AOUT - American Outdoor Brands: Lack Of Clear Growth Catalysts

2023-09-27 12:42:57 ET

Summary

- The company's revenue decreased by 0.5% YoY, while the operating loss (% of revenue) reached 9.4%.

- While management expects the company to post positive revenue growth through 2024 (fiscal) year, I think margins will continue to be under pressure.

- At the moment, I do not see any clear catalysts for stock growth, so my recommendation is hold.

Introduction

Shares of American Outdoor Brands ( AOUT ) have fallen 7% YTD. Despite the fact that the company's management is talking about a possible resumption of revenue growth, I believe that it is still not the best time to open long positions. In my article, I would like to analyze the company's financial statements and share my own expectations about future financial results.

Investment thesis

Buying the company's shares was an excellent bet on tightening Covid restrictions during the pandemic, however, at the moment, I believe future operating and financial results will continue to be under pressure. First, I believe that the company will continue to demonstrate weak revenue growth due to pressure on consumers from macro headwinds and the lifting of Covid restrictions. Secondly, the operating margin of the business continues to be in negative territory, while I do not see additional drivers for improving profitability in the coming quarters. Thirdly, in my personal opinion, the valuation of the company's shares in accordance with the multiples does not look cheap.

Company overview

American Outdoor Brands sells products and accessories for outdoor activities (hunting, shooting, fishing, camping). The company uses both offline (58% of revenue) and online sales channels (42% of revenue). The main revenue segments are Shooting sports (46% of revenue) and Outdoor lifestyle (54% of revenue). The company's main market is the USA (92% of revenue), while international sales account for about 8% of revenue.

1Q 2024 (fiscal) Earnings Review

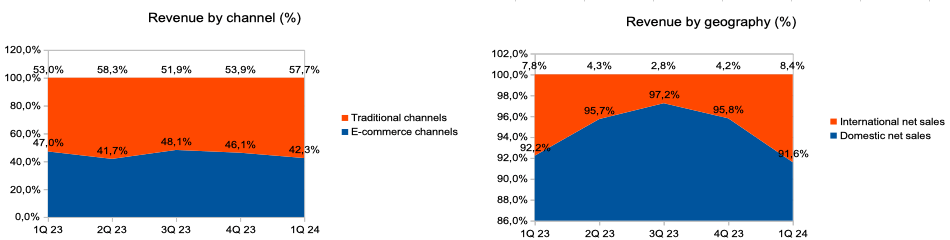

The company reported results better than investors expected . The company's revenue decreased by 0.5% YoY . The main contribution to revenue was made by traditional sales channels, which showed growth by 8.4% YoY, while sales in the e-commerce segment decreased by 11% YoY. In terms of sales geographies, the main contribution was made by international sales, where revenue growth amounted to 7.5% YoY, sales in the US market decreased by 1.2% YoY.

Revenue by channel (%) and revenue by geography (%) (Company's information)

{kind=link}

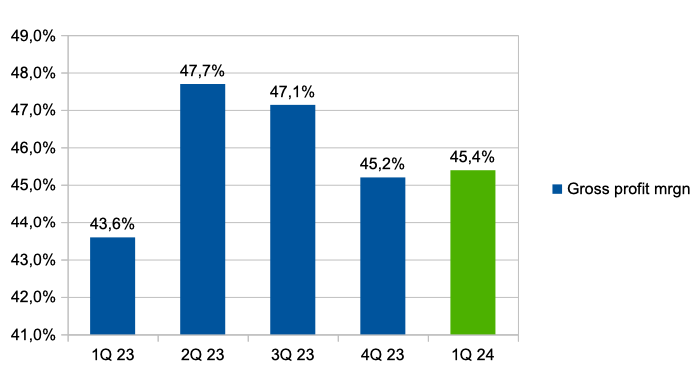

Gross profit margin increased from 43.6% in 1Q 2023 (fiscal) to 45.4% in 1Q 2024 (fiscal) due to a reduction in freight costs.

{kind=link}

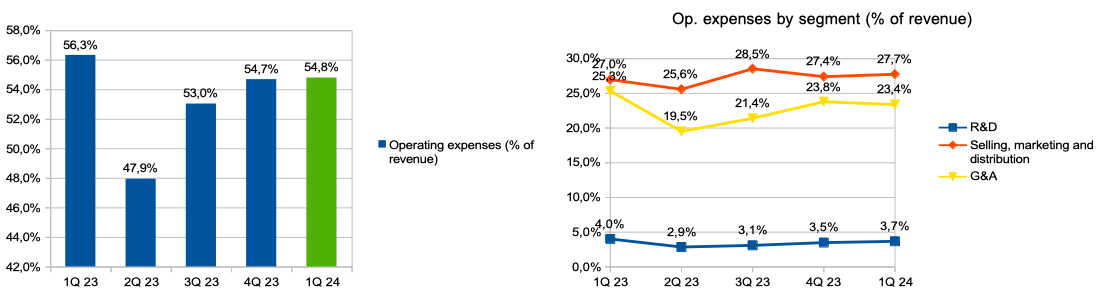

Operating expenses (% of revenue) decreased from 56.3% in the 1st quarter of 2023 (fiscal) to 54.8% in the 1st quarter of 2024 (fiscal). The largest contribution to the reduction in operating expenses was made by R&D and G&A, where expenses decreased from 4% to 3.7% and from 25.3% to 23.6%, respectively.

