UNH - Amedisys: Even Without A Bidding War The Company Appears Undervalued

2023-06-09 01:03:25 ET

Summary

- Amedisys is a leading healthcare services company dedicated to providing clinically excellent care and support at home.

- Currently reporting FCF generation and proposing workforce optimization, clinical optimization, and reorganization initiatives to differentiate service offerings, Amedisys appears quite an attractive stock.

- If the Board recommends the offer from Option Care Health, we may see an increase in the stock price.

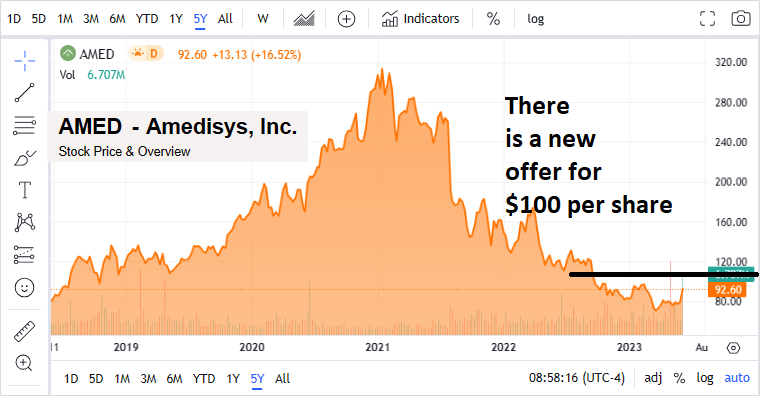

Amedisys, Inc. ( AMED ) recently received a bid for $100 per share in cash, and the company had previously signed a merger agreement with another player. I also saw that management proposed workforce optimization, reorganization initiatives to differentiate service offerings, and certain activities to obtain cash in hand. Already generating a significant amount of free cash flow, AMED stock could be worth more than $103 per share and a maximum of $150 per share. I would consider keeping my shares even if the company does not get acquired.

Amedisys

Amedisys is a leading healthcare services company dedicated to providing clinically excellent care and support at home.

Through its four operating divisions, the company offers a broad range of services, including home health care, hospice care, personal care, and high-acuity care. Amedisys reports more than 20,000 employees in 532 service centers in 37 states of the United States and the District of Columbia.

The company focuses on providing clinically distinct care that is tailored to the individual needs of patients, whether it be for recovery and rehabilitation at home or for chronic disease management. In addition to its focus on Medicare, Amedisys works collaboratively with other payers to structure innovative contracts that reward the delivery of quality care.

Amedisys: Offers From Optum, And An Agreement Signed With Option Care Health ( OPCH )

Very recently, the Board of Directors of Amedisys received an unsolicited offer of $100 per share in cash for the company from Optum, a unit of UnitedHealth (UNH). I believe that shareholders of Amedisys will likely appreciate having a look at the words of the Board. In my view, the proposal is superior to the stock agreement signed with Option Care Health.

Following this evaluation, our Board determined that the unsolicited proposal received from Optum could reasonably be expected to result in an “Amedisys Superior Proposal” as defined in our merger agreement with Option Care Health. We are now engaging in discussions with Optum with respect to their proposal, as permitted by our merger agreement with Option Care Health. There are no assurances that the discussions with Optum will result in a transaction.

Our merger agreement with Option Care Health remains in place while we engage in these discussions. Our Board’s recommendation for the Option Care Health agreement and the Option Care Health merger continues to be in effect. Source: 8-K

The shares are currently trading at less than $100 per share because the market is expecting some kind of response from the Board of Directors. As soon as they accept or recommend the deal, I believe that the stock price could trend higher.

{kind=link}

In another likely case scenario, Option Care Health may decide to increase its merger contribution for Amedisys. In any case, shareholders would most likely see the shares of AMED trading at a higher valuation than what the market reports right now. We are talking about a company that traded, in the past, at more than $281 per share.

