APO - Another Smashing Quarter For Apollo And How Long It Will Remain So Cheap

2023-11-14 00:53:02 ET

Summary

- Apollo delivers strong Q3 results with growth in fee-related earnings and spread-related earnings.

- The market undervalues Apollo due to struggles in valuing Athene, its retirement specialist subsidiary.

- Athene plays a leading role within Apollo, with its unique business model and strong alignment with third parties.

Apollo Global Management ( APO ) has delivered another outstanding quarter. We will shortly review it and focus on possible explanations of why shares are still so cheap. Having described APO many times in my previous publications, I will only remind you that the company consists of an alternative asset manager Apollo ("old Apollo") generating primarily fee-related earnings ("FRE") and some carry (carry and investment income combined constitute the so-called Principal Investment Income or PII segment), and retirement specialist (or insurer or annuity provider) Athene that generates spread-related earnings ("SRE"). While technically Athene belongs to the life insurance industry, it does not underwrite any life business.

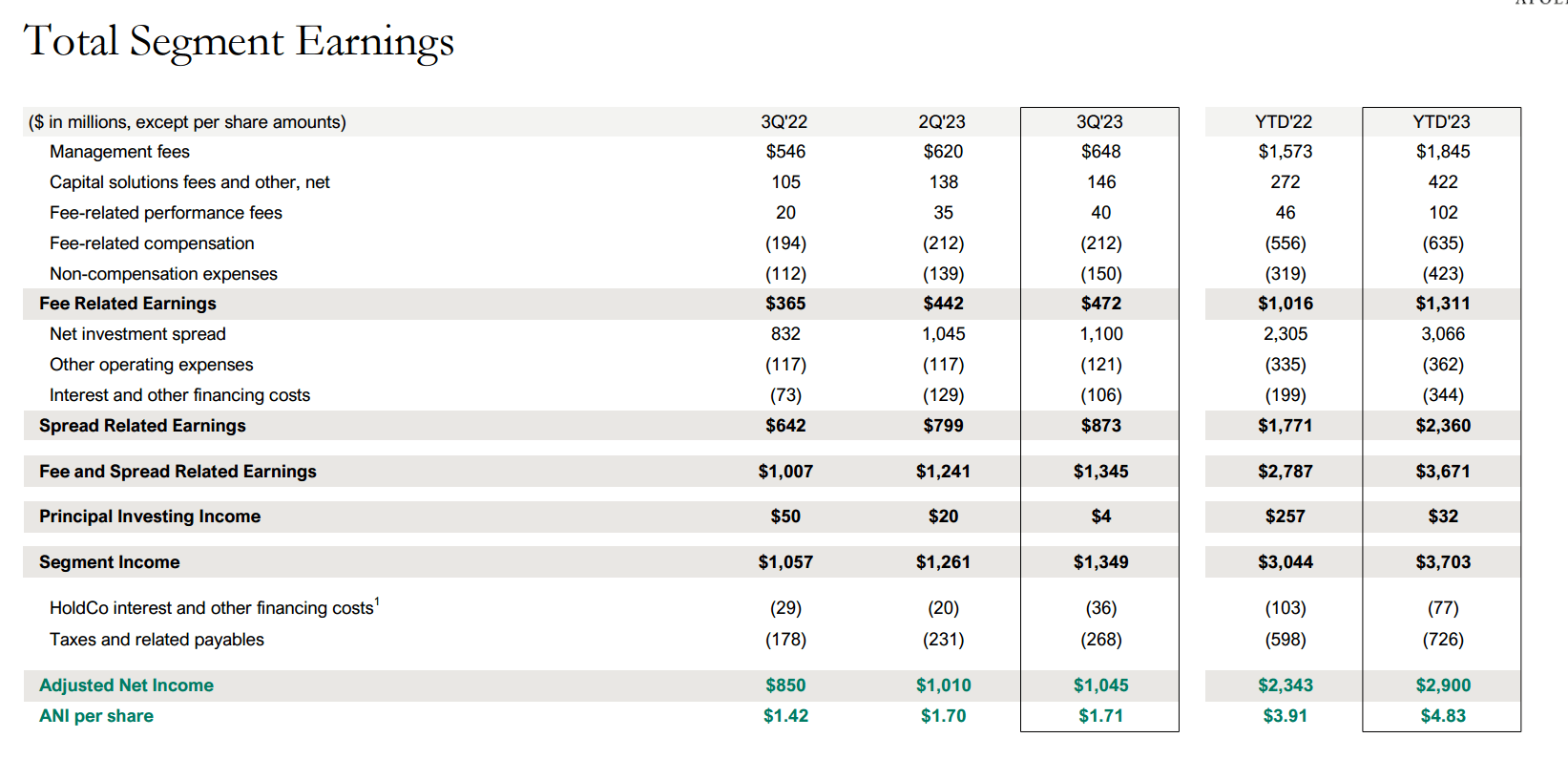

Q3 2023

APO's Q3 results were not unexpected but amazing nevertheless:

{kind=link}

FRE grew 29% vs. Q3 2022 by both growing fee-generating assets under management ("FGAUM") from $394B to $468B and expanding margins. Yield (or credit) FGAUM captured the lion's share of this growth and reached $386B. Of those, $261B is on Athene's gross balance sheet.

SRE grew at an even more impressive 36%. Less valuable PII was minuscule since Apollo, in sync with other alternative managers, delayed exiting private equity positions due to an unfavorable market environment.

The key non-GAAP metric for the company is adjusted net income ("ANI") per share. It grew at about 20% from $1.42 to $1.71. This number would have been more impressive unless Apollo issued convertible preferred stock which increased the share count. This issuance, however, will be highly beneficial for shareholders in the long run as additional capital supports incredible Athene's growth.

We will skip many other positives for the quarter. To finish this section, I will forecast Apollo's results for the year. Assuming that Q4 numbers will be similar to Q3, we can expect the following for the full 2023:

