APO - Apollo Global Management Is My Favourite Private Equity Company - Here's Why

2023-12-25 06:58:35 ET

Summary

- Apollo is the leader in the private credit industry, which is expected to grow at a CAGR of 15% and be worth $40tn.

- The firm has developed the necessary infrastructure to position itself across the private credit pipeline, with a multi-hundred billion dollar ecosystem across asset-backed finance and origination.

- Apollo demonstrates superior multiples-based value and growth capabilities than peers, reflected in a fair value of $107.14, a 14% undervaluation.

- Expecting to double AUM and net income over the next 3 years, Apollo also pays out a 1.85% dividend.

- This leads me to rate Apollo Global Management a 'strong buy'

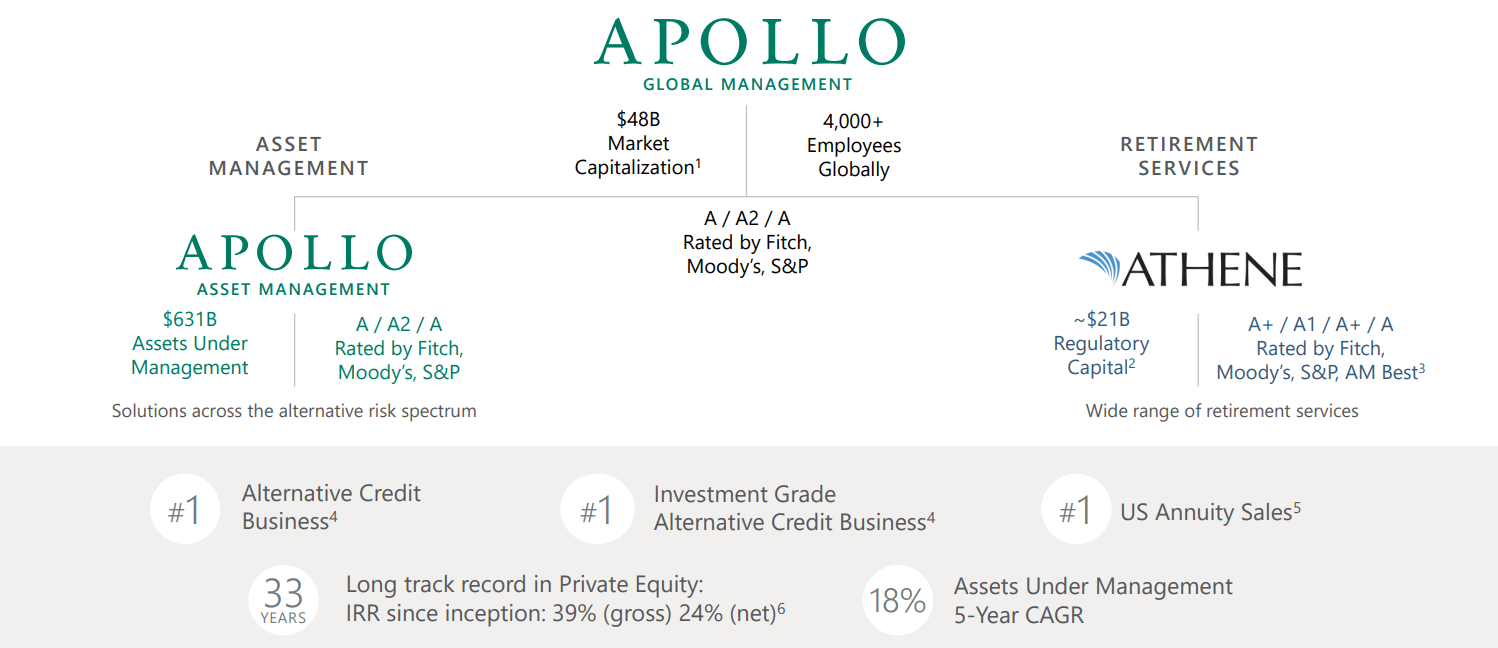

Apollo Asset Management ( APO ) is a New York City-based multinational private equity firm with a focus on private credit and ancillary verticals across the financial services industry, including alternative assets, insurance, annuities, asset management, etc.

{kind=link}

Apollo Global Management November'23 Presentation

{kind=link}

Apollo Global Management November'23 Presentation

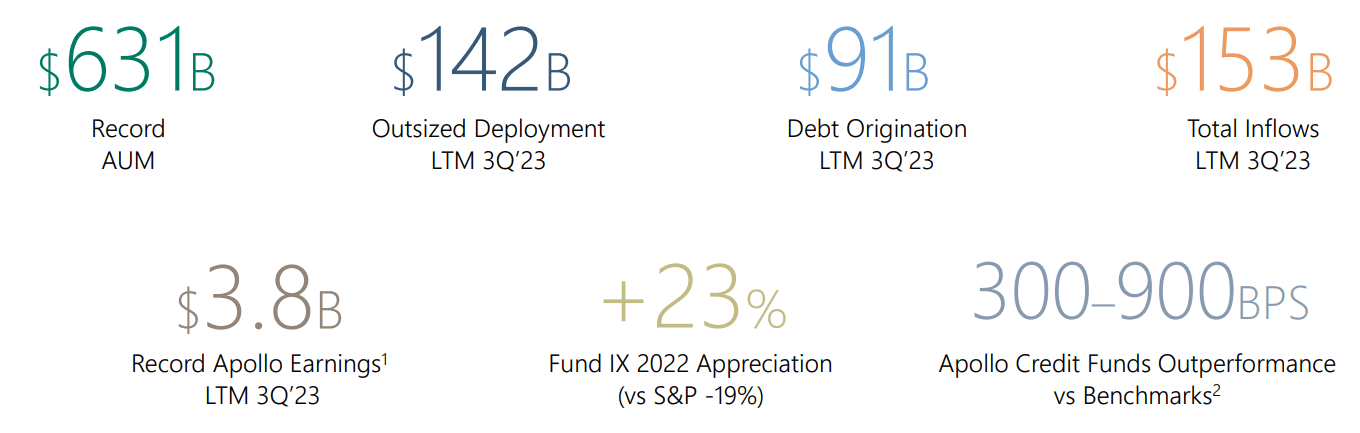

Through these actions, in the previous quarter, Apollo recorded its record AUM of $631bn, supporting earnings of $3.8bn and a free cash flow of $54.00mn.

Introduction

Throughout my 100+ articles on this website, I have covered many industries, from tech to utilities, mining to defence, and so on. However, I maintain a particular focus on financial services, with high levels of coverage of the private equity space, with bullish perspectives on the Carlyle Group, Ares Management, and TPG. Between my 'buy' ratings of all these stocks, though, Apollo stands out.

