REIT - Apartment REITs: A Renter's Market

2024-01-11 09:00:00 ET

Summary

- Apartment REITs were among the weakest-performing property sectors for a second-straight year in 2023 - lagging even the battered office sector - despite delivering another year of mid-single-digit earnings growth.

- Following two years of record-setting rent growth, residential rents decelerated in 2023 alongside a broader cooling of inflationary pressures, with multifamily rents seeing a particularly sharp cooldown amid supply headwinds.

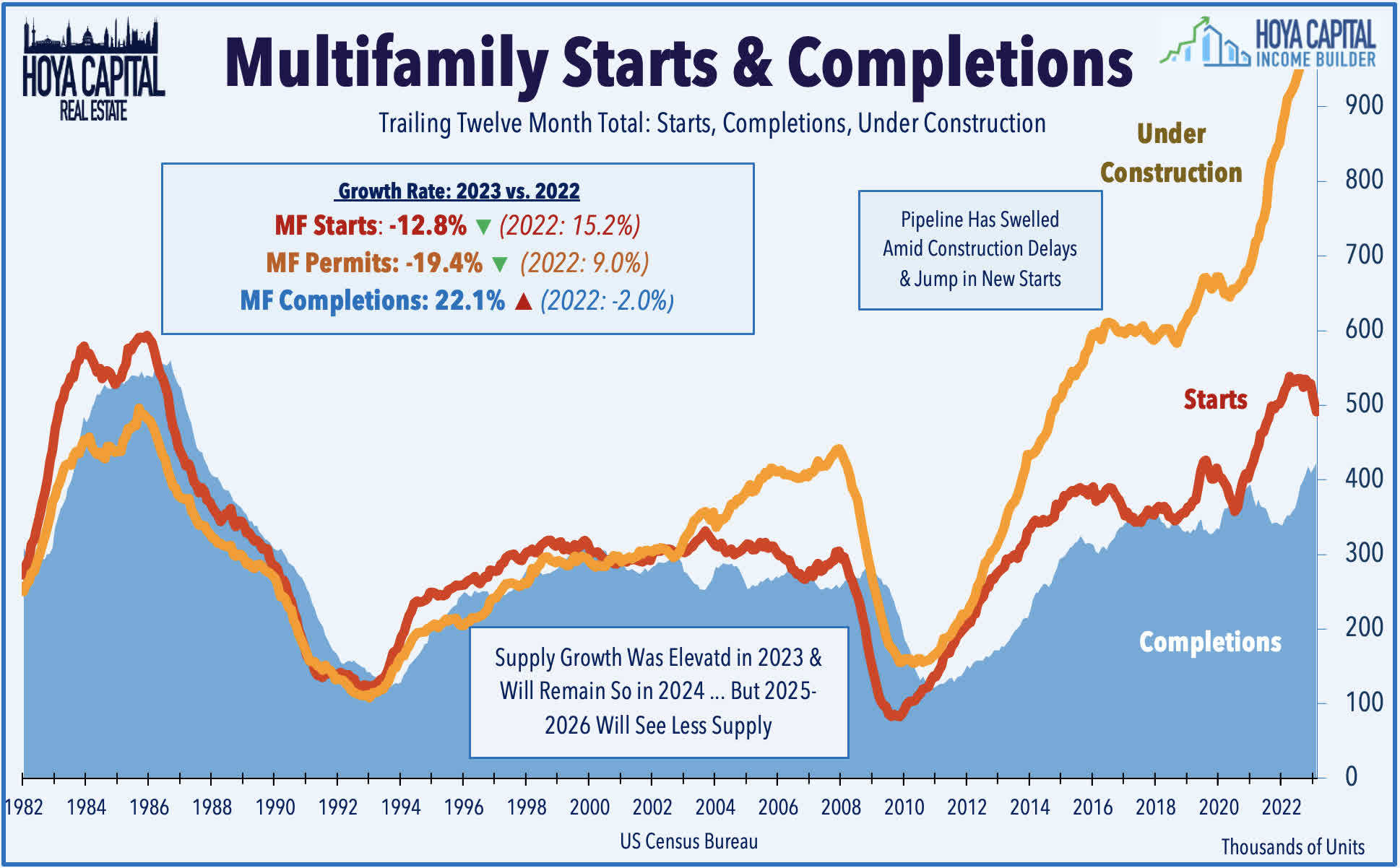

- The wave of pandemic-era development - started at a time when rents were rising double-digits - resulted in a record year of new deliveries in 2023 with similarly elevated supply levels.

- The pundit-predicted rental market "crash" has remained elusive, however, as demand has stayed surprisingly robust, driven by the combination of resilient job growth, homeownership unaffordability, favorable demographics, and elevated inbound immigration.

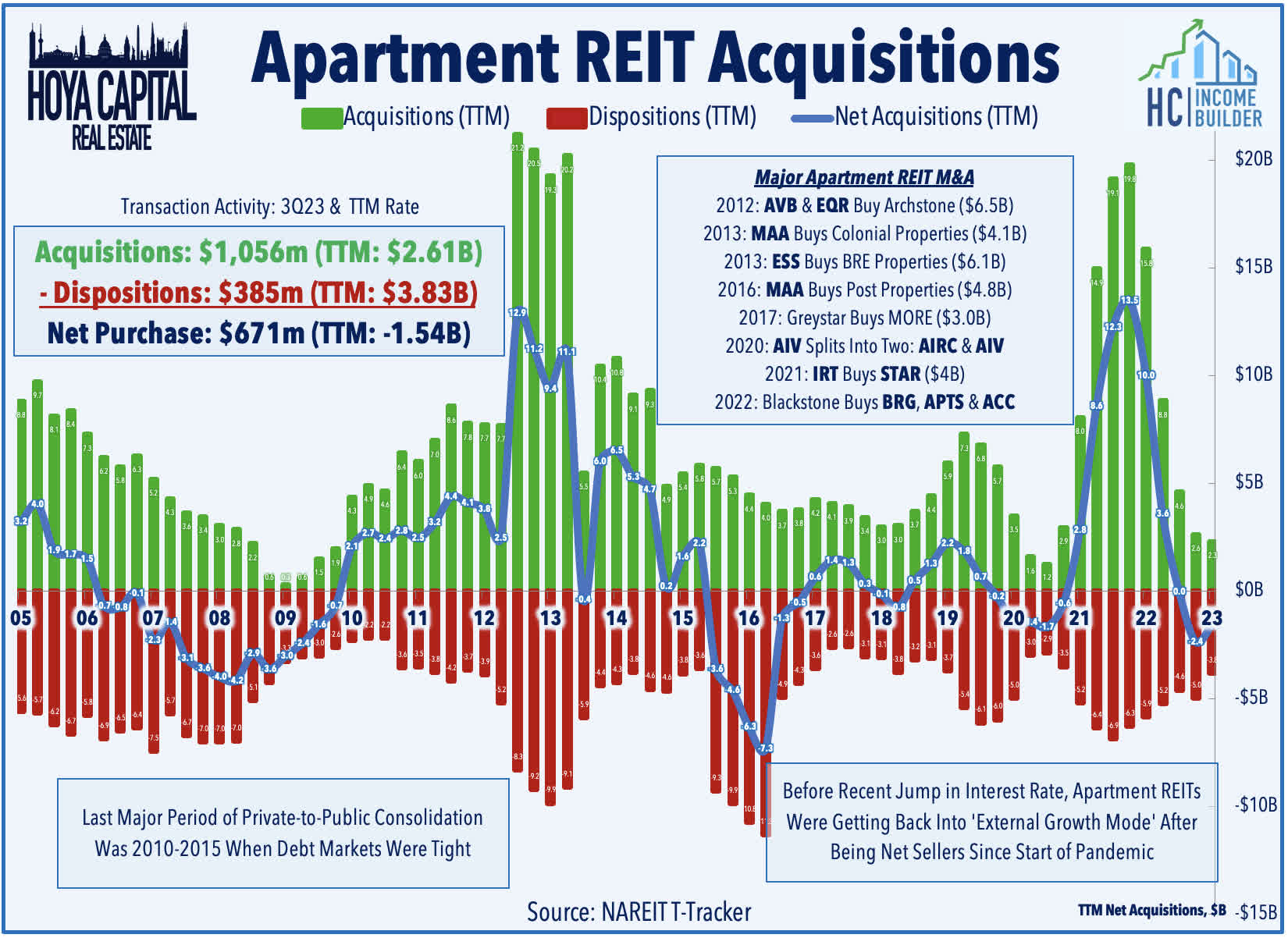

- Pockets of rate-driven distress have remained isolated to the most highly-indebted corners of the private markets, but this distress spells opportunity for well-capitalized REITs. While organic growth will be flat in 2024, conditions are becoming ripe for external growth via acquisitions.