Balance Sheet

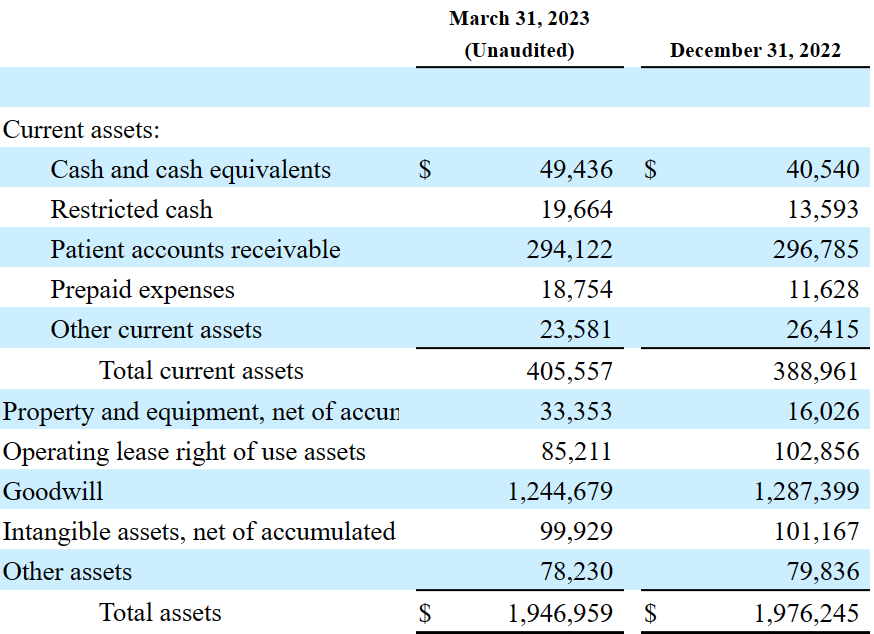

The company reports cash and cash equivalents worth $49 million, restricted cash close to $19 million, and patient accounts receivable close to $294 million. Also, with prepaid expenses of about $18 million, total current assets stand at $405 million.

Non-current liabilities reported included property and equipment of $33 million, operating lease rights of use assets worth $85 million, and goodwill of $1.244 billion. Besides, with intangible assets of $99 million, total assets stood at $1.946 billion. The fact that Amedisys reports a considerable amount of goodwill means that Amedisys knows well what acquisitions are about. Considering the expertise in the M&A markets, I believe that people inside the organization would accept any new corporate transaction.

{kind=link}

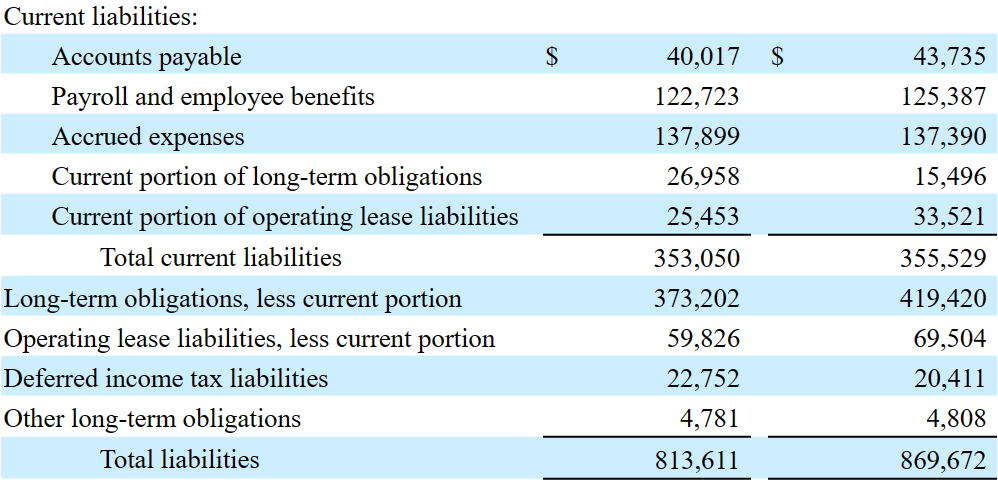

The list of liabilities includes accounts payable worth $40 million, payroll and employee benefits close to $122 million, and accrued expenses of about $137 million. Also, with the current portion of long-term obligations worth $26 million and the current portion of operating lease liabilities of $25 million, total current liabilities are equal to $353 million. The ratio of total current assets/current liabilities is larger than one, so I believe that there is not a liquidity issue here.

Long term obligations stood at $373 million, with operating lease liabilities of $59 million and total liabilities close to $813 million. Considering the FCF expected by investors out there, I am really not concerned about the total debt obligations reported by Amedisys.

{kind=link}

Amedisys' contractual obligations primarily include information technology contracts and software licenses. I believe that future FCF generation would be sufficient to repay its obligations .

{kind=link}

There Are Many Competitors

The company operates in a highly competitive industry. There are few barriers to entry in jurisdictions that do not require specific regulatory approval. Amedisys' primary competitors include privately and publicly owned local health care providers as well as hospitals. Competition is based on the quality of the services offered, the availability and experience of the visiting staff, and, in some cases, the price. In addition, there are competing non-profit organizations that may access tax-exempt funding or receive charitable contributions that are not available to this business.