Perhaps this is because Apollo has grown beyond the bounds of traditional private equity firms and markets, developing the origination and distribution infrastructure to become and remain the leader in the ever-growing private credit market, complementing its pre-existing private equity expertise, ultimately allowing the firm to vertically integrate, reduce its expense base and become a growth leader

{kind=link}

Apollo Origination Deep Dive

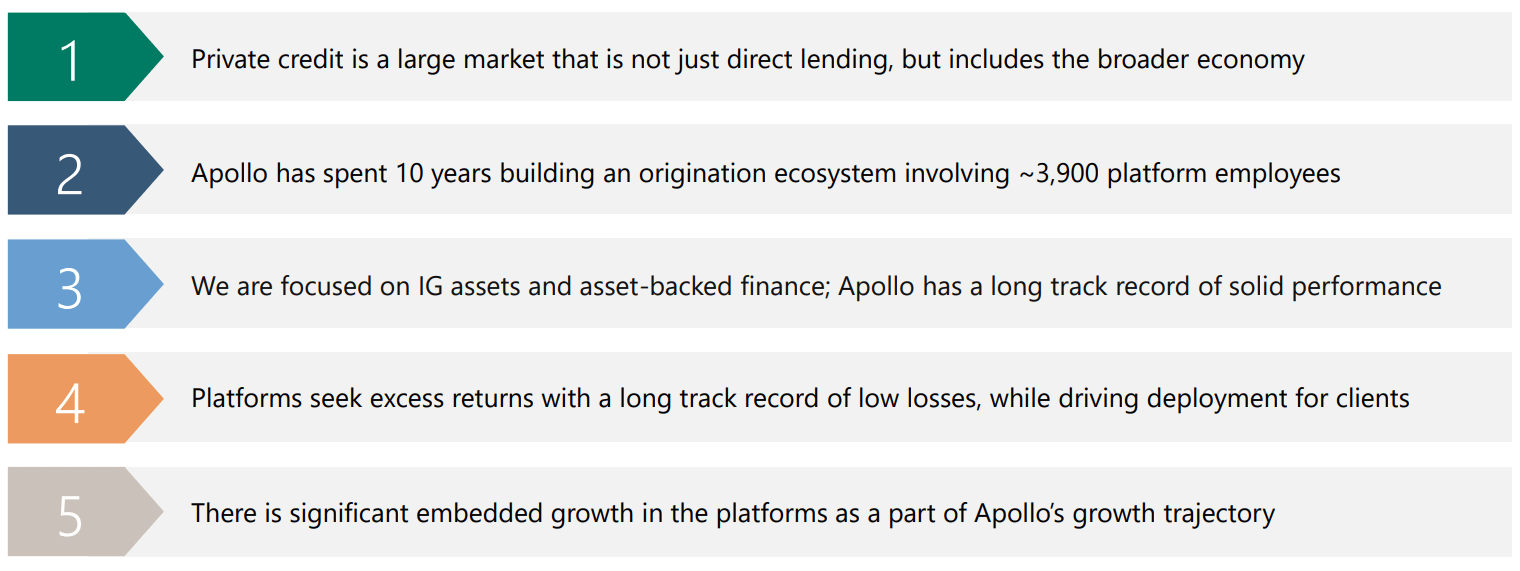

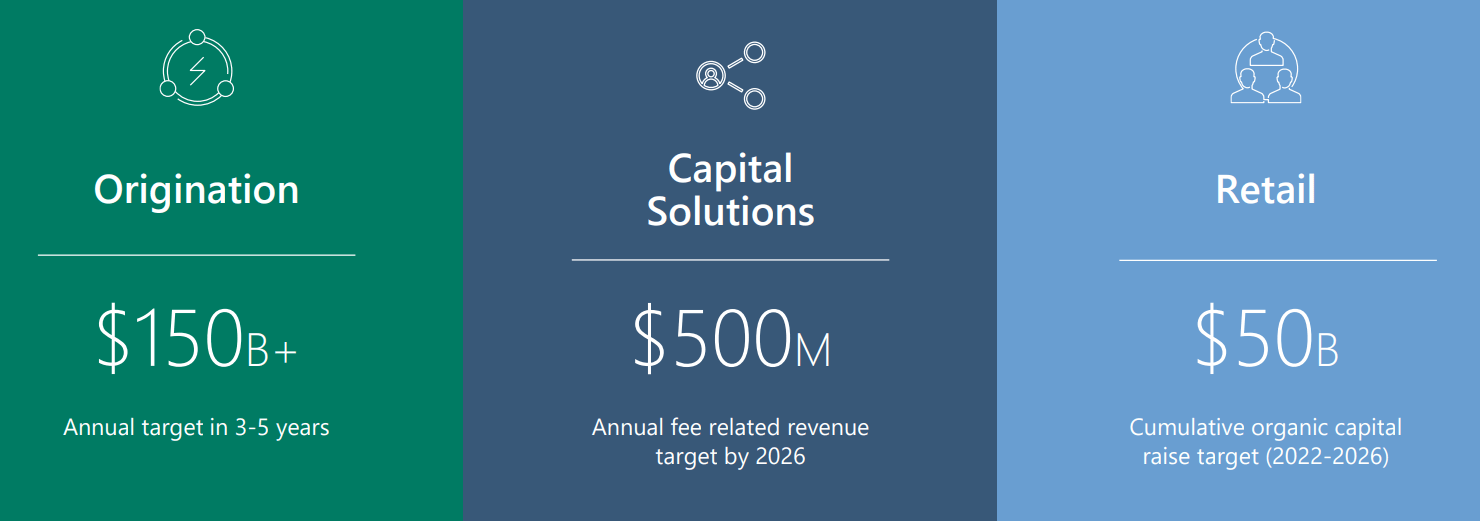

Apollo has thus formulated a fivefold framework to explain its corporate strategy and bull case; the private credit market remains rapidly growing and tied to the growth of the broader economy, Apollo has built the necessary infrastructure to leverage the growth of this asset class, the assets Apollo holds are of high quality and enable low-risk, high reward asset-backed origination strategies, Apollo's platforms support a risk-buffered approach, and, therefore, Apollo can effectively realize intrinsic growth across its origination, capital solutions, and retail financial products and channels.

{kind=link}

Apollo Global Management November'23 Presentation

Although Apollo is fundamentally undervalued, the long-term value proposition of the firm is derivative of Apollo's wider corporate strategy and positioning to leverage long-run megatrends. As such, in the long-term, Apollo receives a 'strong buy' rating from me.