REIT Rankings: Apartments

{kind=link}

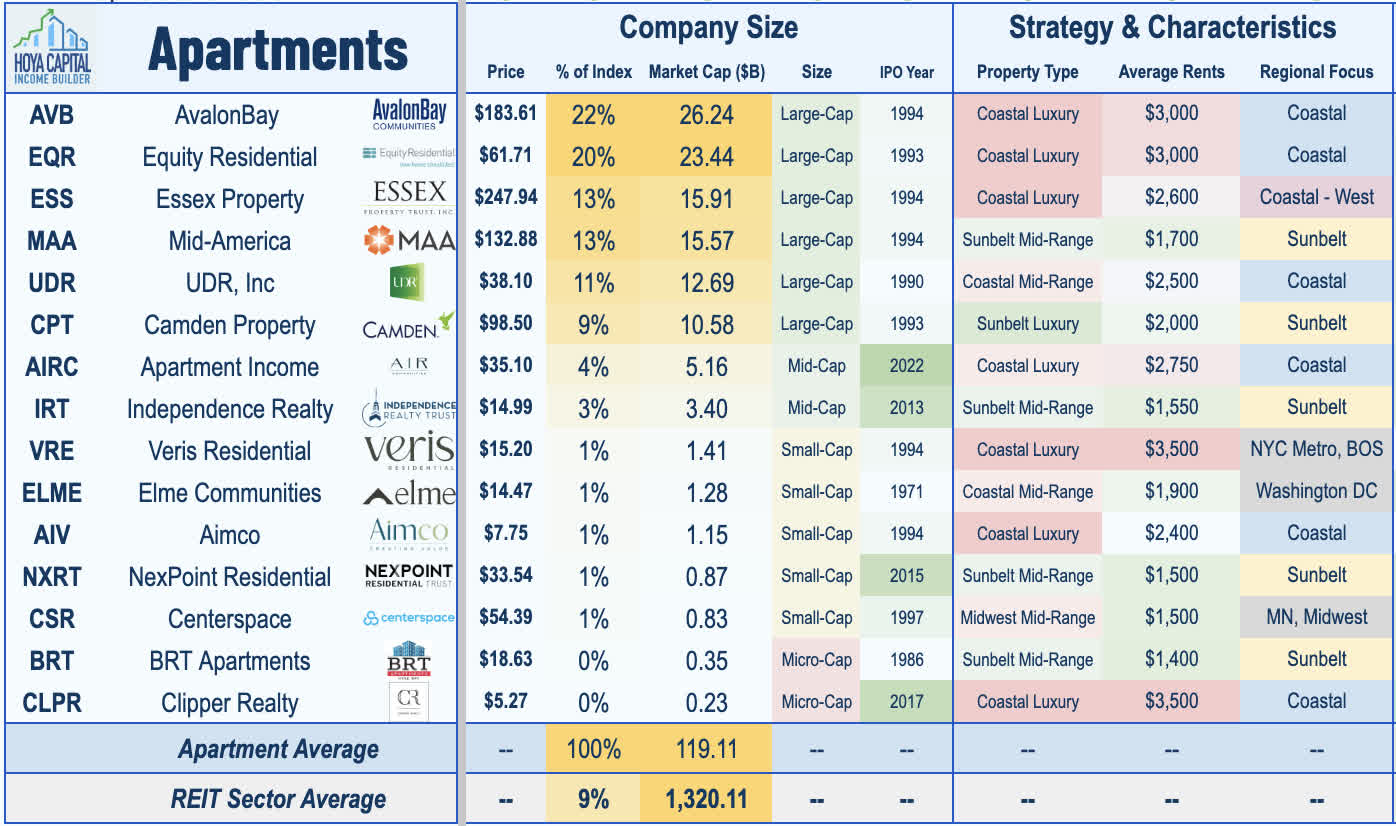

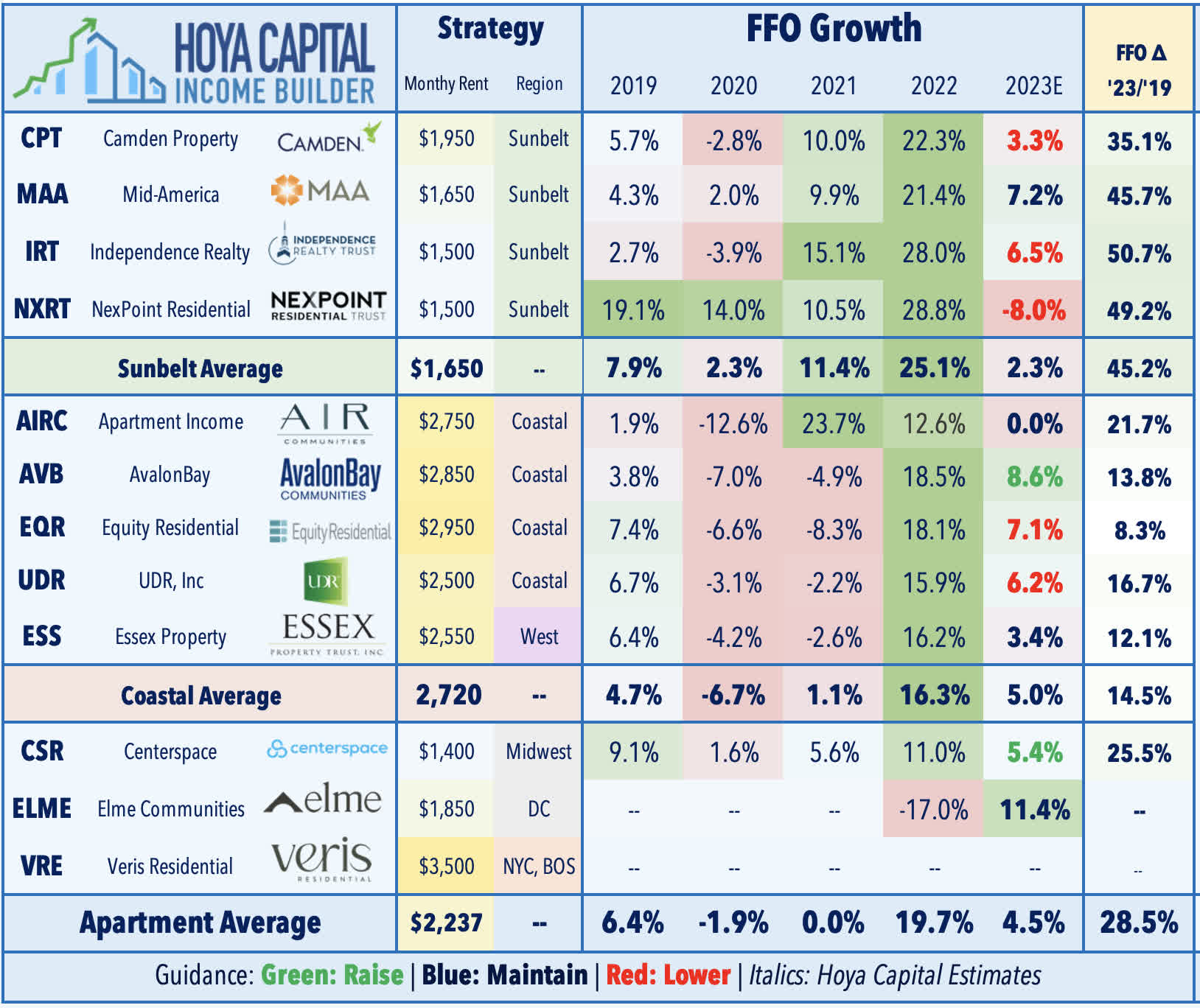

Within the Hoya Capital Apartment REIT Index , we track all fifteen exchange-listed U.S. apartment REITs, which collectively account for roughly $120B in market value and comprise about 10% of the Equity REIT Index. These apartment REITs collectively own roughly 600,000 rental units, representing a relatively modest 2.5% market share of the 23 million apartment units across the United States. Apartment REITs skew their exposure towards the upper tiers of the market, with nearly all of these REITs reporting average rents that are above the national average of around $1,350 per month. One of the longest-tenured property sectors, Apartment REITs have evolved into "fully-integrated" owners and operators of multifamily communities and have become some of the most active multifamily homebuilders in the country.

{kind=link}

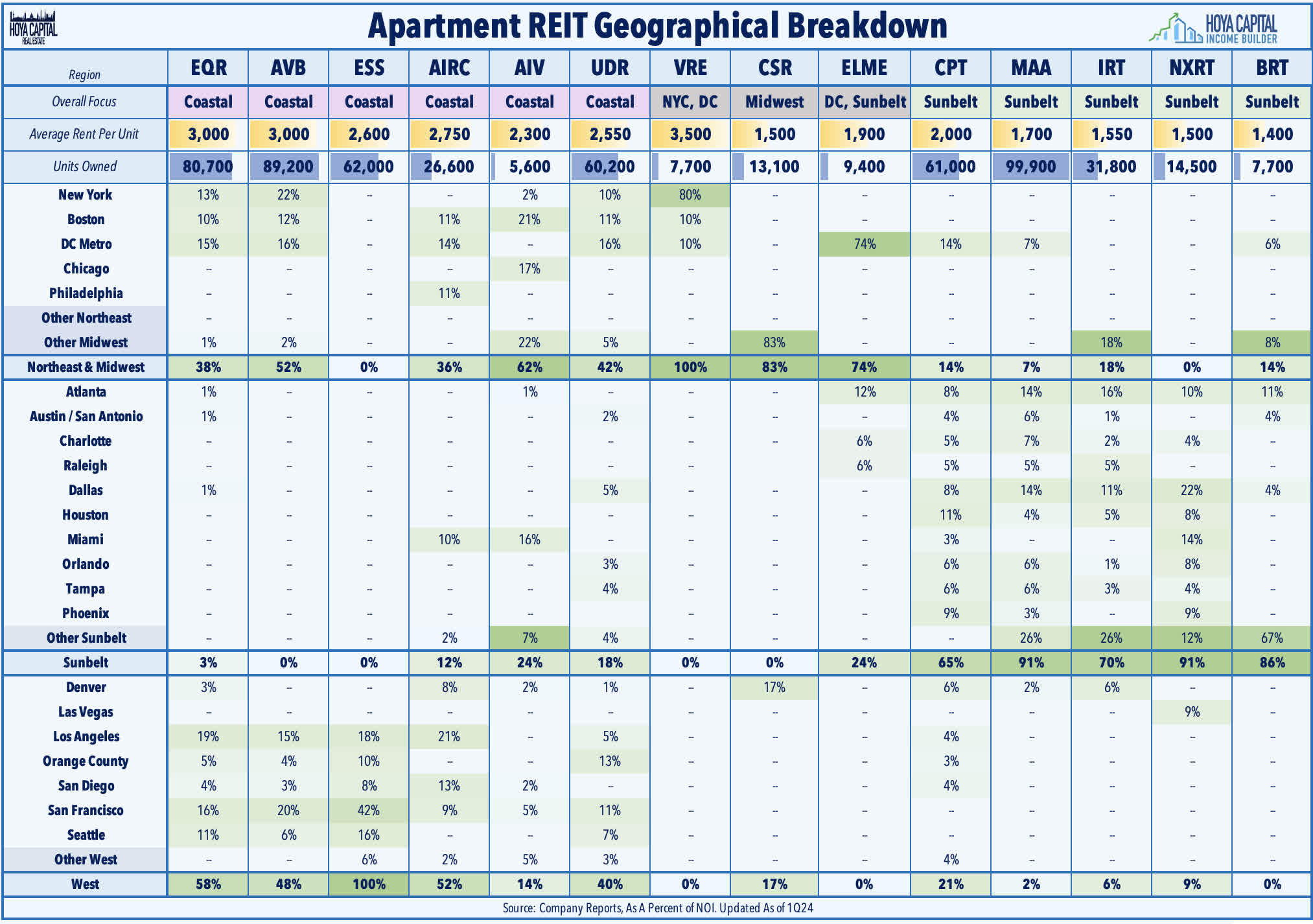

Given the importance of market-level scale for efficient residential property management, apartment REITs tend to adopt a geographic focus. Larger apartment REITs typically adopt a regional focus - which we split based on a Coastal and Sunbelt divide - while smaller apartment REITs typically focus on a handful of individual markets. The major Coastal REITs include Equity Residential ( EQR ), AvalonBay ( AVB ), Essex ( ESS ), UDR ( UDR ), and Apartment Income ( AIRC ), while the major Sunbelt-focused REITs include Mid-America ( MAA ), Camden ( CPT ), Independence Realty ( IRT ), and NexPoint Residential ( NXRT ). One apartment REIT - Centerspace ( CSR ) focuses primarily in Midwest and Mountain West markets. Several of the newer apartment REITs are even more geographically concentrated. Veris Residential ( VRE ) - formerly Mack Cali - derives around 80% of its revenues from the New York City metro region, while Elme Communities ( ELME ) - formerly Washington REIT - operates almost exclusively in Washington, DC.