- pretax FRE ~ $1,783M

- pretax SRE ~ $3,233M

- after-tax ANI per share ~ $6.54

Valuations

At the time of writing, APO is trading at a P/ANI~84/6.54~12.8 multiple. For a big company growing at 20%+, this is surprisingly cheap. Beyond reasonable doubt, the market is struggling with valuing Athene.

What multiples Mr. Market is assigning to Athene right now? Two of Apollo's asset-light peers - Brookfield Asset Management ( BAM ) and Ares ( ARES ) define FRE similarly to Apollo and represent the best comps. Other alt managers are either asset-heavy, less established (like Blue Owl ( OWL )), or define FRE differently (BlackRock's (BLK) FRE is not comparable to Apollo's FRE). BAM trades at ~ 25 FRE multiple, while Ares is more expensive. Over the last 3-4 quarters, BAM's FRE has been rather static, while APO's FRE kept climbing quickly. It follows that APO's FRE should be valued at 25x at least.

Disregarding insignificant and lower-worth PII, one could contend that Apollo's multiple (12.8) ought to match the weighted average of FRE and SRE multiples, with the weights being FRE and SRE respectively. By solving this straightforward equation, we get the following:

- SRE multiple is equal to 5.9 provided FRE multiple is 25

In other words, Mr. Market currently values Athene at ~ $15.1B. Since Athene's book value, ex-AOCI was $19.1B at the end of Q3, the market values Athene at ~0.8 of its book value. This is very unassuming for a company producing 15%+ ROE for many years without missing a beat.

Both P/ANI and P/BV are in line with how the life insurance industry is generally valued today. The best comp for Athene is arguably F&G Annuities & Life ( FG ), which is trading at similar valuations. However, ROE for F&G is close to only 10% with lots of accounting noise.

Investors appear to fail to differentiate Athene from other industry players while, in our opinion, it deserves it. I explain it by specific risks that investors assign to Athene's relatively new business model. Before we consider them, I will further elaborate on Athene.

Athene's role within Apollo

What I say next may surprise many of my readers: within Apollo, it is Athene who plays the leading part. The asset manager serves Athene and not the other way around. This is a rather strong statement that emphasizes Apollo's uniqueness. I will put forth several arguments to articulate the message.

