GM - American Axle & Manufacturing: Historical Challenges Likely To Continue

2023-10-26 11:24:25 ET

Summary

- American Axle & Manufacturing has significantly underperformed the S&P 500 historically.

- AXL shares have struggled due to a highly competitive industry and high customer concentration, which has made it difficult to generate strong financial results.

- AXL carries a relatively high level of debt for a highly cyclical company, and any significant recession will make it hard for AXL to refinance its debt.

- AXL trades at a below market valuation, but I do not view it as attractive given the challenges the company faces.

- I am initiating AXL with a sell rating.

American Axle & Manufacturing (AXL) has been a disappointing investment for long-term holders. Since its IPO in 1999, AXL shares have posted a total return of -51% compared to the 414% total return posted by the S&P 500.

In addition to underperforming the S&P 500, AXL has significantly underperformed General Motors ( GM ), Ford ( F ), and other auto parts suppliers such as Magna International ( MGA ), Standard Motor Products ( SMP ), and Stoneridge, Inc. ( SRI )

AXL shares have struggled recently due to the UAW strike. AXL is highly dependent on General Motors in particular which accounts for ~40% of sales.

In my view, despite a dismal history of performance, AXL does not currently trade at a low enough valuation to warrant an investment at current levels.

Company Overview

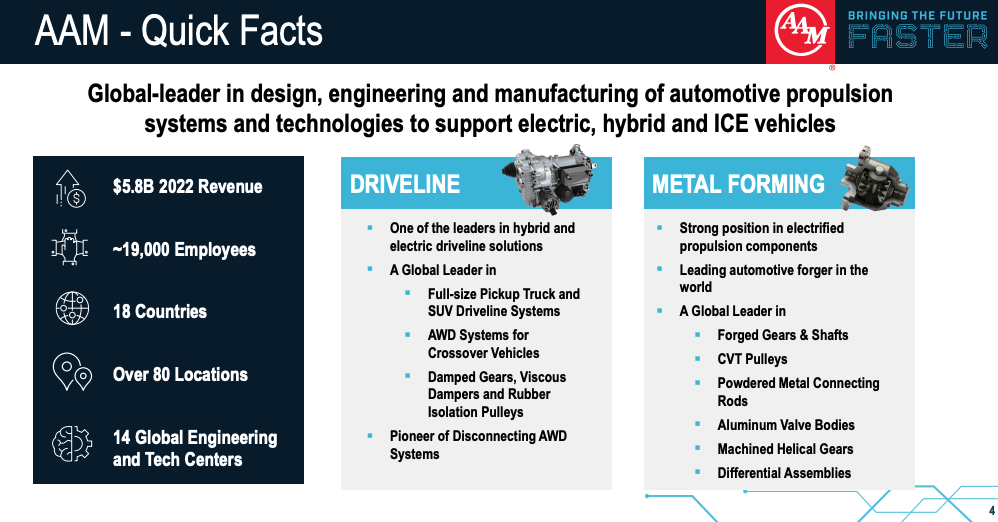

AXL is a global leader in the design, engineering, and manufacturing of automotive propulsion systems and technologies to support electric, hybrid and internal combustion engine ("ICE") vehicles. AXL has ~ 19,000 employees and operates in 18 countries.