{kind=link}

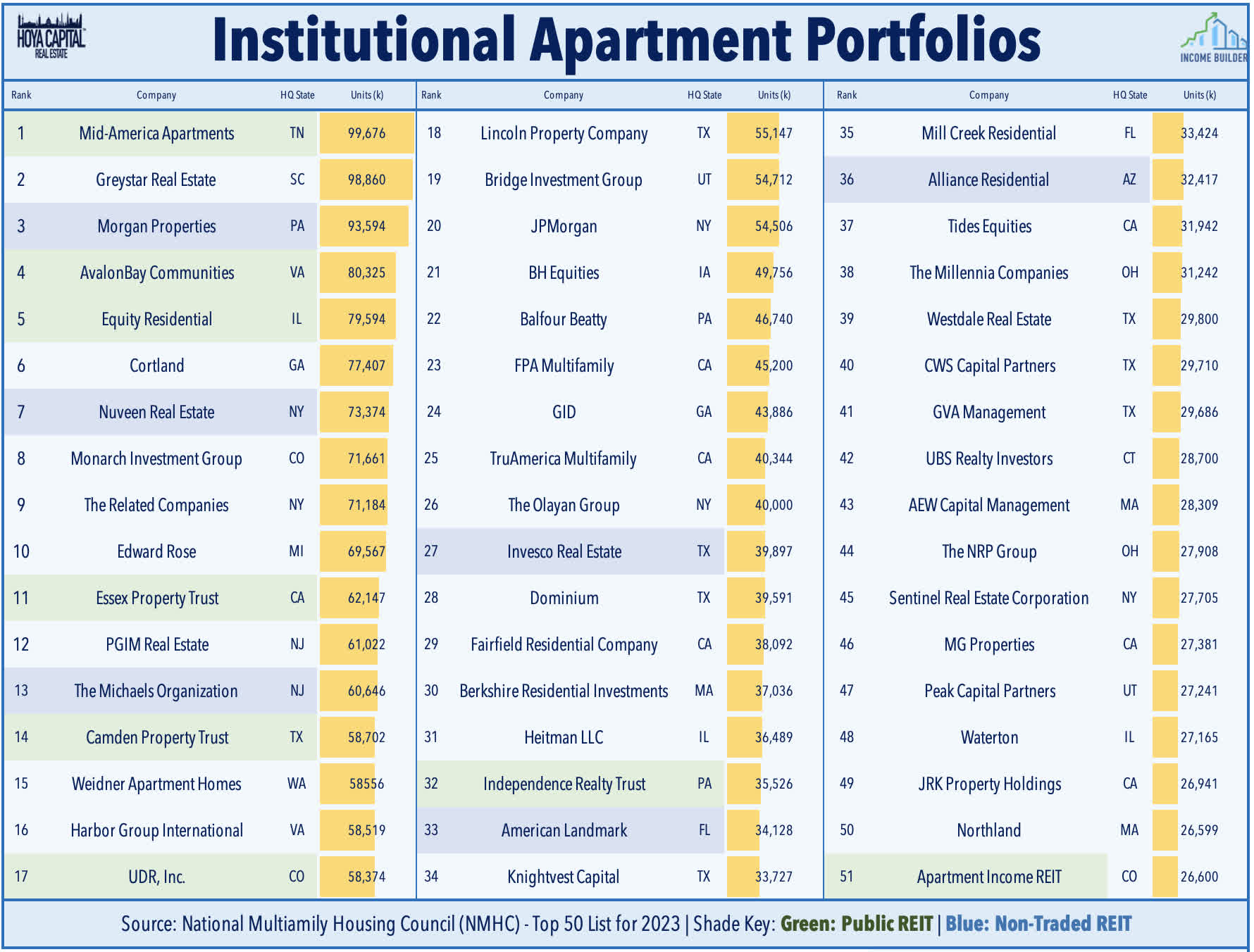

The apartment sector is among the most "fragmented" real estate property sectors. Of note, only 3 of the top 10 largest apartment owners tracked by the National Multifamily Housing Council ("NMHC") are public REITs. As with single-family rentals, there exist dozens of large-scale private equity institutional owners of multifamily properties with portfolios of 10k or more units, hundreds more "family office" investors with portfolios of 1-20k units, and many thousands of "mom and pop" investors with portfolios ranging from 10 to 1,000 units. Major private equity players in the space include Greystar, Morgan Properties, Courtland, Nuveen, Monarch Investment, Related Companies, Edward Rose, PGIM, Michaels Organization, and Weidner Apartment Homes. While we saw few private-to-REIT IPOs over the past decade during the period of ultra-low interest rates and plentiful access to cheap private debt, the new higher-rate conditions are more ripe for public REITs to finally regain market share from their private peers.

