ACTV - An Update On The Banking Crisis

2023-05-10 16:54:34 ET

Summary

- The regional banking crisis has continued after the failure of Silicon Valley Bank.

- Rapid increases in short-term interest rates have pushed the cost of funds for some banks above the interest rate that they can conservatively earn on a loan portfolio.

- This problem will last for as long as the Federal Reserve holds interest rates high and the yield curve remains deeply inverted.

- There will be more bank failures in the months ahead.

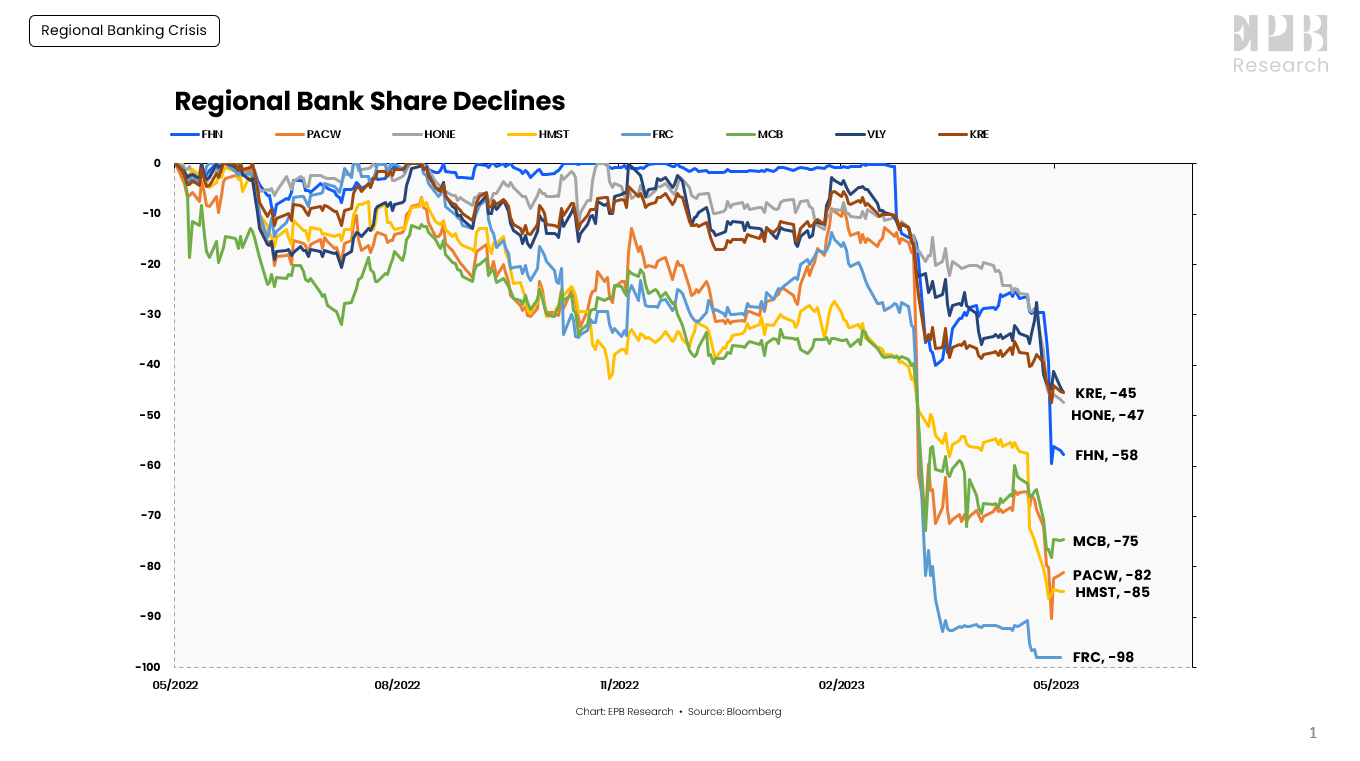

The regional banking crisis has continued after the failure of Silicon Valley Bank (SIVBQ).

First Republic Bank (FRCB) failed in late April, and several other banks have come under considerable market pressure.

Shares of HomeStreet (HMST), Metropolitan Bank (MCB), and PacWest Bank (PACW) have declined more than 75% over the last year.

{kind=link}

Even after the Federal Reserve created the Bank Term Funding Program and offered emergency liquidity to the financial sector, the stress on various regional banks persists.

In this post, we'll look at the true problems impacting the regional banking sector and why there will be more bank failures in the months ahead.

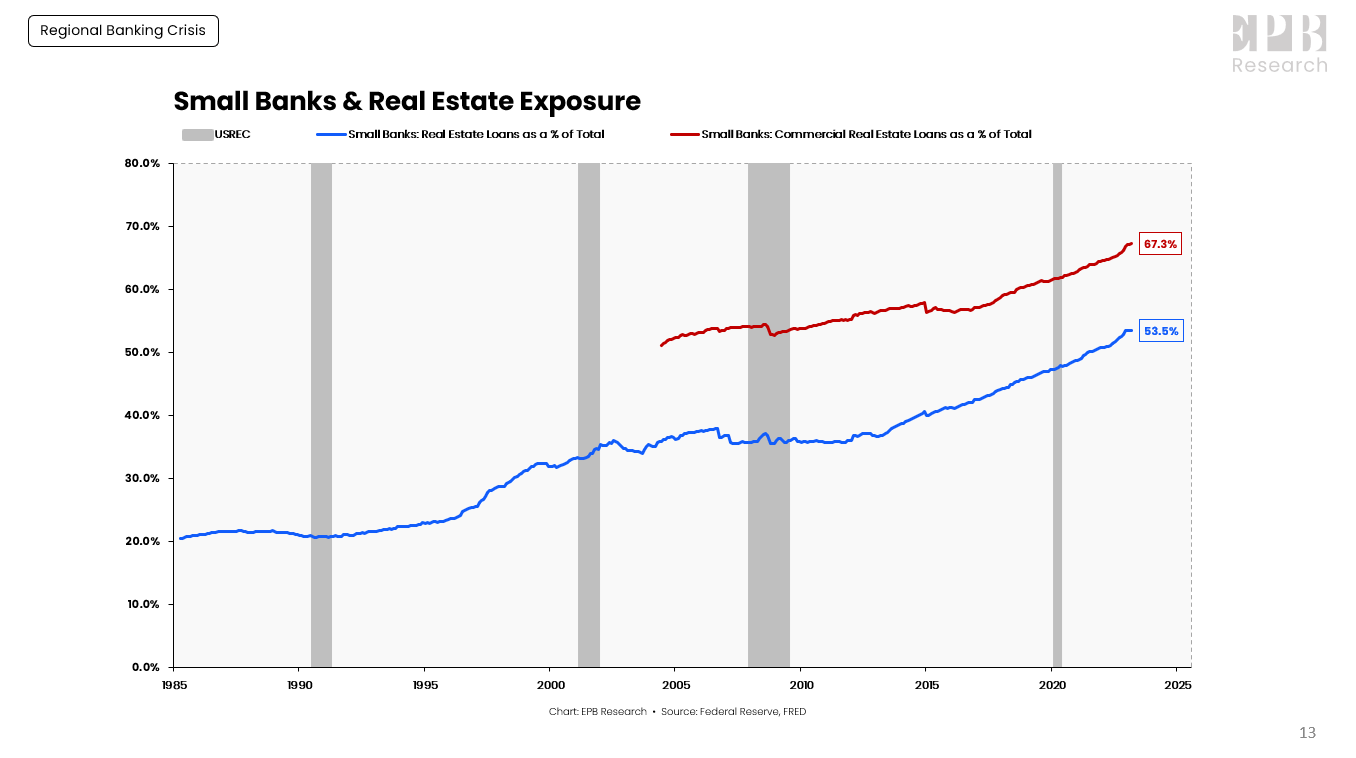

Small banks have massively increased their share of real estate lending over the last several decades, so the reduction in real estate credit availability may be significant, amplifying the existing recessionary forces.

