APO - Apollo Is Winning The Race And Should Help Compound Your Portfolio

2023-08-16 02:58:26 ET

Summary

- Apollo's Q2 results have convinced many investors, leading to a jump in share prices.

- The company's fee-generating assets under management are growing rapidly, primarily due to inflows from retirement services.

- Apollo's capital solutions business is quickly growing as well, allowing the company to provide capital for major companies and generate transaction fees.

- Apollo has reasonable chances to become a ten-bagger in 2031 for those who invested at the time of the merger with Athene.

I posted my first bullish article on Apollo Global Management ( APO ) in June 2021, shortly after purchasing shares. Those who followed me back then should score annualized IRR close to 23%.

However, until the last quarterly report, quite a few investors were skeptical about APO - their strategy is new and complex and their numbers were not mind-blowing enough. The progress was gradual.

The Q2 results delivered on Aug 3 have convinced many. At least, that was my impression from reading comments on my articles and other publications. The shares jumped from ~$81 to ~$87 and then retreated to the low eighties again.

This post will briefly review the Q2 results and share my opinion on what can be expected in the future and how APO is positioned compared with other alt managers. I will also try to fantasize (always fun, often useless, sometimes harmful) regarding whether APO can become a ten-bagger. As usual, I will try to avoid repetitions with my previous publications and refer to them when necessary.

Nothing is guaranteed in the stock market and please do not take the picture above as the happy end. The journey goes on.

Q2 Results

Every quarter APO delivers a waterfall of numbers. We will focus only on several most important ones keeping in mind that the company consists of alternative asset manager Apollo ("old Apollo") producing primarily fee-related earnings ("FRE") and some carry (carry and investment income constitute the so-called Principal Investment Income or PII segment), and retirement specialist (or insurer or annuity provider) Athene that generates spread-related earnings ("SRE").

Arguably, the single most important number is fee-generating assets under management ("FGAUM") displayed below.

Company

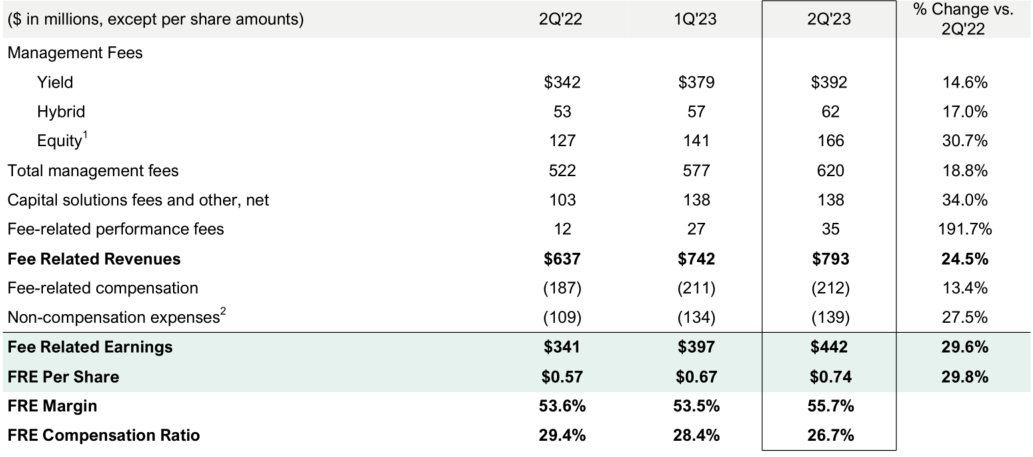

It is hard to miss on this slide that FGAUM grows fast (21% over the last year) primarily due to Yield (this is Apollo's term for fixed-income assets).

The Yield business is mainly growing due to inflows from retirement services (primarily Athene but also its smaller European counterpart Athora, controlled and partially owned by Apollo - more about it later). Athene's inflows have been exclusively organic for the last several years. Let me explain what it means and why it is notable.