{kind=link}

Apartment REIT Fundamentals

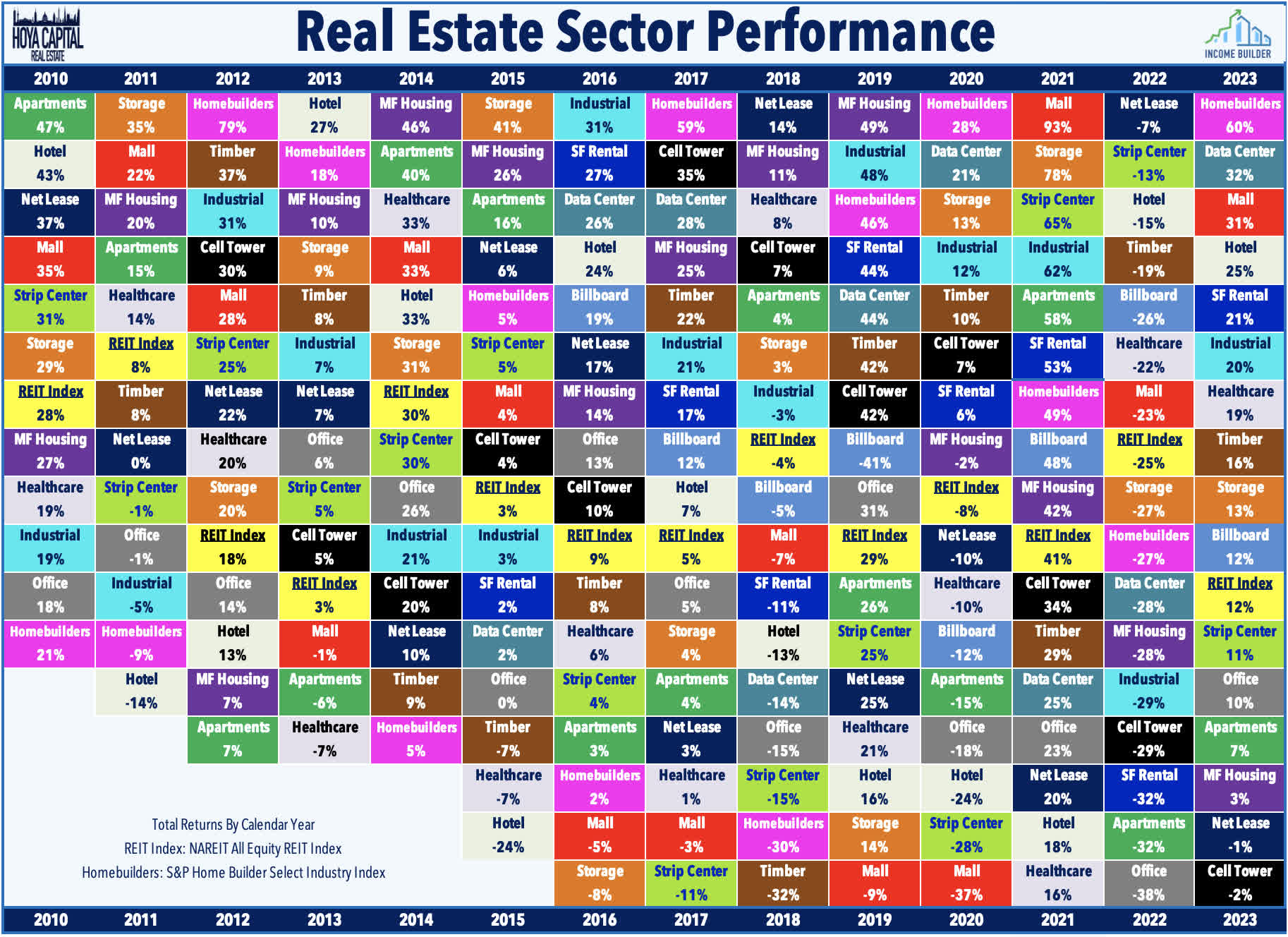

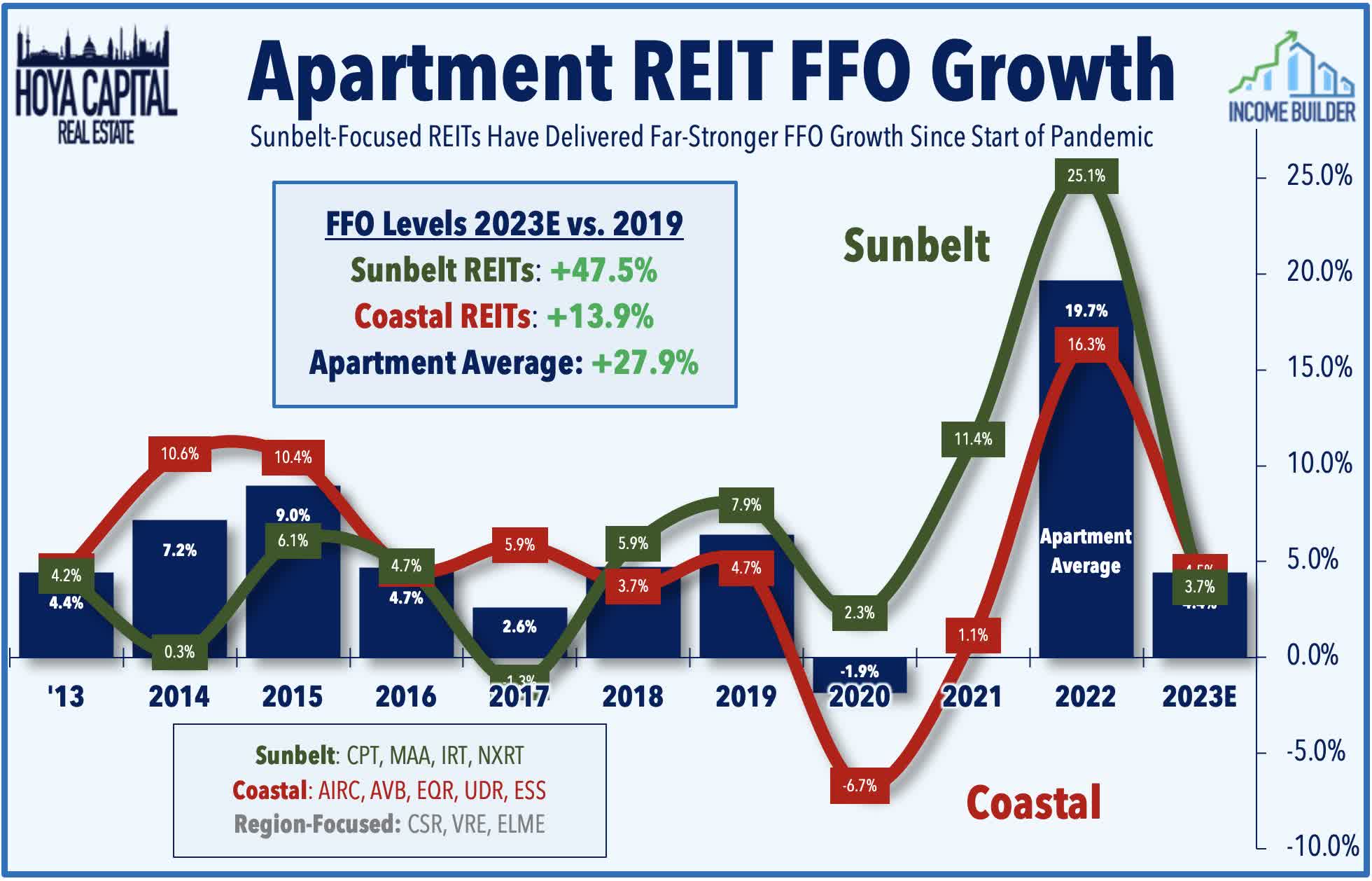

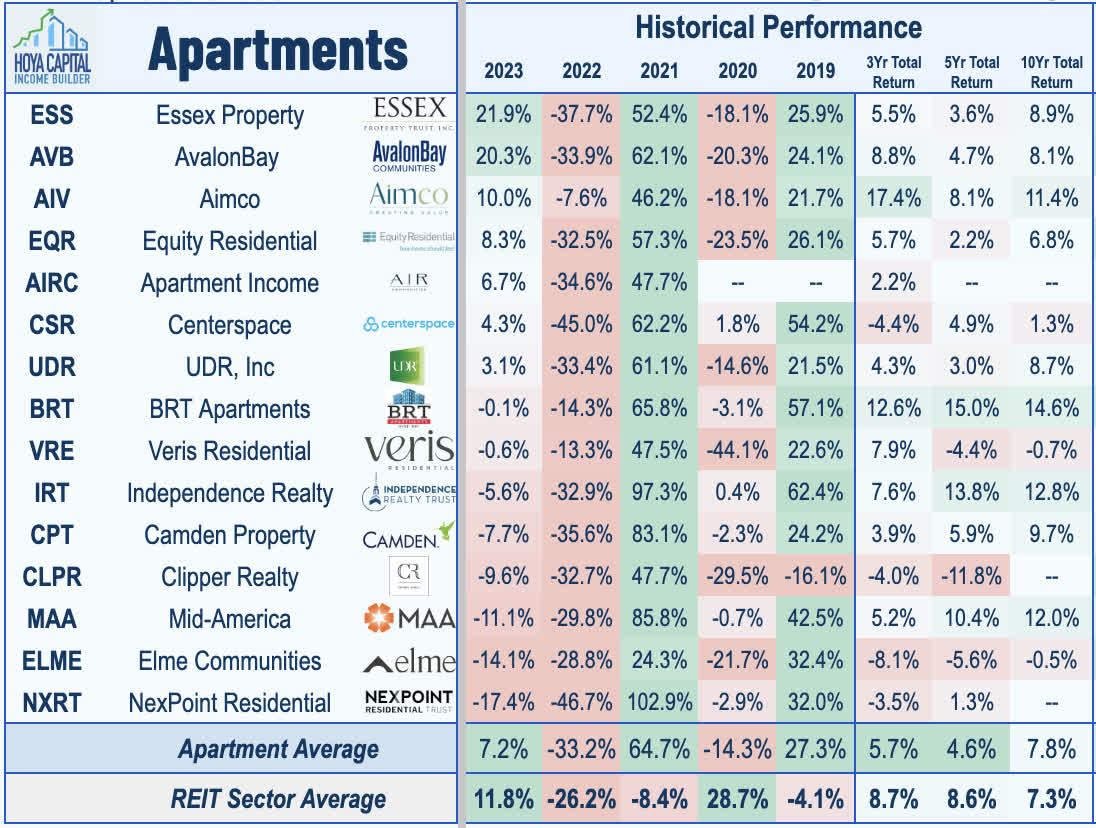

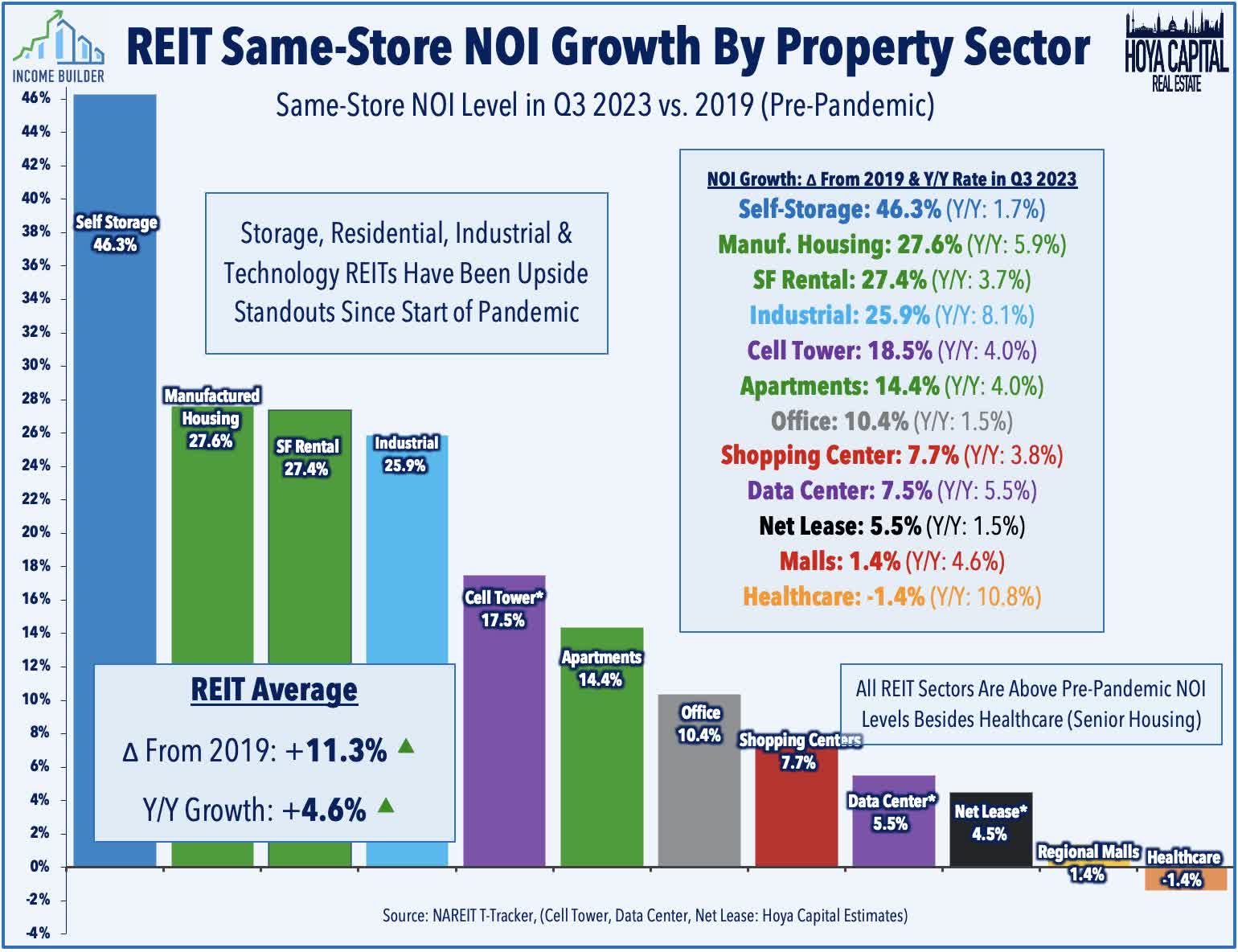

Apartment REITs were among the weakest-performing property sectors for a second-straight year in 2023 as residential rents decelerated following two years of record-setting growth. The Hoya Capital Apartment REIT Index - a market-cap weighted benchmark of these fifteen REITs - produced total returns of 7.2% in 2023, which lagged the 11.8% total returns of the broad-based Vanguard Real Estate ETF ( VNQ ) and the 26.2% returns from the S&P 500 ( SPY ). This followed a rough year for apartment REITs in 2022, in which the Apartment REIT Index dipped over 30%. Remarkably, these two years of underperformance came amid two otherwise impressive years of earnings growth: Apartment REITs reported average FFO growth of 20% in 2022 and are on-pace to record 5% growth in 2023 based on recent guidance.