Valuation & Financials

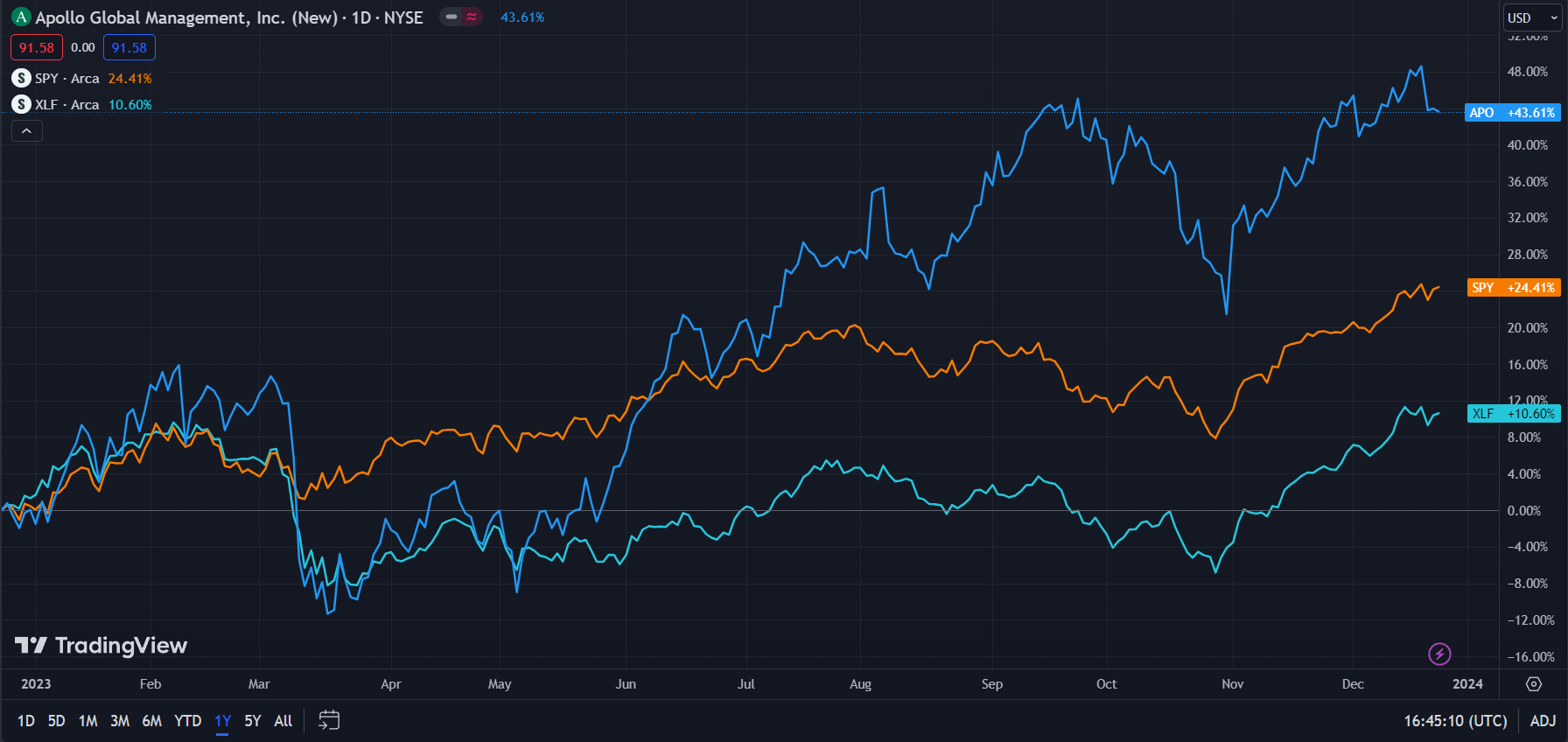

Trailing Year Performance

In the TTM period, Apollo's stock- up 43.61%- has outperformed both the financial services industry, as represented by the Financial Select Sector SPDR Fund ( XLF )- up 10.60%- and the broader market, as represented by the S&P 500 ( SPY )- 24.41%.

{kind=link}

Apollo (Dark Blue) vs Industry & Market (TradingView)

Although the underperformance of the financial services industry can be attributed to rate volatility and the unique risks to banks over the past year, private equity firms have generally outperformed the market, able to leverage their fundraising capabilities to capitalize on distressed and undervalued opportunities in the TTM.

Apollo, both with its inelastic business practices regarding retirement offerings, in addition to its ability to provide alternative credit options to higher rate public credit markets, has seen quality returns, supporting market-outperforming earnings.

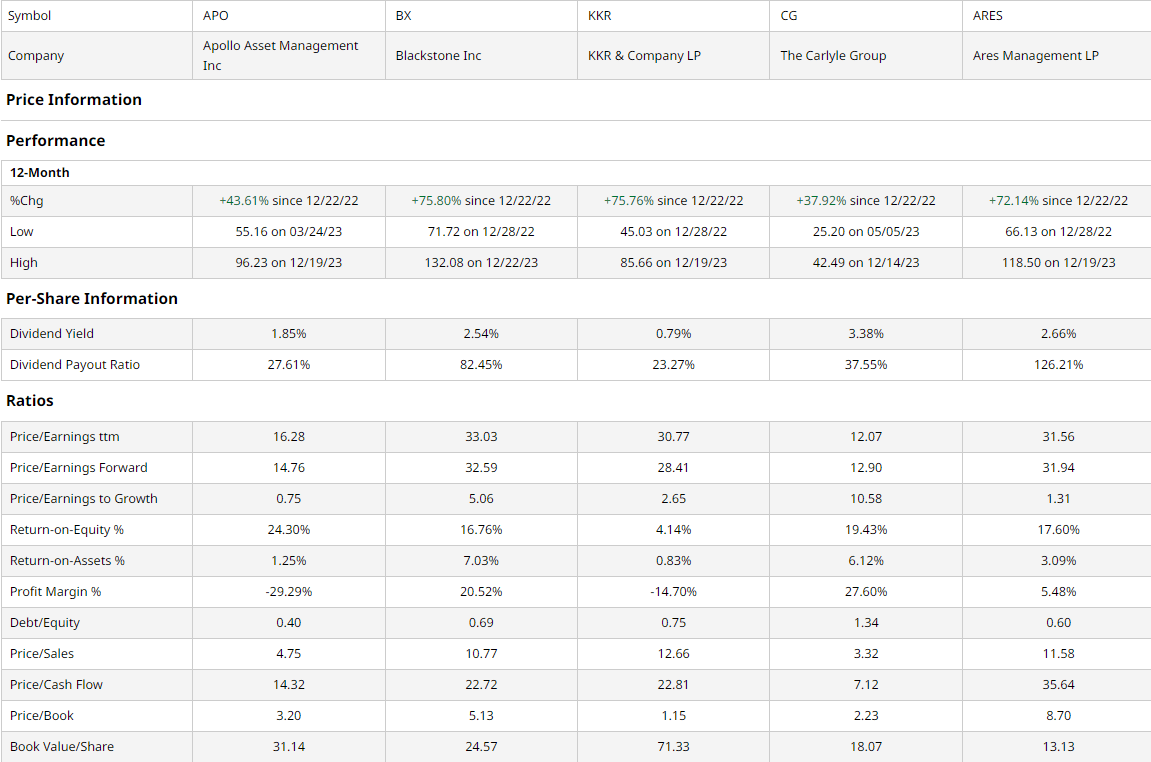

Comparable Companies

Major private equity firms have generally expanded beyond their singular focus on private capital markets- with Apollo, for example, zeroing in on private credit- and therefore have become too operationally different to be panoptically direct competitors. Despite participation across divergent segments, I chose to compare Apollo to the larger private equity majors. This group includes the world's largest private equity firm which has evolved its focus on residential real estate, Blackstone ( BX )- Dividend Sensei's article provides more depth on this comparison, the leveraged-buyout specialized KKR & Co. ( KKR ), the alternative credit, CLO-growth-focused Carlyle Group ( CG ), and the volume-focused Ares Management ( ARES ), which has developed its focus beyond traditional private equity assets towards items such as insurance solutions and SPACs.

{kind=link}

barchart.com

As demonstrated above, Apollo, despite experiencing the second-poorest price action of the peer group over the past year, has seen substantial price growth. While this is a testament to the strength of the private equity industry as a whole, this exemplifies Apollo's longer-term focus. As such, I believe that Apollo has greater room for long-run growth than peers, especially when assessing the company from a multiples and growth perspective.

For example, Apollo maintains the second-lowest trailing and forward P/E ratio, alongside the second-lowest P/S and P/CF ratios. Additionally, Apollo maintains a relatively low P/B, representing value across all three financial statements.

Moreover, the firm sustains the lowest PEG ratio and the highest ROE, representing Apollo's outsized growth capabilities. Along with the lowest debt/equity of the group and second-highest book value per share, Apollo is well-positioned with a lower cost of capital and greater financial security than peers.

Valuation

According to my discounted cash flow analysis, at its base case, the net present value of Apollo is $102.21, meaning, at its current price of $92.06, the stock is undervalued by ~10%.

My model, calculated over 5 years without perpetual growth built-in, assumes a discount rate of 9%, manifesting the firm's high volatility- relative to the financial services industry- and the higher cost of debt as of current. Additionally, remaining conservative, I estimated stagnant net margins alongside a forward 5Y arithmetic revenue growth average of 10%, despite a trailing arithmetic average of 69.94%.

{kind=link}

Alpha Spread

Alpha Spread's multiples-based relative valuation corroborates my thesis on undervaluation, estimating an 18% undervaluation, reflecting a relative value of $112.07.

Thus, taking an average of my NPV and Alpha Spread's relative value, the fair value for Apollo is $107.14, representing a ~14% undervaluation.