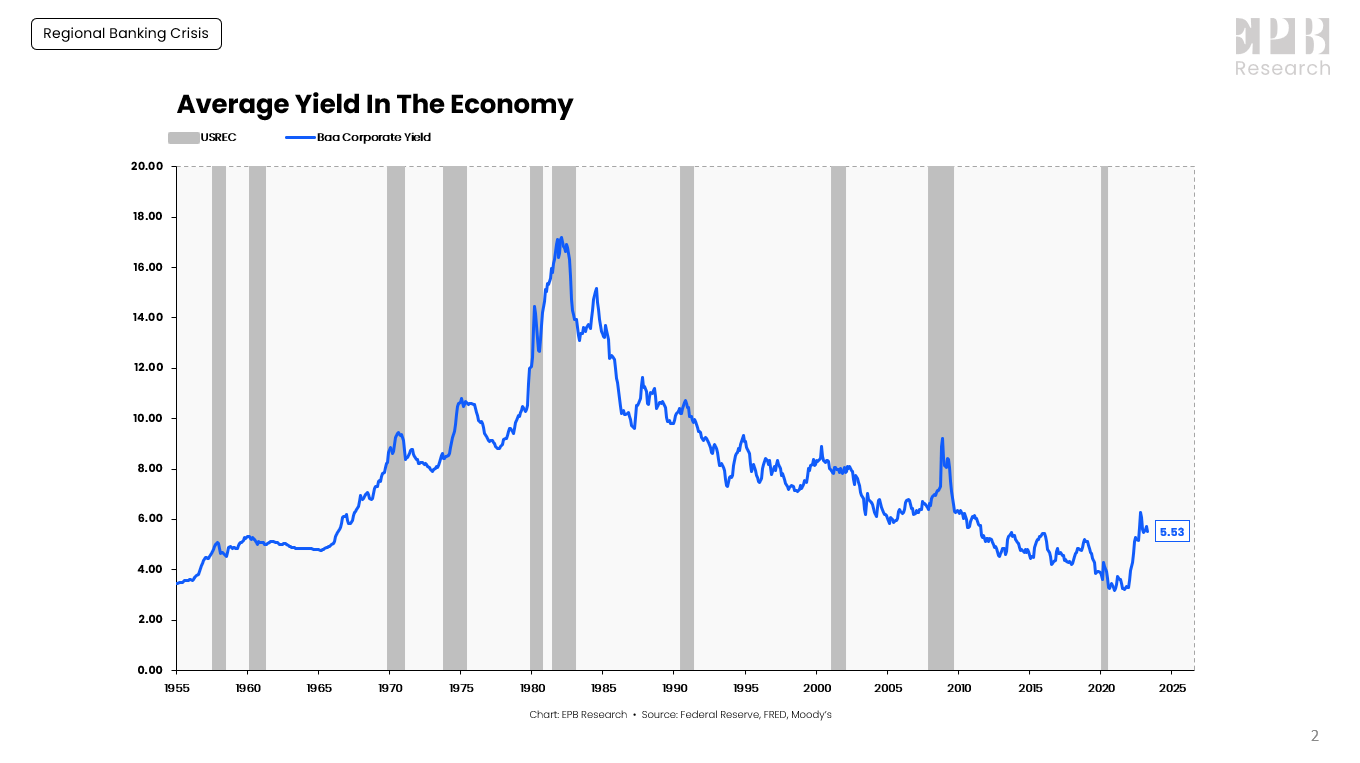

Average Yield In The Economy

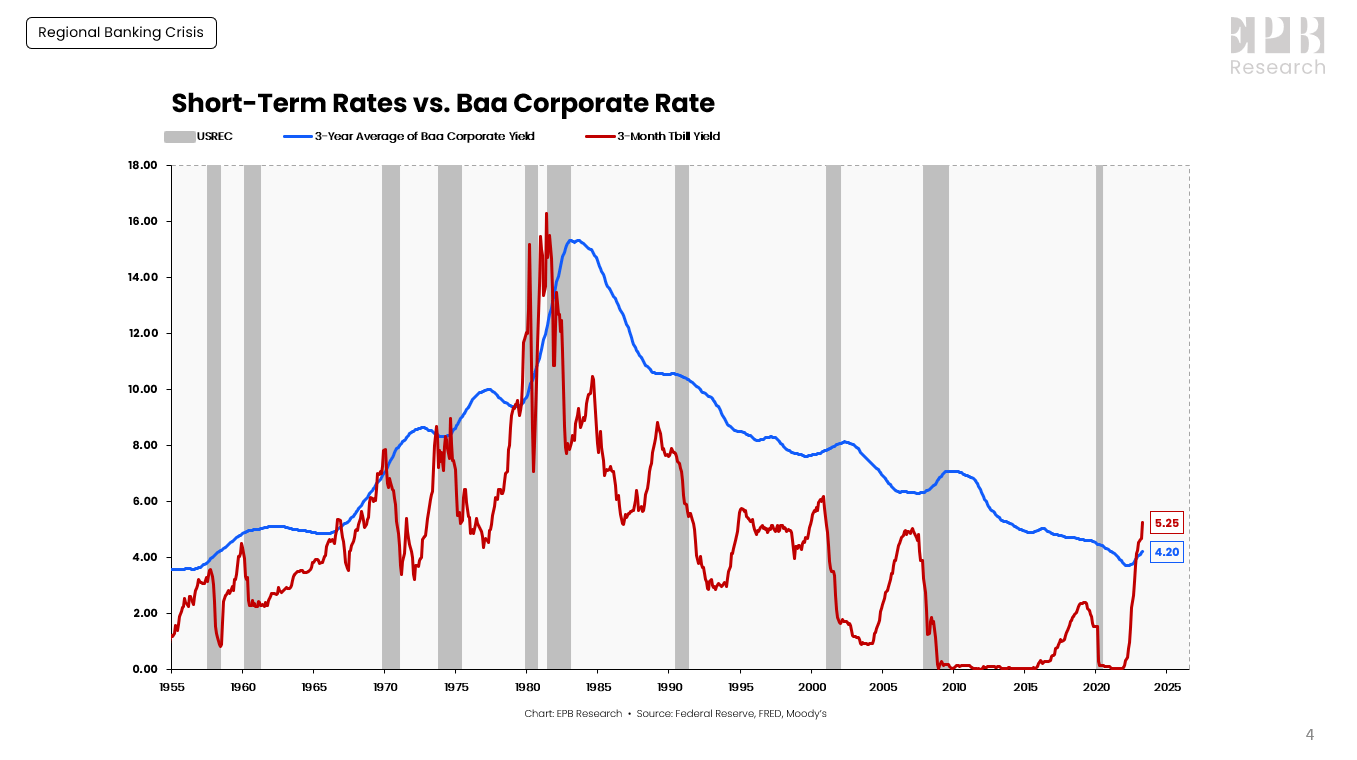

A bank's business model is generally described as "borrow short and lend long."

That means banks borrow money at short-term interest rates and lend money at long-term interest rates. The spread between the interest rate on their long-term loans and short-term funding costs is the profit to the bank.