{kind=link}

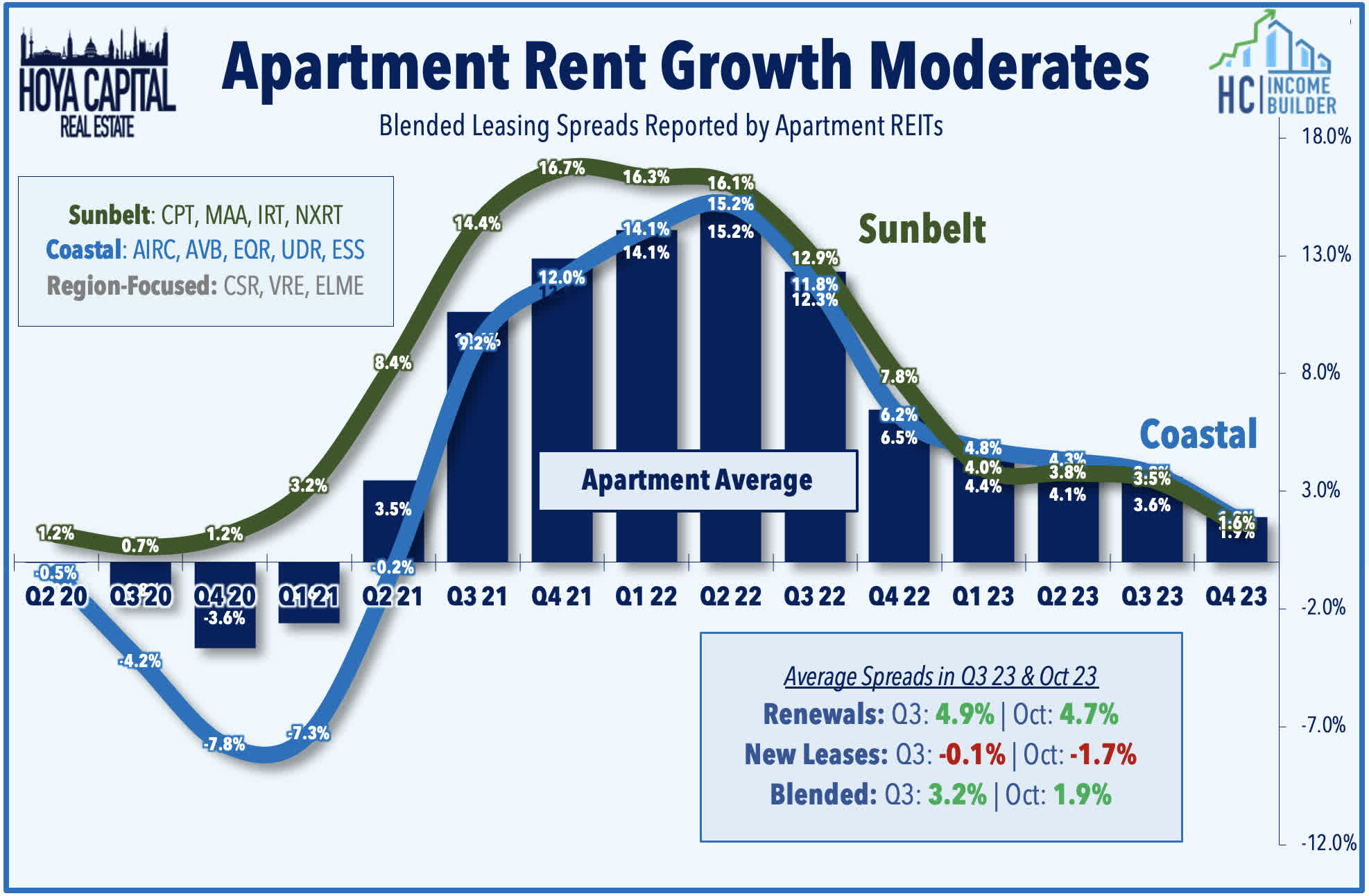

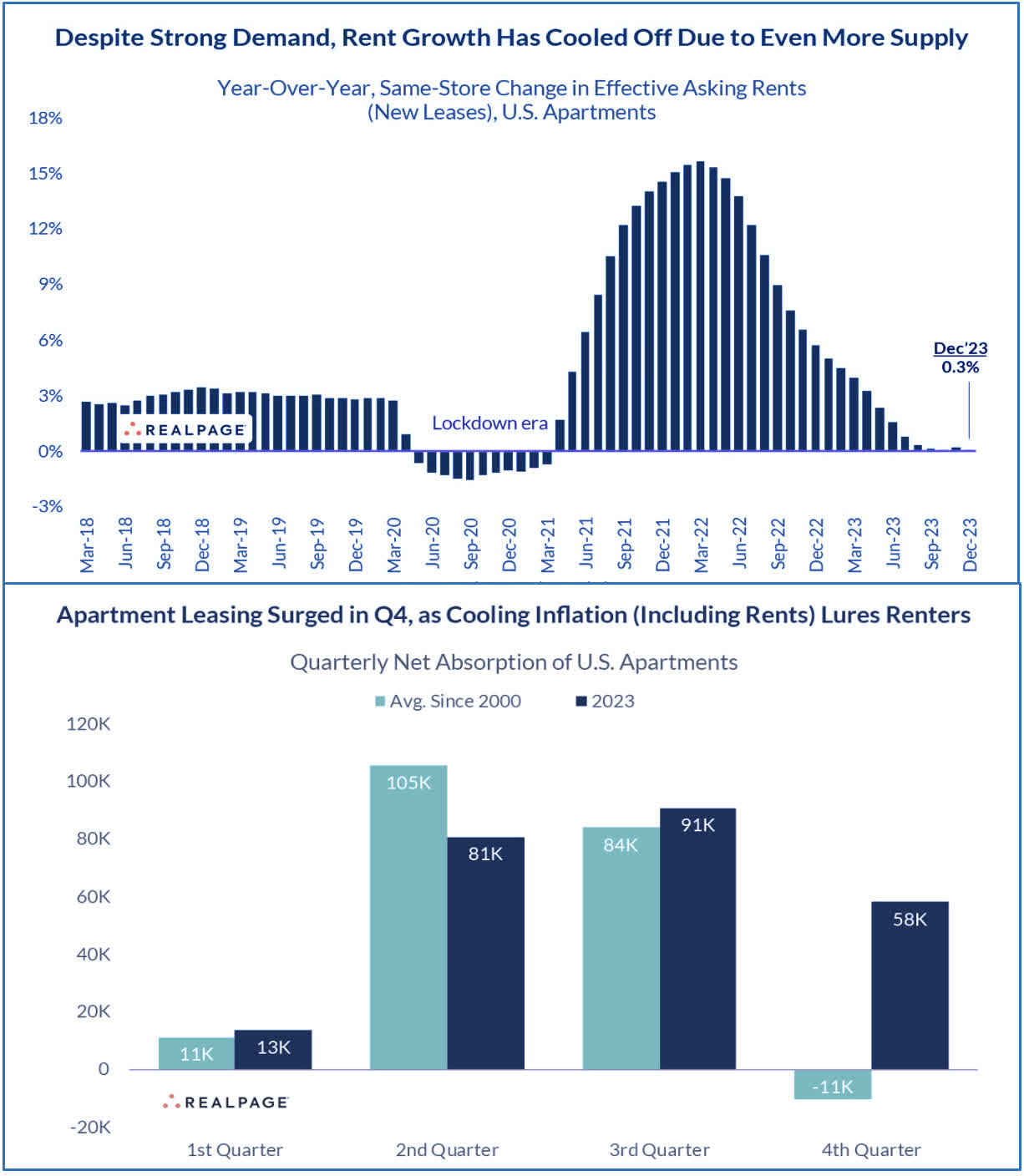

While market valuations still indicate that investors haven't given up on the "hard landing" narrative, recent data and forecasts from the leading multifamily data providers point to a steady normalization in rent growth and a modest uptick in vacancy rates back towards historical averages, but not the outright steep declines in rental rates that are currently being seen in prices off other pandemic-affected commodities and goods. The pundit-predicted rental market "crash" has remained elusive as demand has stayed surprisingly robust, driven by a combination of solid job growth, homeownership unaffordability, favorable demographics, and elevated inbound immigration. These trends are evident in the latest Apartment REIT earnings reports, which showed that blended rent growth slowed to around 2% in the final months of 2023, down from the record-setting growth of over 15% in mid-2022. Of note, however, renewal rent growth has remained relatively healthy at around 5%, which has helped to offset the increased concessions on new leases.

{kind=link}

These reports were broadly consistent with the trends seen across the plethora of rent reports provided by the major brokerage and data firms. RealPage - an apartment software provider that provides rent pricing services to a sizable percentage of the industry - reported last week that apartment completions jumped to 36-year-highs in 2023 with nearly 440 apartments delivered, but demand was "surprisingly" strong in the fourth quarter with net absorption of 58.2k units - the third-strongest 4th quarter in 25 years - bringing the full-year total to 234k units, which was similar to pre-COVID norms. Supply still outpaced demand for the year, resulting in an uptick in occupancy to 94.1% (still within the typical pre-COVID range of 93-95%), and a slowdown in rent growth to just 0.3% for full-year 2023, which was the second-weakest year since 2009. Importantly, RP data shows that rent growth is no longer decelerating, however, holding in the 0-1% year-over-year range since July following a swift deceleration from double-digit peaks in 2022.

{kind=link}

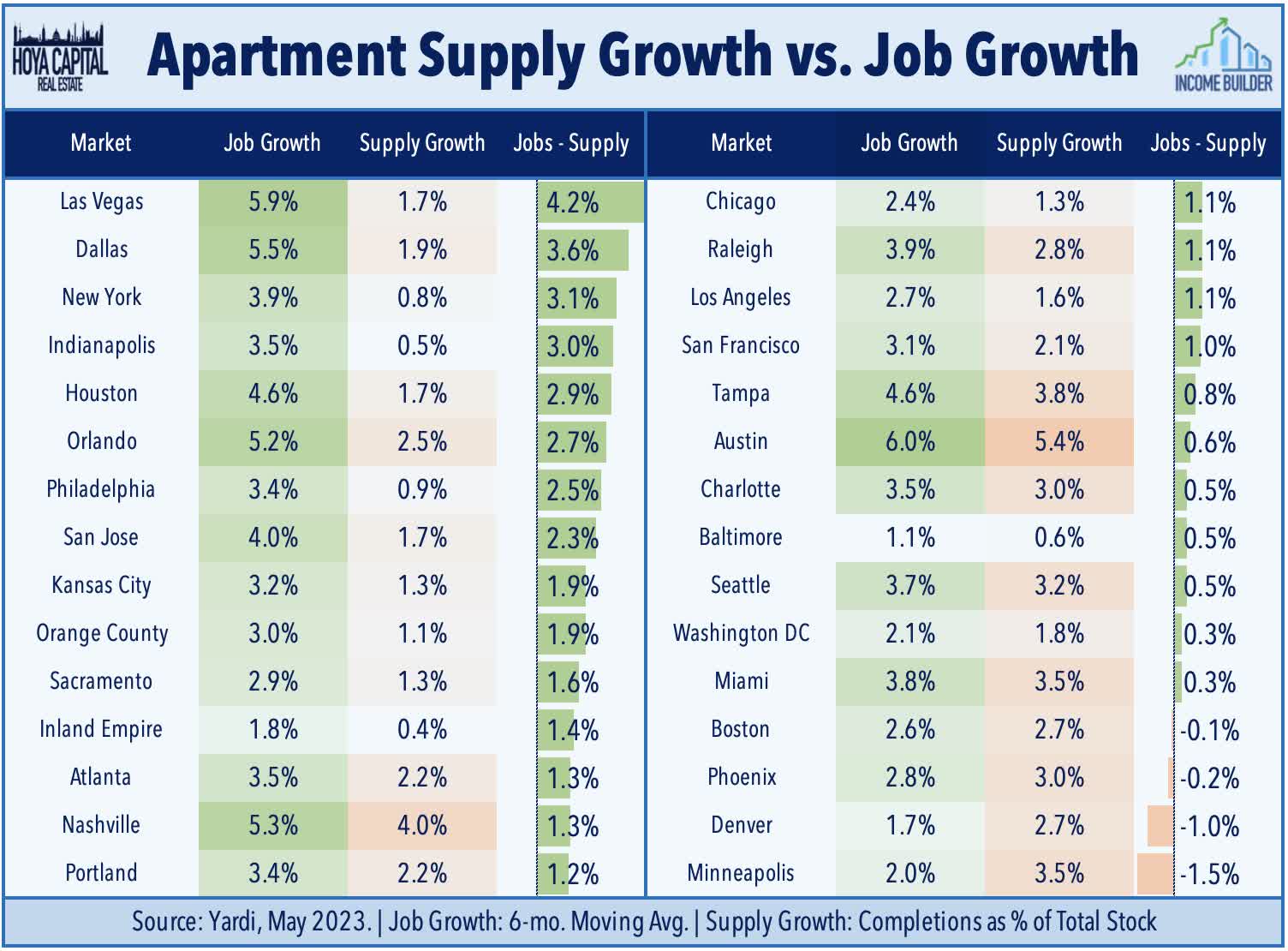

RealPage forecasts 2024 to bring "another year of more supply than demand – adding another challenge for apartment investors also confronting higher expenses and elevated debt costs," but sees a rebound in fundamentals by early 2025 and into 2026, given the recent slowdown in new multifamily starts. At the regional level, elevated supply has generally followed regions with the strongest demand, with the Sunbelt and Mountain West adding the most new supply in 2023: 62% of completions, but also 70% of demand. The Northeast and Midwest regions have seen more balanced conditions, combining for roughly 20% of new supply and 20% of new demand. The West Coast has been the notable weak spot, however, accounting for 10% of new supply but just 4% of net demand. Markets seeing the strongest demand included Dallas, Houston, Phoenix, Austin, and DC. Of note, 10 of the 12 highest-demand markets were in the Sunbelt and Mountain West regions, while just one West Coast market – Seattle – ranked among the top 35.

{kind=link}

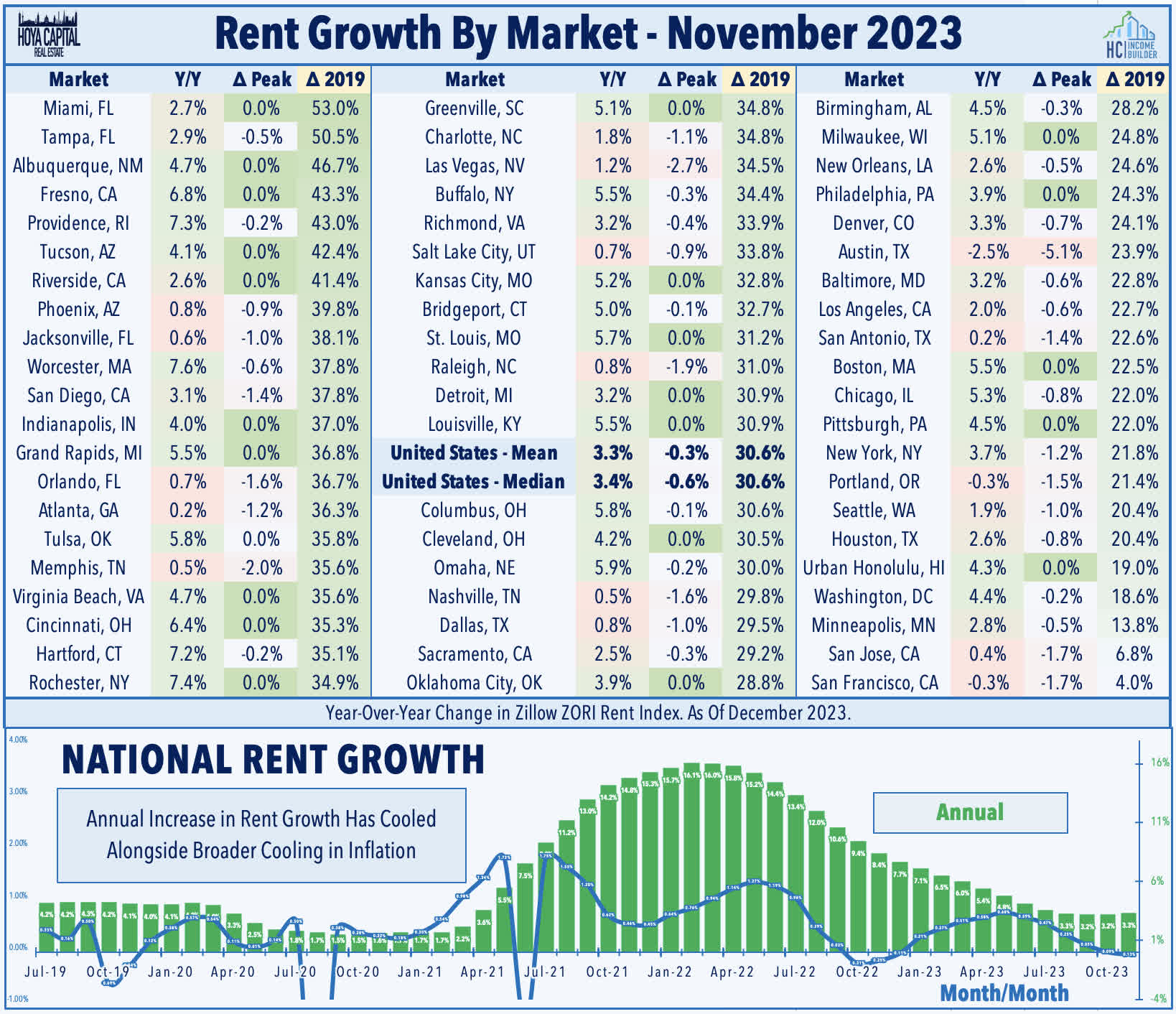

Reports from the six other data providers we track showed similar trends of stabilizing rental market conditions at levels that roughly match the broader inflation rate. Zillow data - which shows "blended' rent growth and includes single-family rentals as well - shows that year-over-year rent growth averaged about 3.3% nationally in its latest report - slightly above the CPI inflation rate. Other data providers generally track new lease "asking" rates - and excluded renewals - which will understate the rental rates achieved by apartment owners given the outperformance of renewals. Apartment List data showed that national asking rents declined -0.8% Y/Y in December, but this marked a second-straight month of improvement since bottoming in October. Redfin data this week also showed that median U.S. asking rent declined -0.8% Y/Y in December, but this was up from the -2.1% in November. Realtor reported annual rent growth of -0.6% last month, but this marked a sixth month of improvement from the lows in June of -1.0%. Yardi reported that rents were higher by 0.4% last month - roughly consistent throughout Q4.

