AGPPF - Anglo American Platinum Q3 Production Results Assessed

2023-10-24 14:03:10 ET

Summary

- Anglo American Platinum Limited's latest quarterly production report revealed glitches in short-term production, leading to a sharp drawdown of its stock.

- Infrastructure issues relating to water stoppages impacted the company's refinery operations in Rustenburg.

- The weak price environment for platinum group metals poses a challenge for Anglo American Platinum, but a technical price recovery isn't out of the equation.

- Anglo American Platinum valuation metrics and dividend yield seem alluring. However, we urge investors to consider the metrics in tandem with the company's fundamentals.

Anglo American Platinum Limited ( ANGPY ) aka Amplats released its latest quarterly production results on Tuesday morning, revealing additional glitches in short-term production, which led to a sharp drawdown of its stock.

Instead of providing an opinion on price discovery, today's article functions as an update of Amplats' latest production report. Moreover, our outlook on Amplats' fundamentals and its valuation metrics is provided to assist investors with their holistic analysis of the stock.

Let's traverse into the main analysis.

Production Update

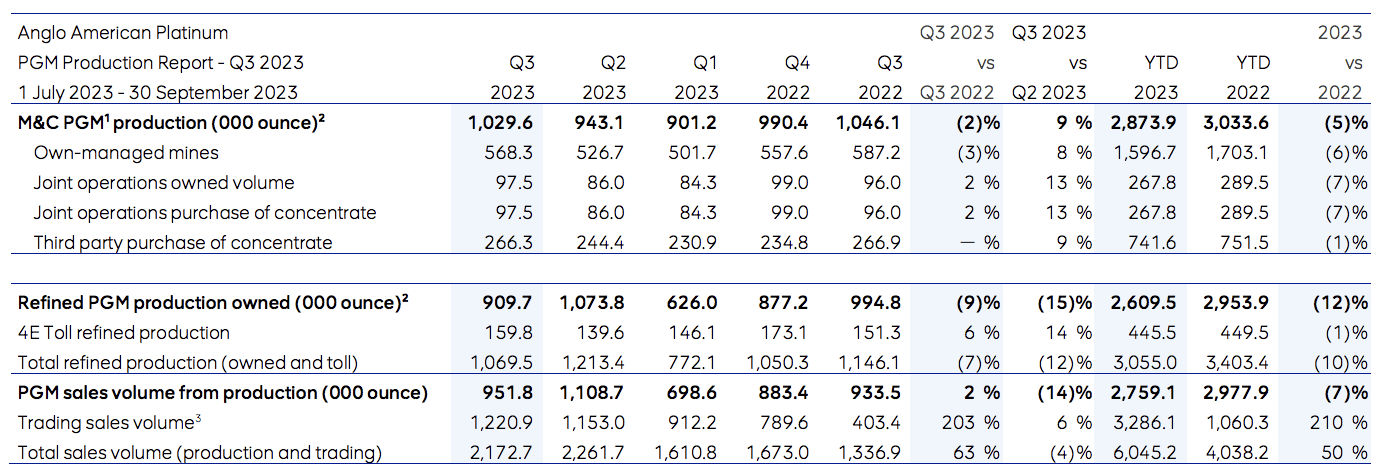

Anglo American Platinum's third-quarter production report disappointed, as communicated by the stock's sharp drawdown in U.S. pre-market trading.

In a similar fashion to its previous quarters, Amplats suffered from regional infrastructure issues that led to a 2% slump in platinum group metals ("PGM") mining production and a 9% fall in refinery output. Moreover, Amplats' Nickel and Copper production slumped by 5% and 21% , respectively, following the same trajectory as its PGM operations.

{kind=link}

Infrastructure

As discussed in one of our previous articles about Amplats, South Africa's Eskom electricity curtailment led to significant headwinds. However, in a change of events, unexpected municipal water stoppages were the culprit in Amplats' third quarter.

The water stoppages stemmed from overflowing manholes and sewage blockages in Rustenburg that especially influenced Amplats' midstream facilities. At Pearl Gray, we have a low level of confidence that matters will be resolved in an orderly manner, which we base on anecdotal experience and Rustenburg's municipal track record, which yet again delivered a poor audit report earlier this year.

On a positive note, Amplats' Eskom headwinds seem to have calmed down.

According to the firm, merely 5000 PGM announced were deferred to future production due to load curtailment, and based on our experience, load curtailments have certainly eased since earlier this year. Moreover, municipal strikes seem to be coming to an end, which might improve Eskom's production function.

Sure, Eskom's long-term woes remain; however, slight improvements may be priced by stock market participants.

Throughput

Anglo American Platinum's Mogalakwena mine suffered from lower throughput in Q3, resulting in a 3% year-on-year decrease in production, with 568 200 ounces delivered in the quarter.