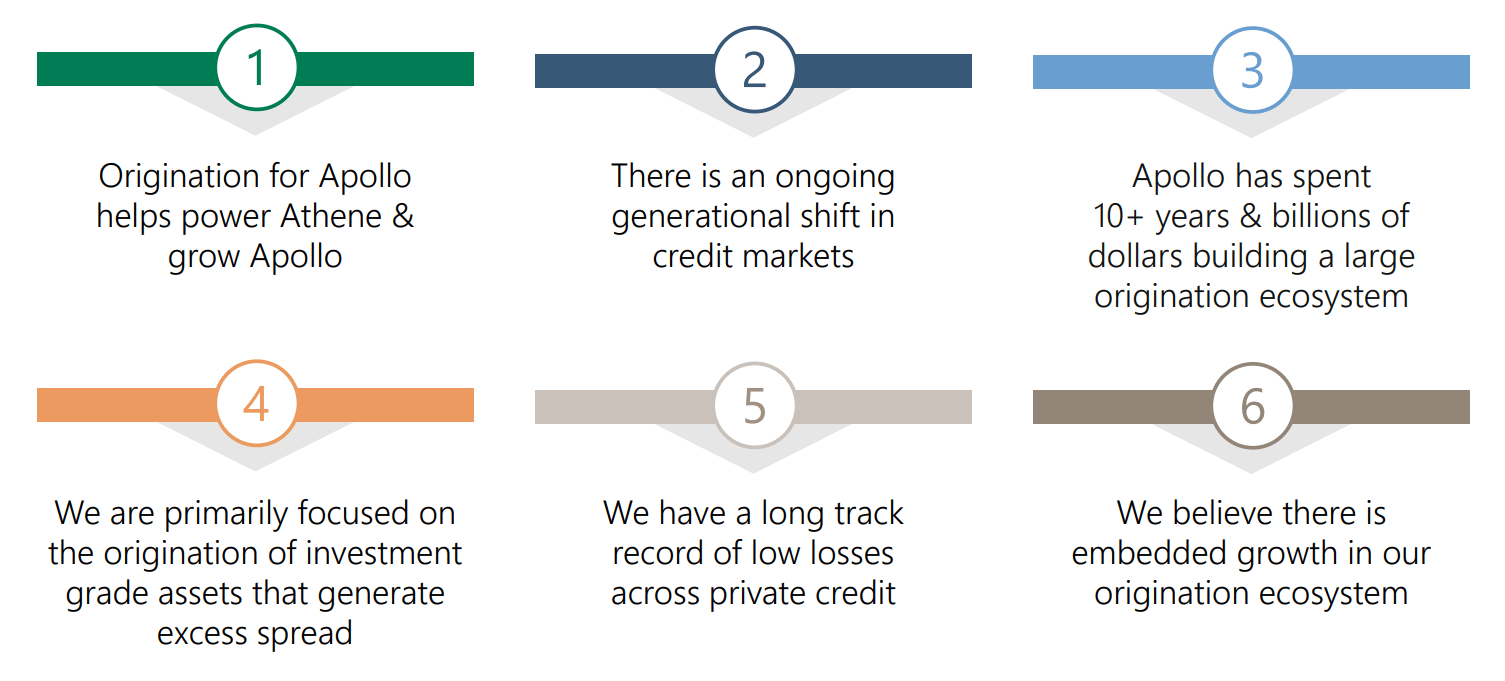

Apollo Has Spent Years & Billions Developing a Holistic, Superior Origination Ecosystem

The first aspect of the capital pipeline Apollo has sought to integrate has been the most significant; the origination platforms, which feed into FAUM and SAUM volumes. To maximize this strategy, Apollo has outlined six primary themes associated with its origination platform; the Athene insurance and annuity platform- and perhaps the Pension Insurance Corporation - works complementarily with Apollo's origination to source capital and provide an anchor clientele; the origination strategy capitalizes on shifts from public to private credit; Apollo is well-positioned in terms of infrastructure to exploit these themes; the firm chooses primarily to originate higher quality assets to draw on their spreads while mitigating risk; Apollo maintains a track record of lower losses across private credit; and therefore, proves the overarching theme of Apollo holding intrinsic growth in its origination platform.

{kind=link}

Apollo Origination Deep Dive

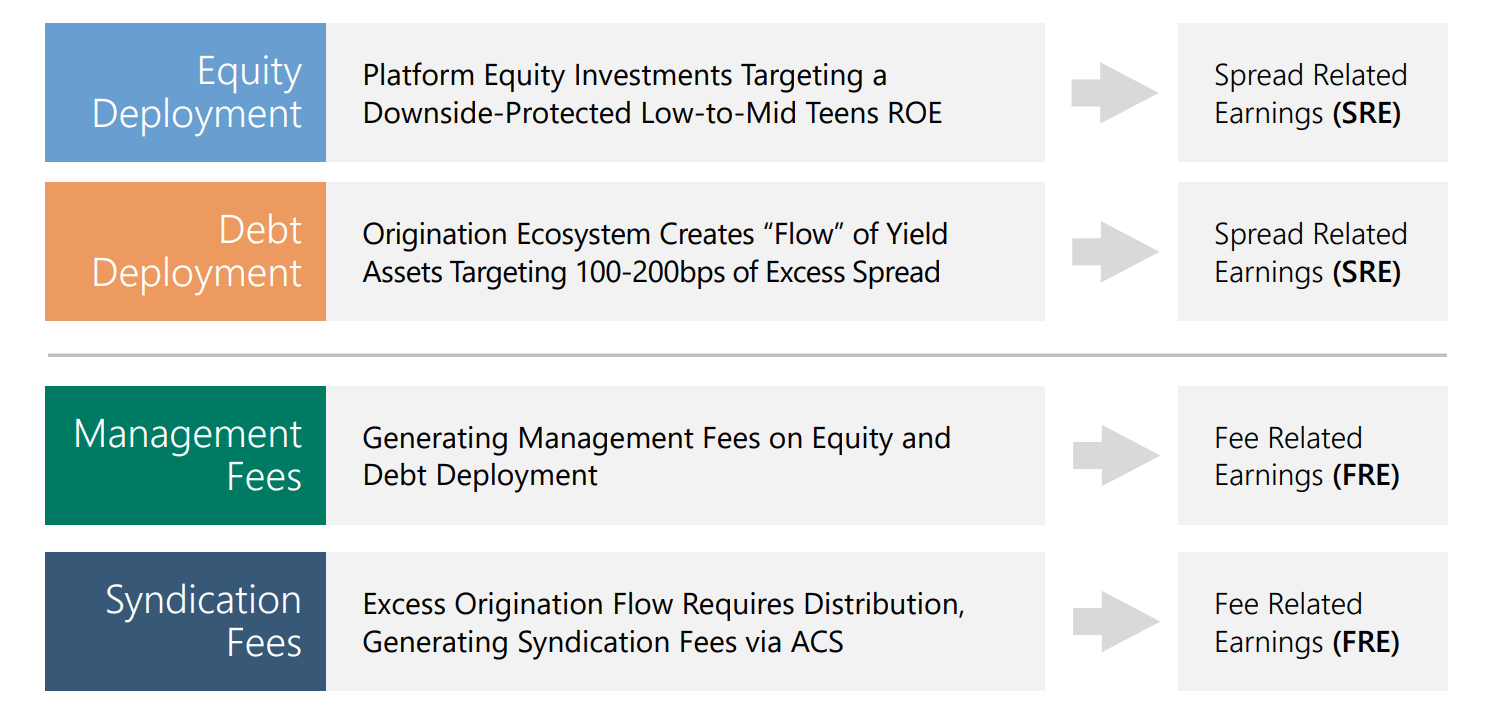

As such, Apollo is able to realize parallel profit centres; through debt and equity deployment, Apollo can generate lower risk, spread-related earnings effectively; through management and syndication fees, Apollo can compound its earnings through FRE.

