AMZN - AMD Q1 2023 Preview: Xilinx And EPYC In Focus

2023-05-02 09:30:13 ET

Summary

- Despite its tepid guidance for sequential declines across all core business units, with the exception of its embedded segment, Advanced Micro Devices, Inc.'s Q1 2023 results are expected to be headlined by data center results.

- This is consistent with better-than-expected hyperscaler demand (a critical end-market for AMD) observed in tech earnings last week, despite tempered expectations amid a still-weak IT spending environment.

- We also look to the continued ramp-up of new technologies supportive of ongoing AI momentum, and Xilinx integration as key focus areas for offsetting the near-term client segment slump.

Advanced Micro Devices, Inc.'s ( AMD ) semiconductor peers that reported last week unanimously struck a cautious tone about the anticipated second half recovery, considering economic data that continues to point to a worsening consumer end market. This is largely in line with AMD management's cautious optimism for second half improvements during the fourth quarter earnings call earlier this year, which should have tempered some of market's expectations.

We have made good progress in inventory normalization. We want to be cautious, obviously, heading into the year just given the macro environment.

Source: AMD 4Q22 Earnings Call Transcript .

This time around, focus is likely to turn towards evidence supportive of continued progress on that recovery timeline ahead of AMD's first quarter report due this week. This includes a search for resilience in data center sales - particularly given recent momentum in AI - to offset what will likely remain subdued results at its client-facing businesses (i.e., client and gaming). Favorable progress on ramping up new technologies - including the Genoa EPYC Processors - and Xilinx integration would also be key for AMD to satisfy current market expectations on its near-term fundamental performance.

While it is clear that the semiconductor sector has yet to emerge from the cyclical downturn, which remains a near-term risk to AMD stock performance, investor expectations remain fairly low taking into consideration the tepid demand environment. And evidence supportive of continued data center market share gains at AMD, alongside participation in incremental new growth frontiers enabled by generative AI and Xilinx integration, are likely to bolster pent-up value that would translate into further stock upsides upon the eventual return of cyclical tailwinds.

Tepid Consumer End-Market Demand

Record high inventory alongside a macroeconomic slowdown have tempered expectations for the semiconductor sector in recent months. Although the recovery timeline differs depending on the specific end market, with weak PC shipments over the past year likely nearing bottom while data center sales continue to find resilience amid a muted spending environment, we believe AMD management's cautious tone earlier this year about its near-term demand prospects was prudent and sufficiently de-risked for the mixed outlook still.

Recall that management has guided client and gaming segment revenues to decline both sequentially and y/y due to continued demand softness, compounded by seasonality weakness. This is consistent with recent economic and industry data that points to further deterioration in consumer end-markets. On the economic front, consecutive months of declining retail sales , deceleration in both consumer credit and debit card spending amid tumbling household savings, and signs of a loosening labor market that risks ensuing declines in employment and income are likely to weigh further on consumption over the coming months. The bleak near-term economic outlook is further corroborated by the Fed's latest findings in its Beige Book report, which cited " flat to down slightly " consumer spending - a key component that accounts for two-thirds of U.S. GDP growth - adding pressure to AMD's end market demand. Meanwhile, on the industry front, global chip sales reported by the Semiconductor Industry Association have remained weak over the first quarter, despite a m/m uptick observed in March that proves too soon to be conclusive of an early recovery in PC demand after related shipments accelerated their plunge this year.

Global Semiconductor Sales (Semiconductor Industry Association, with author commentary)

{kind=link}

Industry peers have also resorted to a tone of increased uncertainty in recent weeks over the extent of the anticipated rebound in the back half of 2023, which we expect AMD to echo in its guidance in order to mitigate incremental valuation compression risks.

3 months ago, we said we expect fabless semiconductor inventory to start gradually reducing 4Q 2022 and we forecast a sharper reduction throughout the first half of 2023.

However, due to weakening macroeconomic conditions and softening end market demand, fabless semiconductor inventory continued to increase in the fourth quarter and exited 2022 at a much higher level than we expected. In addition, the recovery in end market demand from channels reopening is also lower than our expectation. Therefore, the fabless semiconductor inventory adjustment in first half '23 is taking longer than our prior expectation. It may extend into third quarter this year before rebalancing to a healthier level.

