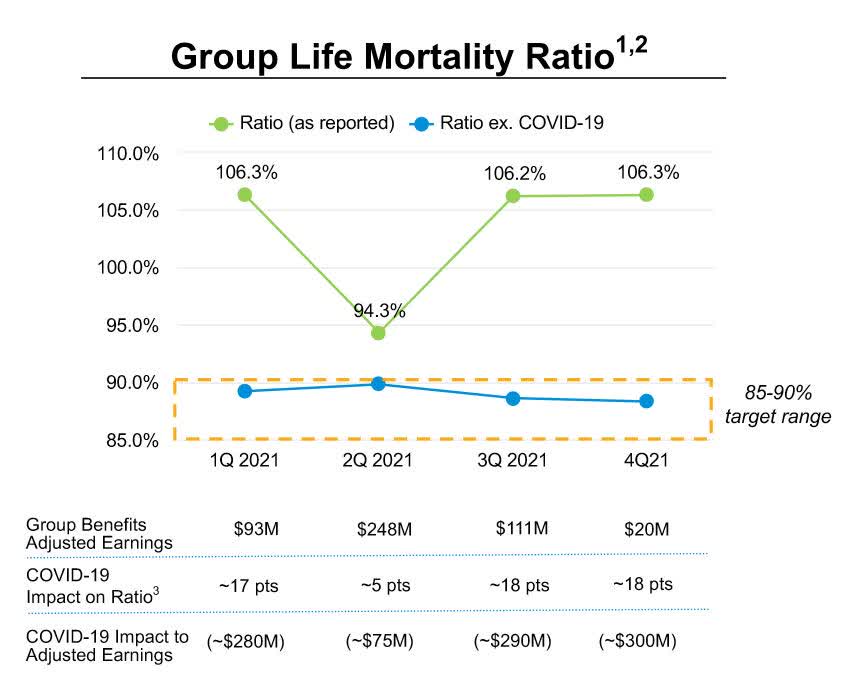

Those providing protection rather than pension products face mortality risk (i.e. if people die earlier and more frequently than initially anticipated they need to pay out the insured sum more often than they anticipated in their pricing). We just had a pandemic that was luckily not that lethal but eventually another one will show up and maybe that one will be much worse. Still, COVID-19 already had a sizeable impact as can be seen here with MetLife's disclosure:

MetLife impact of COVID-19 on mortality (MetLife Q4-2021 supplementary presentation)

{kind=link}

For non-life there is normal variations in claims but also catastrophe risk. In addition there might be claims inflation risk as we have recently seen.

What I want to get at is that neither size nor timing of payouts are certain. Actuaries can do their best estimates but reality will be different and this also makes hedging and matching assets to liabilities complicated.

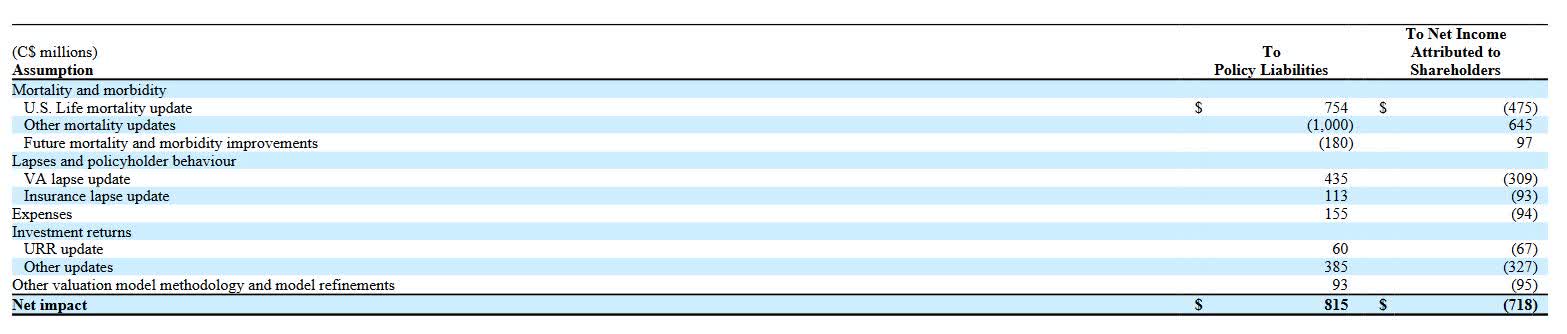

These developments can often be slow but eventually they will catch up. For example Manulife (MFC) completed an actuarial review in 2011 and the had to take a large hit in Q3:

“In the quarter, we completed our annual review of actuarial methods and assumptions, which resulted in a net charge of $651 million"

and

"Year-to-date, the net increase in policy liabilities from valuation method and assumptions reviews is $1,521 million, with an aggregate post-tax impact of $(1,190) million on net income attributed to shareholders. "

Looking deeper into it one can see that there were many partially offsetting changes in their assessment of their liabilities for the quarter:

Manulife assumption changes (Manulife Form 6-K for Q3/2011)

{kind=link}

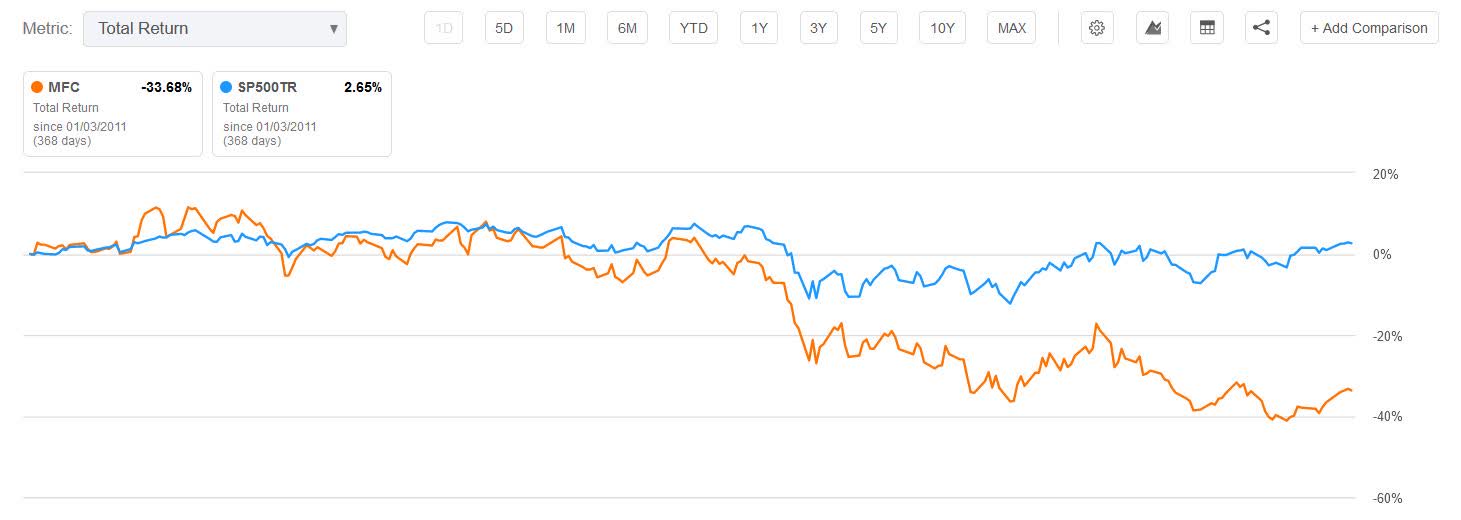

This was not a pleasant time for Manulife stock (it started already in Q2 with their first increases in reserves):

Manulife stock performance 2011 (Seeking Alpha)

{kind=link}

3. Asset Liability Mismatching risk:

We talked about the risks that come from investing in assets and taking on insurance risks on the liability side. Another source of problems can be the so called asset-liability-mismatching. The classic example is a bank run. The bank has short term deposits on the liability side and loans which are long-term illiquid assets on the asset side. If now everyone wants their money from the bank they cannot provide enough liquidity. This is a liquidity based scenario.

Normally insurers are less exposed to this. Their liabilities tend to be longer term, there is only a limited ability to withdraw them depending on the product plus insurance companies tend to be invested in highly liquid assets rather than loans (mind you: part of how private equity companies want to improve profitability at insurance companies is by moving them into less liquid assets with hopefully higher returns). That said, there is still a risk that policyholders cancel their contracts. This is called lapse or surrender risk. This can be partly mitigated by penalties for early lapses or so called market value adjustments to the eventual value that the policyholder gets. It very much depends on the individual contracts. Still, lapse risk is highly relevant in the current environment with strongly rising rates. Especially for fixed annuity contracts which is a typical area many alt managers focus their insurance activities on. As many investments backing those contracts are longer duration bonds they have lost dramatically in value in a rising rate environment since establishing the contracts and the lapse would lead to a realized loss unless there are mitigating factors like above mentioned penalties, market value adjustments or hedges.