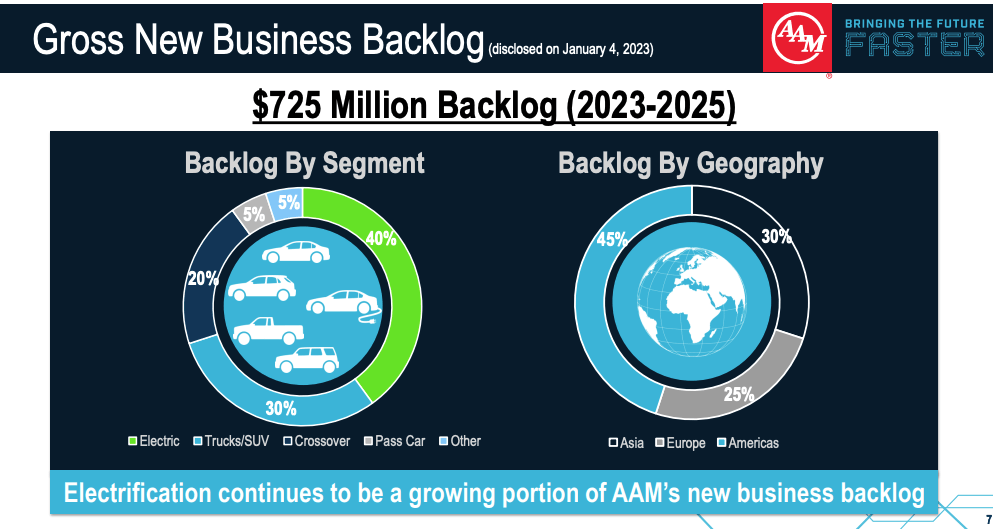

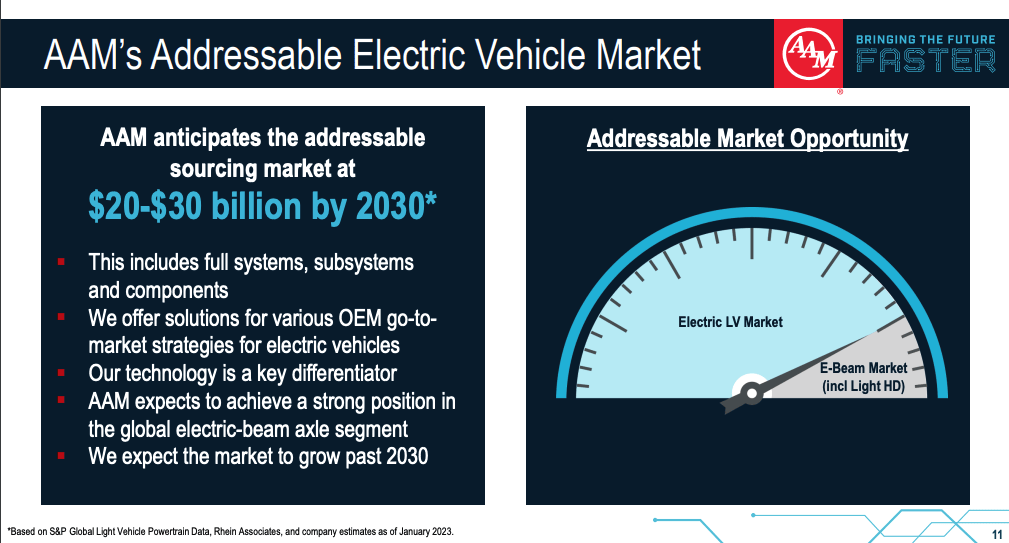

Electric vehicles represent a major part of AXL's business and currently account for 40% of the company's backlog. AXL estimates the addressable EV market at $20- $30 billion by 2030.

GM is AXL's largest customer and accounts for ~40% of sales. Stellantis N.V. ( STLA ) and Ford are also large customers accounting for ~18% and ~12% of sales respectively. Thus the big three represent ~70% of AXL's total sales and no other single customer represents more than 10% of sales.

AXL has been focused on trying to further diversify its business and has recently brought on new customers including Mercedes-AMG ( OTCPK:MBGAF ), Chery Automobile Co. Ltd, and NIO Inc ( NIO ).

AXL Investor Presentation AXL Investor Presentation AXL Investor Presentation

{kind=link}

{kind=link}

{kind=link}

Low Margin and Highly Cyclical Business

AXL competes with independent suppliers and distributors in addition to the in-house operations of some vertically integrated OEMs. For this reason, AXL's business has been characterized by very low profit margins.

As shown by the chart below, AXL historically has posted a negative average net profit margin and an average return on invested capital of just 2.6%.

AXL's historical average beta of 1.8x also serves as evidence of the highly cyclical nature of AXL's business

High Percentage of Union Labor

~69% of AXL employees are represented under collective bargaining agreements with various labor unions. The high % of union labor is a long-term negative for AXL as it limits the ability of the company to generate excess profits as labor will want their share of the pie. This is especially true in the current environment where unions are seeking to assert themselves.

Inflationary Headwinds

Inflation has proved itself to be an important headwind for AXL in terms of margin compression and something that I do not expect to improve over the near term. On the Q2 earnings call the company said:

Net inflation was a headwind of approximately $14 million. AAM's inflationary cost recovery discussions remain ongoing with our OEM customers and we expect resolution should be achieved in the second half of the year with most of our customers.

