AMEH - Apollo Medical Holdings: Good Company Not Quite A Hold

2024-01-16 20:07:50 ET

Summary

- Apollo Medical Holdings provides a healthcare tech platform that aims to increase accessibility and efficiency for patients and providers.

- The company has experienced significant growth in the past five years, with revenues increasing by 10x since 2014.

- ApolloMed's business model simplifies billing processes and reduces staff and payroll burden for healthcare practices, leading to strong profitability.

- Despite these things, the price needs to offer a discount for some of the uncertainty ahead.

Apollo Medical Holdings or ApolloMed ( AMEH ) is a company that hosts a healthcare tech platform, designed to increase accessibility and efficiency for patients and providers alike. It's seldom been discussed on Seeking Alpha, but its first coverage was by none other than Hindenburg Research , a well-known and seasoned stock research firm, back in 2018. At that time, it indicated how a float-calculation error led to its listing on the Russell Index and, consequently, how purchases to include it in those funds led to its price being driven up. They then gave insights into how the business's structure suggested that it could be difficult to value accurately and how such an artificial price hike could lead it to a huge correction.

In the five years that passed, the company has experienced a lot of growth, and that index error is no longer relevant. It's therefore worth taking another look at what exactly we have with AMEH and—with it being up two and a half times from its price when Hindenburg cautioned against it—if there's another opportunity or more overvaluation.

Financial History

First we'll look at the numbers behind this company over the last decade. We'll include YTD 2023 data as well.

Author's display of 10K/10Q data

{kind=link}

First thing to note here is the continuing growth of revenues, up around 10x where they were in 2014. It's a CAGR of almost 26%! Let's break it down a bit further with a view to the cash flow situation.

Yellow bar only subtracts PPE from OCF. Green bar includes the impact of M&A.

Author's display of 10K/10Q data

{kind=link}

Cash flows show a trend toward growth, but there is some subtlety to it. Often when determining the true earnings of a company from the cash flows, an investor would look at Operating Cash Flows and subtract cash spent on additions to Property, Plant, and Equipment. For some businesses, it is the case that Mergers and Acquisitions can account for significant cash outflow too.

Between 2014 and YTD 2023, there was always cash spent on PPE, totaling a net $74.5 in expenditures. While M&A only occurred seven out of ten years, it accounted for a net $53m in expenditures, a couple even gaining cash for the company. I'll get into this more later on, but I wanted folks to understand (and the chart above illustrates this) how much M&A has been a big part of the ApolloMed's financial picture and strategy.

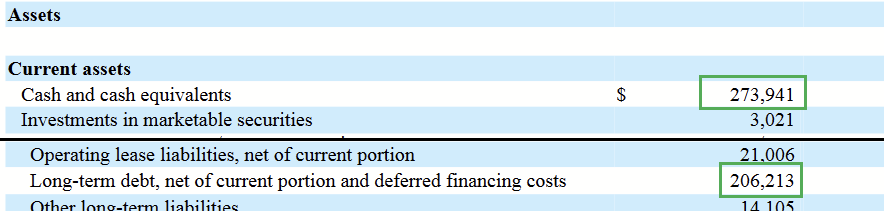

{kind=link}

In Q3, the company reported about $274m of cash, on top of about $206m in long-term debt.

Business Model

First, let's get a grasp on this business model, which has some complexity to it. I thought about how I would want to explain it to a reader, while also doing the material justice. I even consulted with a close friend who's worked in medical billing and has a more direct, hands-on understanding of this kind of business than your average person.

Platform That Simplifies

As she explained to me, it's ultimately not that complicated, and the complexity is actually where ApolloMed adds value. In healthcare, billing comes in many forms and layers in its cycle. For a lone medical practice, having the staff experienced and knowledgeable enough to process all of this can be a huge strain. Even if the turnover rate for an office isn't bad, it's very time-consuming and a high payroll cost.