Op. expenses (% of revenue) and op. expenses by segment (% of revenue) (Company's information)

{kind=link}

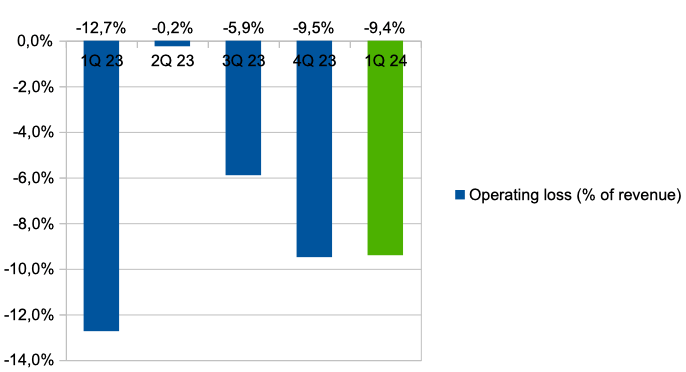

Thus, operating loss (% of revenue) decreased from 12.7% in the 1st quarter of 2023 (fiscal) to 9.4% in the 1st quarter of 2024 (fiscal).

{kind=link}

In addition, the company provided guidance for 2024 (fiscal) year. Thus, management expects that revenue growth can reach 3.5% YoY, and adj. EBITDA could increase by 6.5% YoY. You can see the details in the graph below.

Guidance (Company's information)

My expectations

On the one hand, I don't expect that we can see support from the demand side, so I think the company will continue to show modest revenue growth rates in the coming periods. First, even if we see inflation slow, consumers will continue to face higher day-to-day costs, which I believe will continue to weigh on consumer spending. Secondly, spending on hobbies no longer receives additional support due to the lifting of Covid restrictions and the reduction in the amount of time people are forced to spend at home.

Moreover, if we pay attention to the company's guidance, we will see that management does not expect the level of gross profit margin to improve during 2024 (fiscal) . Thus, I believe that the operating profitability of the business will continue to be in the negative zone, because the potential for reducing operating expenses is limited due to the high share of fixed expenses (salaries, rent).

Turning to gross margins. We expect fiscal ‘24 gross margins to remain flat to fiscal 2023. With regard to OpEx, we believe that overall OpEx for fiscal 2024 will increase slightly, mainly from higher selling and distribution costs, offset by reductions from our facility consolidations, one-time legal and advisory fees, and IT implementation costs. Based on these factors, we continue to believe our adjusted EBITDAS in fiscal 2024 could increase as much as 6.5% compared to fiscal 2023.

Risks

Margin: increased competition, rising costs, declining economies of scale and renewed growth in freight costs could put pressure on future operating margin performance.

Macro (general risk): high inflation and a decline in consumer spending may lead to a reduction in consumer spending in the discretionary segment, which may have a negative impact on the dynamics of business revenue growth in the following periods.

Drivers

Revenue: launching new products (hunting, fishing) and entering new markets can have a positive impact on both future revenue growth rates and the company's market share.

M&A: low debt burden and sufficient cash on the balance sheet provide the company with the potential to conduct M&A transactions, which can contribute to both business growth and improved operating margins due to synergistic effects.

Valuation

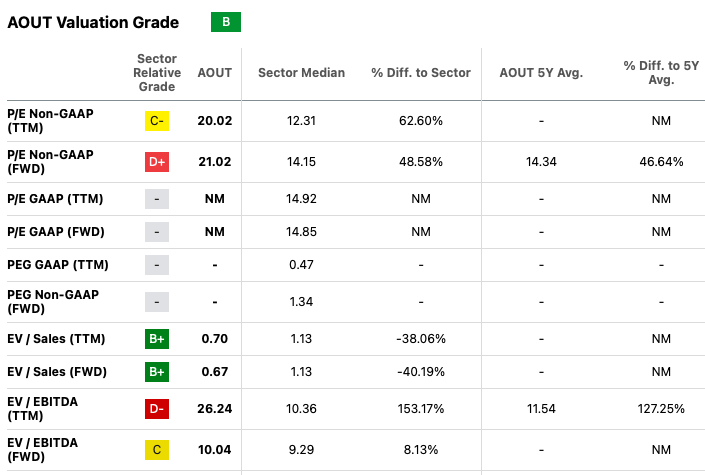

Valuation Grade is B. According to P/E ((FWD)) and EV/EBITDA ((FWD)), the company is trading at 21x and 10x, respectively, which implies a premium to the sector median of about 49% and 8%, respectively. On the one hand, I don't think the current valuation level is high, but on the other hand, I don't think the valuation is low enough, while I don't see any additional drivers/catalysts that could push the stock higher in the future.

{kind=link}

Conclusion

Thus, at the moment my recommendation is hold. I expect revenue growth and margins to continue to show modest levels in the coming quarters. I will continue to monitor the company's financial statements going forward and may change my recommendation if I see signs of recovering demand or improving profitability.

For further details see:

American Outdoor Brands: Lack Of Clear Growth Catalysts