The Amandelbult complex delivered 184 900 ounces, translating into a 4% year-on-year decrease. However, despite the year-on-year decrease, production increased by 25% quarter-on-quarter. Lower grades were of concern here, while the complex's Dishaba mine suffered from poor ground conditions.

Throughput is difficult to predict. Therefore, I'm not going to tell you that we know what Amplats' mines will deliver in the coming quarters. All I can add here is that Mogalakwena and Amandelbult are some of the most sought-after high-grade, low-cost PGM mines in the world, raising the possibility that throughout will settle at desirable levels in the long-term.

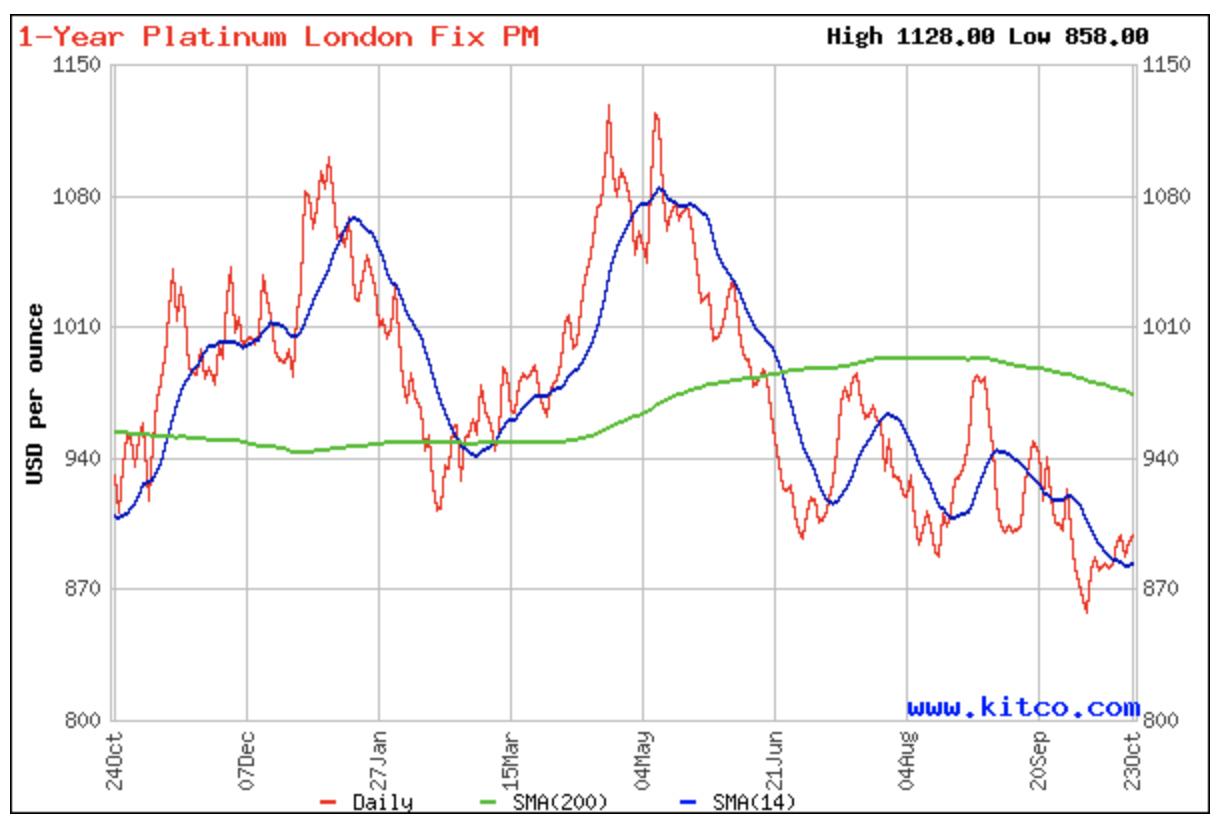

Prices

PGM prices are compressed as global consumer demand has softened year-on-year. PGMs typically struggle whenever the economy is softening due to the effects of disinflation. However, prices are below their moving averages, suggesting a technical mean-reversion may be in store, especially if global interest rates eventually pivot.

{kind=link}

We believe Amplats will need price support from PGMs if it wants its financial results to improve. This may sound trivial; however, I emphasize price realization as regional inflation in South Africa remains above the midpoint target , with input costs stemming from fuel and wages being of particular concern.

Even though miners typically sell their inventory on forward contract prices (instead of spot prices) and hedge a portion of their price exposure, the general trajectory of PGM prices is unappealing at the moment, which is a risk investors should keep in mind going into Q4.

Guidance

Anglo American Platinum left its full-year guidance largely unchanged, stating the following in its report.