Nov. 2023 Company Presentation

{kind=link}

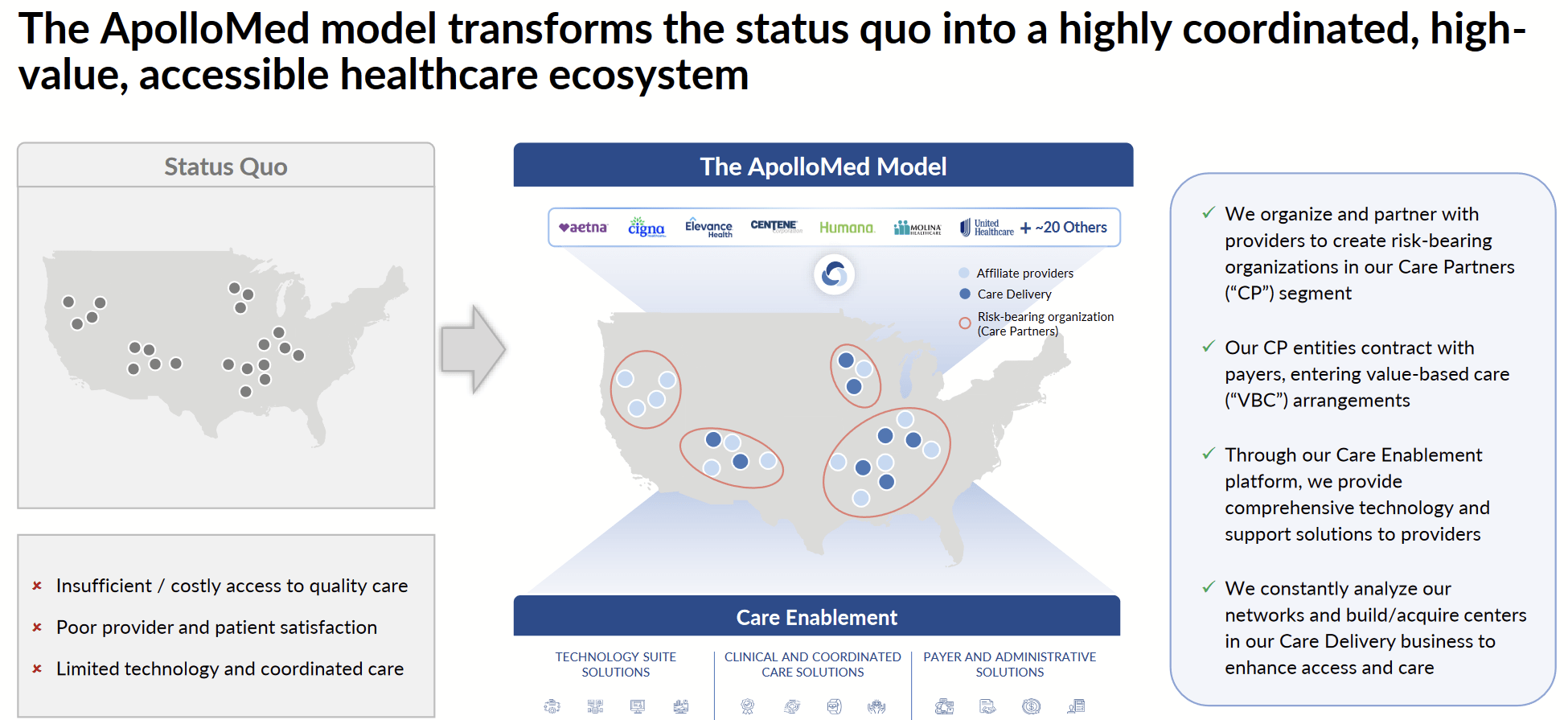

A technology-driven platform to connect patients and providers reduces this headache significantly and in a scalable manner. That's why this is such a profitable company that has enjoyed strong growth over the past decade.

Put another way, the company is able to band isolated practices and other firms into a single-payer system.

Nov. 2023 Company Presentation

{kind=link}

For a very detailed breakdown, I think ApolloMed's Form 10K is going to be the most concise.

The bottom line for something like this is that it speeds up billing processes, minimizes clerical errors, and relieves a lot of staff and payroll burden for smaller practices (which is still a benefit to larger players).

{kind=link}

Nevertheless, I will highlight that the company's largest source of revenue is capitation .

Variable Interest Entities

This detail will be important, though. In addition to its subsidiaries, the company operates through several Variable Interest Entities (VIEs) as part of its model. This is because some states restrict non-physicians from having ownership in businesses that provide healthcare. A VIE is ownership in a separate entity, as a workaround. Consequently, to quote the company's 2022 10K:

Therefore, in addition to our subsidiaries, we mainly operate by maintaining long-term MSAs with our affiliated IPAs, which are owned and operated by a network of independent primary care physicians and specialists, and which employ or contract with additional physicians to provide medical services. Under such agreements, we provide and perform non-medical management and administrative services, including financial management, information systems, marketing, risk management, and administrative support.