Considering the size of Amedisys and the fact that there are many peers all over the country and internationally, we may see more competitors launching bids for the company.

My Valuation Model Resulted In Close To $103-$150 Per Share With An Exit Multiple EV/FCF of 18x and 30x

Amedisys' strategy is to become the best care option for patients in their home environment. Under my financial model, I assumed that the company would successfully differentiate itself through the provision of quality clinical care, being an employer of choice, and achieving operational excellence and efficiency. I believe that Amedisys was successful in the past. I do not know why the company would not do the same in the future.

I also expect that existing partnership agreements with BrightStar Care and other new agencies will most likely bring significant FCF growth.

We have a Care Coordination Agreement with BrightStar Care to add its agencies to the Amedisys personal care network, which helps facilitate the coordination of care between our home health and hospice care centers and a network of personal care partners. We believe this agreement will further our efforts to provide patients with a true care continuum in the home. Source: 10-K

I also believe that in case of not selling the company to the two buyers interested, Amedisys would most likely be able to sell certain assets. As a result, with new cash in hand, more investors would have a look at the company. The stock price would most likely trend north. In this regard, I would invite readers to have a look at the intention of the company to sell its personal care business.

On February 10, 2023, we signed a definitive agreement to sell our personal care business (excluding the Florida operations). The divestment is expected to close during the second quarter of 2023. Source: 10-K

With the previous initiatives, I would expect significant FCF growth thanks to workforce optimization efforts, further recruitment, and innovations delivered from the acquisition of Contessa in 2021. In sum, I believe that even if the company is not acquired, shareholders may enjoy attractive initiatives from management.

In the coming year, our core business innovations will consist of workforce optimization with a focus on new ways to engage, recruit and retain our clinical staff, clinical optimization and reorganization initiatives and continuing to differentiate our service offerings as we build out our aging-in-place capabilities. The acquisition of Contessa in 2021 will also be a platform for continued innovations as we expand Contessa’s lines of business, including palliative care at home. Source: 10-K