Source: TSMC 1Q23 Earnings Call Transcript .

As expected, our results reflect weaker demand in all end markets with the exception of automotive. As mentioned last quarter, a component of the weaker demand was inventory reductions by our customers, which we expect to continue in the second quarter…The overall outlook is roughly flat into second quarter.

Source: Texas Instruments 1Q23 Earnings Call Transcript .

We continue to see mixed signals on demand from the different end-market segments as the industry works to bring inventory to more healthy levels.

Source: ASML 1Q23 Earnings Press Release .

The mixed outlook is further corroborated by industry stockpiles and inventory levels that remain elevated. While AMD has been "[shipping] below PC consumption" for several quarters (including the first quarter based on its guidance earlier this year) now to alleviate downstream inventory build, uncertainties remain over the broader supply chain's digestion of excess stockpiles and the extent of anticipated normalization in near-term demand.

We do believe the first quarter is the bottom for our PC market - for our PC business, and we'll see some growth in the second quarter and then a seasonally higher second half. In terms of the under shipment, I mean, I think we're - we under shipped in Q3, we under shipped in Q4. We will under ship, to a lesser extent, in Q1. So I think you can infer that from our guidance single-digit down…Now just as a reminder though, the first half is not usually a - the first half is usually a seasonally weak client time anyways. So, we would expect more lift in the second half, not so much in the second quarter.

Source: AMD 4Q22 Earnings Call Transcript .

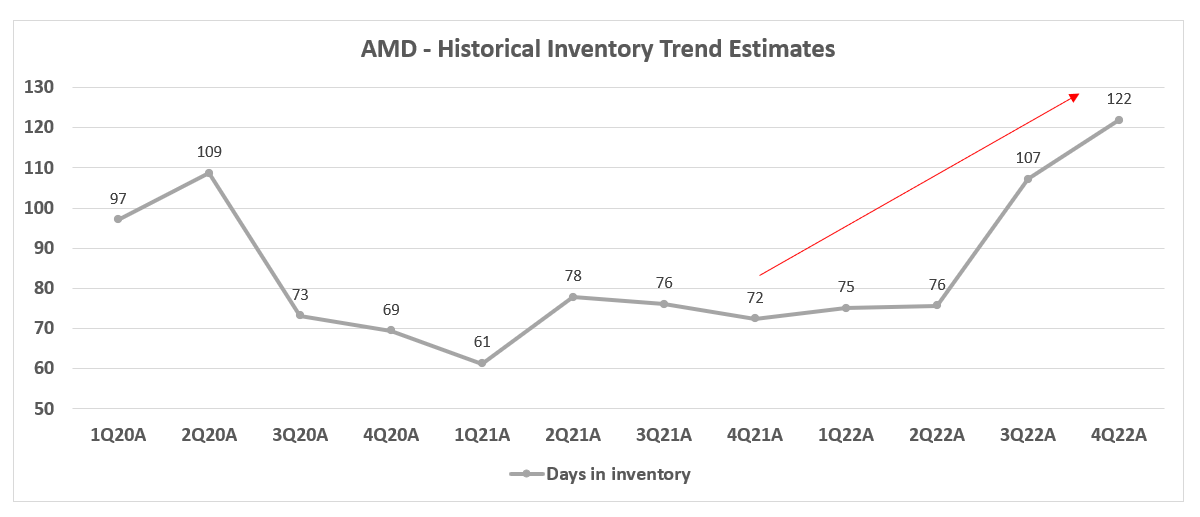

And gradually building days of inventory will likely persist over the foreseeable future as uncertainties over the timing of stockpile digestion across the supply chain remain. Admittedly, some of AMD's inventory build in recent quarters are likely associated with "[increases] in advanced process nodes to support the ramp of new products." But the ballooning figure risks weighing further on the company's near-term fundamentals, nonetheless, especially considering its strong PC product portfolio this year (e.g., Ryzen Z1 Series , Ryzen 7000 Series , Radeon PRO W7000 Series ) that will be shipping into a persistent cyclical downturn that has been particularly acute in consumer-facing end markets.