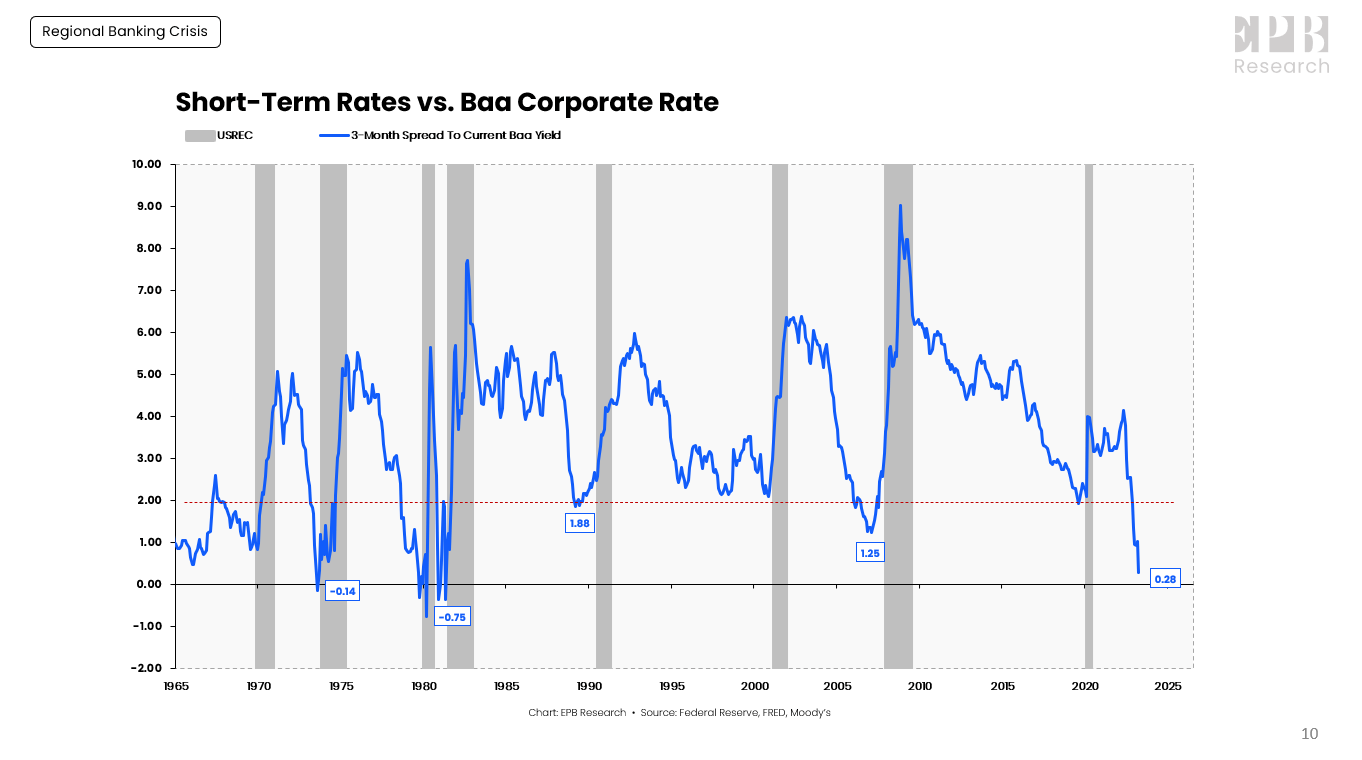

Swedish Economist Knut Wicksell suggested that the average yield in the economy is about equal to the Baa corporate bond rate.

The Baa rate is the best approximation for the average loan yield or asset yield in the economy.

So when a bank loans money or buys bonds, its average yield will be about the same as the Baa corporate rate.

{kind=link}

It takes time for a bank to make loans or reprice their assets, so a three-year average of this Baa corporate rate also can be used to judge the average yield in the economy.

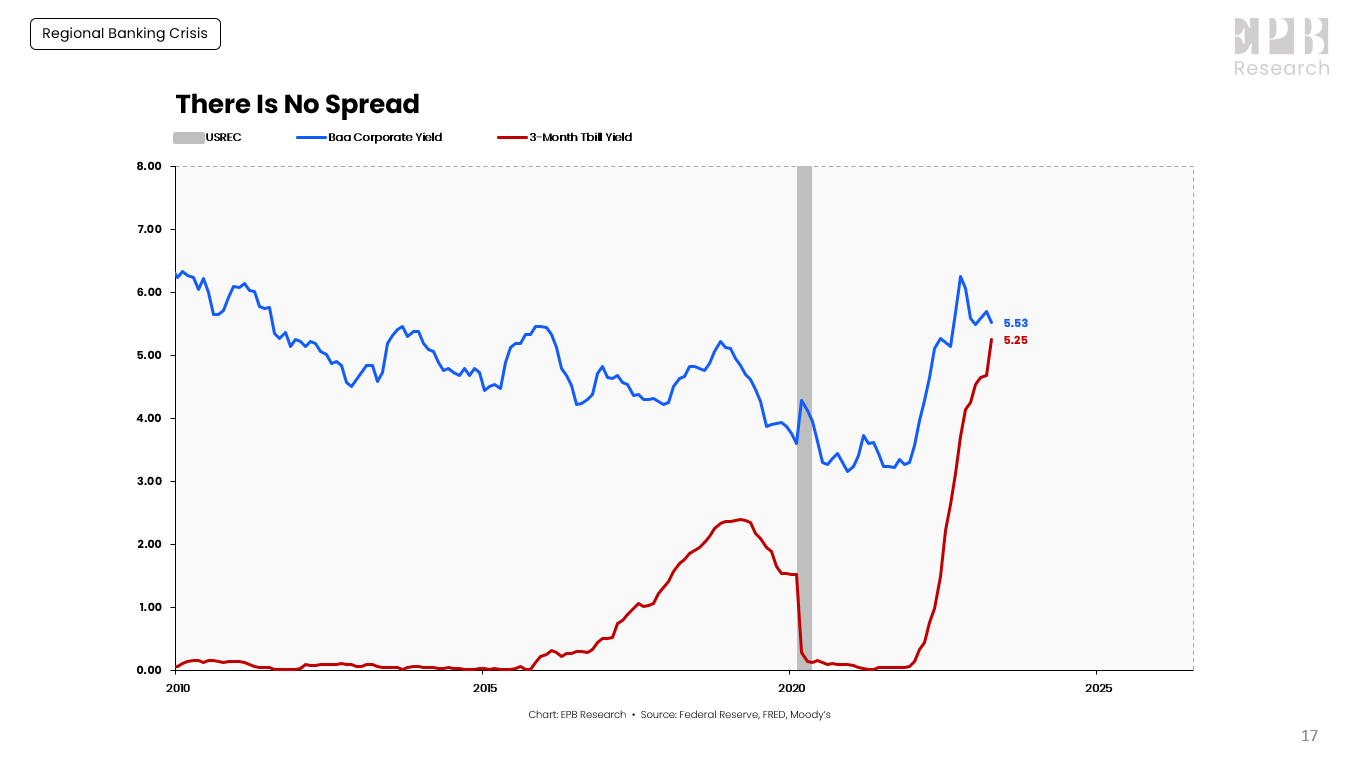

The surface-level problem is that the Federal Reserve has increased short-term interest rates to more than 5.0%.