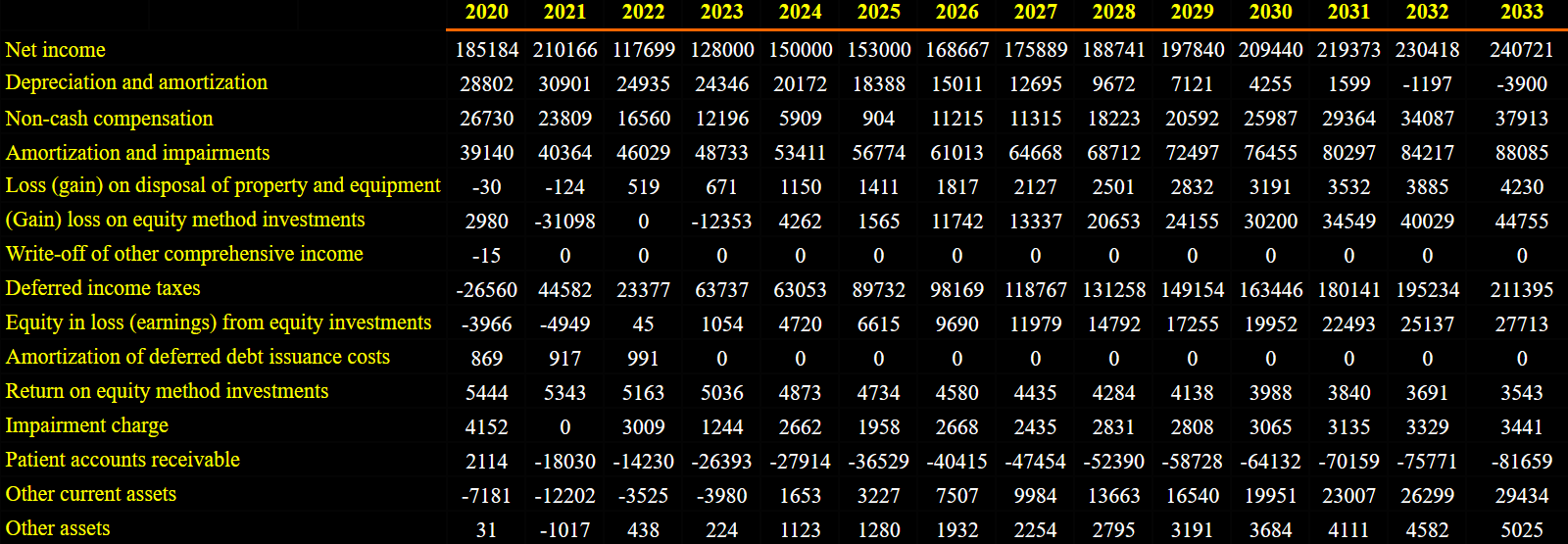

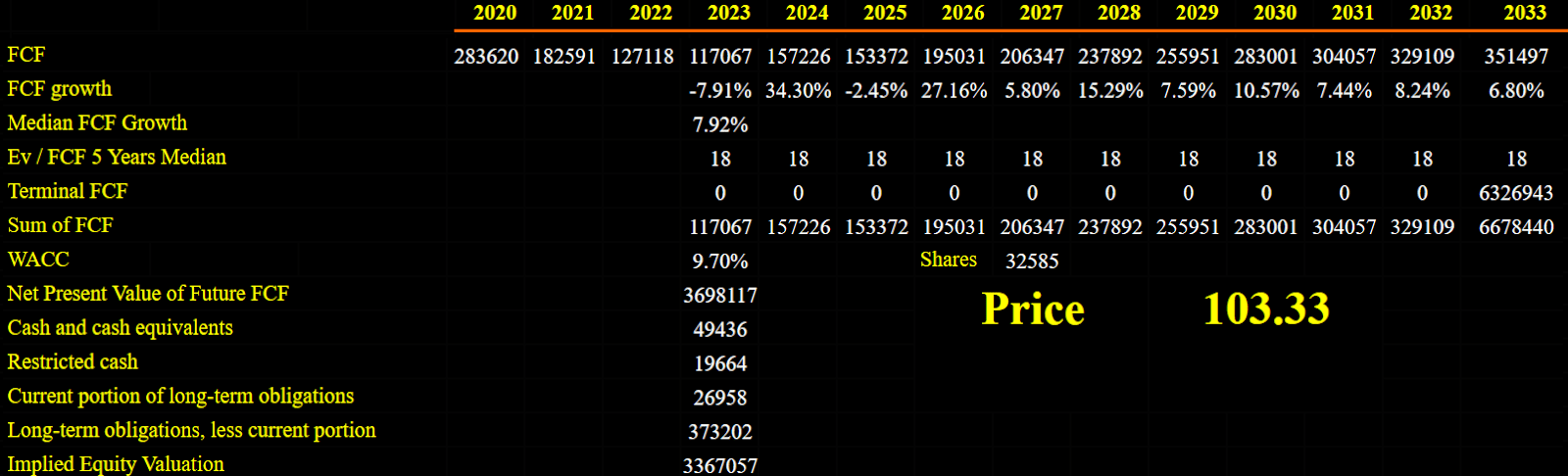

My financial model includes a future cash flow statement from 2023 to 2033. The numbers for 2027 would include net income of $175 million, 2027 depreciation and amortization close to $12 million, non-cash compensation around $11 million, and amortization and impairments of about $64 million.

I also assumed changes in patient accounts receivable of about -$48 million, changes in accounts payable of close to $17 million, and changes in accrued expenses of -$221 million. If we also include other long-term obligations close to $95 million, net cash provided by operating activities of close to $214 million, and 2027 purchases of property and equipment of -$8 million, 2027 FCF would be $206 million.

I also included net income growth from 2023 to 2033 along with FCF growth of around 7%. My numbers would imply 2033 net income close to $240 million, 2033 depreciation and amortization of -$4 million, changes in patient accounts receivable of -$82 million, and changes in accounts payable close to $35 million.

Besides, with long-term obligations of about $220 million and changes due to operating lease liabilities of -$80 million, 2033 CFO would be $361 million, purchases of property and equipment would be -$10 million, and 2033 FCF would be $351 million.

Source: Work From The Author Source: Work From The Author

{kind=link}

{kind=link}

With the previous figures, I made two case scenarios. Under my most bearish cash scenario, I used an EV/FCF 5 Years Median close to 18x and a WACC of 7.9%. Adding the restricted cash and cash and cash equivalent, and subtracting long-term obligations, the implied price would be $103 per share.

{kind=link}

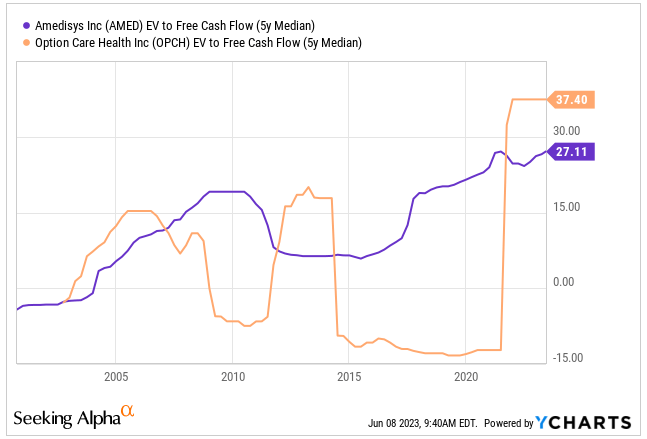

OPCH and AMED report an EV/FCF 5 Years median of close to 27x-37x, so I believe that my terminal multiple of 18x appears quite conservative.