Hindenburg also discussed this in its articles from 2018. Because the company reports its consolidated financial results, we get information from ApolloMed proper intermixed with that of the VIEs. While the assets of the company's subsidiaries and VIEs are outlined in detail separately from the consolidated financial results, this is not done for the revenues. I'll quote some of what Hindenburg had to say at the time:

The company does not report deconsolidated revenue, but Q/Q consolidated revenue declined modestly from the latest March to June quarters. On the earnings side, Q/Q earnings attributable to ApolloMed increased by a robust 23%, but given the limited data points post-merger it is difficult to establish a long-term trend for either revenue or earnings.

Now, it's been five years since then. I believe we have a better idea now of what kind of company ApolloMed is after the merger that had occurred there. Yet, since VIEs aren't quite the same as direct ownership in a business, it's still important for anyone looking at ApolloMed to understand going forward.

A Look to the Future

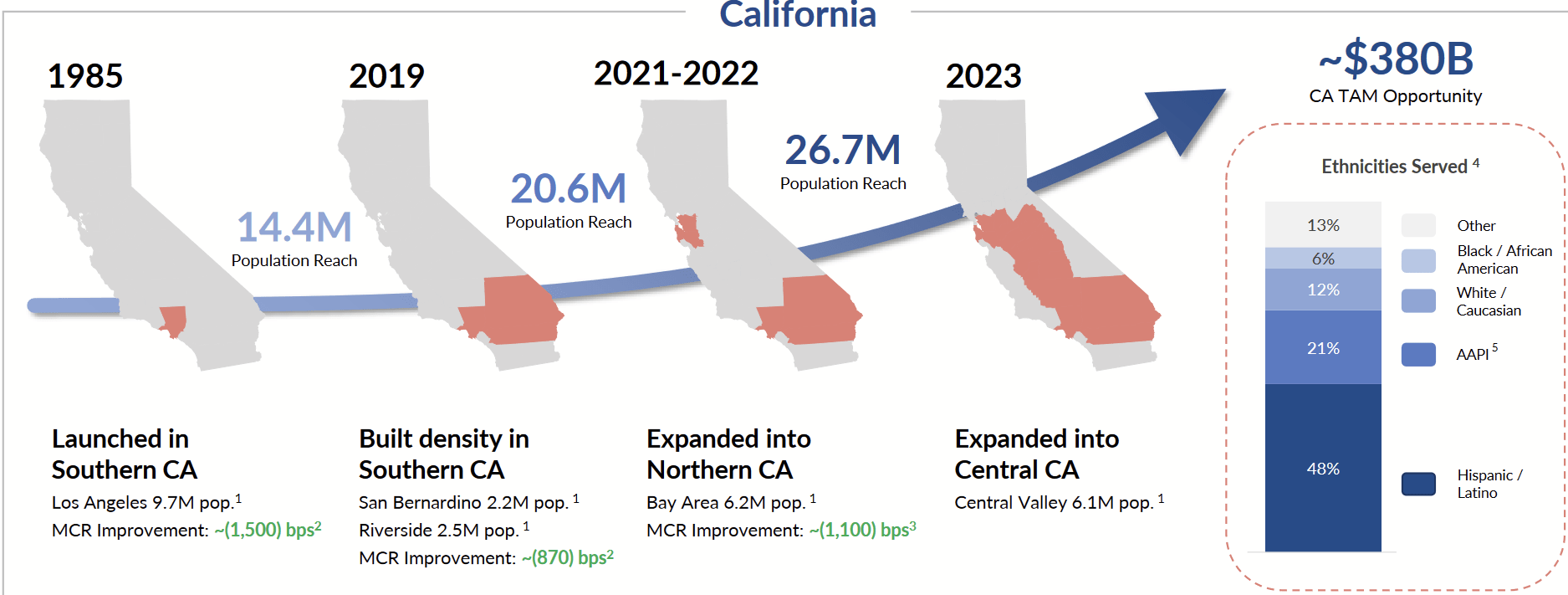

Expansion into Other States

The company has very strong growth ambitions. Nearly all of its business is in Southern California, where most of its growth occurred only recently.