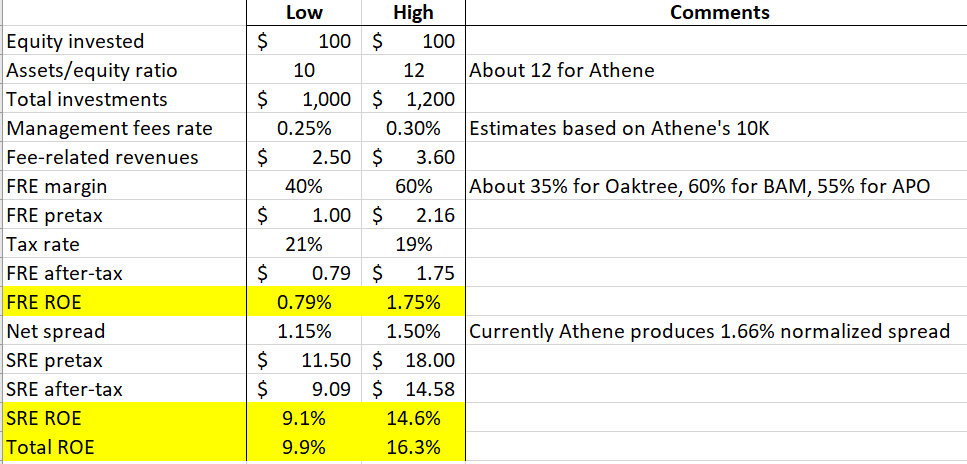

Please take a look at the table below that simplistically describes Athene's model.

{kind=link}

The table shows how $100 in Athene's equity generates both SRE and FRE. Since FRE and SRE are generated within the same company, one can argue that profit partition into SRE and FRE is artificial. We will revisit this point of view later.

Of $468B of FGAUM, $208B is on Athene's net balance sheet directly. But the latter figure grossly underestimates Athene's input. The key to understanding Athene's real role is a slogan often repeated by CEO Marc Rowan: "Athene wants 25% of everything and 100% of nothing."

Roughly speaking, Athene's humongous balance sheet consists of 3 components: traditional bonds and cash, investment grade private credit originated by Apollo/Athene internally, and various alternative assets (including credit-originating subsidiaries themselves) put together by Apollo. Two latter components are differentiators expanding Athene's spread.

Taken literally, Marc Rowan suggests that Athene intends to own only 25% of these differentiators with the remaining 75% going to third parties and thus generating FRE without committing any capital. Athene's participation introduces the strongest possible alignment with various third parties and makes these differentiators credible and desirable. Apollo targets Athene-related FGAUM 2-3 times higher than Athene's QUICKLY GROWING net invested assets. In other words: asset-heavy Apollo strives to become less heavy with time.

So far, it has been about intentions. But what is going on in practice? The short answer is "a lot" and I will outline several important developments:

- ADIP is Apollo's acronym for third parties replicating Athene's investments in proprietary private credit (sidecar in insurance lingo). When Athene purchases Apollo-originated private credit, a fraction of it (the target is 40%) is funded by ADIP with the balance by Athene. For the privilege to invest side-by-side, Athene charges small fees on top of Apollo (these fees show up in Athene presentations as strategic management fees). Today, about $53B of FGAUM is funded by ADIP.

- Athora is a private European retirement specialist that follows Athene's strategy (it has existed for only 5 years and you can think of it as Athene 10 years ago). Athene owns less than a quarter of Athora but Apollo manages its investment portfolio. Athora adds $49B of FGAUM and is quickly growing (a short digress: in my previous post, I made a small mistake describing Athora. The company contacted me immediately and requested a correction which I promptly delivered. They are following!).

- Apollo's recent fund, AAA, is designed primarily for retail investors, although institutional capital is also accepted. It consists of the same alternative assets that Athene had invested in for many years. Now they are consolidated into a fund with Athene being just one of the investors. You can invest in it on par with Athene. Apollo asserts that the fund yields returns comparable to or slightly surpassing the index, all while maintaining lower volatility. AAA growth is approaching $500 million per quarter.

- Catalina and Venerable are two private reinsurers partly funded by Athene with a lower cost of capital. Their investment portfolios are managed by Apollo. From time to time, Athene cedes less profitable parts of its book to these reinsurers to free capital that can be invested more profitably.

This is not a complete list of Athene-inspired and/or Athene-based developments. Today, FGAUM just from Athene, ADIP, and Athora combined comprise $310B of $468B in total.

And now we are getting back to our logical path: if Athene is valued so cheaply, there might be some specific risks accounting for it.

Risk #1: unusual assets

I was concerned with this issue for a while and perhaps, other investors also feel certain discomfort regarding it.

Insurers invest primarily in high-grade bonds. This is understandable as portfolios are funded mostly by float, i.e. money that has to be eventually paid out to clients and customers. It is not a place to take risks.