{kind=link}

Apollo Origination Deep Dive

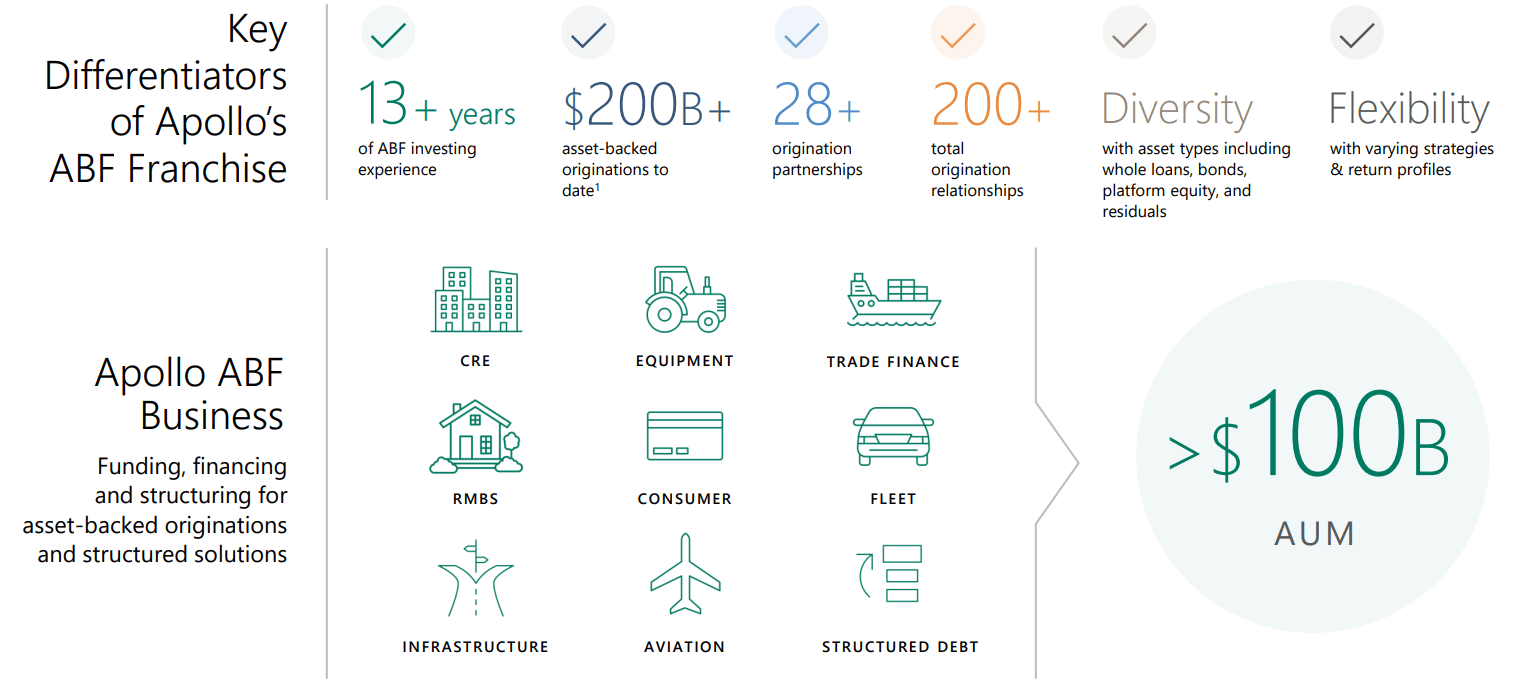

Among the main draws of private credit facilities such as Apollo's is its ability to be structured towards the specialized needs of clients. To best manage risk and securitize assets for maximum flexibility, Apollo has developed asset-backed finance as a key aspect of its origination platform, accounting for >$100bn in AUM. The said asset-backed finance model is highly diversifiable across different industries, such as real estate, trade finance, infrastructure, etc. and enables sustainable horizontal growth.

{kind=link}

Apollo Origination Deep Dive

Apollo is the Leader in the $40tn Private Credit Market

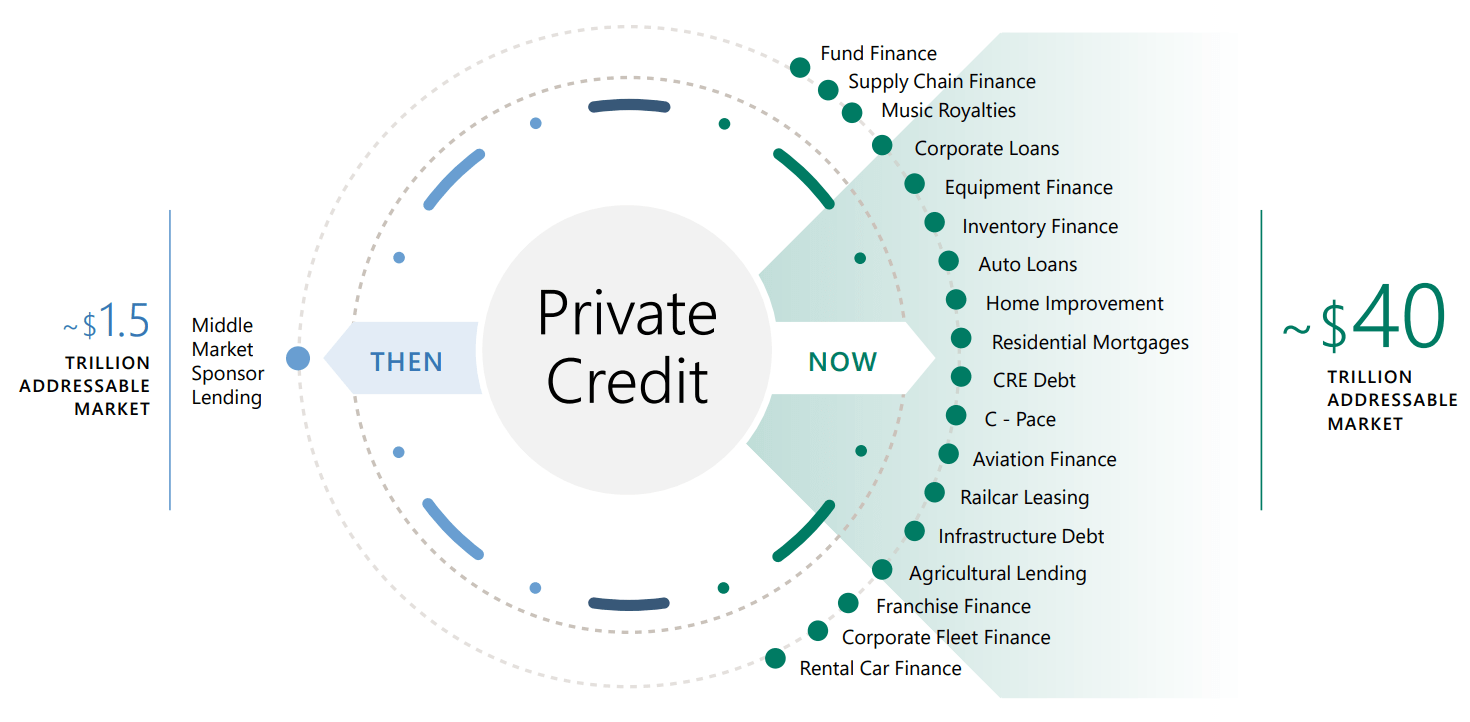

Apollo's origination platform is a single part of its overarching private credit strategy, which seeks to leverage the growth of private credit markets. Private credit markets have grown from a $1.5tn TAM to a $40tn, multivector TAM, expected to grow at a 15% CAGR according to BlackRock.