Federal Reserve, FRED, Moody's

{kind=link}

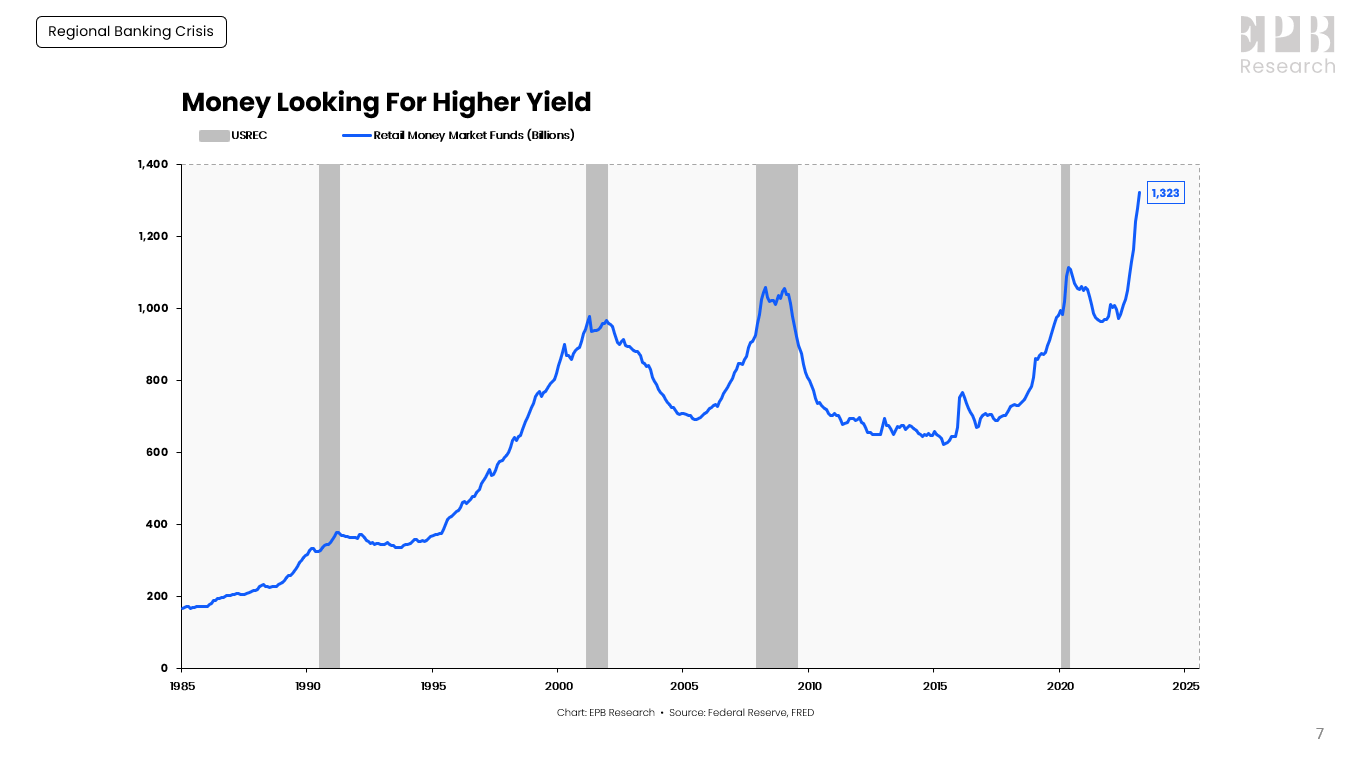

Treasury bills and money market funds, the competition for banks, offer a very high yield. Many people are moving money out of banks paying 2.0% (or less) to money market funds offering nearly 5.0%.

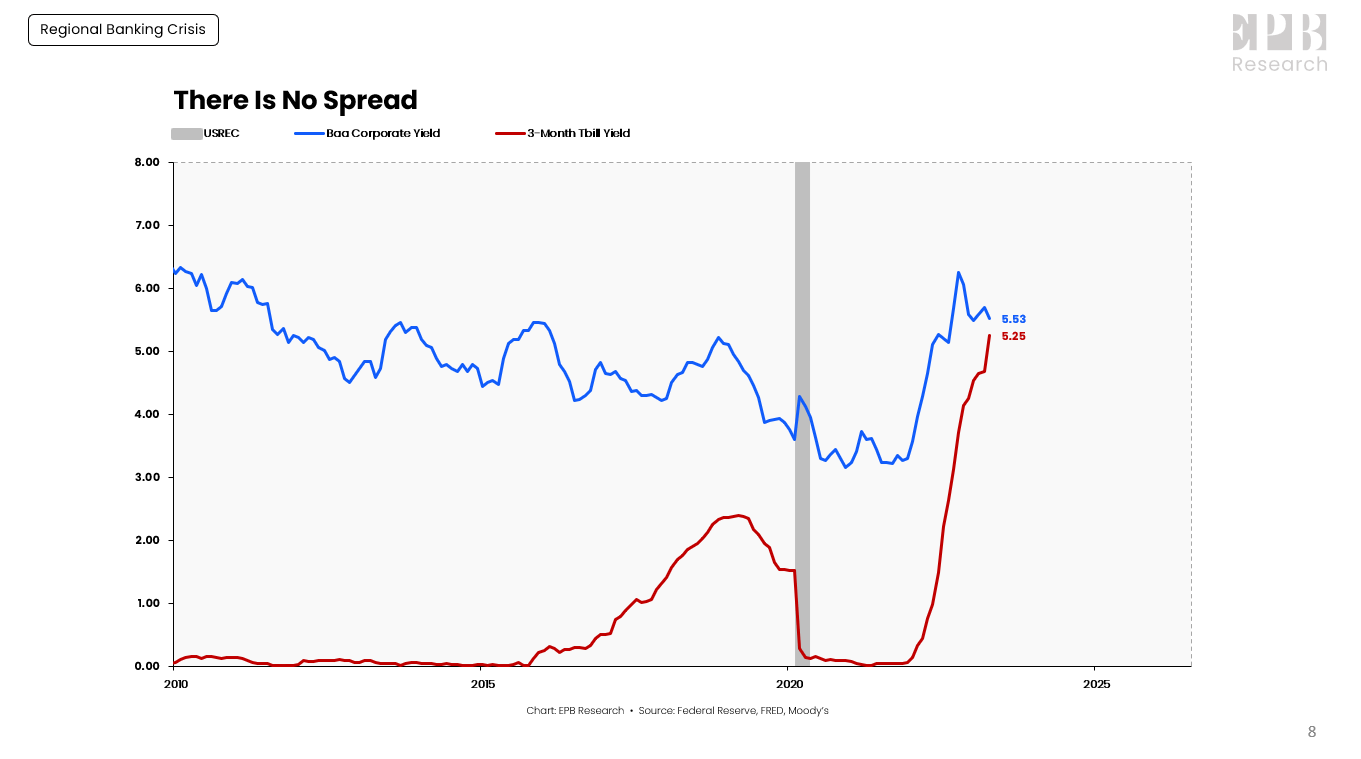

Banks are then forced to rapidly increase the rate they pay on deposits to something closer to 5.0% when the average yield in the economy is still about 5.5%. There's no spread for the bank to make money.