From a cost perspective, we've seen some favorability from our macro conditions on things like utilities and freight, but we still face pressures from an inflation standpoint on labor as well as from our supply base, who are also experiencing these type of inflationary cost pressures that they're looking to pass up through the chain, those continue.

Inflationary cost pressures are particularly challenging for AXL to navigate due to a lack of pricing power. Comparably, companies that have differentiated products such as Procter & Gamble ( PG ) have been able to pass on price increases to customers.

EV Targets Lowered by Automakers

As noted above, EV represents a growing part of AXL's business and accounts for 40% of AXL's backlog. GM recently announced it was slowing the launch of several EV models and pulling back on some EV product spending. GM announced that it is abandoning its previous goal to build 400,000 EVs from 2022 through mid-2024.

The EV ambitions of GM, F, and Stellantis ( STLA ) have proved a sticking point in UAW negotiations. The UAW is calling for a "just transition" from gas-powered vehicles to EVs as part of any contract. The automakers have counted saying it would be difficult for them to compete with Tesla ( TSLA ) due to higher labor resulting from further unionization.

Given AXL's dependence on GM, F, and STLA which account for 70% of sales, AXL is highly exposed to the outcome of the UAW negotiations. In particular, any results that hurt the ability of the big three players to compete in the EV space over the long term would be a major negative for AXL.

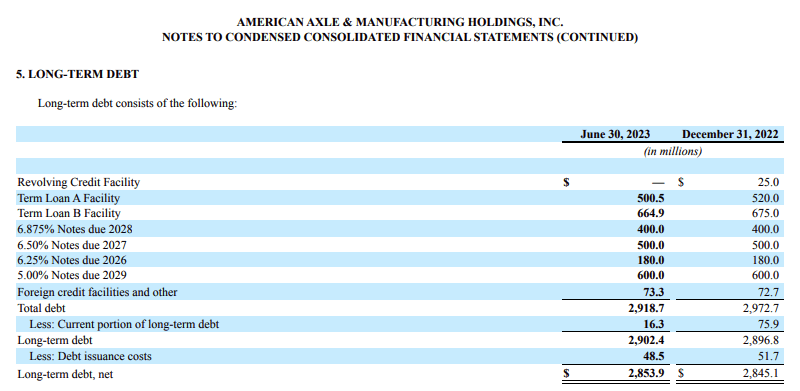

High Levels of Leverage

As shown by the table below, AXL currently has a trailing net leverage ratio of 3.3x and a trailing gross leverage ratio of 3.9x. While I would not consider these ratios to be highly elevated for most companies, I do consider it much too high for AXL given the high degree of cyclicality.

AXL's 5% Notes due 2029 are currently trading at less than 80 cents on the dollar and yield just over 10%. Given the relatively flat structure of the yield curve, I believe that the 10% number serves as a good estimate regarding the rate AXL might be forced to pay to refinance existing debt at maturity.

Currently, AXL has $ 1.68 billion of fixed-rate notes maturing between 2026 and 2029. The annual interest expense related to this debt is ~$101 million each year. If the rate on each tranche were to increase to 10% upon refinancing, interest expense related to these notes would increase by ~$67 million to $168 million.

For context, AXL reported net income of just $64.3 million for FY 2022 and $5.9 million for FY 2021 so even a $67 million increase in interest expense would be meaningful to shareholder value.

While the potential increase in interest expense due to rising rates is a negative for AXL, my real concern is that AXL would struggle to refinance its existing debt stack in the event of even a moderate recession.

AXL Investor Presentation AXL Q2 2023 10-Q

{kind=link}

Relative Valuation

AXL currently receives a Seeking Alpha quant valuation score of A-. I disagree with this rating and do not believe AXL is trading at an attractive valuation relative to the quality of the business and growth potential.