AMD Historical Inventory Trends (AMD Historical Financials) Days in inventory are steeply increasing in recent quarters. (AMD Historical Financials)

{kind=link}

{kind=link}

Enterprise Resilience

However, AMD's strategic focus on prioritizing "commercial as well as the high-end consumer segments" is expected to offset some of the impact from persistent near-term PC total addressable market, or TAM, contraction. Although the IT spending environment remains cautious amid mounting macroeconomic uncertainties, it will likely remain resilient relative to retail consumer end markets. This is consistent with AMD's PC market share gains reported for the fourth quarter despite the tough demand environment. And continued market share gains across the premium segment in the first half of the year will be helpful in mitigating the company's exposure to consumer end-market weakness.

Actually, in the fourth quarter, we believe we gained a little bit of share in the PC market. As we go forward into 2023, we think our product portfolio is very strong. As we look at Ryzen 7000 and where it goes and where we are positioned in the commercial as well as the high-end consumer segments, we're not changing our strategy on PCs…We have less penetration in the low end, which I think is helpful. And as we go forward, we're continuing to focus on commercial PCs and getting a larger footprint in there.

Source: AMD 4Q22 Earnings Call Transcript.

Considering client and gaming segment results are likely to stay muted on a net basis, with anticipated enterprise resilience to partially offset a weakening consumer end market amid persistent macroeconomic deterioration, data center strength in line with better-than-expected hyperscaler demand observed in last week's big tech earnings will be key for AMD to keep up with market expectations and maintain investors' confidence. Specifically the cloud spending segment has proven more durable than expected, with the big three hyperscalers - AWS of Amazon.com, Inc. ( AMZN ), Azure of Microsoft Corporation ( MSFT ), and GCP of Google ( GOOG / GOOGL ) - "showing more resiliency" despite previously bleak expectations for unprecedented deceleration to imply a structural slowdown in enterprise cloud migration. Although management has reasonably guided for sequential declines in first quarter data center sales that would be "more than seasonal" in the double-digit range, recent industry results and market observations indicate an actual demand environment that has performed better than expected.

Meanwhile, cloud infrastructure, software, and services are growing more slowly than a year ago but continue to account for a larger share of total IT spending and are reinforcing the general sense of resilience which the industry still enjoys.

Source: IDC's Forecast for Worldwide IT Spending in 2023 Continues to Slowly Trend Downward .

Although the recent buzz over generative AI is unlikely to drive immediate incremental impact on AMD's P&L, it does underpin a promising new growth frontier in which the company plays a critical role in and will benefit from over the longer-term. Specifically, generative AI is expected to expand the cloud TAM given incremental demand for high-performance computing capacity, which will inadvertently bolster the need for supporting hardware including AMD's server processors.

This is consistent with significant incremental investments allocated by hyperscalers in recent months towards the continued development of generative AI technologies and solutions. Market currently expects the market for AI-specific processors to blossom into a $38 billion market by 2026, representing a fourfold increase from 2022 levels or a four-year CAGR of 24%. To put into perspective, the infrastructure for Microsoft's integration of ChatGPT into Bing alone has already cost $4 billion , with an additional hundreds of millions of dollars allocated towards the development of architecture needed to optimize the performance of existing processor technologies in the market to facilitate next-generation AI capabilities. And over the longer-term, capex spend by big tech allocated towards AI developments are expected to accelerate , underscoring significant tailwinds for AMD amid a multi-year rush across the industry to ensure adequate participation in the new growth frontier.

Considering the budding momentum, evidence of continued progress in generative AI developments will be a key focus area ahead of AMD's upcoming earnings call to maintain confidence over its competitive positioning in capturing related opportunities. This includes management's confirmation that the Bergamo EPYC Processors optimized for cloud-computing will ship on schedule in 2H23, as well as continued ramp up of Genoa EPYC processor shipments to ensure adequate market share capture. The Instinct MI300 accelerators based on the next-generation CDNA 3 architecture curated for facilitating "large model AI applications in cloud data centers," which will begin shipping in the second half of the year, are also expected to help preserve its momentum in generative AI. Dubbed the "world's first data center integrated CPU + GPU", which combines CPU, GPU and memory into a "single integrated design," the MI300 accelerations will be fitted into " El Capitan " - an exascale supercomputer currently under development with delivery expected this year - which provides further validation for AMD's mission critical role in next-generation HPC opportunities.