Nov. 2023 Company Presentation

{kind=link}

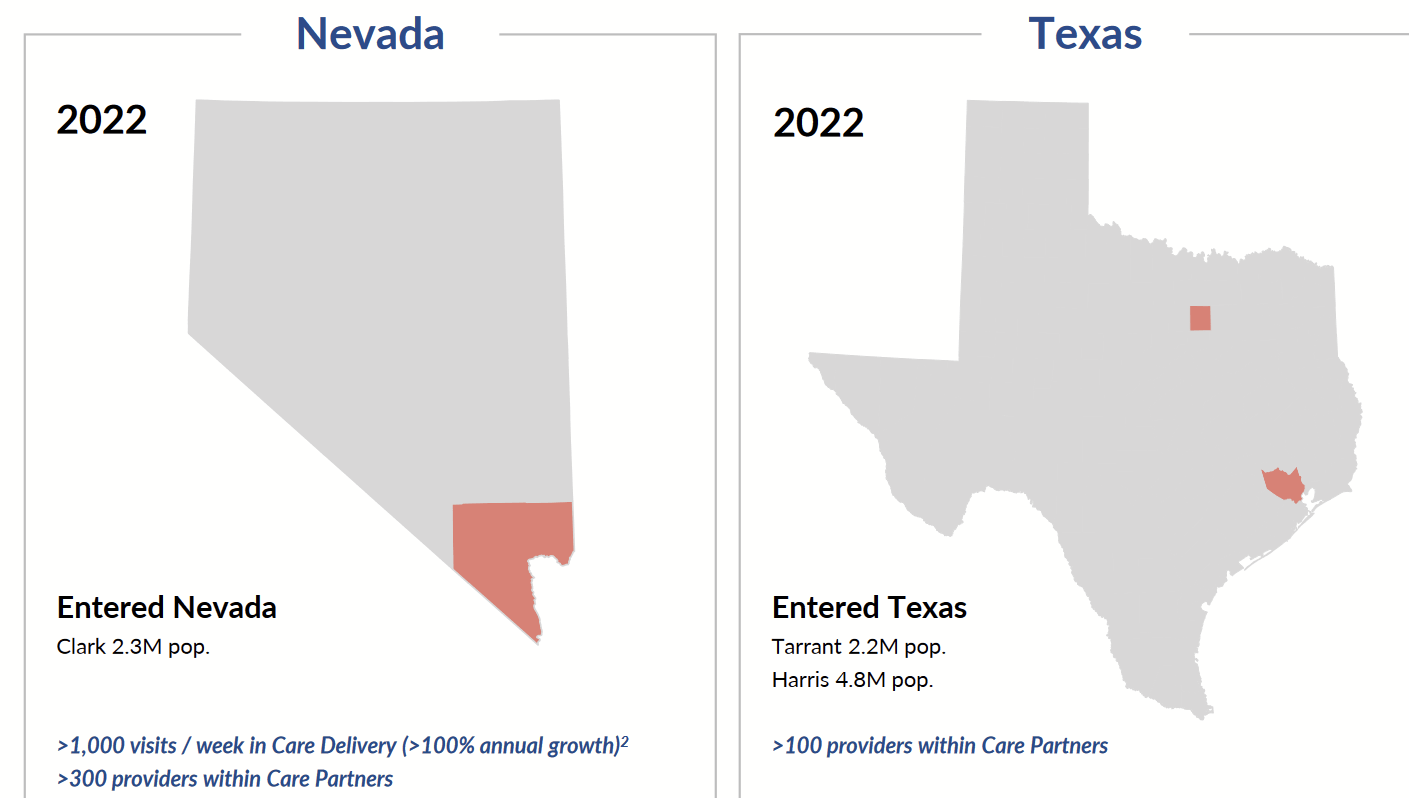

With the economy of scale they've been enjoying, they have begun to leverage their working model into expansion in other states like Nevada and Texas.

Nov. 2023 Company Presentation

{kind=link}

The company has potential for nationwide growth, and so far that hasn't stopped. Again, revenue growth has been about a 26% CAGR, and that's focusing principally on southern California, with the rest of the country available for expansion. The larger they get, the more effective their risk-sharing, single-payer model becomes. The primary method for growth will likely be more M&A. It's the just the easiest way to get new accounts, and it works with practices and clinics that are already established.