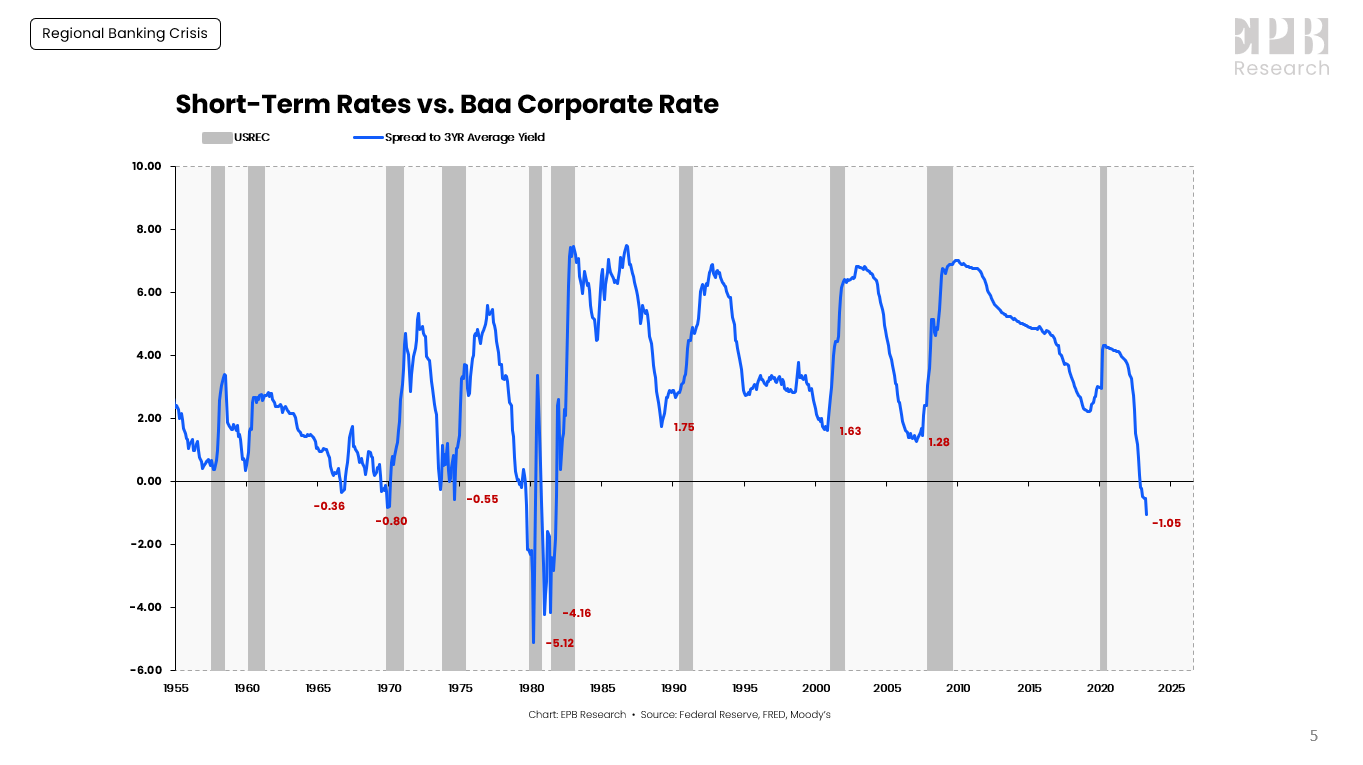

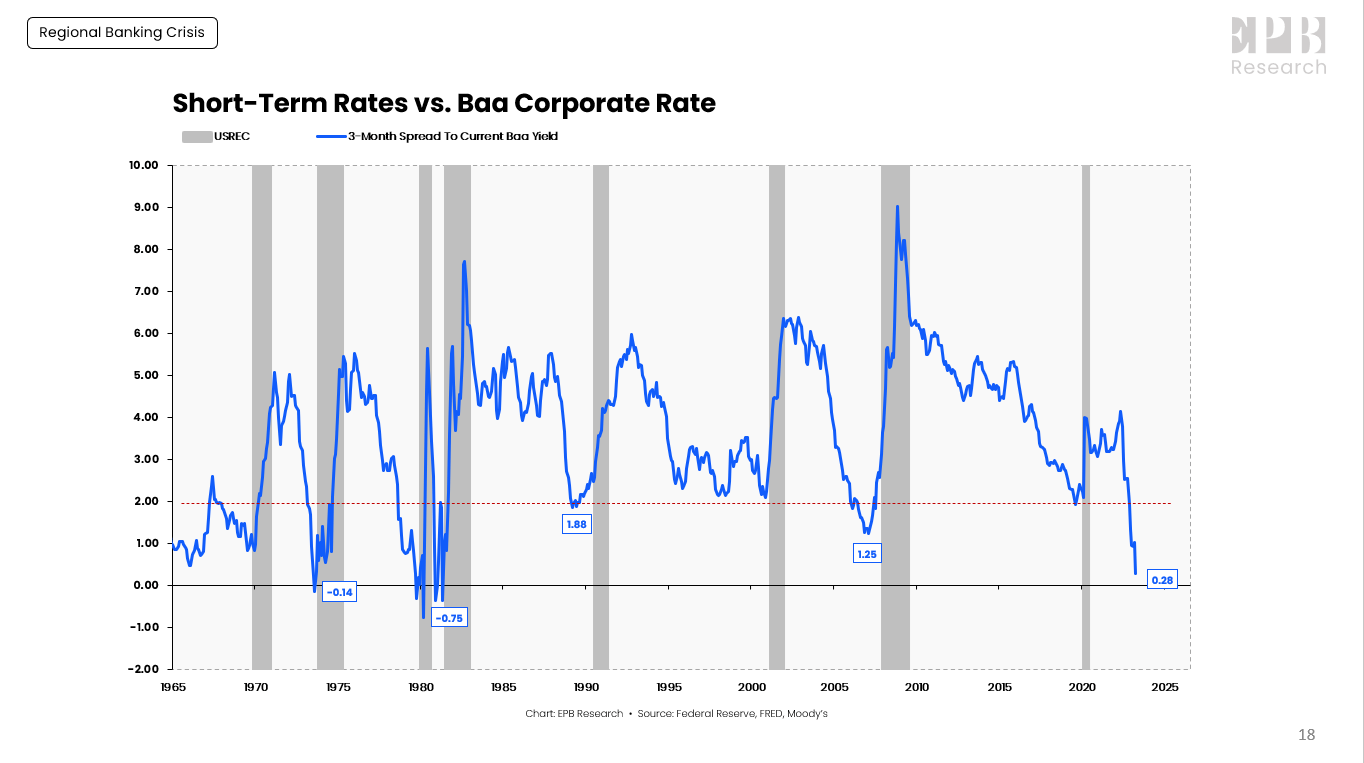

The spread between short-term interest rates and the three-year average Baa corporate rate has only been below -1%, like today, in the double 1980 recession.

Federal Reserve, FRED, Moody's

{kind=link}

Ironically, the 1980 recessions were engineered to combat an inflation problem, resulting in the failure of a portion of the nation's savings and loan industry (S&L crisis).

Today, rapid increases in short-term interest rates have pushed the cost of funds for some banks above the interest rate that they can conservatively earn on a loan portfolio.