{kind=link}

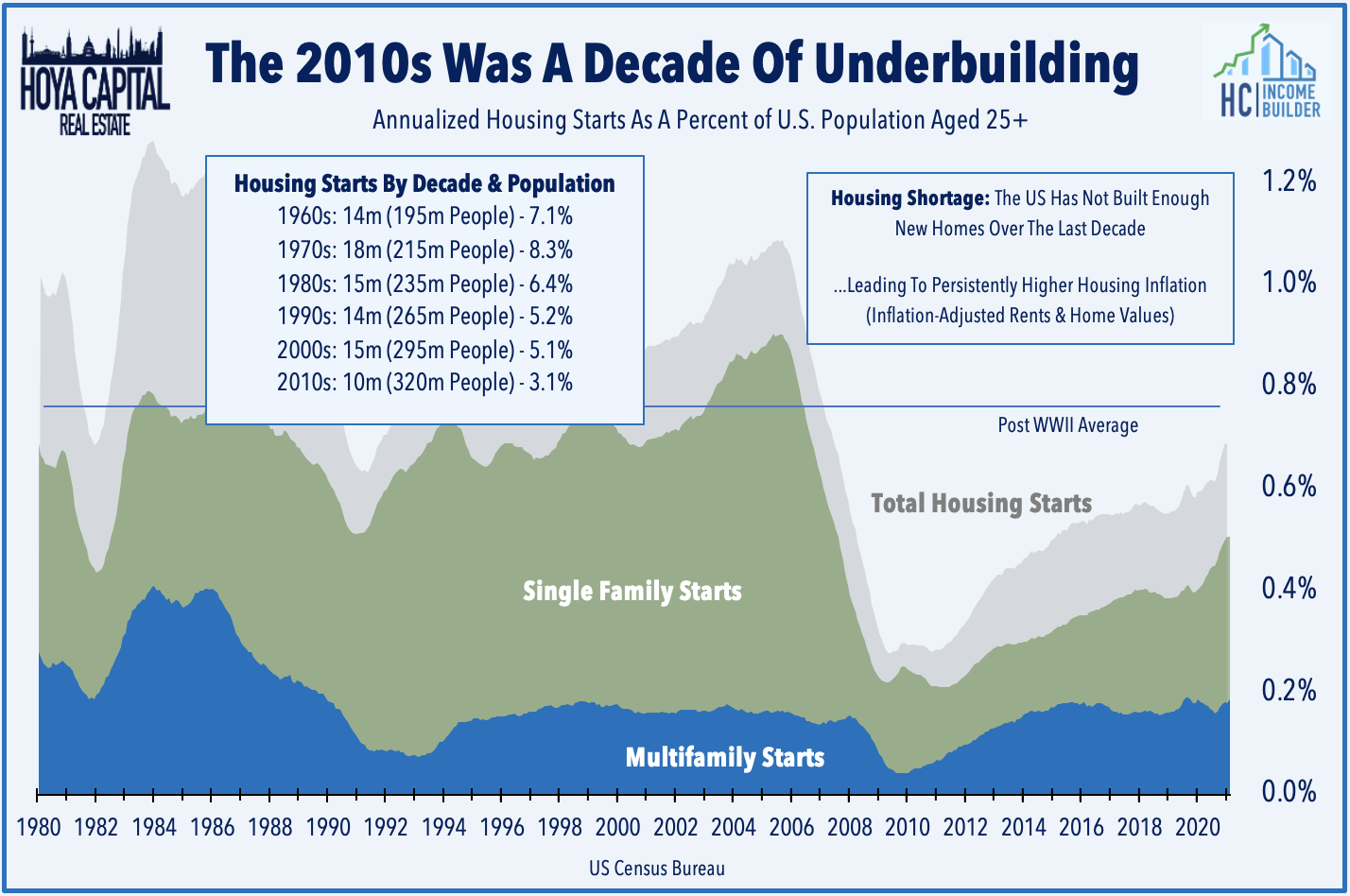

Supply concerns remain the root of the market pessimism as soaring rents sparked a wave of new development that we're seeing come to market, but we believe the often-cited metrics look more menacing than reality. After several years of muted supply growth, multifamily starts jumped 20% in 2021 and another 15% in 2022, but pulled back by 13% in 2023. Also of note, the acceleration in apartment development in recent years was offset nearly one-for-one with a pull-back in single-family development. Yardi expects that deliveries will top 500k in 2024 - representing a roughly 3.0% increase in existing stock - with concentrations in rapidly growing markets in the South and West. Yardi expects this year to be the peak for deliveries of this cycle with supply growth tailing off by early 2025. Despite the elevated supply, Yardi expects positive rent growth of 1.5% in 2024, led by strength in the Midwest region, where supply growth has remained more muted.

{kind=link}

While the overall level of supply growth appears manageable - serving as a moderate headwind but not the looming disaster that some would suggest - Yardi does predict supply growth of over 4% across a handful of markets - primarily in the Sunbelt region - including Austin, Charlotte, Phoenix, Miami, and Nashville - markets that have generally seen the strongest population growth and cumulative job growth over the past three years. Yardi projects that deliveries will begin to wane by mid-2024, however, due to lingering or worsening impediments to new development, including the difficulty of getting construction financing, ongoing delays in labor, and challenges in getting entitlements from local planning and zoning boards. These supply headwinds require an even more discerning approach, but it's important to avoid putting too much weight on the supply factor alone - which would otherwise suggest that markets like Baltimore and the Inland Empire are poised to become top markets. Instead, supply growth should be balanced against job growth - the best available proxy for apartment demand - which shows that some of the more supply-heavy markets actually remain undersupplied relative to demand.

{kind=link}

Deeper Dive: Macro Fundamentals

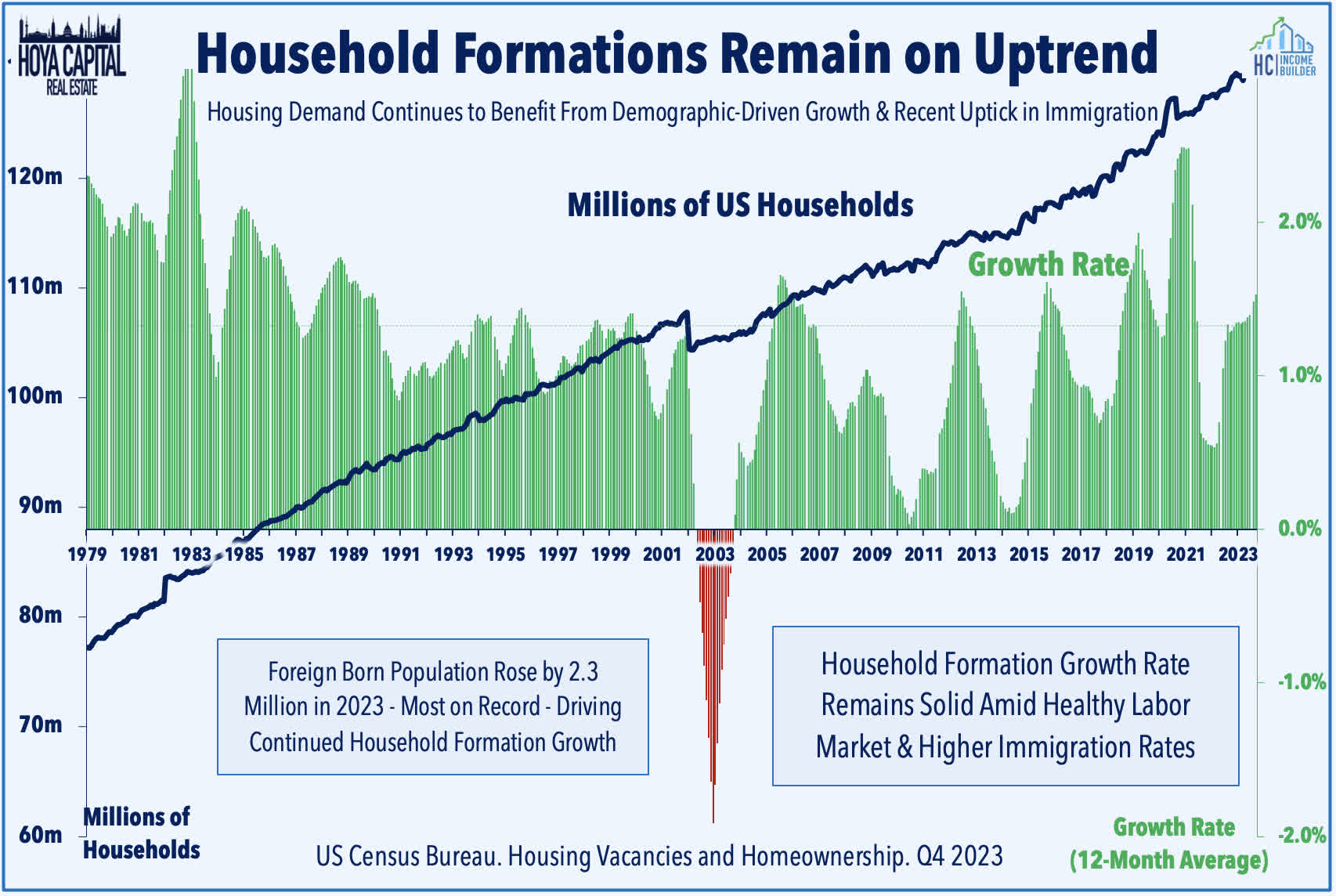

As we've discussed at length over the past decade, demographics suggested the 2020s were already poised to see historic levels of housing demand as the millennial generation - the largest cohort in American history - comes full-steam into a severely undersupplied U.S. housing market. What we could not foresee, however, was the added acceleration provided by the pandemic-driven "Work From Home era" which has begun to unleash millions of extra "deferred" formations among adult children, in particular. Additionally, stronger-than-expected household formations trends are consistent with our long-held theory that population estimates and - and thus U.S. population growth - have been materially understated by Federal statistical agencies over the past several administrations due primarily to the undercounting of immigrant populations, an undercount that the Census Bureau confirmed in a report last month. Net international migration added more than a 2.3 million people to the U.S. population in 2023, marking the largest single-year increase since 2010.

