AOUT - American Outdoor Brands: No Solid Reason To Buy (Technical Analysis)

2023-07-21 12:13:37 ET

Summary

- American Outdoor Brands reported a 22.7% decline in net sales for FY23, with a net loss of $12.7 million, largely due to weakness in its shooting sports and outdoor lifestyle category.

- Despite a strong balance sheet, the company's disappointing financial performance and low projected growth rate for FY24 have led to a hold rating being assigned.

- The company's success in e-commerce is critical, but reliance on external platforms and competition could negatively impact margins and relationships with brick-and-mortar clients.

American Outdoor Brands ( AOUT ) offers outdoor products globally. They provide hunting, camping, and defense products. They also provide electro-optical devices and firearm cleaning supplies. AOUT recently posted its FY23 and Q4 FY23 results. I will analyze its financial performance in FY23 and the technical chart in this report. I think there is no solid reason to invest in AOUT right now. Hence I assign a hold rating for AOUT.

Financial Analysis

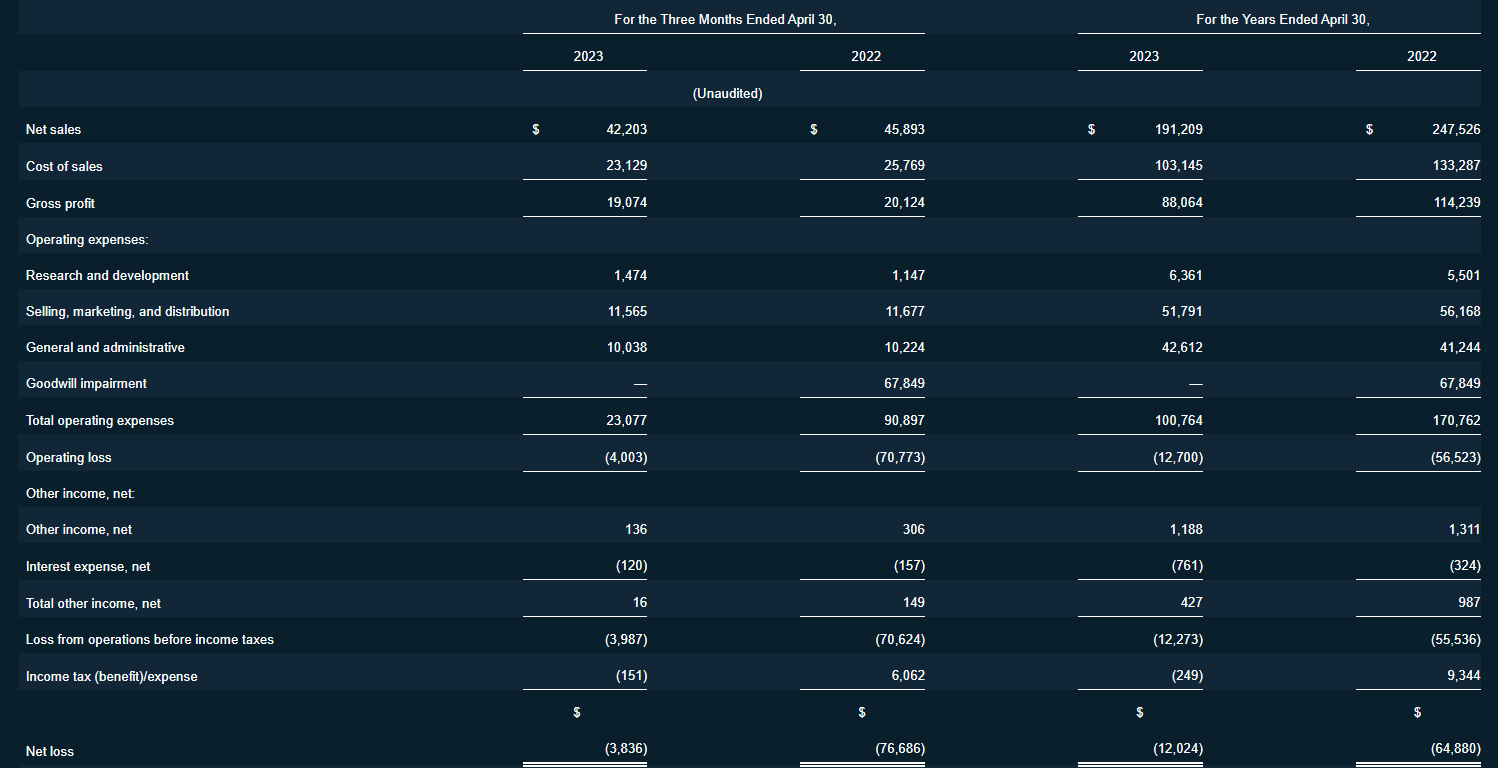

AOUT recently announced its FY23 and Q4 FY23 results . The net sales for FY23 were $191.2 million, a decline of 22.7% compared to FY22. I believe weakness in its shooting sports and outdoor lifestyle category was the main reason behind the sales decline. Its net sales in the shooting sports and outdoor lifestyle category declined by 30.7% and 14.3% in FY23 compared to FY22. I think that measures taken by retailers to cut their total inventory levels and lower consumer spending were the main causes of this decline. Its gross profit margin in FY23 was 46% which was 46.1% in FY22. I think the slight decline was mainly due to the product mix. The net loss for FY23 was $12.7 million compared to a net loss of $56.5 million. In FY22, there was a $67.8 million noncash goodwill impairment charge. So the decline in net loss in FY23 wasn’t something significant.