Under Pressure Banks

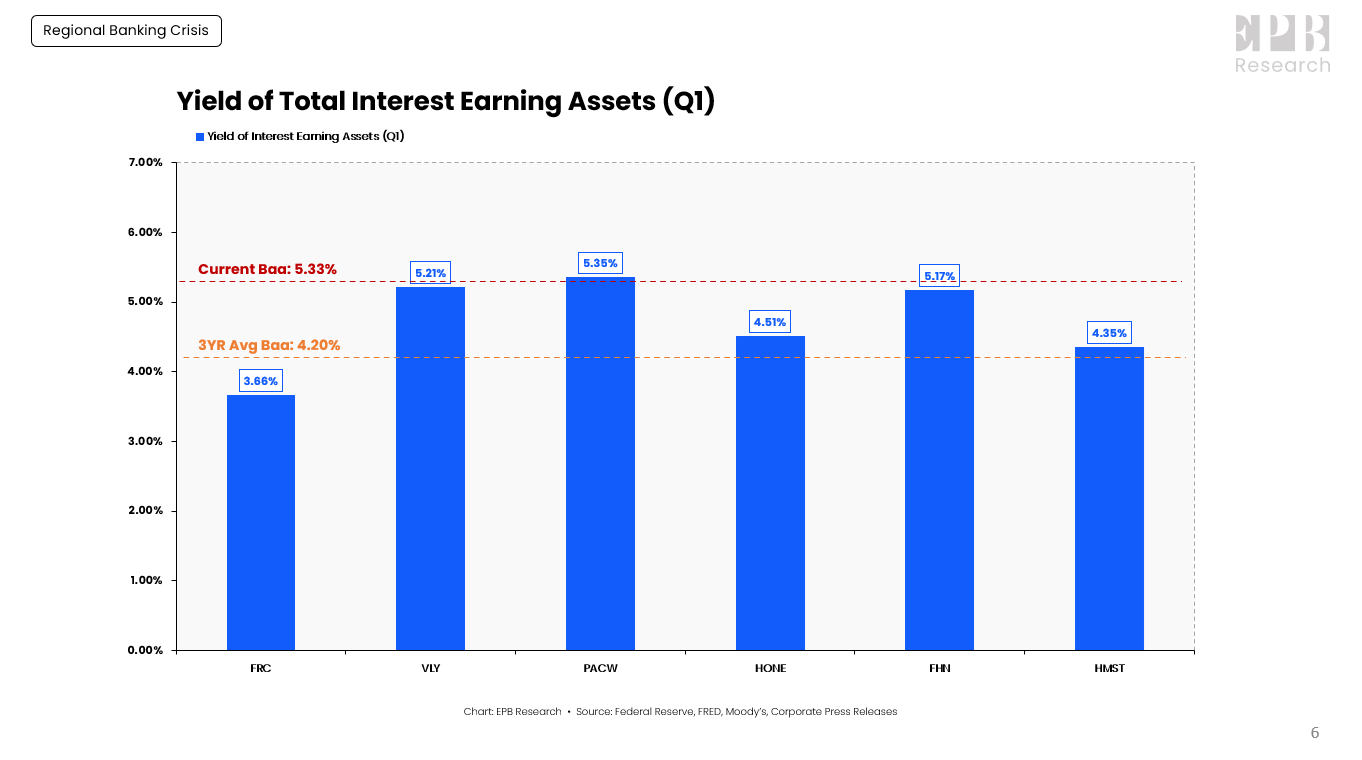

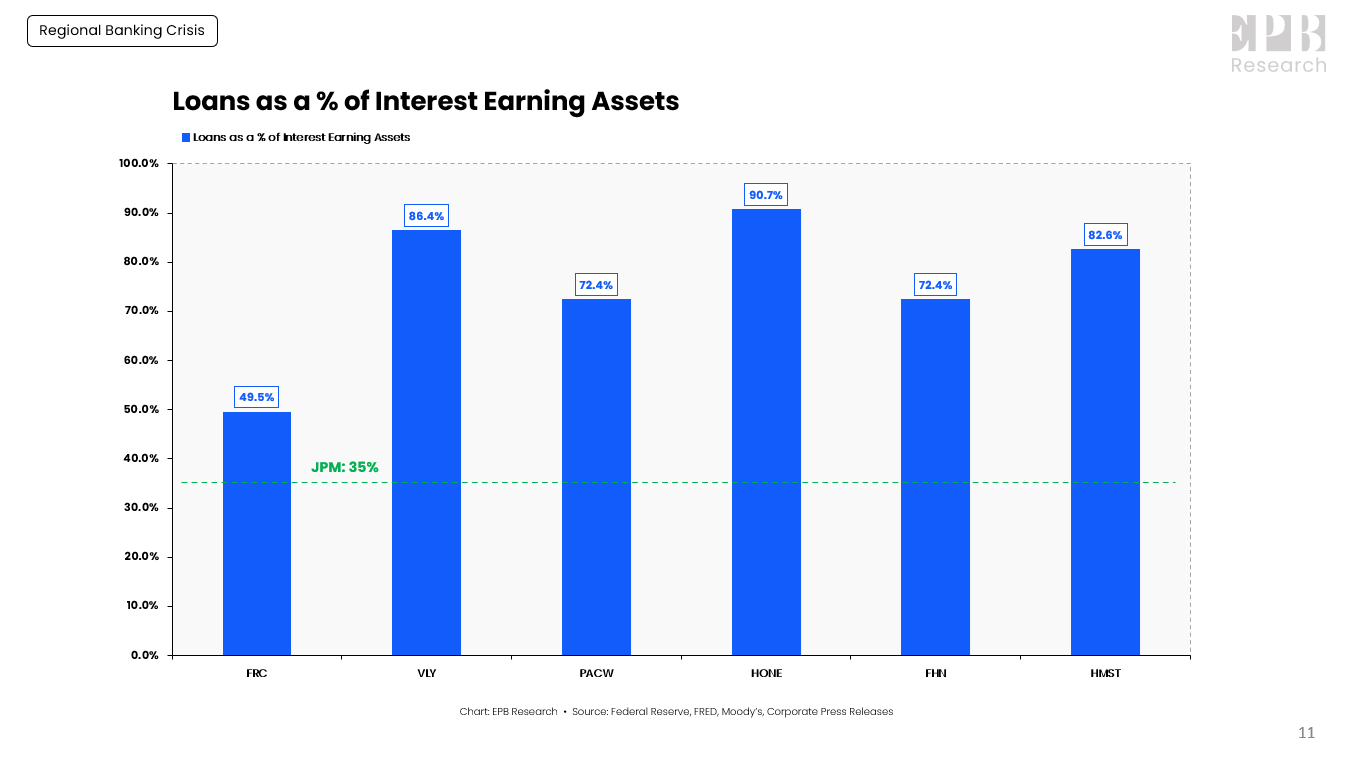

If we look at some of the banks that the market has punished, the problem is clear. This is not a problem of a "few bad management teams" but rather an industry-wide issue of unprofitability.

The 3YR average of the Baa corporate rate is 4.2%, and the current yield is 5.33%. That means that the yield banks can earn on their asset portfolio will likely converge somewhere in this range. If we round up, that means most banks will earn about 4.5% to 5.5% on their assets.

{kind=link}

A bank may try and earn 6% or 7%, but that also means the bank is likely taking on more credit risk, which is not a good idea if your deposit base is unstable and recession risks are imminent.

First Republic Bank, as of their Q1 filing, had an average yield of 3.66% on their interest-earning assets. If deposits are leaving and you must increase your rates and pay nearly 5.0% to keep customer money, the bank clearly cannot operate.

This issue is not solved by the government guaranteeing all deposits. Cash is flowing into money market funds, not necessarily for safety, but rather for more yield. It's free money, after all.

{kind=link}

If a bank is experiencing an outflow of deposits and has to increase rates to near 5.0% to keep money or attract new customers, but the average yield the bank can earn in the economy is about 5.5%, the bank will not be able to operate profitably.

{kind=link}

It's hard for banks to reprice their loan books quickly, but if deposits are fleeing, they have to reprice the interest they pay on deposits very quickly.