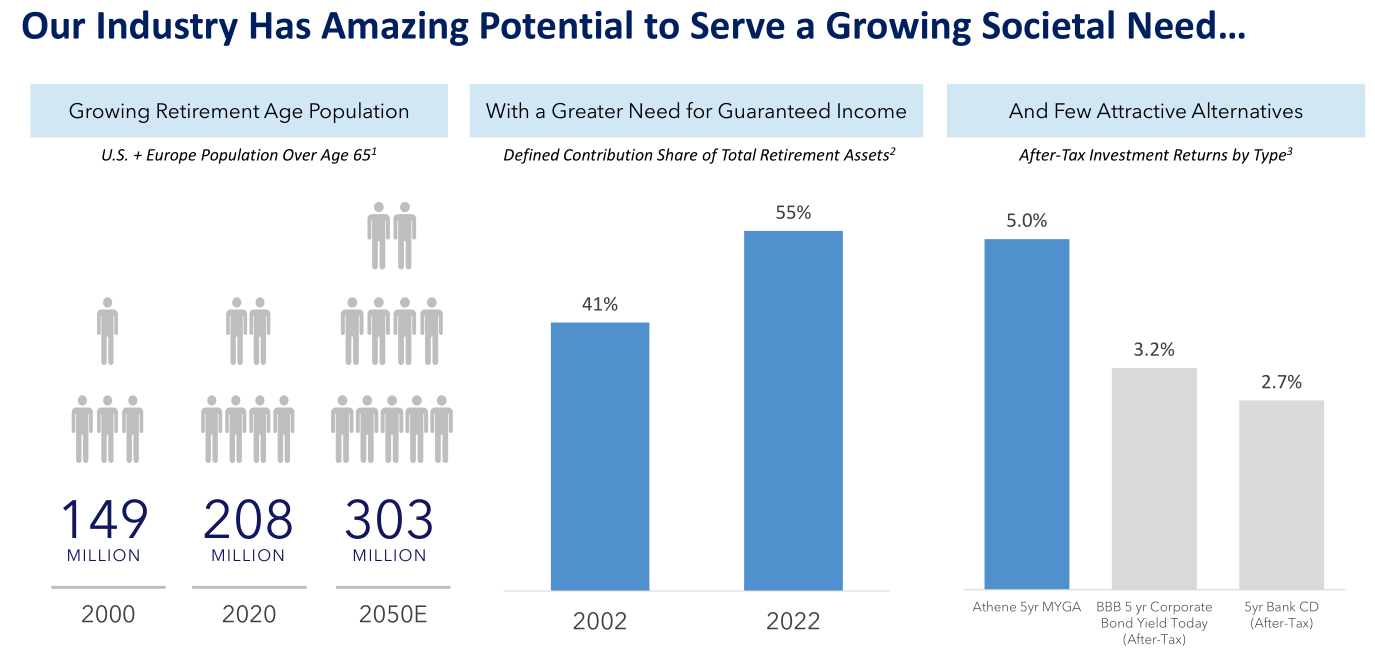

The number of retirees in the US (as well as in the rest of the world) keeps increasing due to population growth, the retirement of baby boomers, and higher longevity.

{kind=link}

A fraction of retirees always use fixed annuities as their main or supplemental retirement vehicle. Today fixed annuities are particularly attractive due to high interest rates. Athene is the #1 fixed annuity provider in the US, and it has certain cost advantages vs. competitors.

Imagine a big square with tens of millions of people on a hot day. Many stands sell cold drinks on the square, but one stand is bigger than others, has higher throughput, and has better or similar prices. People will be flocking to this stand without any additional efforts from its owner. This is Athene during the period of high interest rates. Every annuity purchased from Athene increases FGAUM and FRE. But it also increases Athene's balance sheet and SRE. Growing already dominant Athene has become the most profitable activity for APO.

Let us focus on FRE now. We can expect that management fees should be growing slightly slower than FGAUM because Yield assets, on average, are subject to lower fees than, say, private equity funds. The slide below confirms it. Management fees grew at ~19% in Q2. This is still very high but importantly FRE grew faster than both management fees and FGAUM.

{kind=link}

There are two reasons for it. First, due to economies of scale and certain changes in compensation structure, APO has reached operating leverage and increased FRE margins from ~54% a year ago to 56%. This is not the end of it as APO is targeting a FRE compensation ratio of 25% vs. 26.7% today.

Secondly, APO is quickly growing its capital solutions fees (38% year-to-year in the table!). Here I need to explain what Apollo Capital Solutions ("ACS") business is and why it matters.

Consider a situation when a company needs some sort of financing. APO is unique in its ability to offer different kinds of loans or equity or a combination of them across the spectrum: it can be leveraged loans, investment grade loans, asset-backed financing, debtor-in-possession loans, preferred shares, private equity - you name it. But how to source capital for all these loans (as well as for other loans, including consumer credit, that APO's originating businesses produce)?

APO has three sources: private credit funds and BDCs for low-grade loans, retirement services balance sheets for high-grade loans (Athene, Athora, other reinsurers controlled by APO), and critically, syndication and distribution mostly but not only for high-grade loans. As long as APO is successful in syndication and distribution, the originated loans can end up within hedge funds, mutual funds, banks, insurers, and other unaffiliated financial institutions. This can allow APO to quickly provide big chunks of capital for the biggest companies in the world. ACS has already handled transactions for the likes of Softbank, Hertz, Anheuser-Busch, Air France, and so on.

