DIS - AMC Entertainment: The Barbenheimer Effect Is Not Easily Replicated

2023-12-12 10:29:05 ET

Summary

- Investors should not view AMC's excellent FQ3'23 results through rose-colored glasses, since the Barbenheimer effect is unlikely to be replicated by Taylor Swift's Era tour.

- The management also recently signed additional operating lease agreements worth $78.2M, despite its apparent working capital deficit of -$571.1M by the latest quarter.

- AMC is expected to remain unprofitable on an FCF basis over the next few years as well, implying the increased likelihood of dilutive capital raises to pay down its obligations.

- With $3.04B of its long-term debts due by 2026, we believe that things may get worse before it eventually gets better.

- Combined with the elevated short interest of 11.53% at the time of writing, we are not certain if there is any chance of reversal ahead, with market sentiments surrounding AMC likely to remain pessimistic.

We previously covered AMC Entertainment Holdings, Inc. ( AMC ) in September 2023, discussing its risky investment thesis, due to the lack of sustainable profitability and reliance on share dilution to raise liquidity.

Combined with the inherent lack of bullish support, or in this case, APE support, we believe that the stock may remain volatile with minimal chance of recovery ahead, resulting in our re-iterated Hold rating then.

In this article, we will be discussing why investors should not view AMC's excellent FQ3'23 results through rose-colored glasses, since the Barbenheimer effect is unlikely to be replaced by Taylor Swift's Era tour.

Most importantly, with the company likely to dilute existing shareholders by up to +177.2%, we do not recommend anyone to add this overvalued stock here.

The AMC Investment Thesis Remains Flawed, Only Temporarily Boosted By Barbenheimer

For now, AMC has reported an excellent FQ3'23 earnings call , naturally attributed to the massive success enjoyed by Barbenheimer, with revenues of $1.4B ( +4.4% QoQ / +45.2% YoY ) and adj EBITDA of $193.7M (+6.1% QoQ/ +1601% YoY).

This has allowed the company to temporarily boost its balance sheet, with cash/ short-term investments of $729.70M (+67.6% QoQ/ +6.5% YoY) and a stable long-term debt of $4.75B (inline QoQ/ -8.4% YoY).

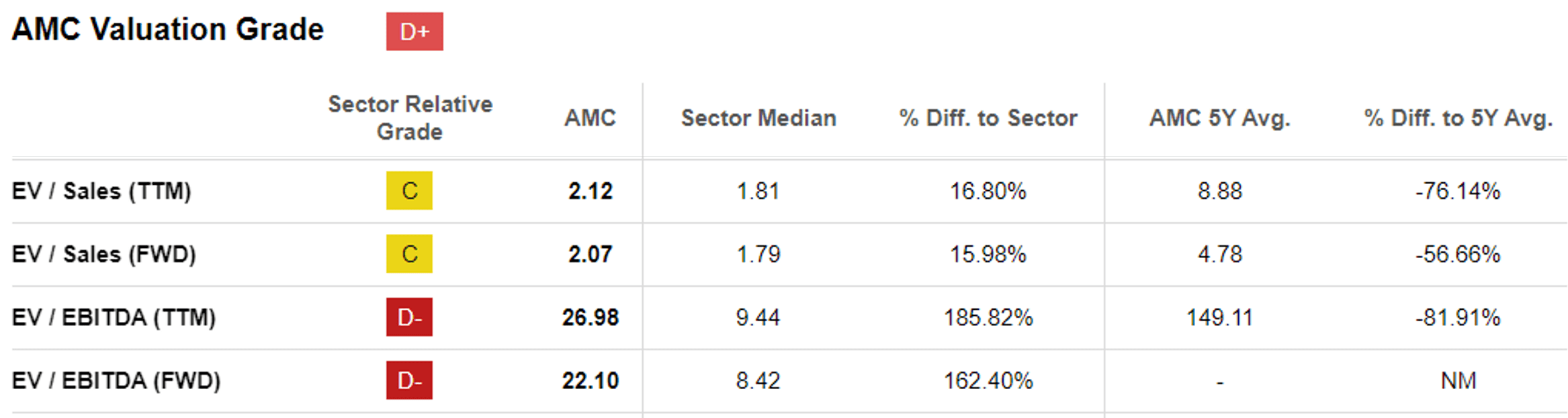

AMC Valuations

{kind=link}

Perhaps this is why the AMC stock currently trades at an eye-watering premium FWD EV/ Sales valuation of 2.07x and FWD EV/ EBITDA valuation of 22.10x, compared to its 3Y pre-pandemic mean of 3.11x/ 18.92x and the sector median of 1.79x/ 8.42x, respectively.