{kind=link}

Apollo Origination Deep Dive

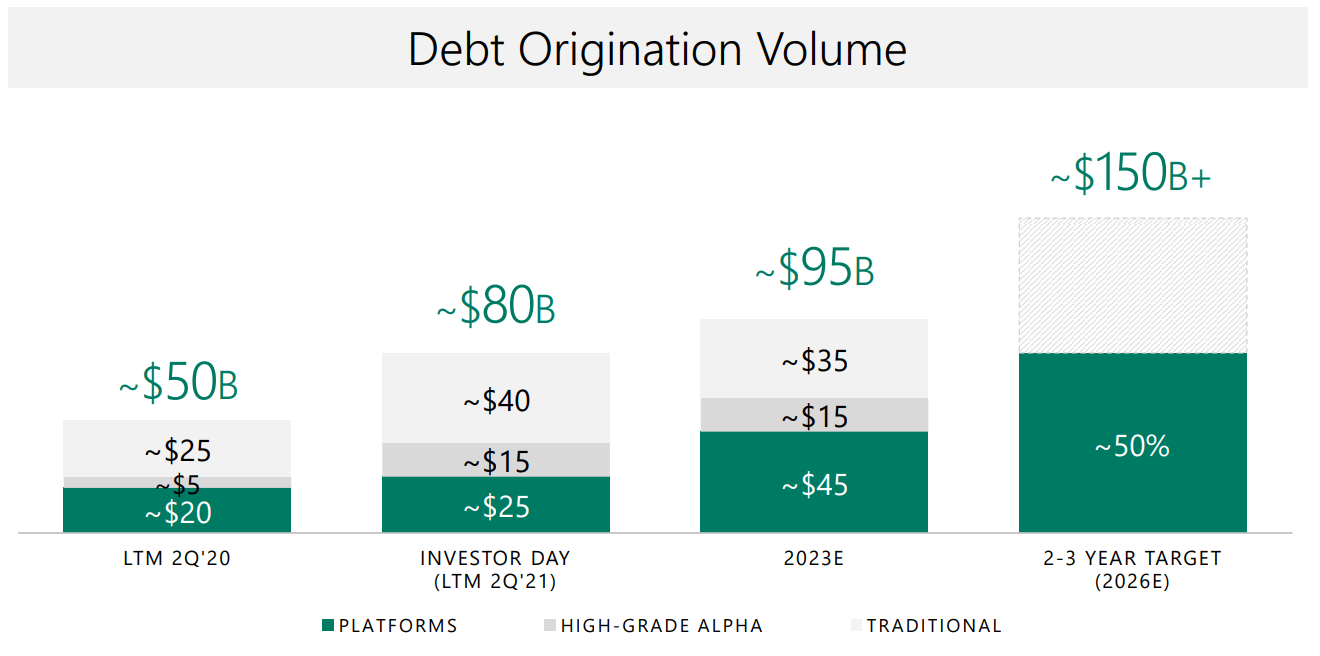

In focusing on this, Apollo has nearly doubled its debt origination volume from $50bn to $95bn in the span of 3 years. Apollo, as the leader of the private credit market, expects this volume to grow >50% over the next three years, demonstrating extraordinary scalability.

{kind=link}

Apollo Origination Deep Dive

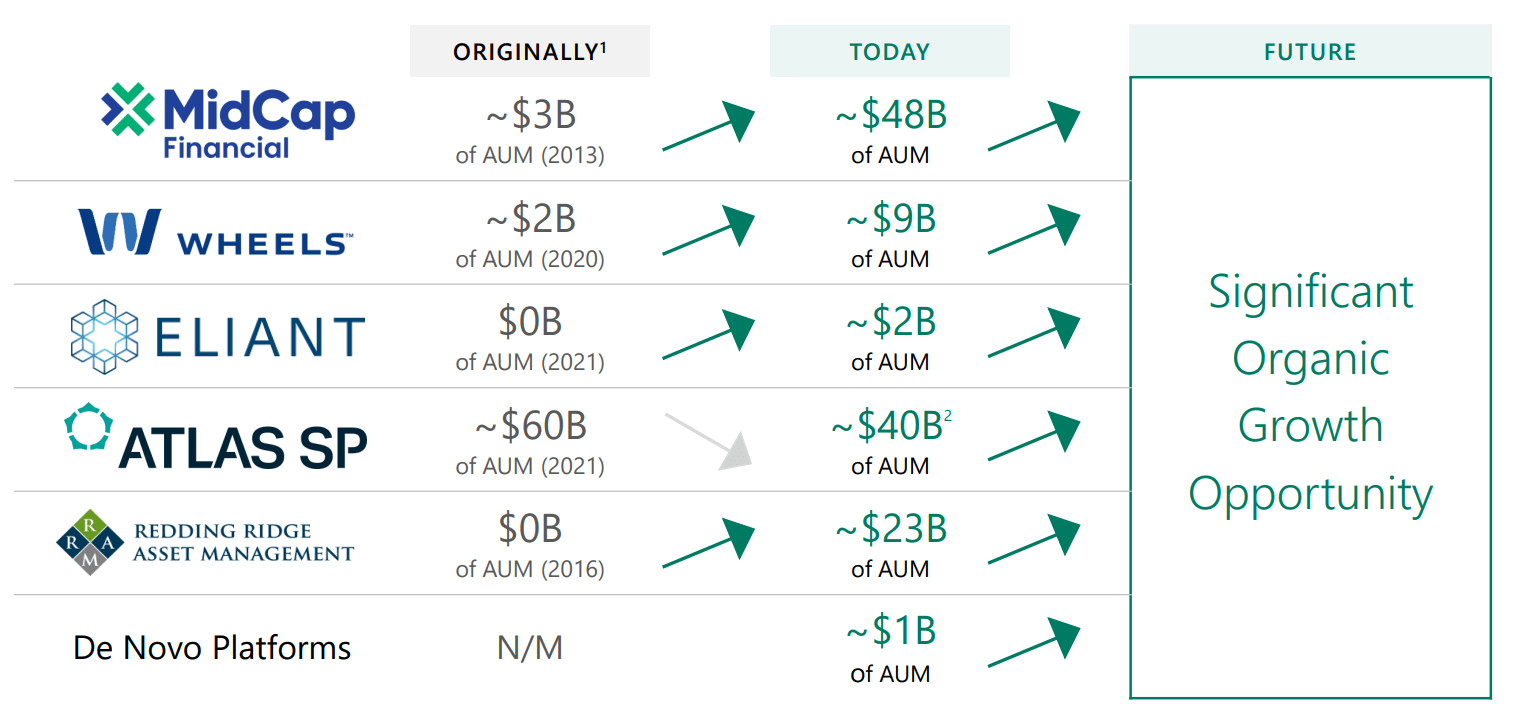

Apollo additionally retains the strategic advantage of its component subsidiaries, each targeting a specific credit niche. For example, MidCap Financial provides, as the name suggests, middle capitalization firms with private credit and asset-backed finance solutions, while Atlas SP, for instance, offers bespoke credit solutions to REITs, mortgage lenders, and other financial services companies.

