AGPPF - Anglo American Platinum: Some Concerns Over ICE Volumes

2023-06-12 13:48:41 ET

Summary

- While most companies connected to automotive focus on the current situation of pent-up demand, ANGPY is being a little more honest in its outlook.

- While Platinum is seeing a unique demand uplift from renewables and hydrogen, Palladium is more connected to autocatalyst demand.

- With newer cars being richer with Palladium, recycling is going to grow supply on top of pressures on automotive demand that they expect after 2023.

- Supply is pretty tight due to supply and energy shortage issues in South Africa, and that is supporting PGM prices, but Palladium is still expected to go into some surplus.

- Realistically, the party has to be stopping soon for automotive given the credit situation.

Anglo American Platinum ( ANGPY ) continues to be a great way to get exposure to a low-cost operational miner in PGMs. There's still a compelling case for the PGM renewable thesis, particularly for Platinum which stands to gain the most from the green agenda, but the issue is that the conditions in automotive markets are still pretty important for the business on the demand side. The supply side conditions look favourable, but ANGPY is sounding the alarm on itself around automotive demand - not this year but next. Overall, the stock remains an interesting speculative choice but the time isn't right. We would wait for the opportunity for automotive demand to exhaust pent-up demand from the semiconductor shortages first before taking stock.

Dynamics

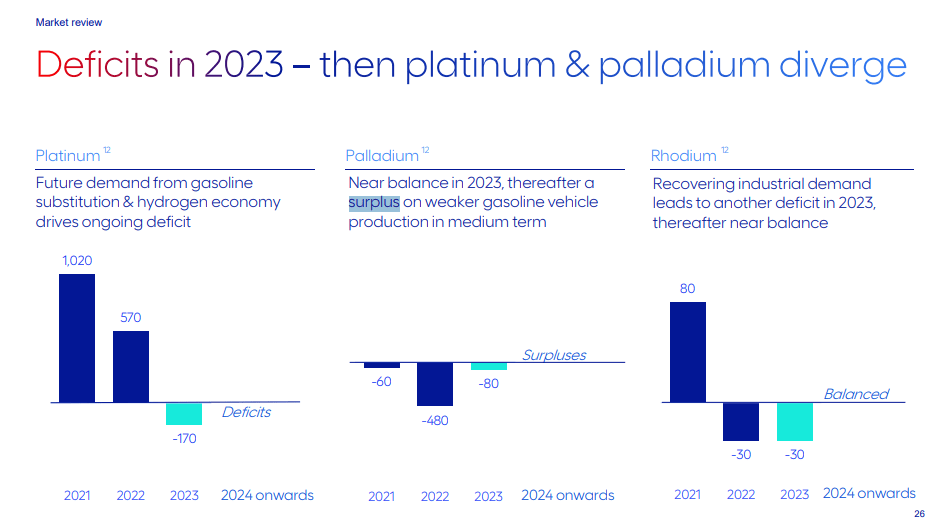

Ultimately, ANGPY depends on PGM prices being high. Really only two commodities matter, Palladium and Platinum. Platinum has recently gained a real needle-moving industrial application in the hydrogen economy. Palladium could be similarly important for hydrogen energy , but its main use case and the decider for its price and demand lies in automotive.

As a baseline, the S/D dynamics are not too bad because with all these resources being mined to a large extent in South Africa, general issues with infrastructure, namely electricity, is making it harder to operate at full utilisation. Commodities are flowing slower from mines. With further renewable development and future demand for hydrogen, it's expected that Platinum should have a pretty good S/D situation.

{kind=link}

For Palladium, things are different. It depends on automotive demand a lot, and while rising emission standards in places like China have been helpful, the West is stepping over into the BEV camp. For 2023, there is the expectation that the continued pent-up demand situation caused by the semiconductor shortages will continue to keep Palladium in deficit, but after that it will be in surplus. ANGPY forecast this on the basis of just the fact that BEV are gaining production share, but with the credit concerns in the interim, and just the simple fact that higher interest rates will affect automotive demand, surplus Palladium may come sooner rather than later, and affect ANGPY's EBITDA meaningfully as their commodity basket falls more than expected in price. There is the added issue that the new cohorts of scrapped cars are more rich with Palladium to be recycled, creating a larger backflow of recycled materials onto the market.

Bottom Line

PGM prices have held up pretty well, but it was thanks in part to the massive pop that happened in early 2022 around the Ukraine invasion. We speculated on Palladium at that time . The average FY 2022 levels were buoyed but things have gotten worse in Palladium prices.

Cash costs are rising as electricity becomes more of a bottleneck for SA operations, and general inflation is pushing things too. Growing volumes back to pre-COVID levels are an offset. Still EBITDA is down around 33%, and it is likely going to get worse as average prices decline.

ANGPY trades with a 5-6x PE on run-rate profits which does consider the fact that declines in the commodity can already be observed ahead of the H1 2023 report. Profits are going to decline a good deal more. However, the dividend is variable, and ultimately ANGPY remains a game of figuring out how the market has appraised the downward trajectory. An average smoothed-out multiple for mining is around 8x . A repeat performance of 2022 in terms of EBITDA declines brings you back to fair. Markets have likely assumed such a decline until the multiple reset to a more reasonable level. It's anyone's guess whether this will make money in the short term. In the long-term, there is more promise around hydrogen developments, although we have some doubts about its viability . It's a hold at these prices.

For further details see:

Anglo American Platinum: Some Concerns Over ICE Volumes