Then again, anyone hoping for similar top/ bottom line numbers over the next few quarters may be sorely disappointed, since we do not expect any of the upcoming pipelines to generate a similar effect as the Barbenheimer.

For example, many production companies have had to delay their theatrical release dates to 2025 instead, including The Walt Disney Company ( DIS ) and Paramount Global ( PARA ), attributed to the four months long SAG-AFTRA/ WGA strikes.

It also remains to be seen how successful Taylor Swift's Eras and Beyonce's Renaissance concert-movie may be, with the former only grossing $220M globally within four weeks. This number is underwhelming indeed, compared to Barbie's domestic feat at $552M / globally at $1.18B and Oppenheimer, domestically at $264M by the fourth week.

While there may be more concert-theatrical release opportunities ahead, we believe that AMC's FQ4'23 performance may disappoint after all, with us concurring with a fellow contributor in Seeking Alpha, in that " Taylor Is No Barbie ."

Despite the robust adj EBITDA expansion, readers must also note that the company only reported a GAAP EPS of $0.08 (+60% QoQ/ +103.9% YoY), partly attributed to the burgeoning share count of 162.61M (+4.23M QoQ/ +52.08M YoY) by the latest quarter.

The other headwind is attributed to AMC's growing annualized interest expenses of $377.2M (+1.3% QoQ/ +9.5% YoY), thanks to the elevated interest rate environment and its variable rate Senior Secured Credit Facility-Term Loan due 2026.

