APO - Apollo Is The Definition Of Growth At A Reasonable Price

2024-01-09 11:28:07 ET

Summary

- Apollo Global Management is an under-covered and under-appreciated alternative asset manager with high growth prospects.

- The company's business model, which combines asset management with an insurance arm, allows it to charge higher fees and be resilient to high interest rates.

- Apollo stock remains cheap as the market refuses to value Athene at more than 5x earnings despite 15% ROE and growth.

Dear readers,

Apollo Global Management (APO) is an alternative asset manager with nearly half a trillion in asset under management ("AUM"). The company has the size to rival the biggest players in the sector such as Blackstone (BX) or Brookfield Asset Management (BAM), but remains under-covered here on Seeking Alpha and under-appreciated by the market. In particular, APO trades at a significantly lower multiple than its more well-known peers, despite higher growth prospects and a unique business model which allows for high fees and is more resilient to high interest rates.

I've published two articles on APO already, the most recent one from early October can be found here , have been bullish on the stock since $60 per share and have recorded an RoR of nearly 50% from the initial BUY call. My initial thesis was primarily based on Apollo's valuation being below that of peers and also on the fact that I regarded the stock as very well positioned for a high interest rate environment. Little has changed with regard to both of these aspects and today the stock remains my second biggest position in the alternative asset management space, after Blue Owl Capital (OWL).

Since my last article, the company has (1) recorded another great quarter of results (Q3 2023), (2) Apollo's insurance subsidiary Athene has moved out of Bermuda to Delaware which I see as a major positive due to added transparency, despite the fact that it has resulted in a downgrading of Athene's preferred shares from BBB to BBB- and (3) the company seems positioned to deliver good Q4 2023 results which will be released on February 8. All three of these lead me to believe that Apollo is well positioned going forward which is why I reiterate my BUY rating here and dive deeper into Apollo's financials to help you decide whether to invest ahead of Q4 earnings or not.

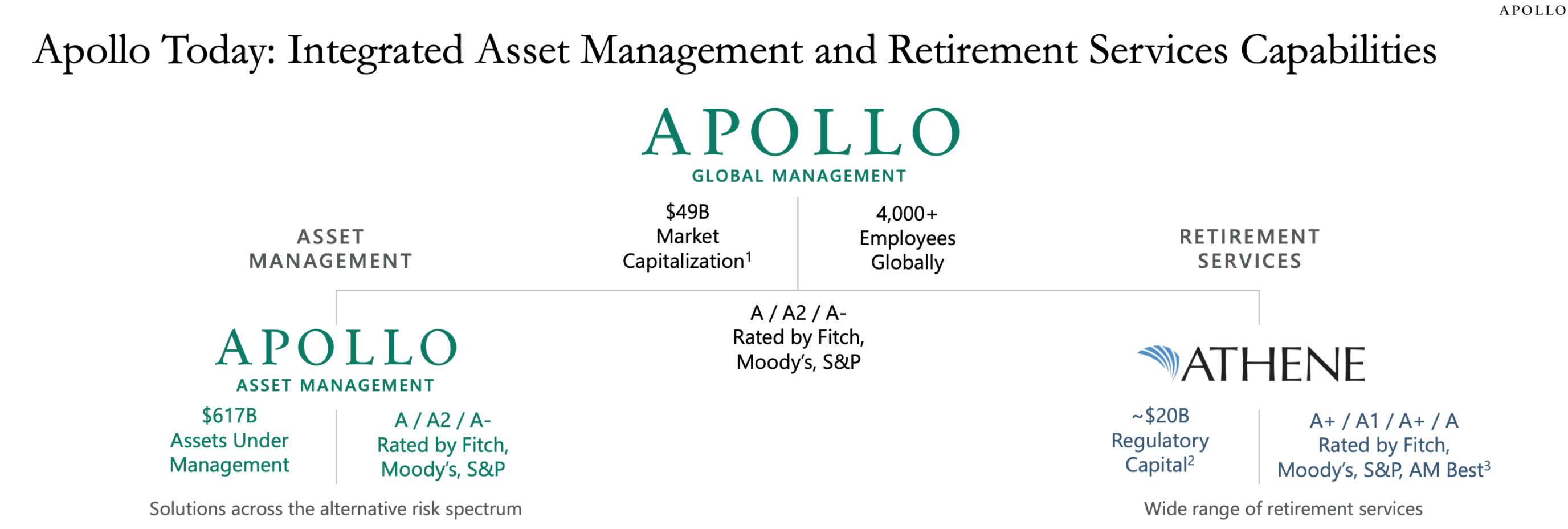

Overview of Apollo

Before diving into the latest available results and valuation, let me quickly recap what Apollo does.