Departing from this tradition, Athene invests big chunks of its fixed-income portfolio in high-grade private credit (fixed-income replacement in Apollo's lingo). While these investments are structured as investment grade, they are different from bonds, and to the best of my knowledge, no other insurer had tried it before Athene at least at this scale. Can something go wrong?

These thoughts kept bothering me until I figured out a very simple thing: while insurers had not tried it before, banks did! Fixed-income replacement is not different from traditional bank loans. In fact, Apollo's originators are nothing else than groups of bankers doing what all bankers do - lending money. There is nothing new here! The practice has passed the test of time.

Banks have the liberty to invest in both public bonds and private loans but long ago they discovered that loans are safer and more profitable. Athene confirms their conclusions. Its credit losses are minuscule and they mostly happen in bonds rather than loans.

Except for isolated cases of reckless lending, banks' problems are typically caused by funding illiquid long-term loans with short-term liquid deposits. Depositors can quickly withdraw money but banks cannot quickly liquidate their loans.

In this regard, Athene has a big advantage. Its funding through annuities is illiquid and long-term as well. As long as assets and liabilities match in duration and mass surrenders do not happen, Athene is safe.

I have previously delved into the topic of mass surrenders in my earlier posts and won't revisit it here. Nevertheless, it's crucial to observe that this risk is not exclusive to Athene but pertains to all life insurers. Consequently, it cannot be used to rationalize the comparative valuations of Athene.

Risk #2: fees on Athene's assets

I have already mentioned that some investors can consider FRE generated from Athene's assets as an expansion of SRE. Since the market assigns materially lower multiples to SRE vs. FRE, it makes Apollo less valuable.

I think this argument is flawed because of three reasons. First, it implies that an insurer can have an internal group engaged in credit originations and other activities that are very specific for alternative asset managers. I am not aware of such examples and do not think it is possible due to the task complexity and scale required.

Secondly, Apollo's fees are transparent, disclosed in Athene's filings, and do not exceed industry standards. For example, they are in line with what Blackrock charges F&G. The merger between Apollo and Athene did not affect these fees, and Athene's after-fees performance remains outstanding.

Finally, we have an example of asset-light Brookfield Asset Management that charges fees on its parent Brookfield Corporation ( BN ) in a less transparent fashion. It does not prevent BAM from trading at ~25xFRE which is the multiple we used for Apollo's FRE.

Risk #3: Bermuda Triangle

Of all Athene-specific risks, I am least comfortable with this one though it is not straightforward.

First of all, Athene's filings are very detailed in stark contrast with the filings of, say, Brookfield's Bermuda-based subs. I have read plenty of Athene's filings and they are on par or even more detailed than the filings of US-based insurers. The slide below illustrates the point.

{kind=link}

But why does Athene need Bermuda at all? Taxation is unlikely the main reason. Most of Athene's profits are taxed in the US and Apollo's overall tax rate is 20%, not very different from the statutory 21%. So taxes may play a marginal role at best.

Athene's Bermuda reinsurers are not empty shells as most of its equity is stationed there together with ADIP (for ADIP, funded in part by foreign capital, tax considerations are very important). Athene's Bermuda reinsurers together with ADIP reinsure US annuities transferring ultimate liabilities out of the US. Many insurers are doing the same thing but Athene uses its captive reinsurers instead of third parties.

One might suspect a case of regulatory arbitrage though Apollo denies it. I have read a lot about this issue and still cannot provide you with a clear explanation of what is going on. I still think that Bermuda domicile allows Athene to use its capital more efficiently but cannot pinpoint the details. In general, it means that Bermuda's accounting and regulatory rules require less surplus from an insurer (vs. the US) to support the same liabilities.

Is it a material risk? I guess not immediately but would not bet my house on it. But since we are dealing with the pensions of millions of US retirees, this issue may easily become politically charged.

Conclusion

Concerning our discussion of Athene-specific risks, I would like to remind you that insiders hold about one-third of APO shares. This indicates at least that the management watches Athene's risks very closely but eventually does not guarantee anything.

Taking all factors into consideration, it appears more likely than not that APO is undervalued. Are there any catalysts that could trigger rerating?

It seems probable that eventually investors will get more comfortable with Apollo's business model and rerating will happen without specific catalysts. Whether it will happen next quarter or next year, I do not know.