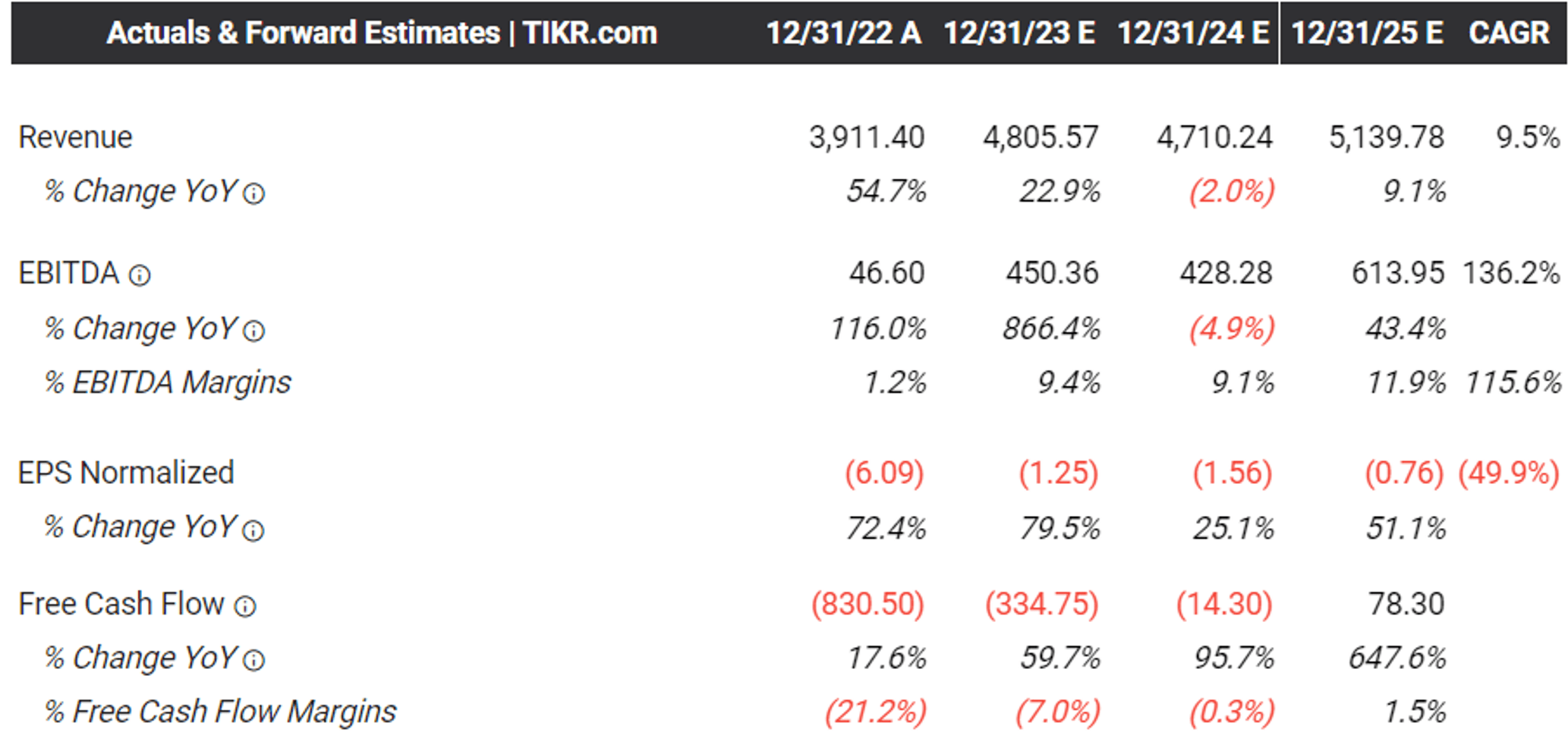

The Consensus Forward Estimates

{kind=link}

The same has been highlighted in the consensus forward estimates, with AMC expected to remain unprofitable on the FCF basis over the next few years, implying the increased likelihood for dilutive capital raises to pay down its obligations.

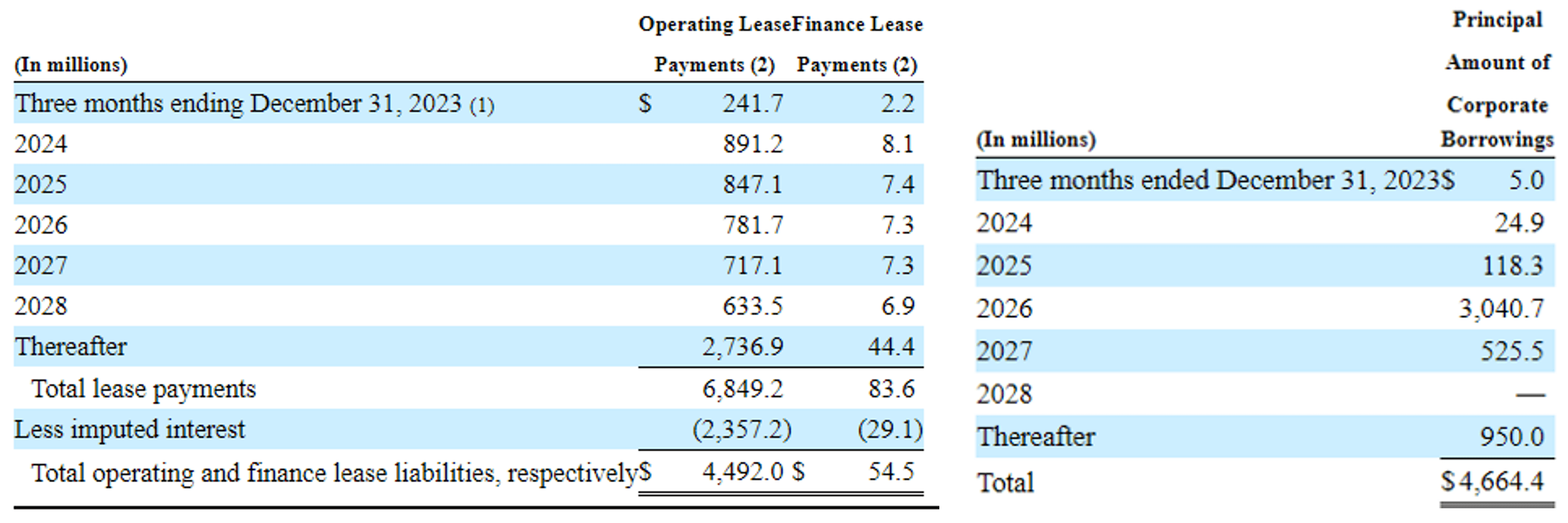

AMC's Lease Obligations/ Long-Term Debt

{kind=link}

As of FQ3'23, AMC reports a manageable annual operating lease obligation of approximately $890M and a debt maturity of $148.2M through FY2025. However, things are set to change after that, with $3.04B of its long-term debts due by 2026, resulting in two potential outcomes.

One, we may see the management continue their share dilution through equity raises as they have for the past few quarters, naturally leading to its increasingly bloated share counts ahead.

For context, AMC has already obtained the regulatory approval to increase its total number of Class A shares to 550M, with a forward balance of 351.65M as of November 7, 2023, implying an eventual dilution of up +177.2% from current levels.

Then again, with the stock already losing -88.4% of its value on a YTD basis, we are not certain how much liquidity may be raised at these depressed levels.

Its prospects are also worsened by the recently signed additional operating lease agreements for five theatres worth approximately $78.2M, with lease terms ranging from 10 to 20 years, and its apparent working capital deficit of -$571.1M by the latest quarter.

As a result of its immense obligations, we believe that the AMC management may also exercise the second option, of which is to refinance the debt at a later date. Interestingly, this may be a prudent choice then, with the inflation already cooling by October 2023 and the Fed unlikely to further hike rates.