{kind=link}

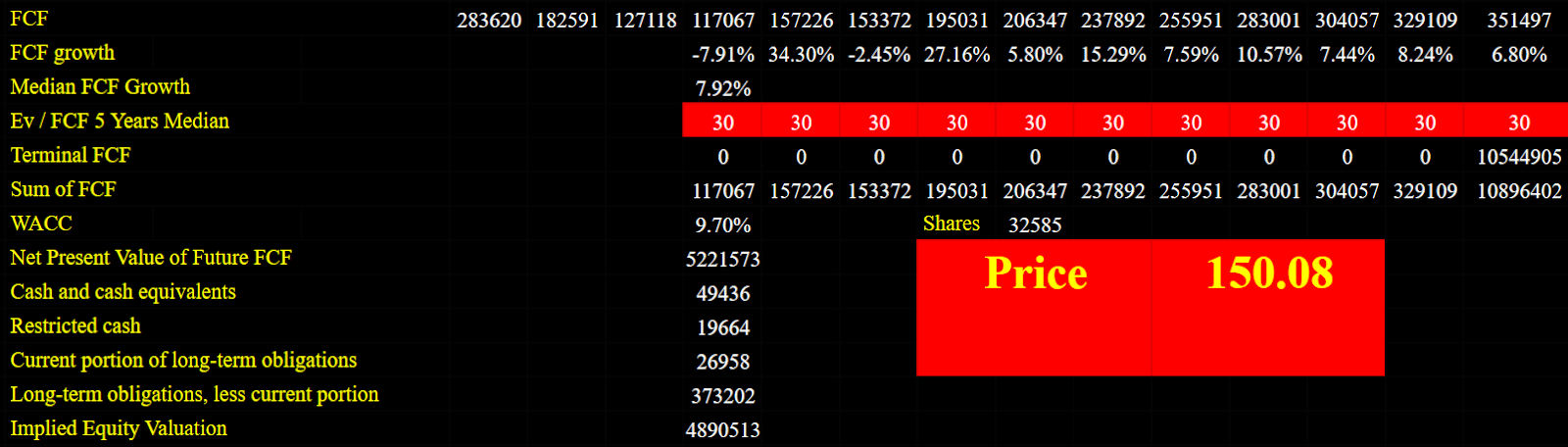

With the same FCF figures reported in the previous case scenario and a terminal EV/FCF of 30x, I obtained an implied valuation close to $150 per share. Note that the company traded at more than $280 per share in the past; however, I do not believe that a buyer would pay that amount of money for Amedisys.

{kind=link}

Risks

In my opinion, the company faces significant risks in terms of the efficient integration of the acquired contact centers and regulatory compliance. The lack of a successful integration could negatively affect the quality of services and operational efficiency, generating internal conflicts and loss of key employees.

In addition, non-compliance with regulations in government programs, such as Medicare and Medicaid, can result in refunds, fines, and penalties that would affect the company financially, and damage its reputation in the marketplace. It is critical that the business implement robust strategies to address these risks and ensure effective integration and proper regulatory compliance.

I do not think that shareholders would lose a lot of money under normal circumstances. If the Board of Directors decides not to recommend the bid for $100 per share, I believe that Amedisys may not see a significant decline in its stock price. Keep in mind that we have another merger agreement in place.

In any case, failed M&A could harm the business model and recognition of Amedisys. If investors decide to sell their stakes because buyers decide to withdraw their bids, I believe that the stock price could trade lower.

My Opinion

Currently reporting FCF generation and proposing workforce optimization, clinical optimization, and reorganization initiatives to differentiate service offerings, Amedisys appears quite an attractive stock. If the Board recommends the offer from Option Care Health, we may see an increase in the stock price, close to $100 per share. In any case, we have the previous merger agreement in place, so I would not expect the stock to decrease a lot, even taking into account that it is a stock for stock agreement. In any case, I believe that Amedisys could be worth around $103 and $150 per share, so I would keep the shares even if the company does not get acquired.

For further details see:

Amedisys: Even Without A Bidding War, The Company Appears Undervalued