Dividends will be growing but not in leaps. For asset-heavy alt managers, we cannot expect increasing dividends by 20% or so in line with Ares or Owl.

Material buybacks are possible in case shares keep trading at a big discount (modest buybacks happen every quarter). The likeliest source of funding for big buybacks is PII which is now producing next to nothing but can deliver big chunks of cash once the market turns around.

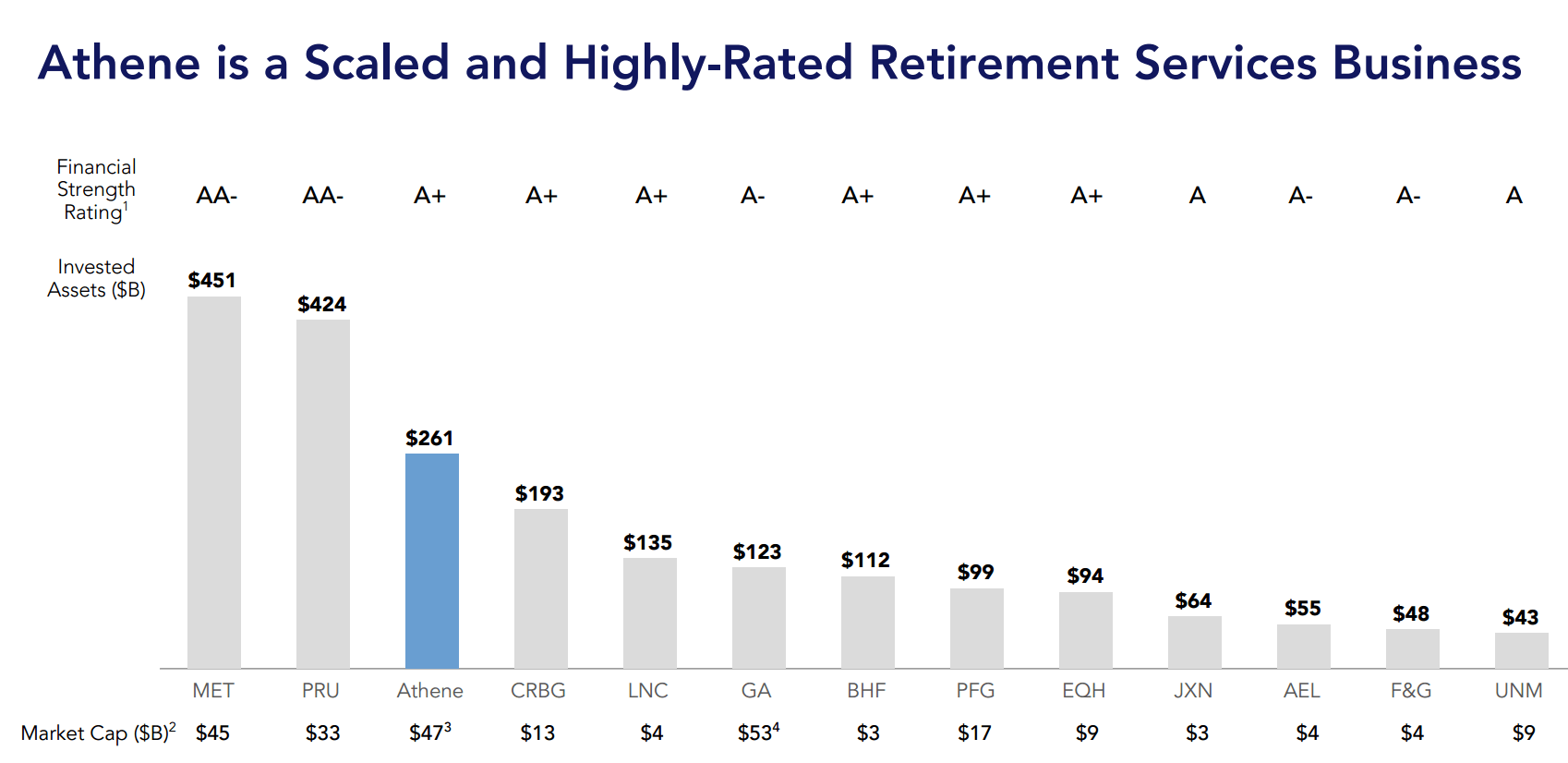

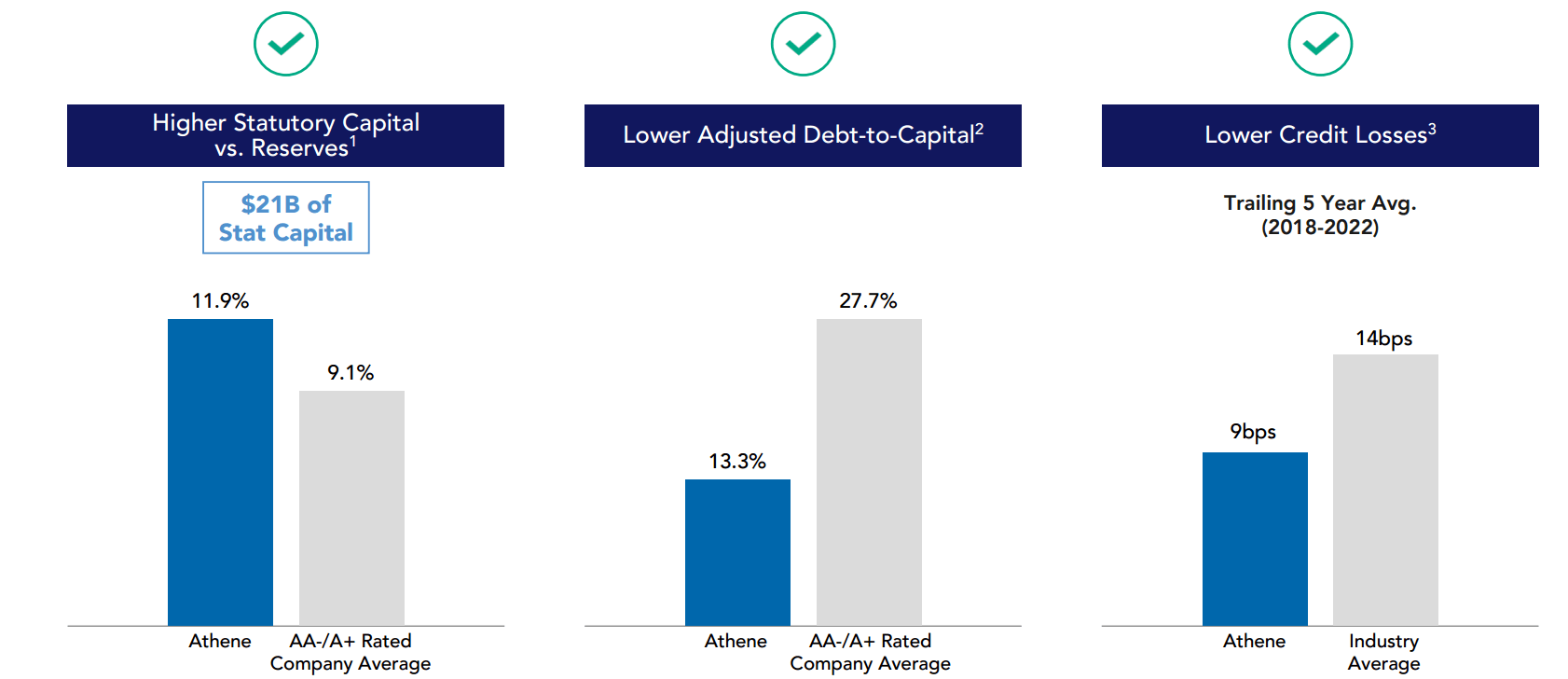

Upgrade of Athene's ratings is another possible catalyst. Please take a look at the landscape of the US life insurance and Athene's capital metrics below.

{kind=link}

{kind=link}

Athene is the third biggest with capital metrics deserving higher ratings, perhaps, in line with MetLife ( MET ) and Prudential ( PRU ). Once one of the rating agencies changes its outlook to positive from neutral, Athene will become more valuable and it may cause a jump in Apollo's shares.

Please note that even without multiple expansions Apollo shares remain attractive due to expected growth. I would still caution my readers to keep total exposure to alt managers in check. Apollo is a big position for me but I would be cautious to buy at dips. The reason? It is primarily the Risk #3.

For further details see:

Another Smashing Quarter For Apollo And How Long It Will Remain So Cheap