Every step in the chain of events that comprise a capital transaction generates transaction fees. Often a capital transaction can lead to transaction fees, management fees, and SRE simultaneously when, say, a part of a loan ends up on Athene's balance sheet.

CEO Marc Rowan often repeats: Athene wants 25% of everything and 100% of nothing. It means that Athene strives to retain only a fraction of every originated investment-grade asset. APO already originates more high-grade debt than Athene needs, so it is a must to distribute the balance while keeping alignment with clients.

Apart from a strong contribution to FRE, further development of ACS may put Apollo in the center of the financial world where giant banks are playing. In its turn, it will lead to uncountable direct and indirect advantages.

Please note that while often playing as a bank, Apollo/Athene combination has several advantages over banks: 1)it can quickly originate bespoke loans across the credit spectrum; 2)it is not regulated as a bank and has more latitude; 3)as an insurer, Athene matches its assets and liabilities, while banks fund long-term loans with short-term deposits that may cause instability like during the recent banking crisis.

Retirement services did even better than asset management in Q2. First, Athene's assets grew 16% year-to-year. And secondly, due to a high investment spread, SRE grew 76% vs. a year ago. This is a one-off. Under normal circumstances, we should expect SRE to grow in line or slightly higher than assets.

In Q2, Apollo generated insignificant carry because of unfavorable markets but it did not prevent the quarter to be outstanding. Adjusted net income per share ("ANI" or distributable earning - the ultimate number for alt asset managers) was $1.70 in the quarter vs $0.96 a year ago.

In previous posts, I suggested a simplified model to value APO. Without going into detail here, I use only after-tax FRE and SRE discarding both volatile PII and Holdco costs (over a full year, PII is always bigger than Holdco costs). My multiples are 20-25 for FRE and 10-15 for SRE (they are not arbitrary, I substantiated them in one of my previous posts ). This model produces a $85-116 fair value range at the end of 2023 and APO may trade close to $100 in early 2024.

New preferred stock

On August 8, APO filed an SEC form detailing Series A Mandatory Convertible Preferred Stock. Issued at $50 per share, it will be paying a 6.75% annual dividend. It should start trading on the NYSE within 30 days under the symbol APO PR A.

The Mandatory Conversion Date is July 31, 2026. The conversion ratio will be between 0.5052 and 0.6062 of APO's average trading price shortly before the Conversion Date (0.5052 if APO price is above $98.97, 0.6062 if APO is below $82.48, and an intermediate figure for APO trading in-between).

Does it make sense to buy preferred shares assuming they will be trading close to $50? Hardly, if you are an Apollo bull. Let us assume APO will deliver a 15% annual appreciation and be trading close to $120 in mid-2026. Then, a preferred holder will receive 120*0.5052~$60 in APO's shares. It translates to ~6% capital return plus 6.75% in dividends. The total annualized return will be equal to ~13% vs. ~17% for an APO shareholder (15% appreciation + 2% in dividends). The gap between common and preferred returns will be higher if APO delivers more than 15% per annum. Being hopeful for ~15-20% annual appreciation, I will skip preferreds.

This arithmetic should not surprise anybody. APO management holds close to one-third of common stock and nothing compels APO to issue preferred shares. They are doing it only because it benefits common shareholders. Since preferred returns are paid out of common shareholders' pockets, common shares are expected to deliver higher returns. Hence, the issuance of preferred shares is one of the most bullish signals APO investors could receive.

Regarding proceeds, the SEC filing states the following:

The Issuer estimates that the net proceeds to it from the offering, after deducting the estimated underwriting discounts but before estimated offering expenses payable by it, will be approximately $1,219 million (or approximately $1,402 million if the underwriters exercise their over-allotment option to purchase additional shares of the Mandatory Convertible Preferred Stock in full). The Issuer expects to use the net proceeds from the offering to accelerate its Retirement Services growth, helping Athene Holding Ltd., the Issuer’s subsidiary that conducts its retirement services business, capitalize on attractive opportunities available in the current market environment.

In my opinion, it means one of two things: either Athene can execute an attractive acquisition, most likely internationally, or the US annuities market is so hot that additional capital is needed not to miss the opportunity.

We will know the truth shortly. And by the way, dilution from the preferred shares will be minuscule - ~2 million additional shares vs. ~595 million outstanding.

Can Apollo become a 10-bagger in 10 years?

If APO can deliver 24% annually (including dividends), it will double in 3 years, quadruple in 6 years, become an 8-bagger in 9 years, and be close to a 10-bagger after 10 years. Since APO has already delivered about 23% IRR over my 2.2 years of holding, it is a candidate.