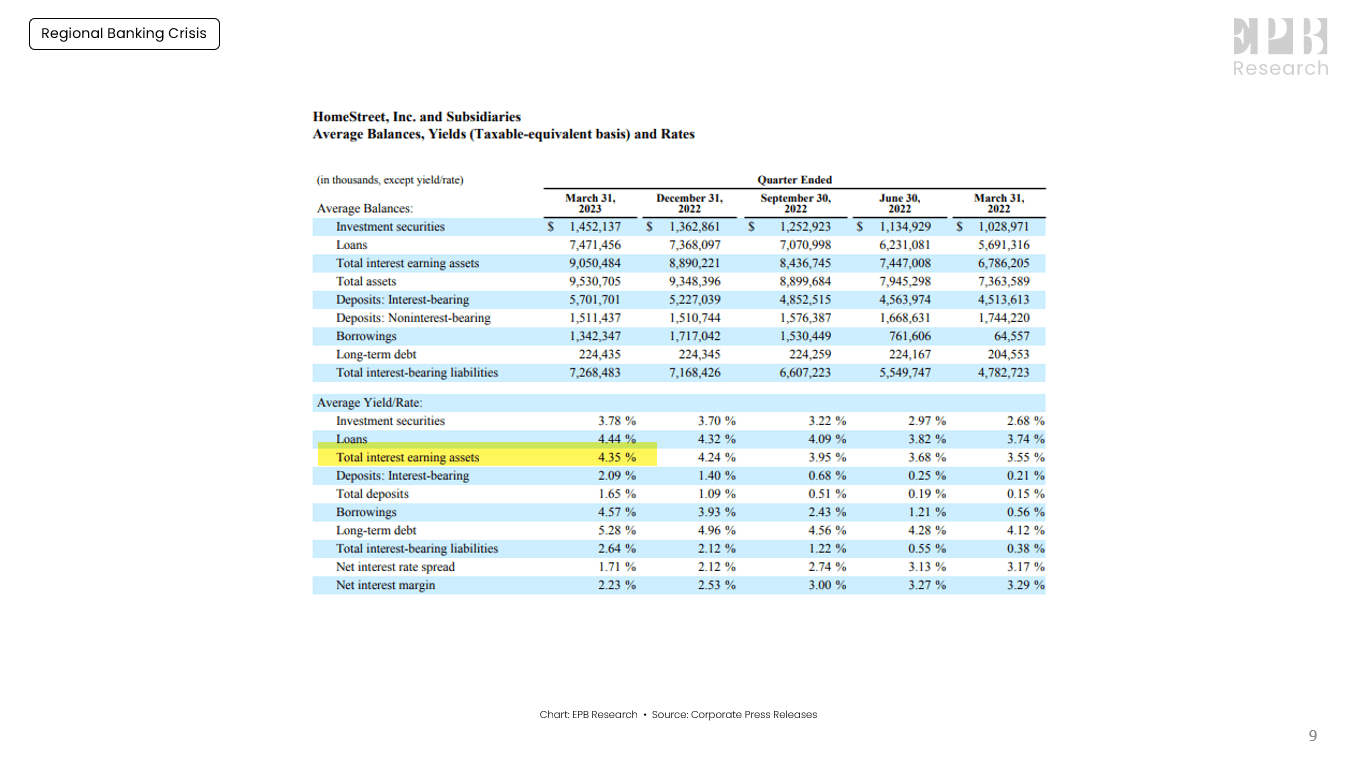

If we look at the press release from HomeStreet, one bank the market has placed under considerable share-price pressure, we can see that they earn 4.35% on their interest-earning assets.

This is up from 3.55% a year earlier, but that means over the course of one year, they increased the yield on interest-earning assets by less than 1.0%.

{kind=link}

The interest rate paid on liabilities has increased more than 2.0%, rising to 2.64% from 0.38% a year earlier. So the cost of funds will have to jump again and continue to rise towards 5.0% while the interest on the assets will struggle to rise and keep up.

This is just one example, but the industry as a whole will face the same issue. There is a distribution, and some banks will be above the average and some below, but as a collective industry, funding costs have increased too much relative to prevailing asset yields.

{kind=link}

Historically the Baa corporate rate or the average yield in the economy must be 2.0% higher than the short-term interest rates. When the spread drops too low, bank lending tightens, and a recession occurs.

Real Estate Heavy Banks

Funding costs are only one issue plaguing the banking sector.

The second problem is that these banks, the same banks facing funding cost issues, are very concentrated in real estate and commercial real estate in particular.

Some of the regional banks currently under market pressure have 70%, 80%, or 90% loans as a percentage of interest-earning assets, with many banks having commercial real estate loans as the largest share.

{kind=link}

We can see that in the 1980s, during the S&L Crisis - which was caused by the same issue of rapidly rising rates - small banks made about 20% of all real estate loans. Today, small banks make up more than 50% of all bank real estate lending.

Most of that is commercial real estate lending. Small banks are responsible for 67% of all bank commercial real estate lending.