It is, in a way, a combination of an asset light asset manager and an asset-heavy insurance provider (called Athene). In contrast to other asset manager, the insurance arm, which specializes in annuities, forms the very core of Apollo and the asset management business is complementary to it. As a result, inflows to Athene are the single most important driver of Apollo's performance.

{kind=link}

This model also enables Apollo to charge a lot of fees. It works like this.

Future retirees regularly pay money to Athene in exchange for the promise of future annuity payments. Athene takes the proceed and invests in investment grade loans with a higher rate than what's promised to future retirees. The process is done through the asset manager which takes a 0.25-0.30% fee from every dollar, generating fee-related earnings (FRE). Athene then keeps the spread between the higher rate it gets in the originated loan (net of the fee paid to the asset manager and Athene's OPEX) and the rate it has to pay to annuity holders. The spread averages about 1.6% and generates spread-related earnings ("SRE"). Finally, Apollo is able to generate a third layer of fees on every dollar deposited into Athene through its capital solutions business which off-loads the originated IG loans to other institutions.

I like Apollo's model a lot because it takes full advantage of Athene's rapid growth in assets and allows Apollo to charge higher fees than most peers (I dive into the calculation deeper). Moreover, because the business relies so heavily on annuities, which are positively correlated with interest rates, Apollo is incredibly well positioned for a high interest rate environment.