Before investing in APO in 2021, I checked its financial history: from 2011 to Q1 2021, it had delivered a ~19% annual compounded return in appreciation plus significant dividends. So its total return was probably close to the same 23% annualized.

Within APO, SRE is much higher than FRE today ($2,327M vs $1,750M in 2022) but FRE is expected to grow faster as every incremental dollar on Athene's balance sheet generates both FRE and SRE. However, there are many additional sources of FRE such as ACS fees, Equity and Hybrid fees, Yield fees on assets beyond Athene's balance sheet, various funds for retail investors (wealth channel), Athora's balance sheet, and so on.

These additional fee-generating opportunities are very substantial. You can check the slide with management fees above: Equity, Hybrid, and ACS fees combined are roughly equal to Yield fees, only part of which is attributable to Athene.

Consider Athora for a further example. It exists as a separate private entity for only five years but towards the end of 2023 should have ~$100B of AUM. Since Athene owns only ~25% of Athora, the latter's contribution to FRE is much higher than to SRE. On top of it, Athora is scaling up quickly following Athene's trajectory adjusted for the European insurance landscape.

Of note, FRE also enjoys higher multiples and its contribution to the value will keep increasing disproportionately. The key to becoming a 10-bagger is the fast growth of FRE, north of 20%. And this is possible because APO's total addressable market ("TAM") is gigantic.

{kind=link}

APO estimates its TAM as $40T in investment-grade private credit that may replace traditional fixed-income securities in various portfolios. If this estimate is correct, with less than $400B of high-grade Yield assets, APO's share is less than 1% of TAM. There is plenty of room to grow.

SRE should grow slower, at mid-teens at maximum. However, the market may assign higher multiples to SRE.

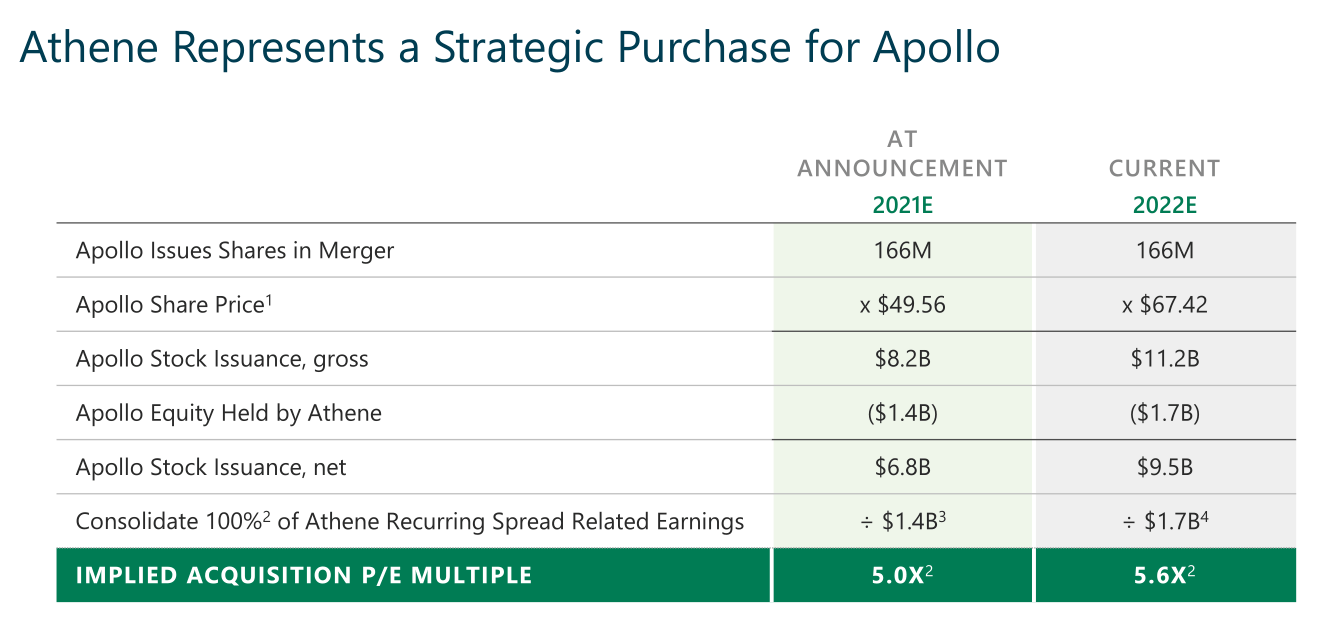

APO paid very little for Athene in 2021 as displayed on the slide below.