{kind=link}

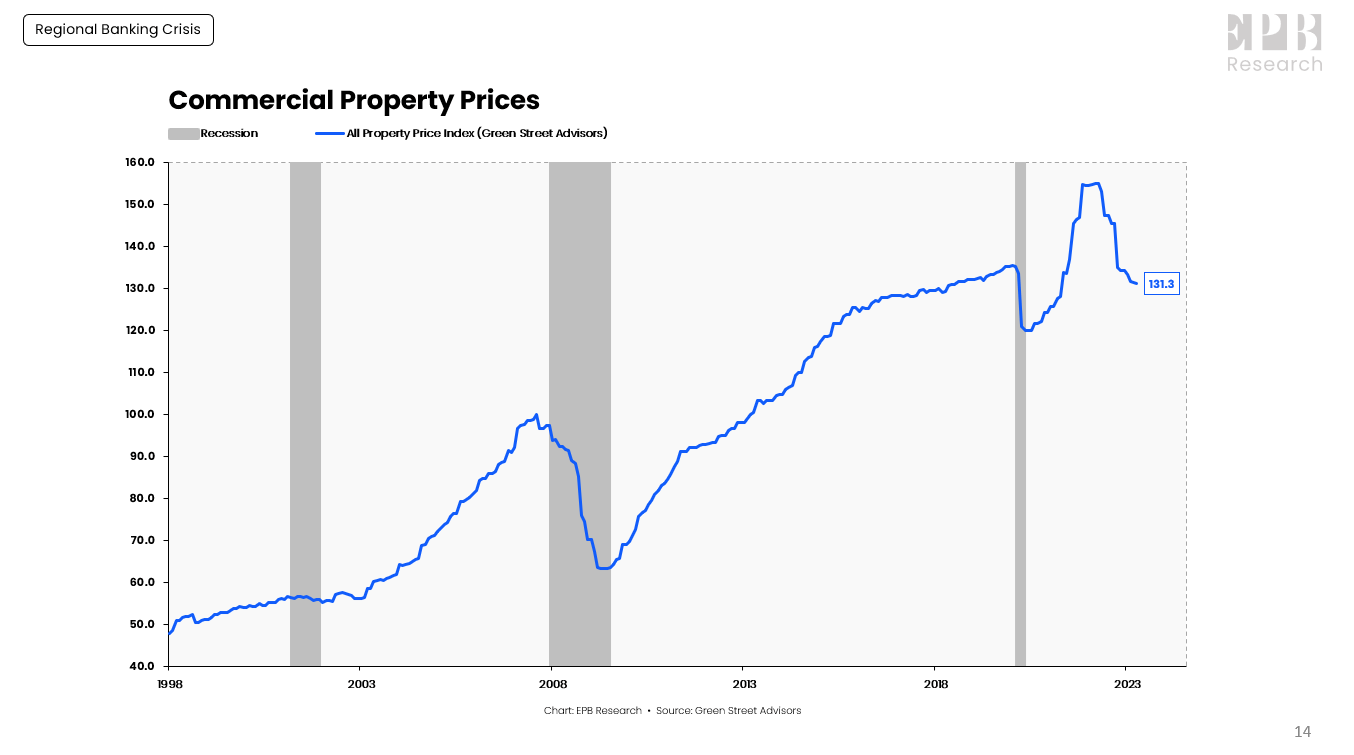

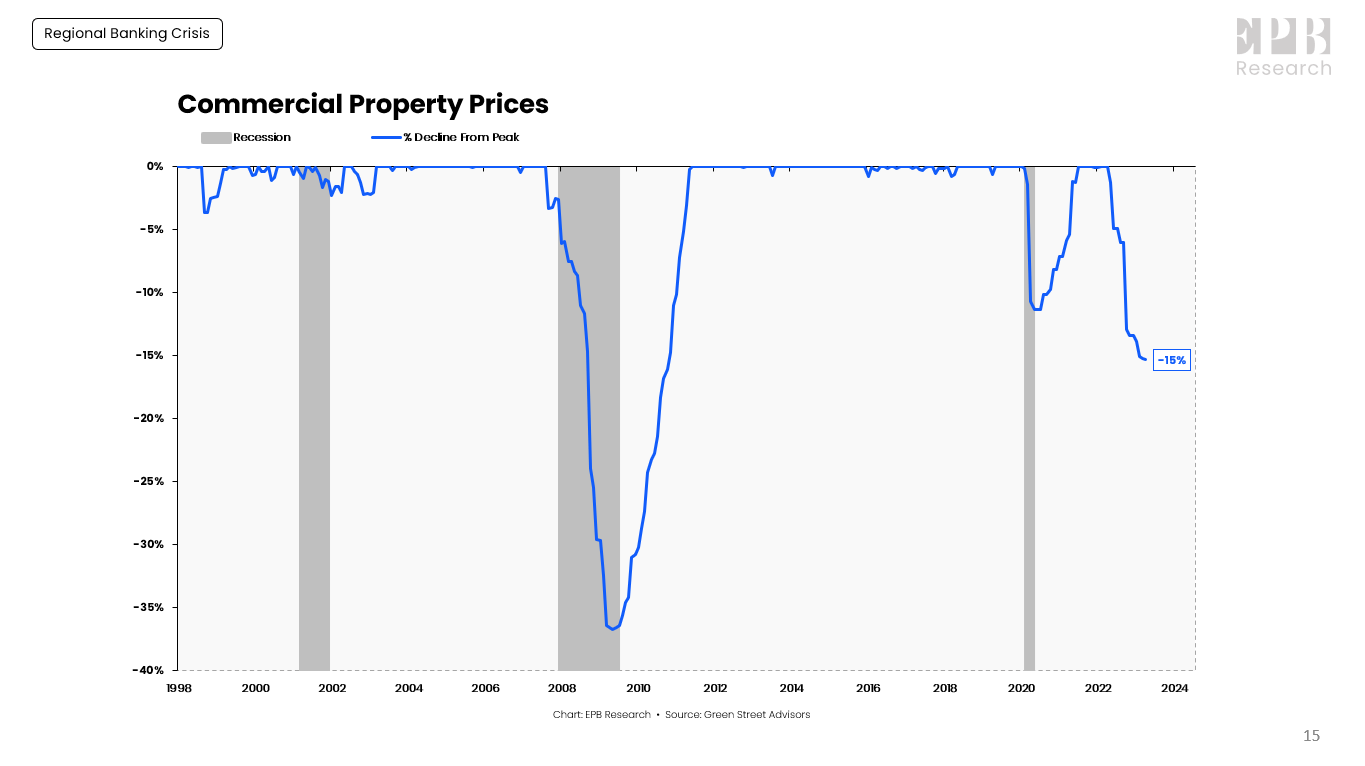

The value of the properties that many of these small banks have loaned money to is declining. The Commercial Property Price Index published by Green Street Advisors peaked in early 2022, and as interest rates have gone up, the price has declined.

{kind=link}

The commercial property sector has declined 15% in total. These price declines are not spread evenly. Some declines are more severe in office buildings, and some sectors are holding up better than others, but every sector is off its peak level, and the price declines as a total industry are the largest in the last 15 years.

{kind=link}

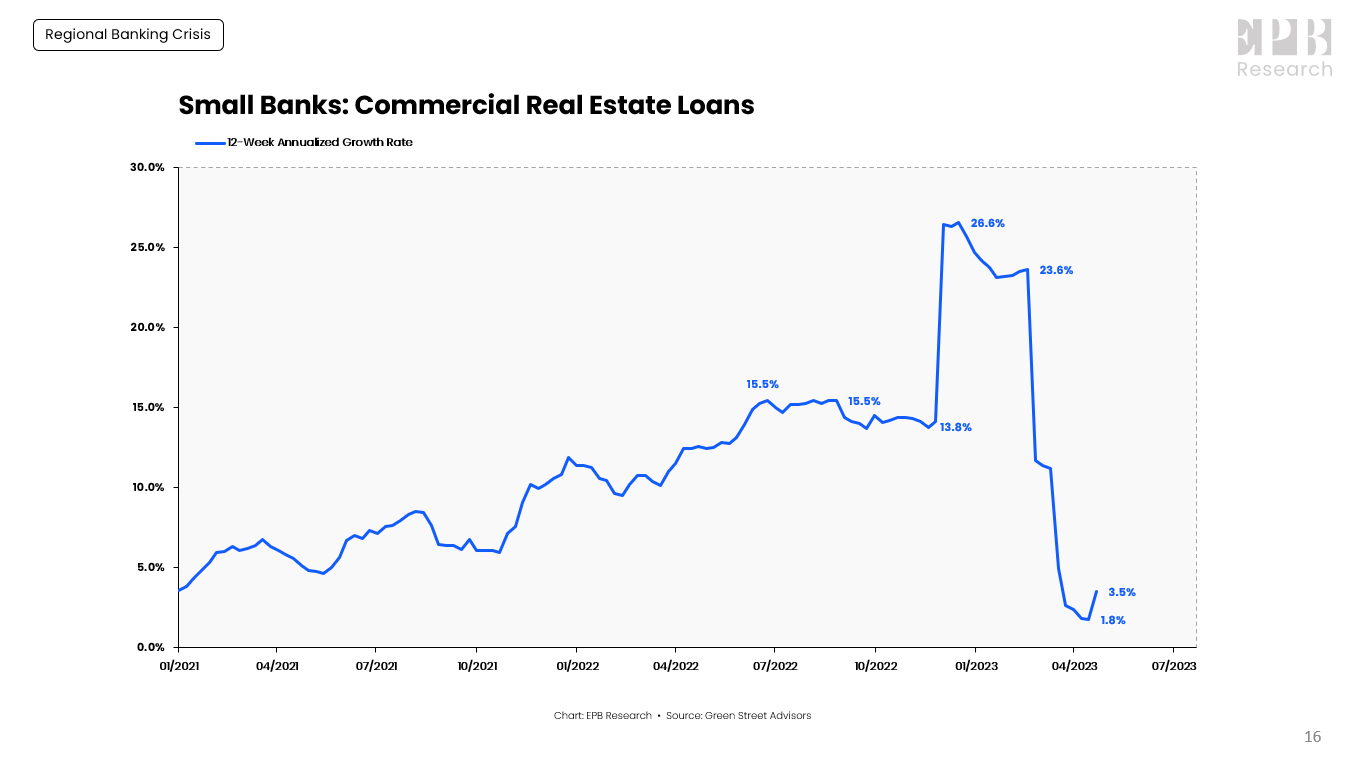

As bank lending has become unprofitable, with no spread between short-term rates and average yields in the economy, and as banks have experienced volatile deposits outflows, commercial real estate loan growth has slowed from 15% or 20% to just 2% or 3% over the last 12-weeks.

Two Major Problems

So banks are facing two problems. Treasury bills and money market funds offering nearly 5.0% are serious competition for bank deposits.

{kind=link}

Individual banks will face outflows if they do not raise the interest rate they pay on deposits. The cost of funds for certain banks will rise above asset yields and pressure bank profitability.

This problem will last for as long as the Federal Reserve holds interest rates high and the yield curve remains deeply inverted.

{kind=link}

The second problem is that the value of the assets at some smaller banks, specifically some of the commercial real estate assets, may be worth a lot less compared to one year ago or two years ago.

Banks cannot operate when there is no spread, or an inverted spread, between the short-term rates and average yields in the economy.

The business model of banks has not changed from borrowing short and lending long. As a result, an inverted yield curve and deposit outflows will lead to more bank failures in the months ahead.

{kind=link}

Lowering interest rates will help the cost of funds issue. However, the value of some real estate assets may still be in question, like empty office buildings, even if interest rates are lowered to alleviate any bank funding stress.

For further details see:

An Update On The Banking Crisis