This was liquidity side of ALM but there is also an economic risk. Insurance liabilities can be very long term (pensions, worker's liability,... some companies still have reserves for asbestos claims originating from the 60s or 70s). Therefore, if the liability side has a longer duration than the asset side in a low interest environment the value of these liabilities rise more than those of the assets. Also the insurance company has a reinvestment risk if they have, e.g., contracts with high guaranteed rates which was another big problem during the low interest environment. Luckily, for the time being it seems like we move towards a more normalized interest rate environment.

Generally, the best way to manage asset liability risk is through smart contract design, the second best to re-insure those parts of the risk out that you don't like and thirdly, you can also try and hedge those risks which is likely to be an imperfect hedge because as we have seen above the timing and size of liabilities is uncertain and many contracts have embedded optionality that is very hard to impossible to hedge out. Also the better the hedge the more expensive it tends to be. And finally, you can always simply hope for the best (which happens more often than you would think).

Here is Warren Buffett on the discontinuity risk of trying to hedge one's liabilities with derivatives:

If you have a major cyber or nuclear or biological attack on the country—a major discontinuity—you have a lot of problems…When you open back up, you can have large gaps in the positions," said Buffett. He added that such a situation was a "potential time bomb.

This is a new risk category for alternative managers as they had no ALM risk so far. They call upon funds when they need them to invest and then keep them invested as long as they like. Easy. With insurance it is no longer that easy.

4. Regulation in Insurance

It should be clear by now that managing an insurance company is not easy. However, insurance is a very important part of everyone's life. Some insurance policies are even mandatory. Therefore regulatory oversight is much tougher and more strict compared to what private equity firms are used to.

Regulators impose capital requirements like the so called risk based capital requirements and rating agencies work off these to apply their rating. Some regulators also apply other restrictions for example on what assets are eligible for investment etc. Luckily, some jurisdictions like Bermuda are less strict which opens up the possibility of engaging in regulatory arbitrage. But generally speaking, insurance is heavily regulated. All of this is fine and needed but the problem is twofold:

Firstly, a temporary stress situation can be made permanent by regulators requiring action. That could be the disposal of certain assets at poor prices or a highly dilutive equity offering to shore up the capital within the insurance company. This is partly why Hartford's share price never recovered whereas BlackRock as an asset manager just traded through all of this turmoil and eventually came back:

Hartford Financial Services Group Inc. said Friday it has taken $3.4 billion of federal bailout money, the maximum it was authorized to accept, to bolster capital in the wake of large investment losses.

Secondly, even if an insurance company gets through a financial crisis unscathed thanks to superior management or sheer luck they can still suffer because the regulator tends to take actions after such events which are generally detrimental to insurance companies' profitability and flexibility. Manulife stated the following in 2011:

"As we have said before, regulatory risk is the biggest risk to our industry. Our regulator continues to work on many initiatives which could result in increased capital requirements even though our regime is already very conservative. Although we cannot predict the outcome of these deliberations, we remain comfortable with our capital position. "

Therefore the main risk with regulation is not that it is somewhat limiting but that it can make temporary market effects permanent by forcing actions on companies. In addition to that the regulator can also change the rules of the game as it sees fit.

Summary

Investors in alternative asset managers have to understand that getting into insurance is much more than just another pool of permanent capital to manage. Insurance is a whole different ball game than what alternative asset managers are used to. It fundamentally changes the risk profile. Not only do they carry all the investment risk (excluding separate account assets) but they are also exposed to getting the liability side wrong and operate in a highly regulated environment. While there is undoubtedly opportunity to strongly increase AuM there is also the risk of missteps along the way.

However, not all alt managers pursue the same strategy and their exposure differ. It therefore does make sense to look more deeply into the specific strategies chosen rather than lumping them all together as a simple expansion of the existing business. I do intend to look into this in more detail at some time in the future.

If you found this article helpful please give it a like. If you have questions or remarks please comment below. I would love to hear from you. Many thanks!

For further details see:

Alternative Asset Managers Getting Into Insurance: Beware Of The Changing Risk Profile