{kind=link}

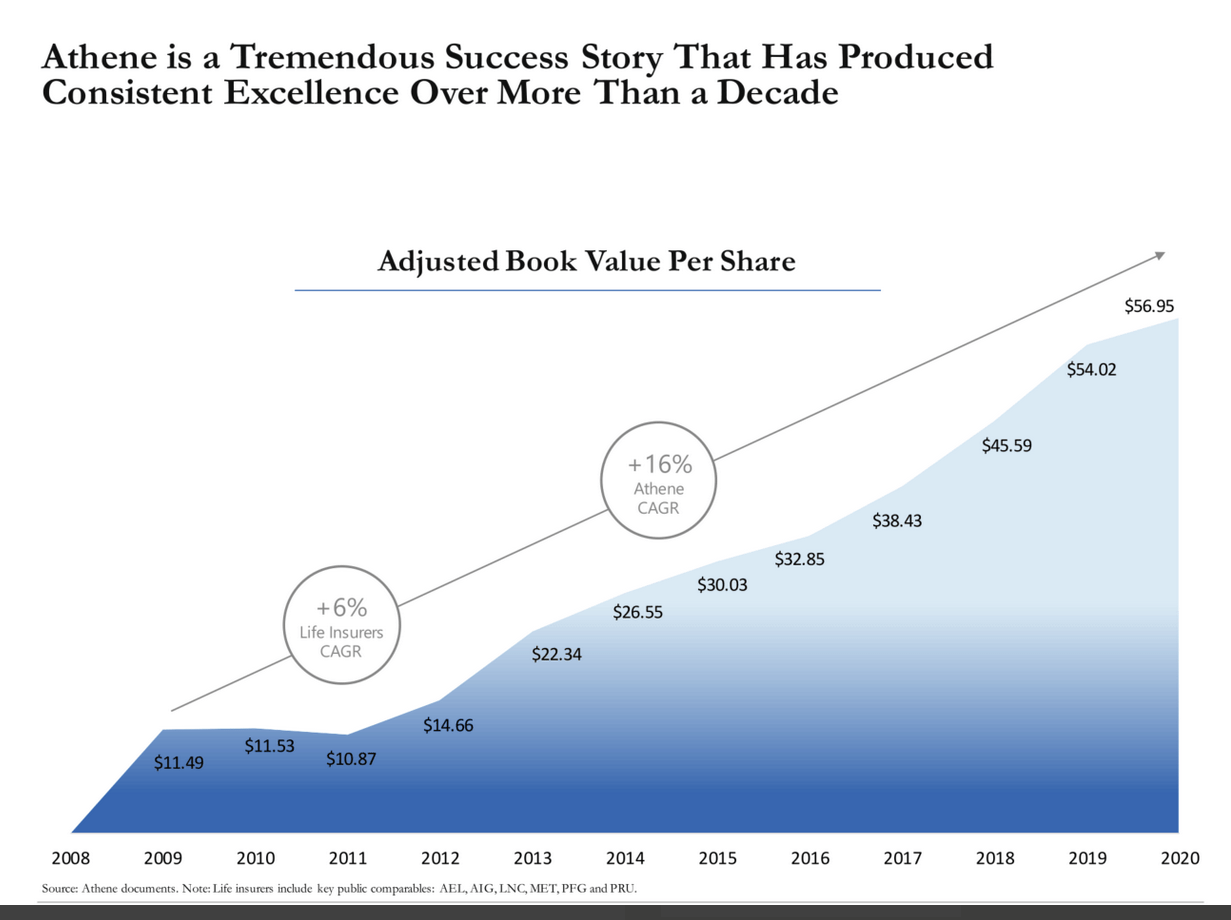

It was only two years ago and I doubt anybody would seriously value Athene at 5-6 multiples today. My multiples for Athene are 10-15, but many investors are still reluctant to assign more than 10 for a life insurer. Meanwhile, Athene keeps printing money at 16-17% ROE year in and year out since 2009.

{kind=link}

Assuming no changes, these numbers will affect the market's mind sooner or later. The combination of growth in the mid-teen range along with an expansion in multiples could potentially lead to SRE's contribution growth surpassing the 20% mark.

Our exercise suggests there are chances for APO to become a ten-bagger in 2031 for those who invested at the time of the merger with Athene.

Conclusion

Within the promising alt management space, I am trying to place my long-term bets on companies that have structural advantages compared to peers. It does not guarantee the result but seems a reasonable strategy. Apollo has two unique differentiators: Athene and the focus on investment-grade debt.

For further details see:

Apollo Is Winning The Race And Should Help Compound Your Portfolio