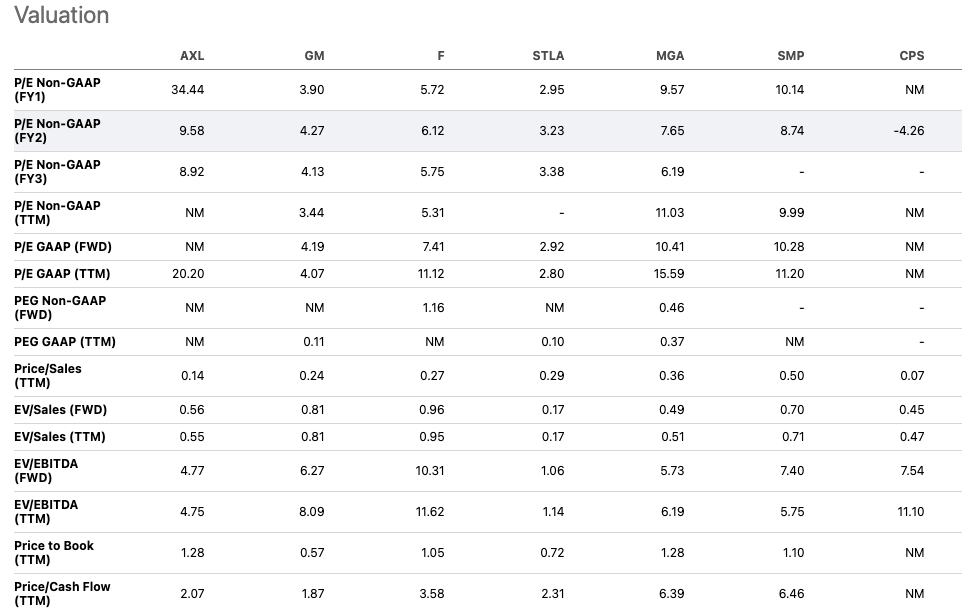

AXL is currently trading at a forward P/E ratio of 9.5x. Comparably, the S&P 500 trades at a forward P/E ratio of 17.4x. However, when adjusting for growth potential AXL looks much less attractive. AXL does not have a strong history of growing earnings and has actually experienced significant EPS and EBITDA declines over the past few years. Comparably, the S&P 500 has been able to grow earnings at mid-single digits rates historically and is expected to grow earnings by ~12% in 2024.

Despite performing significantly worse historically than its primary customers, GM, F, and Stellantis AXL trades at a major valuation premium based on the P/E ratio. AXL trades at 9.5x forward earnings compared to 4.3x, 6x, and 3.3x respectively for GM, F, and STLA.

Seeking Alpha Seeking Alpha Seeking Alpha

{kind=link}

{kind=link}

Historical Valuation Analysis

As shown by the charts below, AXL appears to be trading somewhat cheap to its historical valuation. This does not get me excited given AXL's historical performance. The poor historical performance of AXL historically suggests the stock had been previously overvalued. Furthermore, given where we are in the economic cycle at the end of a high-growth period I believe AXL should be trading at the lower end of its historical range.

Risks To My View

The biggest near-term risk to my view is that AXL shares bounce back following the announcement of a deal between the UAW and big three automakers to end the ongoing strike. AXL is only down 6.6% compared to the nearly 14% drop in GM shares since the strike started. For this reason, I expect any bounce in AXL shares to be relatively small in the event the strike ends soon.

Another potential risk to my view is that AXL explores strategic alternatives including a sale of the company. In late 2022, AXL released a statement that it was not engaged in talks to sell the company. This statement followed rumors that Melrose Industries PLC (MLSPF), BorgWarner (BWA), and Dana (DAN) had expressed interest in a deal. Any deal could see AXL shares acquired for a premium to the current share prices as buyers would be willing to pay a premium in hopes of capitalizing on synergies.

Conclusion

AXL shares have not proved a good investment historically and I do not believe that is going to change. The company competes in a highly competitive industry and tends to generate low profit margins even in the best of times.

AXL's customer base is highly concentrated with GM, F, and STLA accounting for 70% of sales. This gives customers increased bargaining power relative to AXL. AXL also has a highly unionized workforce which makes it difficult for the company to generate outsized profits over the long-run as labor will want its share. Additionally, AXL is highly exposed to the EV business. GM recently announced that it was slowing production and investments in the EV business which is a negative for AXL.

Despite being in a highly cyclical industry, AXL carries a relatively high debt load at 3.3x EBITDA. While the current debt load is not yet unsustainable, that could quickly change in the event of any economic weakness.

AXL shares trade at below market forward P/E of just 9.5x. However, I do not view this valuation as attractive given the high earnings volatility, low growth, and poor historic performance. Moreover, AXL trades at a higher valuation than customers which enjoy a generally superior business.

For these reasons, I am initiating AXL with a sell rating. One factor that could cause me to re-consider my rating would be if AXL announces that it is putting itself up for sale as I believe there would be a number of interested buyers.

For further details see:

American Axle & Manufacturing: Historical Challenges Likely To Continue