{kind=link}

Apollo Origination Deep Dive

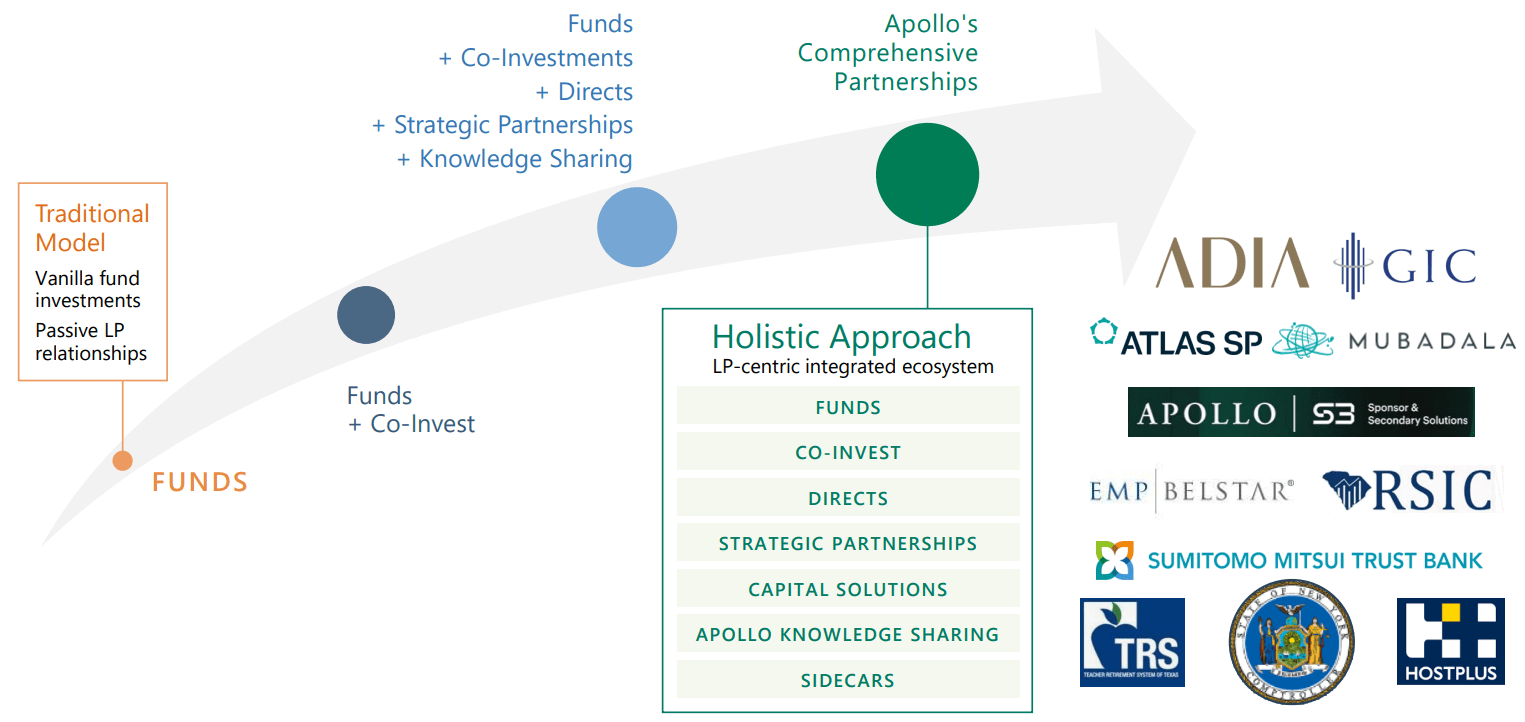

Across the previously discussed private credit space but also Apollo's private equity verticals, the firm seeks to align its success with the success of its stakeholders, whether they be shareholders, counterparties, or clients. And where Apollo does not yet maintain strategic expertise, they holistically integrates comprehensive partners, also allowing the firm to upsell its products to a larger client base.