{kind=link}

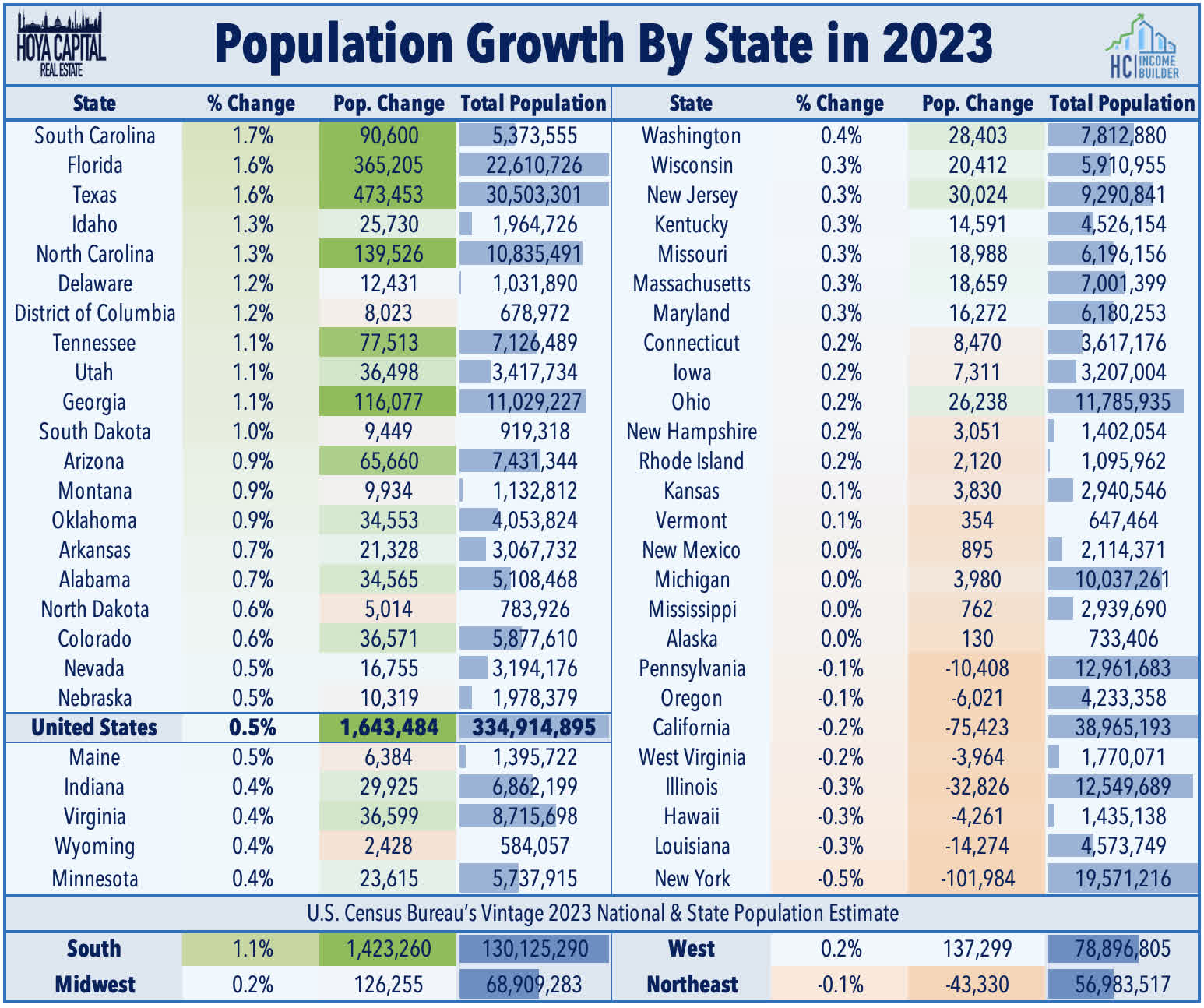

Diving deeper into the recently-released Census data, we observe that South Carolina and Florida were the fastest-growing states in 2023 on a percentage basis with an annual population increase of 1.7% and 1.6%, respectively, while Texas earned the top spot on an absolute basis with the addition of nearly a half-million new residents. For a second-straight year, New York saw the highest outflows on both a percentage basis and an absolute basis, losing 0.5% of its total population this past year. California and Illinois also recorded significant decreases in the resident population of 75k and 33k, respectively. At the regional level, the South was the fastest-growing and the largest-gaining region last year, increasing by 1.1% while the Midwest region recorded an annual increase of 0.2% and the West recorded growth of 0.2%. The Northeast region, however, recorded a population decline of 0.1%.

{kind=link}

Apartment REIT Fundamentals

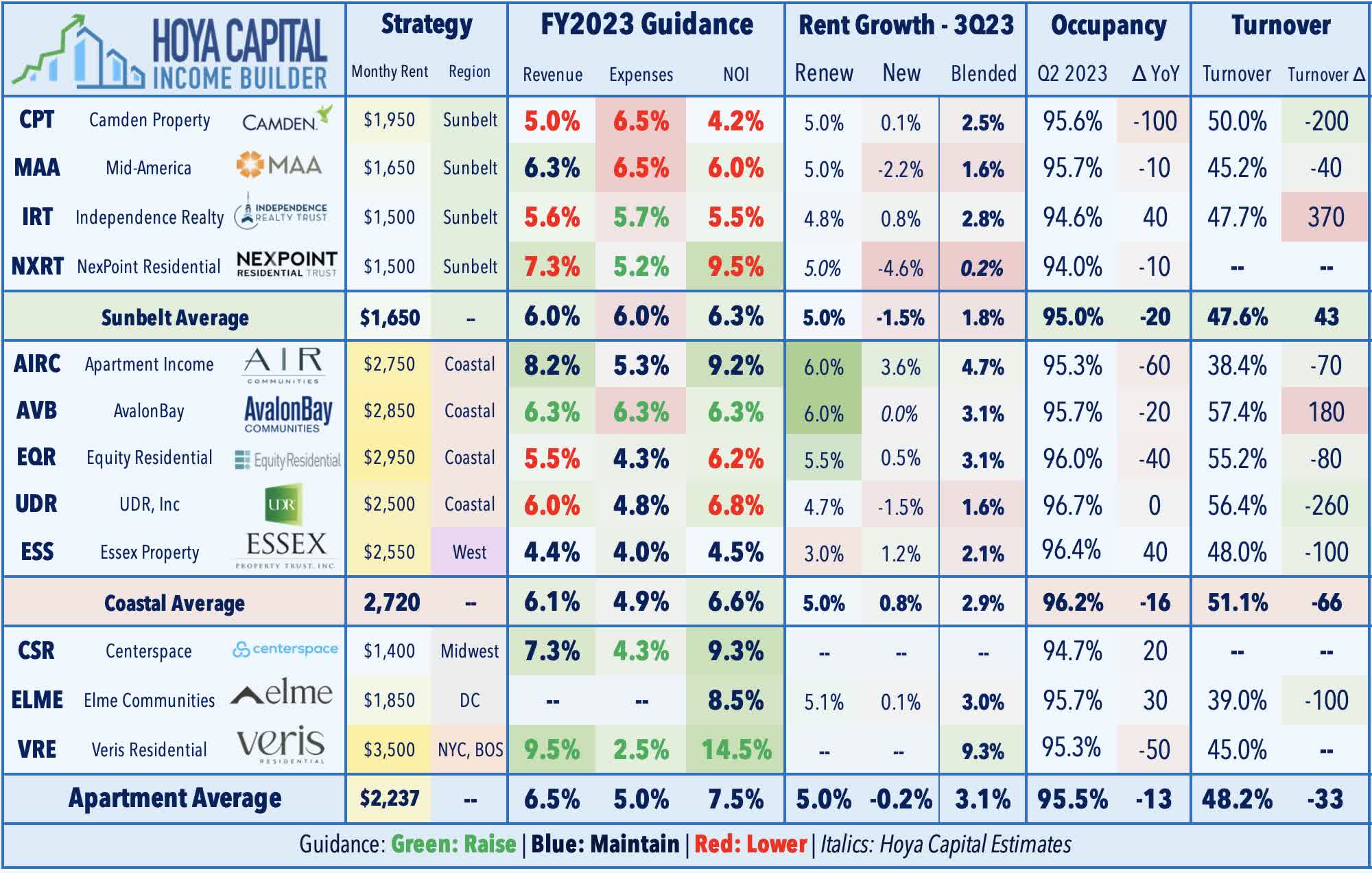

As discussed in our REIT Earnings Recap, Apartment REITs were among the few notable soft spots during third-quarter earnings season, accounting accounted for nearly half (5) of the total (11) downward revisions to Funds From Operations ("FFO") guidance. Following a very strong second quarter, results showed that fundamentals softened later in the summer, resulting from a combination of modest demand softening, pockets of supply headwinds, and upward expense pressures. Blended rent growth cooled to 3.2% in the third-quarter - comprised of a 4.9% increase on renewal rates, and a 0.1% decline in new lease rates - and cooled further in October, with blended spreads averaging 1.9%. Supply pressures are expected to abate into 2025 given the extremely challenging financing environment for new ground-up development. Despite the uptick in supply, however, occupancy rates remained essentially unchanged from last year, while turnover rates actually declined from last year.

{kind=link}

At the regional level, coastal-focused apartment REITs generally reported stronger results this earnings season as strength from East Coast markets offset weakness out West. AvalonBay was the upside standout, raising its outlook across the board while noting that it's seeing less supply growth than its peers, given its focus on suburban Coastal markets. Equity Residential was a notable laggard, lowering its full-year outlook on weakness in its San Francisco and Seattle markets. Apartment Income was also a notable upside standout, maintaining its outlook for sector-leading same-store NOI growth of 9.2% in 2023. AIRC also provided an initial 2024 outlook, noting that it expects same-store revenue growth of 3.5%. Supply headwinds are more pronounced in the Sunbelt, driving downward revisions from all four REITs with notably soft results from Camden - the lone apartment REIT to report negative blended spreads in October.

{kind=link}

Apartment REITs delivered average FFO growth of 19.7% for full-year 2022 - the strongest year ever for the sector and the second-highest earnings growth rate across the real estate industry behind the roughly 23% growth from the storage REIT sector. The outlook for 2023 now calls for FFO growth of 4.5%, on average, which would likely trail only the industrial and manufactured housing sectors for the strongest across the REIT industry. If these full-year outlook targets are met, apartment REITs will have delivered an average cumulative FFO growth of 28.5% since the start of the pandemic. Sunbelt REITs never skipped a beat during the pandemic and now expect 2023 FFO levels to be 47.7% above their pre-pandemic rate from 2019 while Coastal REITs now expect 2023 FFO levels to be about 14% above 2019-levels.

{kind=link}

Coastal-focused REITs led the gains in 2023, led by returns of over 20% from Essex Property and AvalonBay . Despite the underperformance over the past two years, Apartment REITs have been some of the strongest-performing REITs over most long-term measurement periods. From 2010 through 2022, Apartment REITs delivered average annual returns of 15.0%, outpacing the 10.4% annual total returns from the broad-based REIT average during that time. Among the major apartment REITs, the three Sunbelt-focused REITs - Independence , Mid-America , and Camden Property - have delivered the strongest 10-year total returns - despite lagging rather significantly in 2023. Small-Cap BRT Apartments has also quietly delivered impressive total returns over the past five and ten years.

{kind=link}

Balance Sheets & External Growth Prospects

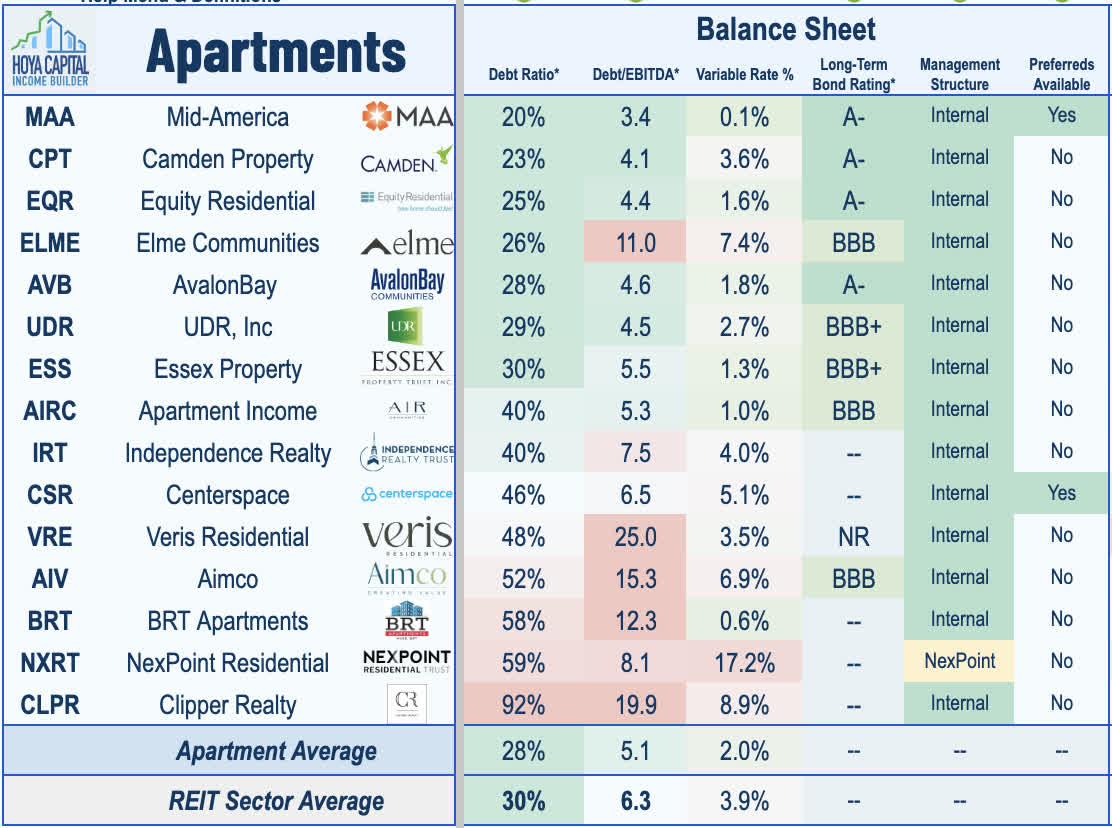

The larger apartment REITs are generally some of the most well-capitalized companies across the REIT sector - a critical attribute during the pandemic-related turbulence and the subsequent surge in benchmark interest rates - but several of the small-cap apartment REITs do operate with elevated debt levels with more exposure to variable-rate debt. Among those is NexPoint Residential , but we've been pleased with NXRT's recent progress in reducing their variable rate exposure through asset sales, refinancings, and the use of interest rate locks. The seven largest apartment REITs command investment-grade credit ratings from Standard & Poor's, led by A- ratings by AvalonBay , Equity Residential , and Camden . The larger REITs in the sector also tend to rank high on the corporate governance scale with shareholder-friendly governance structures.