Xilinx Ramp Up

The continued progress on integrating Xilinx a little more than a year after the acquisition closed is also likely to be a key focus area at AMD's upcoming earnings call. Considering the uncertain demand environment, Xilinx offers AMD exposure to a "diversified set" of end markets to mitigate some of the cyclical weakness that has been most prominent in consumer verticals.

The synergies are corroborated by record demand in AMD's embedded segment during the fourth quarter, and expectations for further growth through 2023. The segment's robust demand is supported by AMD's foray in communications enabled by Xilinx, which currently represents a mission critical vertical in supporting connectivity services, such as "expanded 5G wireless installations," a relatively recession resistant end market. Xilinx's expansive 5G installed base also complements the deployment of AMD's Ciena EPYC Processors later this year, which is curated for optimized telco application. Xilinx also bolsters AMD's exposure to opportunities stemming from the automotive end market, which has been resilient despite macroeconomic challenges as supply chain constraints start to ease and OEMs catch up on addressing previously pent-up demand as mentioned in the earlier section.

More importantly, progress in AMD's continued integration of "Xilinx's performance leading AI engine" ("AIE") is expected to reinforce its competitive positioning in the generative AI growth frontier, representing a tailwind for the stock when transient macroeconomic challenges to market sentiment subside. Evidence supportive of this would include progress in ramping up Ryzen 7000 Series processor shipments. As mentioned in our previous coverage , Xilinx's proprietary AIE technology, which is built on its programmable Versal ACAP architecture, is key to AMD's next-generation XDNA Architecture on which the Ryzen 7000 Series processors are based off of. Specifically, the Ryzen 7040 CPU series will be the first to feature "Ryzen AI" - a built-in "AI inference engine" within the CPU to unlock optimized performance efficiency in any application, underscoring AMD's competitiveness enabled by continued integration of Xilinx technologies.

The Bottom Line

Much of the momentum observed in the AMD stock rally this year has been a result of external factors outside of fundamental considerations, given it is clear that the broader semiconductor sector is still reeling from a cyclical downturn with an uncertain recovery timeframe. Instead, the stock's recent upsurge has been primarily driven by a broad-based market rotation into tech havens amid turmoil in the financial sector that has been refreshed by First Republic Bank's ( FRC ) failure last week, and expectations that the current monetary policy tightening cycle is nearing an end, which would benefit growth valuations underpinned by future cash flow prospects.

This essentially leaves the recent rally fragile still, given persistent multiple compression risks driven by the looming macroeconomic overhang on AMD's near-term fundamental performance. The company is expected to see its earnings crater by more than 50% in the first quarter to $0.56 per share, with its first quarterly revenue decline in 3.5 years by almost 10% to $5.3 billion. Despite industry's optimism for signs of demand recovery in the second half, AMD is expected to finish the year with a full year earnings decline of 14% at $3.01 per share, and flat sales at about $23.6 billion, in line with tepid fundamental performance estimates across the broader tech sector this year.

However, the risk/reward on AMD remains attractive, given the underlying business' longer-term market share gain prospects, as well as its mission critical role in enabling next-generation technologies. This will continue to create pent-up value in the stock in our opinion, which will get little credit until cyclical market tailwinds return. While we do not believe AMD's cyclical weakness has bottomed out yet, expectations for relative resilience compared to its previously tempered guidance (particularly in data center segment sales), as well as positive progress on ramping up new technologies (particularly, the Gen 4 EPYC server processors and Xilinx integration) will be critical to reinforcing its competitive positioning in capitalizing on new growth frontiers like generative AI opportunities.

We continue to view anticipated fragility in Advanced Micro Devices, Inc. stock's recent rally as an opportune time to build positions given prospects for an eventually structural reacceleration when cyclical tailwinds return.

For further details see:

AMD Q1 2023 Preview: Xilinx And EPYC In Focus