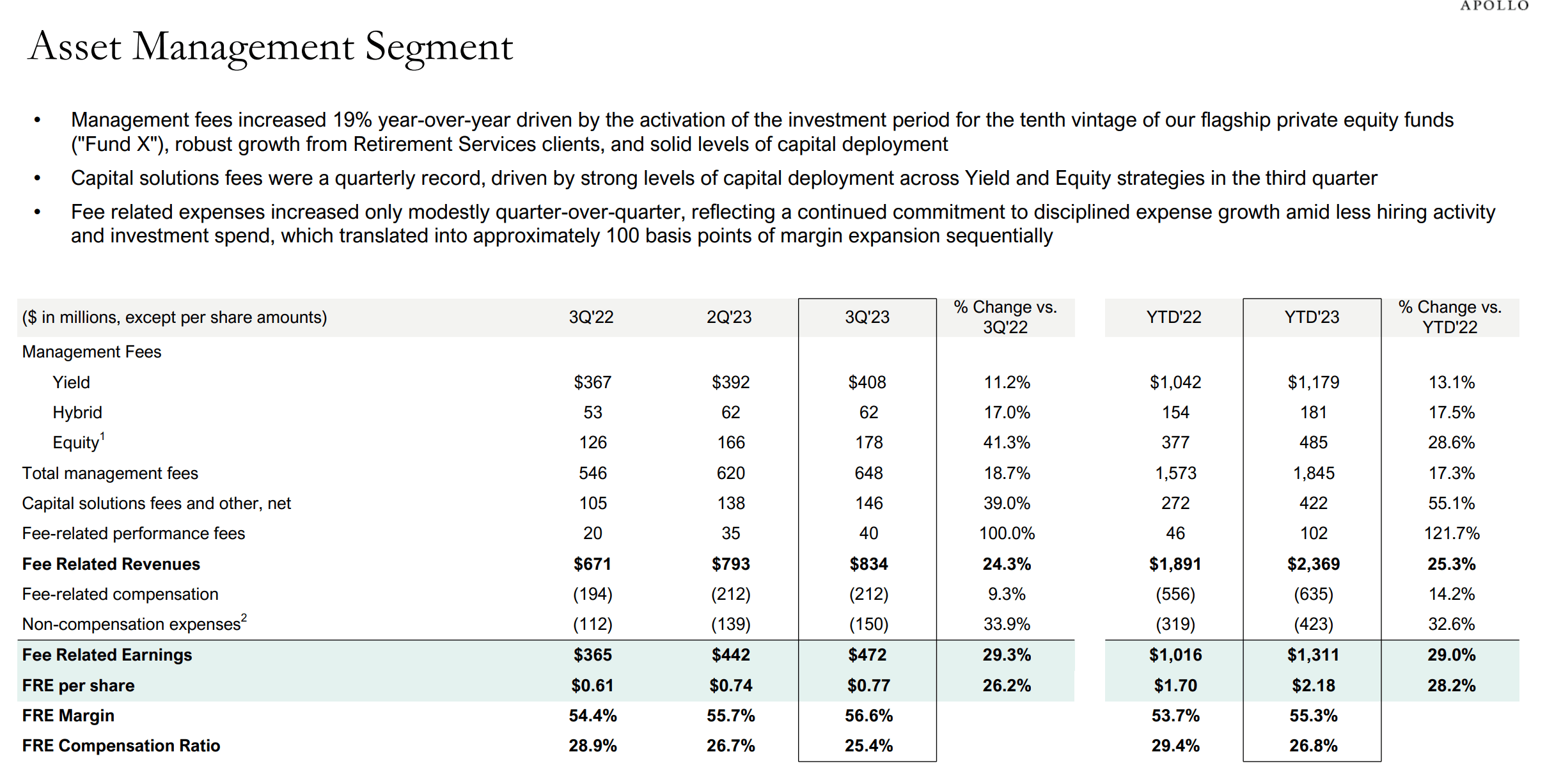

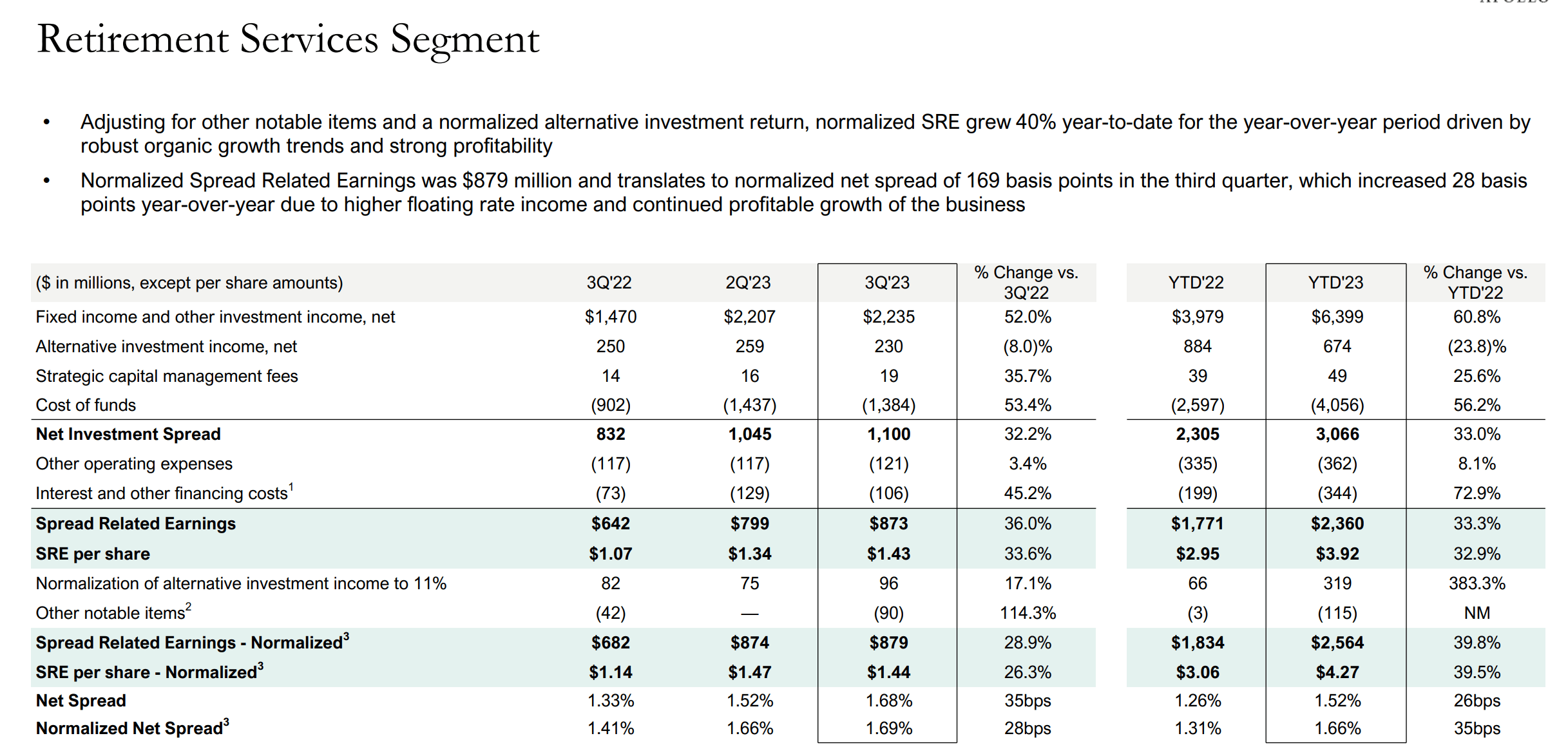

Q3 2023 Results

APO has seen $33 Billion in inflows during the third quarter and $153 Billion over the past twelve months which has contributed to strong 19% YoY growth in Fee-earning AUM.