{kind=link}

Apollo Global Management November'23 Presentation

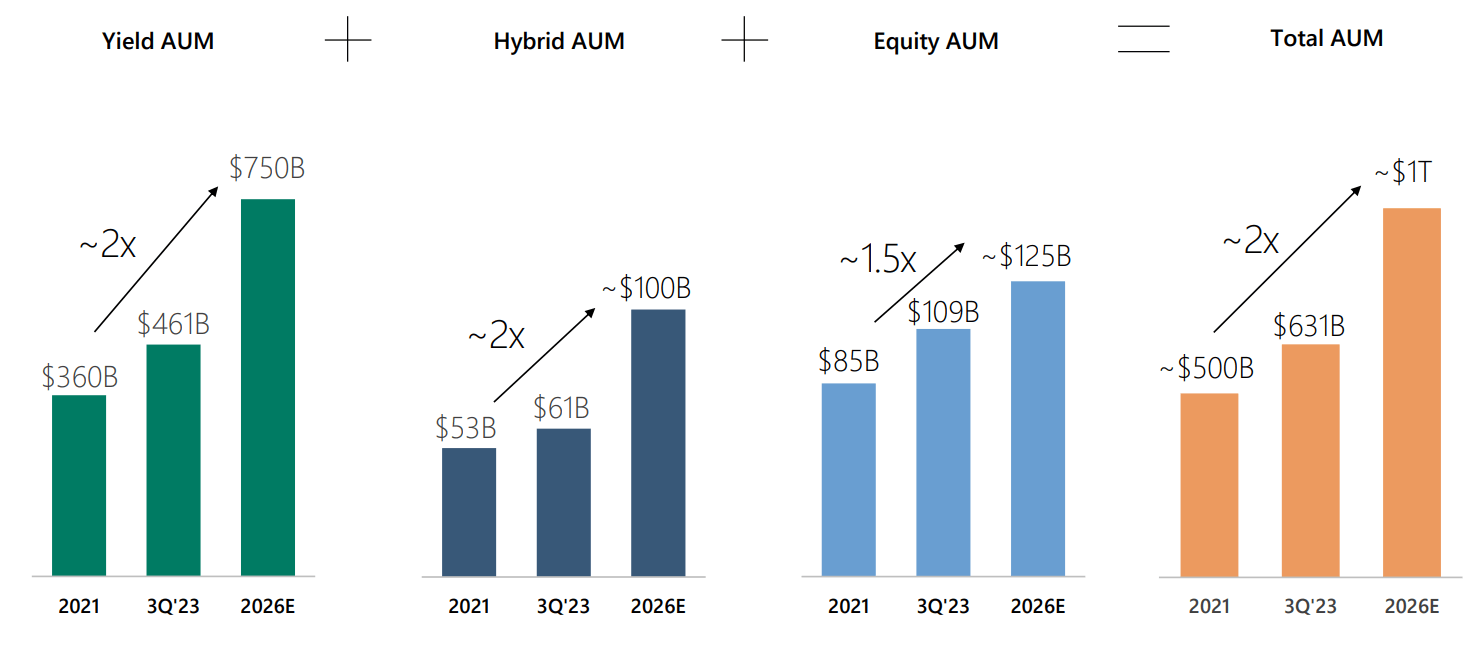

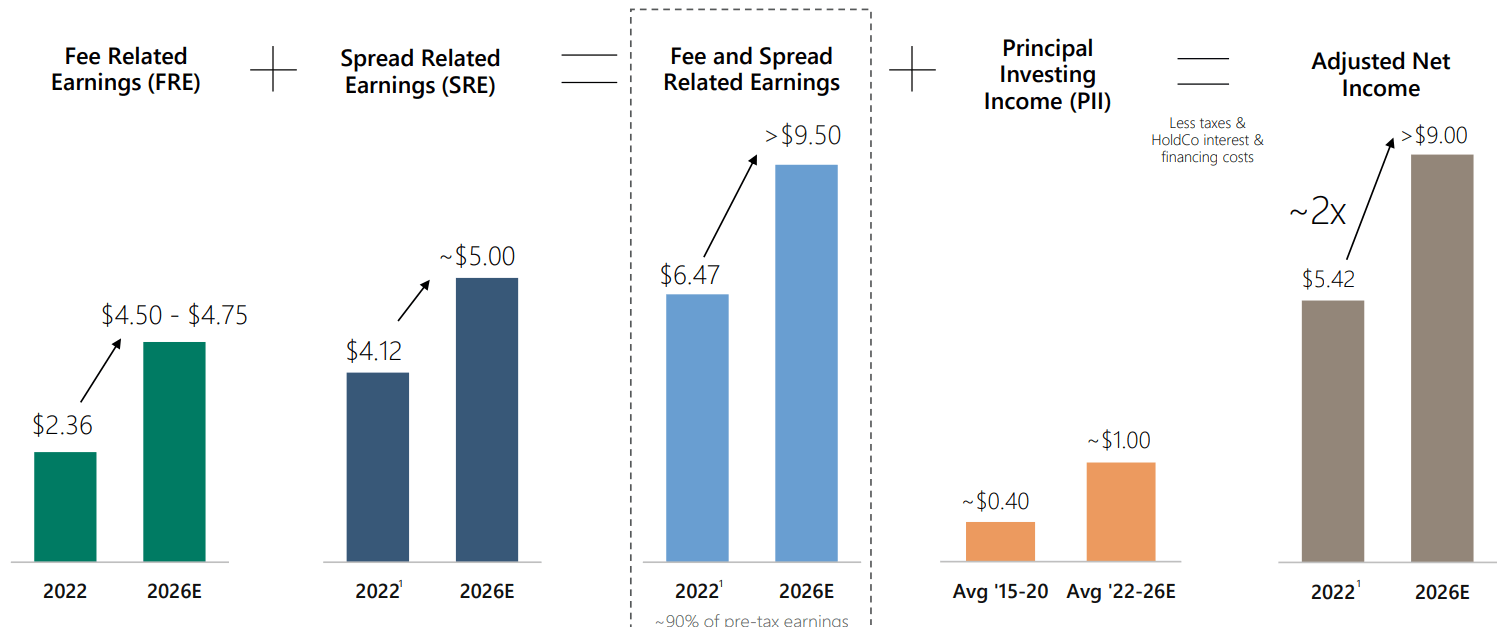

Ultimately, through all the strategies discussed in this analysis, Apollo aims to double its overall AUM in the coming three years, while nearly doubling adjusted net income figures.

{kind=link}

Apollo Global Management November'23 Presentation

{kind=link}

Apollo Global Management November'23 Presentation

Wall Street Consensus

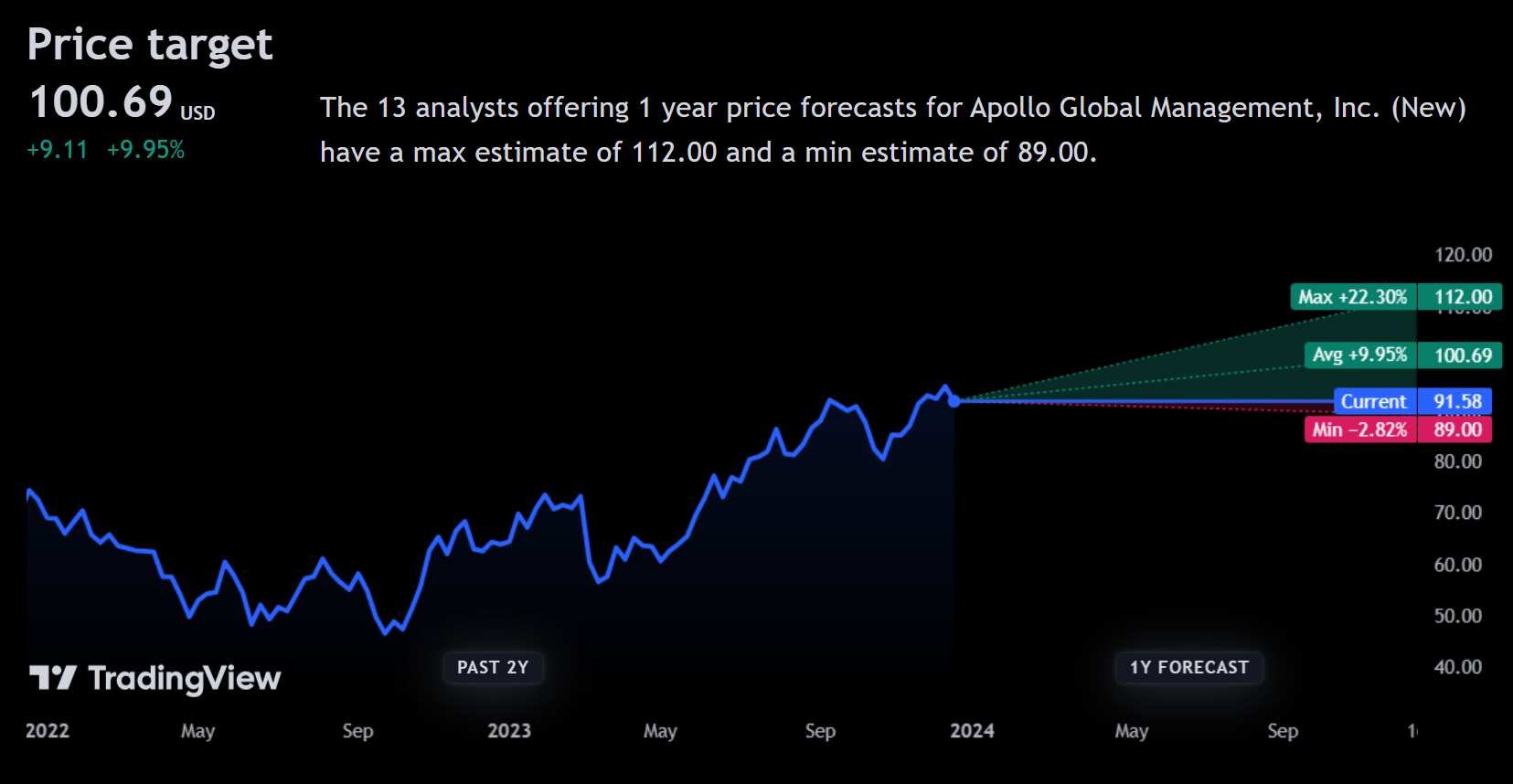

Analysts generally support my positive view of the stock, estimating a 1Y average price target of $100.69, a 9.95% increase.

{kind=link}

TradingView

Even at the minimum projected price target of $89.00, a decline of 2.82%, analysts expect investors to be breaking even net of dividends.

I believe this positive outlook reflects Wall Street's sentiment that Apollo's operational model and private credit focus will yield growth over time.

Risks & Challenges

Higher Cost of Capital May Slow Growth

Although Apollo maintains lower debt/equity levels than its peers and can effectively self-source capital, the company is exposed to the downstream effects of higher rates; there remain fewer higher-grade credit instruments or increased counterparty risk. As such, to manage risk effectively, Apollo must either ensure greater capital buffers or reduce growth.

Greater Regulatory Scrutiny May Limit Overall Upside

Apollo has quite clearly staked its future on the private credit industry and associated organic growth. Therefore, if the private credit industry is limited in any way, Apollo would see the consequences. The most obvious risk to private credit is the SEC or potential scrutiny from Congress, which sees the private equity and credit industry as opaque and potentially systemically harmful. Such thinking and consequent compliance costs may stem the growth of private credit, thus, Apollo.

Conclusion

In the long-term, Apollo's leadership in private credit and origination makes the firm an agile, future-focused firm with tremendous growth potential.

For further details see:

Apollo Global Management Is My Favourite Private Equity Company - Here's Why