AGPPF - Anglo American Platinum: Don't Get Spooked (Rating Downgrade)

Summary

- Many investors are worried about Anglo American Platinum Limited's soft Q4 production and South Africa's systemic headwinds. Nevertheless, the market has likely already priced a worst-case scenario for PGM miners.

- The situation in South Africa is grim, and Eskom is a severe issue. However, Anglo possesses the necessary resilience to fight through tough times.

- Anglo Platinum has a stronghold over the global platinum supply, and most systemic challenges to its operations will probably be offset by higher PGM prices.

- The Polokwane smelter will likely bolster the firm's total refined output when it's up and running again.

- Anglo Platinum's total return prospects are still well-aligned, especially as the stock is trading below its cyclical average P/B ratio.

Anglo American Platinum Limited's ( ANGPY ) stock has suffered an approximate 20% capitulation during the past month, influenced by variables such as softer production guidance, ongoing geopolitical battles, and lower overall macroeconomic activity.

Although Anglo Platinum's year-to-year has been disappointing, the company and its stock possess underestimated influencing variables. As such, we believe investors have overreacted to recent events and argue that Anglo Platinum still provides a valuable investment opportunity.

Operating Results

Production Update

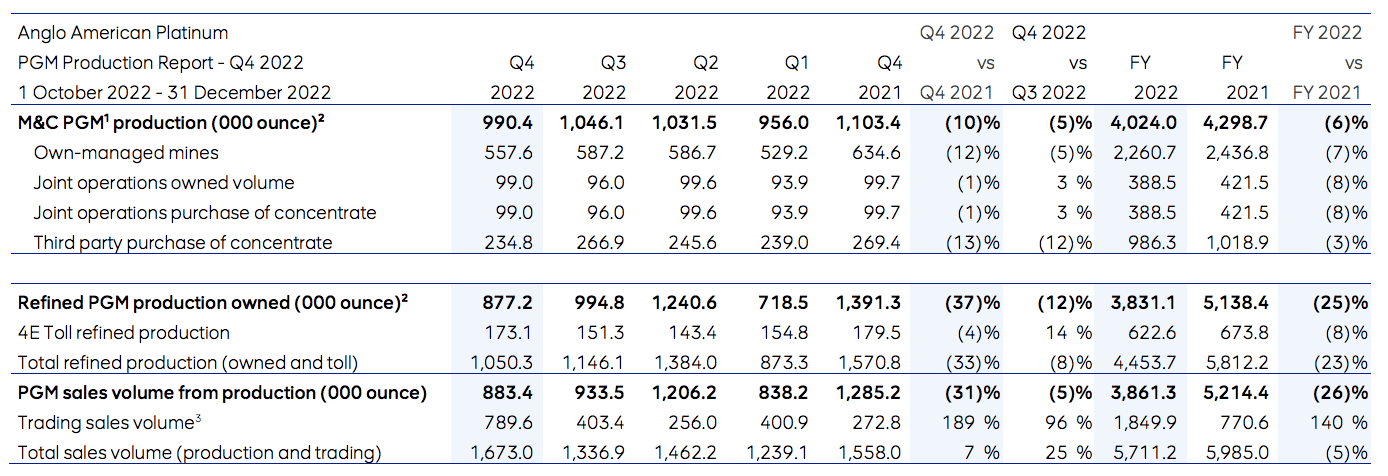

Similar to other South African PGM (platinum group metals) miners, Anglo Platinum has suffered from various uncontrollable factors, and thus underperformed during its fourth-quarter.

Amplats' total production slumped by a staggering 10% year-over-year in its fourth quarter, while its own-operated mines' production slipped by 12%. Most of its own mines' subdued performance can be attributed to lower grades from Mogalakwena and Unki. However, a strong quarter from Mototolo phased out some of the damage.

In other bad news, the Polokwane smelter's rebuild has progressed slower than initially anticipated due to implications with furnace construction proceedings. The smelter's inactivity led to a 37% slump in year-over-year refinery production from Anglo Platinum. Moreover, although the company's Waterval and Mortimer smelters phased out some of the Polokwane-inflected refinery damage in Q4, the Eskom crisis (discussed later in the article) has resulted in lower "work-in-progress" inventory as the company's refineries are struggling to ramp-up with constant electricity issues.

{kind=link}

Lastly, the company's base metal production also slipped as Nickel and Copper realized lower than a year ago.

Base Metals (Anglo American Platinum)

{kind=link}

Looking Ahead

Let's take our outlook from the top and move down incrementally.

Anglo Platinum realized significantly lower prices in its fourth quarter. Logic and basic observation of asset return distributions tell us that the metal price surges during 2021 and early 2022 were never sustainable.

However, it would not be surprising if PGM and base metal prices experienced a slight recovery in the coming months.

On what premise?

Firstly, the economic outlook has improved, with U.S. GDP growing faster than anticipated, China is reopening, Europe is expected to abate a recession, and the interest rate hiking cycle is nearing an end. As such, demand factors could exceed recent expectations.

Furthermore, the Eskom power crisis and decaying South African infrastructure could halt PGM production. However, there could be leveling as lower output from South Africa could cause elevated PGM prices.

To illustrate the supply/demand impact that Anglo Platinum and South Africa have on the PGM space, consider that Anglo Platinum is the world's largest platinum producer and that South Africa's bushveld complex supplies up to 75% of the globe's annual platinum and palladium demand ( 80% platinum, 40% palladium ). Thus, diminishing production will likely be met with more supportive prices.

Price Realization (Anglo Platinum)

{kind=link}

Moving down the ladder, Anglo Platinum has guided toward a 2023 production of refined production of 3.6 to 4 million PGM ounces, subject to Eskom implications at a unit cost between R16 800 and R17 800 per ounce (approximately $975 at the midpoint).