{kind=link}

Pockets of rate-driven distress in apartment markets have remained isolated to the most highly-indebted corners of the private markets, but this distress spells opportunity for these well-capitalized REITs. While organic growth will be flat in 2024, conditions are becoming ripe for external growth via acquisitions. As noted above, "lower forever" interest rate conditions and limitless access to private debt negated the true competitive advantage of public equity REITs - access to public equity and debt markets - but we foresee a similar revival in private-to-public transactions as we saw in the immediate aftermath of the Great Financial Crisis from 2010-2015 and during the S&L Crisis of the early 1990s that gave rise to many of these public REITs that exist today. This will mark a reversal from the trends seen in recent years in which private firms - notably Blackstone ( BX ) - picked off a trio of multifamily REITs - Bluerock Growth REIT, Preferred Apartments, and American Campus - for its nontraded REIT platform known as BREIT. A wave of investor redemptions from BREIT in recent months has raised our longstanding expectation that these portfolios eventually come back to the public markets either as independent entities or through the acquisition by an existing REIT.

{kind=link}

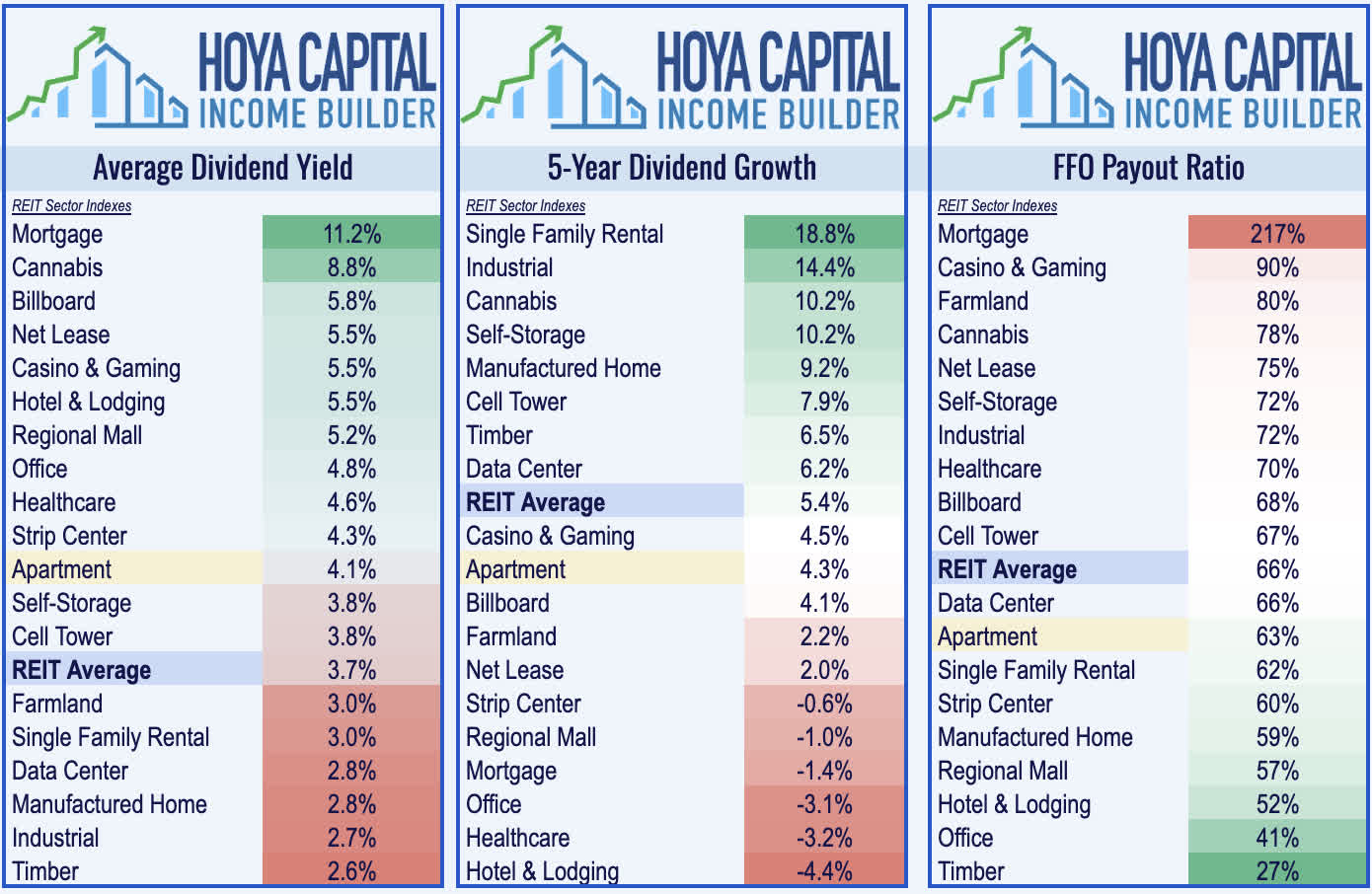

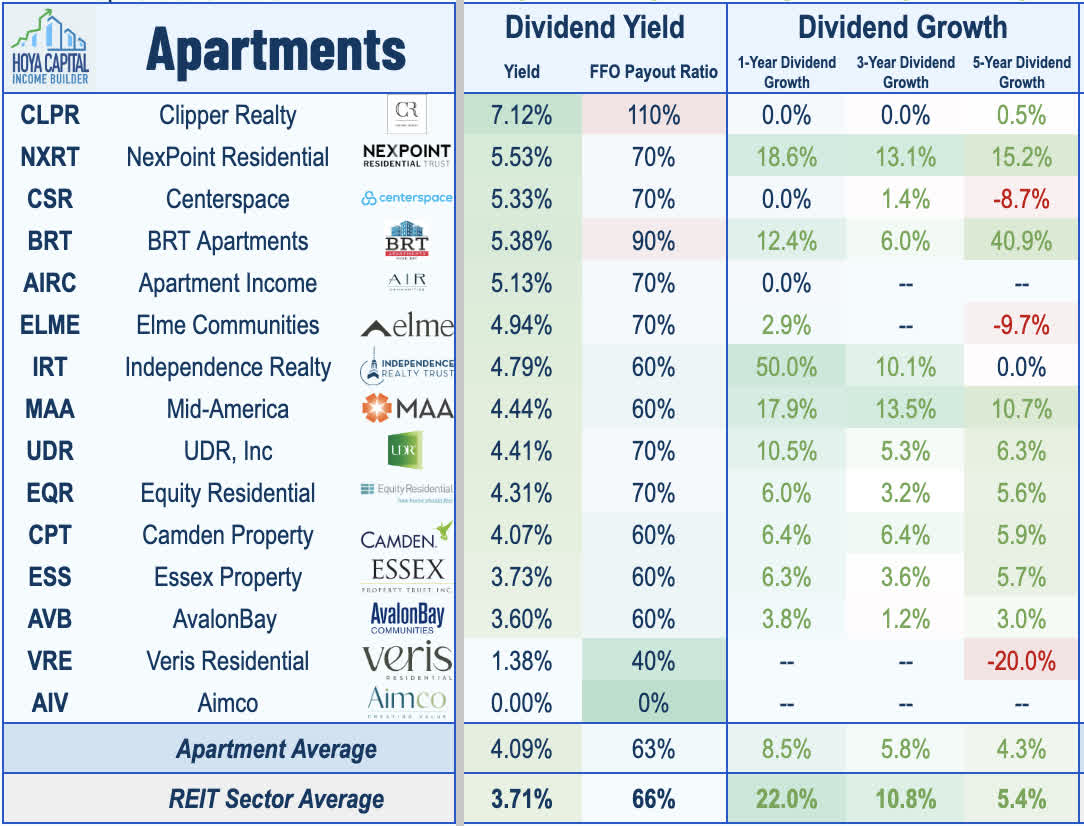

Apartment REIT Dividend Yields

Near-perfect rent collection throughout the pandemic allowed apartment REITs to not only avoid the wave of dividend cuts that swept through the REIT sector during the early stages of the pandemic but also to be among few REITs to raise their distributions in during the depths of the pandemic in 2020 - a trend of dividend raises that continued into 2023. Apartment REITs pay an average dividend yield of 4.1%, which is slightly below the REIT market-cap-weighted sector average of 3.7%. Since the start of 2015, apartment REITs have delivered average annual dividend growth of roughly 4% as near-double-digit growth from Sunbelt-focused REITs has offset the more muted dividend growth delivered by Coastal-focused REITs.

{kind=link}

Apartment REITs only payout around 60% of their available cash flow, giving these companies the flexibility to take advantage of external growth opportunities or to increase future distributions. Nine apartment REITs raised their dividends in 2023 including a 14% dividend hike from Independence and a pair of 10% dividend hikes from NexPoint Residential and UDR . Camden and Elme Communities each raised their dividends by 6%, while AvalonBay raised its payout by 3%. Small-cap Clipper ( CLPR ) tops the charts with a dividend yield of 7.12%, followed by NexPoint ( NXRT ) at 5.33% and Centerspace at 5.33%.

{kind=link}

Takeaway: Deep Discounts As Supply Worries Ease

Following two years of record-setting rent growth, residential rents decelerated in 2023 alongside a broader cooling of inflationary pressures, with multifamily rents seeing a particularly sharp cooldown amid supply headwinds. The wave of pandemic-era development - started at a time when rents were rising double-digits - resulted in a record-year of new deliveries in 2023 with similarly elevated supply levels expected in 2024. The pundit-predicted rental market "crash" has remained elusive, however, as demand has stayed surprisingly robust, driven by the combination of resilient job growth, homeownership unaffordability, favorable demographics, and elevated inbound immigration. While fundamentals remain more favorable on the single-family side - where the lack of supply is perhaps the bigger issue - we're maintaining our overweight positioning and positive outlook on the multifamily side. We expect a return to the "inflation-plus" level of rent growth that was the norm in the pre-pandemic era as housing demand outpaced new home development. Elevated rent growth and stretched affordability metrics are perhaps the most obvious indication of a lingering undersupply of housing, as Freddie Mac estimates that the U.S. housing market is still more than 3 million housing units short of what's needed to meet the country's demand.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

{kind=link}

For further details see:

Apartment REITs: A Renter's Market