{kind=link}

The net sales for Q4 FY23 were $42.2 million, a decline of 8% compared to Q4 FY22. I think the sales decline in its shooting sports and outdoor lifestyle category was the main reason behind the drop. The net sales in its shooting sports and outdoor lifestyle category declined by 7.5% and 8.6% in Q4 FY23 compared to Q4 FY22. The net loss for Q4 FY23 was $3.8 million compared to a net loss of $76.6 million. The Q4 FY22 included impairment charges; hence the net loss was huge in Q4 FY22. My opinion looking at the numbers, is that I would avoid it because there wasn’t a single positive to take out of its annual results. Its sales and margins declined, and I would not be comfortable investing in it based on its financials.

Technical Analysis

{kind=link}

AOUT is trading at the $9.1 level. It is trading 50% below its IPO price and 75% from its all-time high, which shows that it has been a wealth destroyer in my opinion. Talking about the current price action. In May 2023, the stock made a beautiful double-bottom pattern, one of my favorite reversal patterns. A double-bottom pattern indicates that a downtrend might be over soon. But after making a double bottom pattern, the stock has already moved up by 28%, so in my opinion, investing right now would not be worth it because of the unfavorable risk to reward. So based on the technicals, I am assigning a hold rating on it. A fresh buying opportunity will only arise if it crosses the $12 level, as it is a resistance zone, and if the price crosses it, then we might see fresh momentum in the stock.

Should One Invest In AOUT?

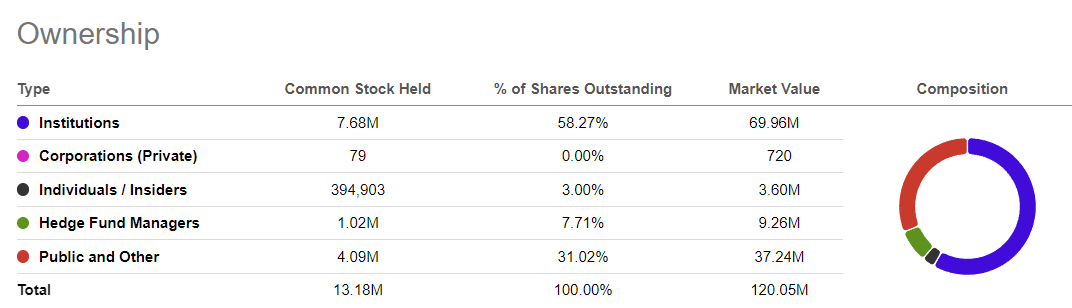

The shareholding pattern of AOUT looks good, with 58.27% of the shares owned by institutions which is a positive sign, especially for a small capitalization company like AOUT. In addition, by the end of FY23, it had cash worth $22 million, a rise of 12.2% compared to FY22, and its short-term debt was $11.5 million, which is quite small considering that it is a micro-cap company. Usually, micro-cap companies have a large debt amount in my experience. So looking at its cash, the debt is not an issue which shows that it has a strong balance sheet which is an optimistic sign.

{kind=link}

But despite having a strong balance sheet, I would advise ignoring the company for now. I am saying this because of its disappointing financial performance in FY23, and talking about the FY24 expectations, the company expects its sales to be around $198 million, which is just 3.5% higher than FY23 revenue. I think a growth rate of 3.5% is quite low, and with this growth rate, I think it might be difficult for them to expand the company and keep up with the industry. In addition, their first quarter is usually the lowest in terms of sales, so I think its share price might remain under pressure in the short term. Hence considering all the factors, I assign a hold rating on AOUT.

Risk

E-commerce retailers are under strong pressure to make their products easily and quickly accessible through e-commerce services as consumers shop more and more online through these shops. AOUT's success in e-commerce depends on its capacity to use its marketing tools to successfully engage with current and potential clients. They might need to compete by being more promotional to improve their e-commerce sales, which could affect their gross margin and raise their marketing costs. They just created, and are continuing to improve, their direct-to-consumer e-commerce platform, but they largely rely on external e-commerce platforms to sell their goods, which might allow their e-commerce clients more say in setting the price of their products. Due to the e-commerce pricing to end customers, this could have negative relationship repercussions with their clients who own brick-and-mortar shops as they may believe themselves to be at a disadvantage in my view. They might struggle to grow their online store and adapt to changing customer traffic patterns and direct-to-consumer purchase trends.

Bottom Line

Their financial performance in FY23 was disappointing, and the company expects its sales growth rate in FY24 might be slow. Hence, I don’t think there is any solid reason to invest in it right now. Hence I assign a hold rating on AOUT.

For further details see:

American Outdoor Brands: No Solid Reason To Buy (Technical Analysis)