During Q3 reported in November, Fee-related earnings reached $472 Million, up 29% YoY and Spread-related earnings came in at $873 Million, up a whopping 36% YoY. Year-to-date FRE and SRE growth has been equally impressive at 29% and 33%, respectively.

APO Presentation APO Presentation

{kind=link}

{kind=link}

And thanks to strong AUM growth (especially in Athene) the company seems positioned to deliver on their full year targets of 25% FRE growth and 30% SRE growth in 2023 which would put 2023 FRE at $2.95 per share and SRE at $5.7 per share.

Beyond this year, management expects a slowdown in FRE growth to 15-20% and low double-digit SRE growth, driven by inflows to Athene as well as APO's asset management business.

Financials - What Makes Apollo Different?

Apollo's main differentiator is really Athene which contributes almost two thirds of earnings (YTD SRE of $2.36 Billion vs YTD total earnings of $3.7 Billion) and most importantly allows Apollo to generate a high ROE of around 15%, which is about 50% higher than most insurance peers.

This high ROE is a results of a high assets/equity ratio of 12x and a high net spread which currently sits at 1.66%. With an effective tax rate of 20%, Athene's spread-related ROE sits at 12*1.66%*80% = 15.9%.

Net spread is positively correlated to interest rates, meaning that it tends to be higher in a high interest rate environment. This is another reason why APO performs really well in a high interest rate environment. But I also want to point out, that the 15% ROE isn't a short term phenomenon caused by a recent surge in rates. If we look back as far as Q1 2022 , when interest rates were still low and the 2-year treasury yield was still below 2%, we notice that even back then, net spread sits at 1.48% which corresponds to a ROE of around 14.2%.

So how is it that Athene/APO is able to generate such good returns on equity?

A large part of this is the fact that in contrast to peers, the company doesn't invest solely in bonds, but also in private credit which generally has higher interest rates. Moreover, the company aims to offload 75% of originated loans through the capital solutions division which frees up capital while still generating fees.

For completeness, let's also consider the asset management side which isn't that different (and certainly not better) than other asset managers. APO's FRE margin has improved by about 100bps YTD thanks to less hiring and lower investment spend and now stands at 56%, but still sits below BAM's 60% and BX's 65%.

Apollo also maintains a strong A- rated balance sheet and has $59 Billion of dry powder ready to be deployed into high ROE strategies.

Is Apollo Still Cheap?

A company generating a 15% ROE and growing as rapidly as Apollo is, should trade at a premium, but that is simply not the case for Apollo. While APO has continued to post great results, valuation multiples haven't changed since my original article. I see no reason to change my price target assumptions at this point.

I've previously valued the asset manager at 22.5x fee-related earnings, an assumption that I consider quite conservative in light of peer such as BX or BAM that trade closer to 25-28x FRE.

The market, however, seems to be struggling with valuing Athene above 5-6x SRE which is how much Apollo paid for the company several years ago.

With some simple math, assuming that APO delivers on their 2023 guidance as described above and using 22.5x FRE to value the asset manager, I estimate that the market currently values Athene at just 5x SRE.

Author's calculations

That's very low for a company that has grown at a 16% CAGR since 2008, demonstrated incredible 30%+ growth this year, adds about 15 cents in earnings to Apollo for every dollar that future retirees deposit, and benefits from a high rate environment which happens to be the one we're currently in.

I have no doubt that Athene's business deserves at least a multiple of 8-10x SRE which would put Apollo's fair value today at $110-120 per share, up about 20% from today's price.

Apollo pays a low dividend yield of 1.8%, but with 15%+ future earnings growth and a 20% upside potential from multiple re-rating of Athene it's not difficult to be bullish on APO.

I reiterate my BUY rating here at $95 share and consider APO one of the best positioned companies to outperform over the next two years. And I don't mean just in the alternative asset management space either. I feel strongly that it's better to invest in the stock ahead of Q4 earnings which are very likely to see further growth in both FRE and SRE, driven by net inflows to Athene and a strong net spread driven by high interest rates.

Risks

Before investing, investors should consider that the thesis is based on Apollo reaching their growth targets which may not happen. In particular, if interest rates decline, there is a risk that inflows to Athene will slow as future retirees deposit less money into annuity schemes which become less attractive at lower rates.

Moreover, there's also a risk that the market will continue to value Athene at a low multiple of 5x SRE which is equal to that of a similar insurance provider F&G Annuities & Life (FG). Though it's important to note that FG makes a significantly lower ROE of 10% and doesn't grow their assets nearly as fast Athene.

For further details see:

Apollo Is The Definition Of Growth At A Reasonable Price