Some market analysts are already predicting a pivot as soon as Q1'24, with the Fed expecting a normalized economy by 2026, implying that the company may be able to reduce its interest expenses assuming a lower interest rate then.

However, prior to then, things may get worse before it eventually gets better. This is especially true since AMC is unlikely to replicate its FQ3'23 success in the intermediate term, with market analysts already cutting their 2024/ 2025 box office estimates due to the industries' underwhelming performance on a YTD basis.

So, Is AMC Stock A Buy , Sell, or Hold?

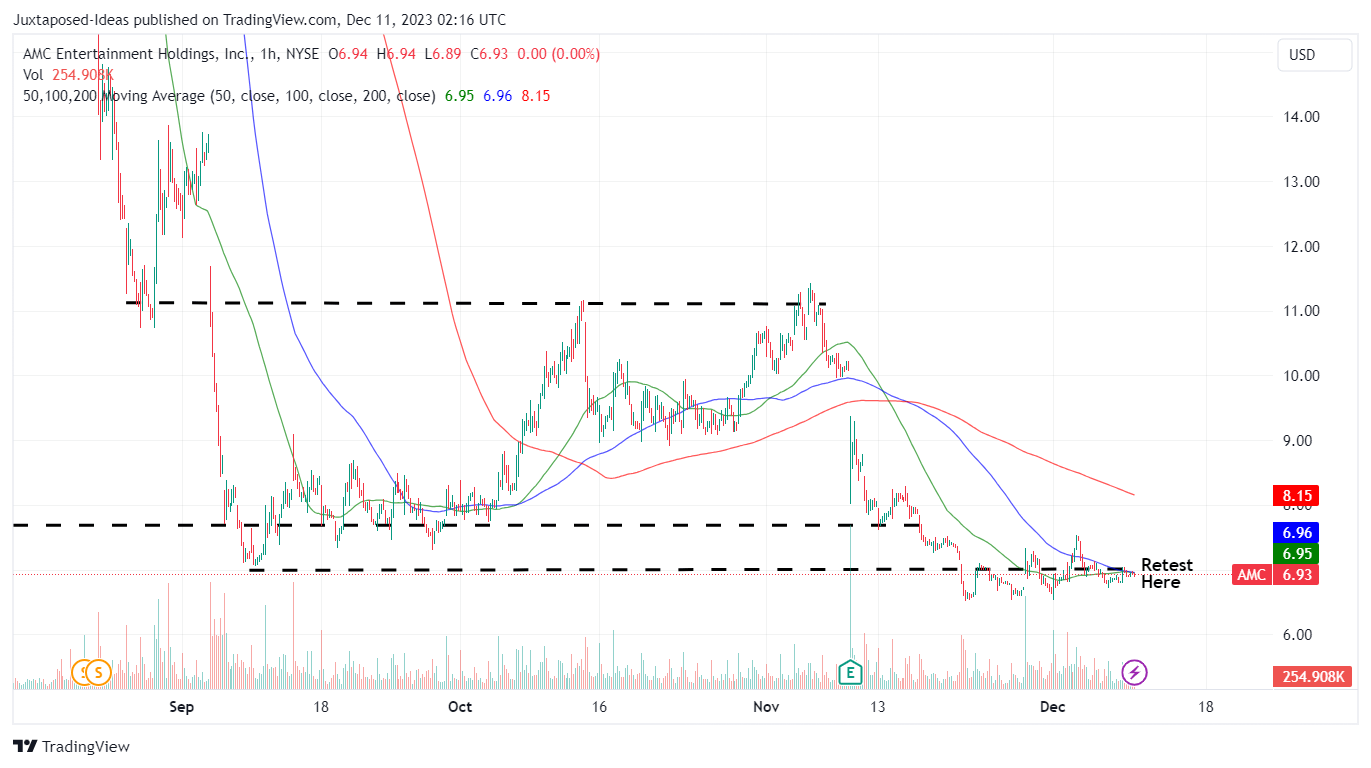

AMC YTD Stock Price

{kind=link}

Combined with AMC's volatile performance over the past few months and the elevated short interest of 11.53% at the time of writing, we are not certain if there is any chance of reversal ahead, with market sentiments surrounding AMC likely to remain pessimistic.

While the management has taken drastic steps to improve its portfolio, with a net reduction of 99 locations since the pandemic, it is apparent that these efforts have been too little and too late, with the company yet to generate a consistent/ meaningful profitability.

As a result of the potential capital losses, we prefer to maintain our Hold (Neutral) rating here.

For further details see:

AMC Entertainment: The Barbenheimer Effect Is Not Easily Replicated