We think Eskom's situation will only worsen before it gets resolved. In fact, there is strong reason to believe that the entity will run out of capital before it delivers consistent electricity. However, the mines still have adequate electricity to operate for large portions of the day. In addition, Anglo Platinum has enormous 5-year average profit margins, leaving it with plenty of dry powder to fund alternative power sources.

{kind=link}

Furthermore, the Polokwane smelter could arrive online soon, providing an enormous boost to the company's refined production, consequently phasing out much of the damage caused by South Africa's state-owned electricity producer, Eskom.

Dividend Analysis & Valuation

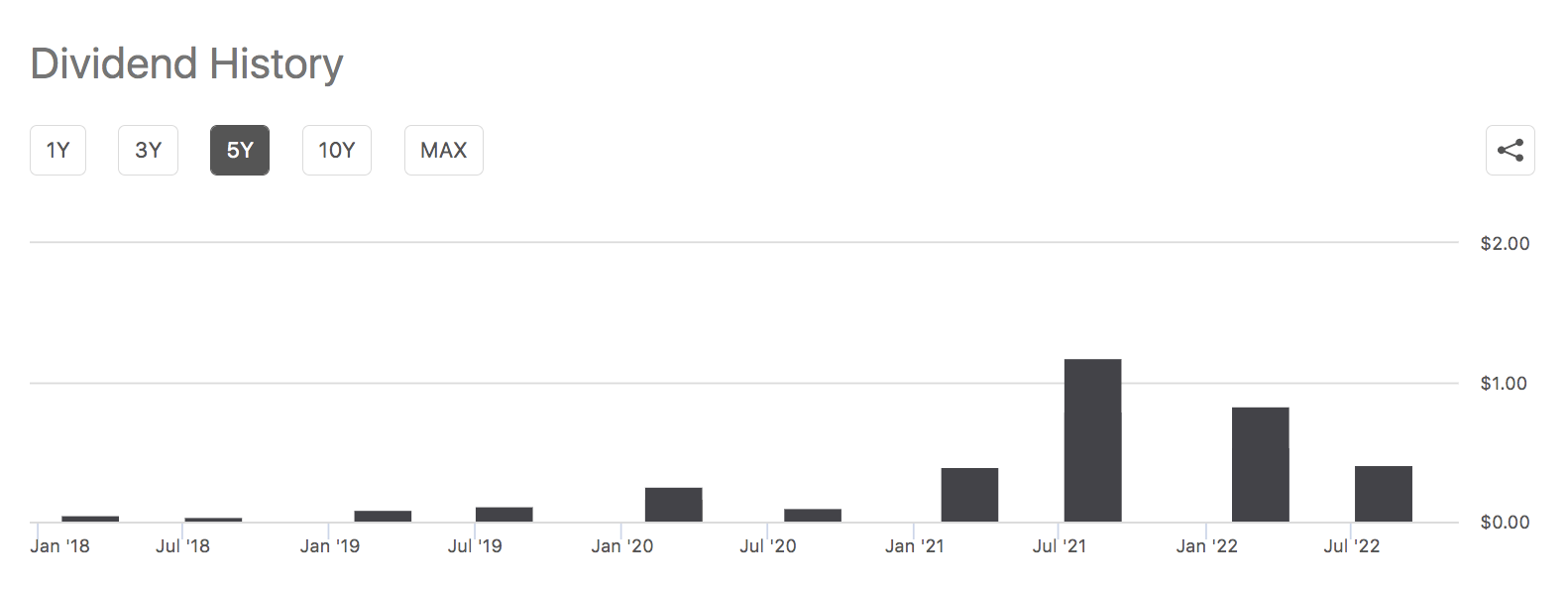

There is no doubt that Anglo Platinum's dividend is in danger of being reduced amid slower results. In addition, CEO, Nastacha Viljoen was recently quoted saying : "Will our investors continue to get their returns? Yes, they will, but the size of returns will be slightly softer."

However, Anglo Platinum currently hosts a dividend yield worth 7.55% , meaning it would need a calamitous cut to no longer be attractive. Therefore, we believe Anglo American Platinum Limited stock will still present a top-tier dividend profile even if its dividend payout recedes.

{kind=link}

At a price-to-book ratio of 1.87x , one could argue that Anglo American Platinum Limited is fairly valued. Nevertheless, investors must consider that this stock has historically traded with elevated price-to-book ratios. As a matter of fact, Anglo Platinum's price-to-book ratio is currently sitting at 7.9 times below its cyclical average.

Final Word

Although it may seem that Anglo American Platinum Limited has the world's problems on its doorstep, we think it can deal with the headwinds it faces.

The company's broad-based production has slumped recently amid persistent Eskom issues, which has restricted refinery outputs. Although we do not anticipate improvements at Eskom, it is likely that the market has priced the worst of it all.

The Polokwane smelter could arrive online soon, and there could be a tradeoff between PGM prices and lower regional production, simultaneously phasing out much of Anglo Platinum's top-line risk. Moreover, persistently strong grades delivered instills confidence in our bullish outlook of the company's production.

Anglo Platinum will likely pay softer dividends this year. Nevertheless, the firm's dividend could remain in the upper percentile of the broader stock market.

Lastly, according to its price-to-book ratio, Anglo American Platinum Limited is undervalued relative to its cyclical average, providing us with an additional premise to reiterate our bullish outlook.

- We assign a Buy rating, down from our previous Strong Buy .

For further details see:

Anglo American Platinum: Don't Get Spooked (Rating Downgrade)