We are on track to meet our production and unit cost guidance. Metal-in-concentrate (M&C) PGM guidance for 2023 is 3.6 - 4.0 million PGM ounces, and refined PGM production guidance is 3.6 - 4.0 million PGM ounces. Unit cost per PGM ounce produced is anticipated to be at the upper end of the range considering foreign exchange rate volatility, load-curtailment, and continued inflationary pressure. Guidance for unit cost per PGM ounce produced is R16,800 - R17,800.

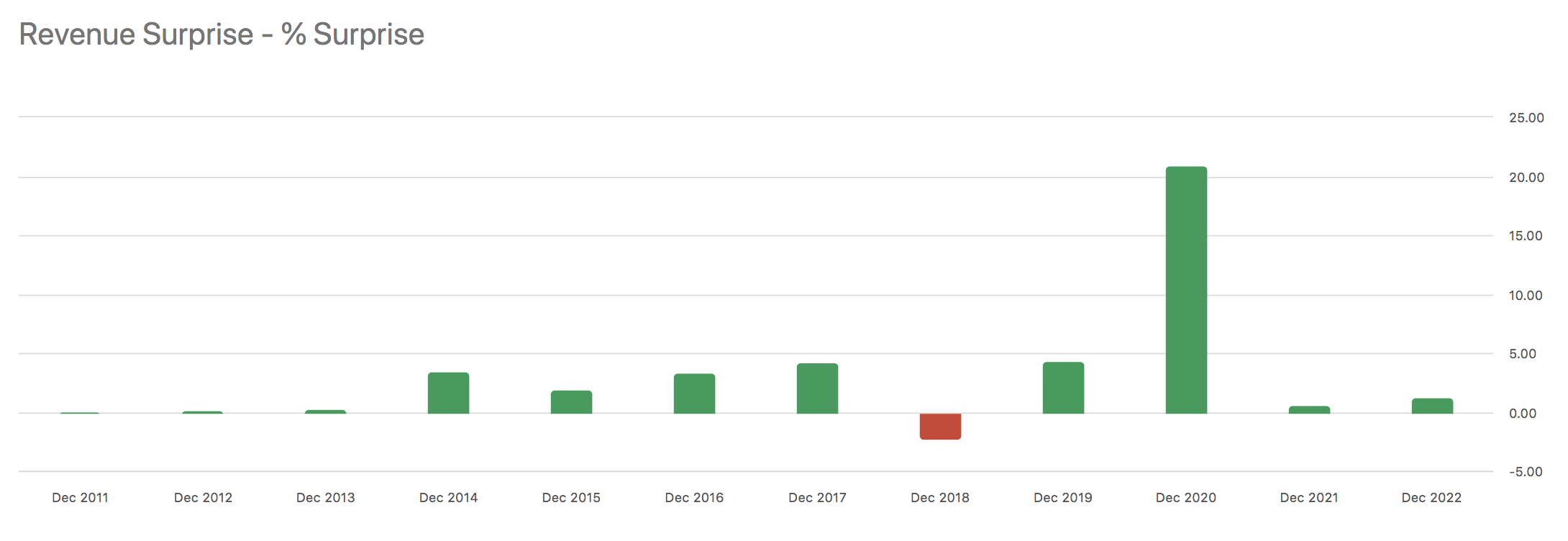

Although not a direct comparison to production, I extracted the accuracy of Amplats' past earnings guidance to illustrate that it usually guides its earnings within a realistic range. However, investors should consider that current socio-economic matters in South Africa are volatile, meaning surprises can arise at any given moment.

{kind=link}

{kind=link}

Valuation Metrics & Dividends

A glance at Anglo American Platinum's price multiples suggests its stock is at a crossroads. Firstly, I believe it can be reasonably stated that the stock's dividend yield of 7.35% is alluring; however, Amplats' price volatility may phase out its dividend benefits.

Furthermore, I think Amplats' price-to-book ratio is slightly higher than most of us would like it to be, especially as year-end impairments could enter the fray due to sustained pressure on PGM prices and resilient interest rates.

Lastly, Amplats' price-to-earnings ratio of 5.6 looks respectable if considering that it is at a 59.93% sector discount. However, the question becomes whether earnings growth will surface in this stage of the economic cycle.

| Metric |

| Value |

| Price-Earnings |

| 5.6 |

| Price-Book |

| 1.73 |

| Dividend Yield |

| 7.35% |

Source: Seeking Alpha.

Final Word

Anglo American Platinum Limited's third-quarter production report displayed disappointing results, echoing the structural issues embedded in South African municipalities and the weak price environment for platinum group metals.

However, the firm maintained its full-year guidance, which could be met with a technical price recovery of PGM metals.

Lastly, the stock's price multiples and dividend yield both look good after Amplats' year-over-year drawdown. Nevertheless, we encourage investors to consider the risks of a value trap induced by the economic cycle.

For further details see:

Anglo American Platinum Q3 Production Results Assessed