While a growing company is an attractive investment, let's consider possible foils to this story.

Competition

ApolloMed is not the only company with tech platform for a payments and billing in healthcare. While they have done well in their own turf, expansion into other states means that they'll run into rivals vying for that market share. While this doesn't endanger the company's current standing, it could slow down the high rate of growth that some investors expect to continue.

As the growth in Nevada and Texas proceeds, we'll want to observe if this is occurring as smoothly as has been seen in southern CA.

Regulations

Healthcare is highly regulated industry, both at the state and federal level. This is why the VIEs I mentioned earlier even exist. Changes to the law concerning medical practice itself or insurance could have impacts for which the company is not ready. As it aspires to acquire market share in other states, whose laws and practices will be less familiar to ApolloMed, the potential for this increases.

VIE Structure

While I believe the company reports financial data about their VIEs as directed by law, that doesn't mean their value to shareholders is going to be a 1:1 equivalency to business operations that are owned directly by ApolloMed. As the company expands into other states that have similar requirements, it will likely have to create more VIEs to do this. This means that the financial structure of the company could become increasingly complex and difficult to value accurately over time. The practical risk here then is that the long-term holder may have trouble "maintaining the pulse" of the company.

Valuation

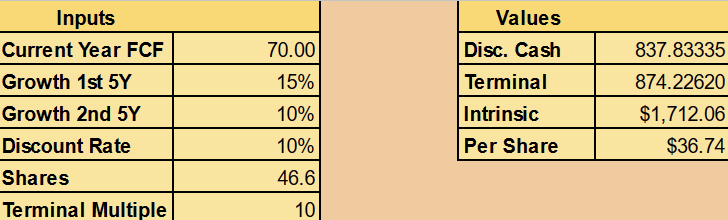

With the growth trend, we can make a valuation through Discounted Cash Flow. I'll calculate it with the following assumptions:

- $70m in annual cash flow

- 15% average growth the first 5 years

- 10% for the second 5 years

- Terminal multiple of 10

Cash flows over the last decade were a bit volatile but leaned toward growth, with most of it happening in the latter half. As such, I believe $70m is a reasonable, lower estimate of the average cash the company can earn each year. I won't assume as high as 26% growth. The reason is that I want to allow for unexpected barriers to growth as the company spreads into new states and encounters novel problems not found in southern SA. Higher rates like 26% can often be hard to sustain as well.

I do think 15% is at least a fair assumption, given its current growth, the robustness of its platform, and the continuing rise of demand for healthcare spending broadly. I'm going to guess that momentum slows down to 10% as it runs into potential competition. I'll give a terminal multiple of 10, as the company will likely have more of the country to penetrate in the decade to follow this, on top of new revenue opportunities it could leverage with a more mature ecosystem.

{kind=link}

That gives an intrinsic value of $36.74, which is very close to the current share price as I write this. Perhaps this means the market, on average, has very similar assumptions. Where many might say this company is a Hold at such a price, I nevertheless consider it a Sell here.

The reasons are simple. We know that the VIE structure can complicate the valuation, since it's mixed into the consolidated results. I think a margin of safety is warranted before buying into it. At the very least, I'd want to see the shares trade around $30 before buying, which occurred briefly last fall.

Similarly, there's no clear benefit to holding right now if it's too high to buy. There's no dividend. It's not about to spinoff shares of a new company that have hidden value. There's no tender offer for $45 being made. I suspect investors can look and find companies trading at a discount, so their money would be better invested there until a better price for AMEH comes along.

Of course, with FY 2023 financial results on the horizon, investors may want to reassess if my current valuation is too conservative.

Conclusion

ApolloMed made great strides to grow its business with a handy platform that has simplified billing process and united different medical practices into a single-payer ecosystem. With an engine of cash from its network across southern California, the business is well-capitalized to penetrate markets in other states.

Yet, the VIE structure that regulations require in many states could result in a financial entity that is difficult to value accurately, and new states come with new challenges. Investors should watch this company carefully and study its progress in Nevada and Texas over the next couple of years. As long as ApolloMed can execute on that, it has the makings of a great business. Until then, holders might be better off selling and putting their money into a company with clearer cash flows and steeper discounts.

For further details see:

Apollo Medical Holdings: Good Company, Not Quite A Hold