AMEH - Apollo Medical Holdings: Rich Premium But Returning To Its Former Self

2023-08-02 08:27:12 ET

Summary

- Apollo Medical Holdings' share price has dropped over 30% in the last year, making it more reasonably valued.

- The company has recently signed an agreement to acquire assets in Texas, expanding its operations and potentially increasing revenues.

- AMEH's margin profile is not ideal, with low gross margins, but its improving FCF margin and strong partnerships are positive indicators for future growth.

Investment Outline

The share price of Apollo Medical Holdings ( AMEH ) has been nothing but disappointing in the last 12 months, down over 30%. The company is not that large with a market cap of just $1.7 billion. The trend for the EPS seems to be upward though and the drop in the share price has brought AMEH into more reasonable levels in terms of valuation sitting at a p/e of 30. To spoil the rating I have for AMEH this 30x earnings multiple is still too high to pay for the business in my opinion. To make the most from an investment we need to get in at what we think are undervalued levels to secure strong returns. Right now AMEH doesn't tick any of those boxes for me.

The company has operations in the United States where it provides medical care services and has become a very popular health management and healthcare delivery platform for professionals. EPS has contracted from the highs in 2021 but the outlook seems to be that AMEH will eventually return to those levels and that makes me optimistic enough to have a hold rating for AMEH.

Recent Developments

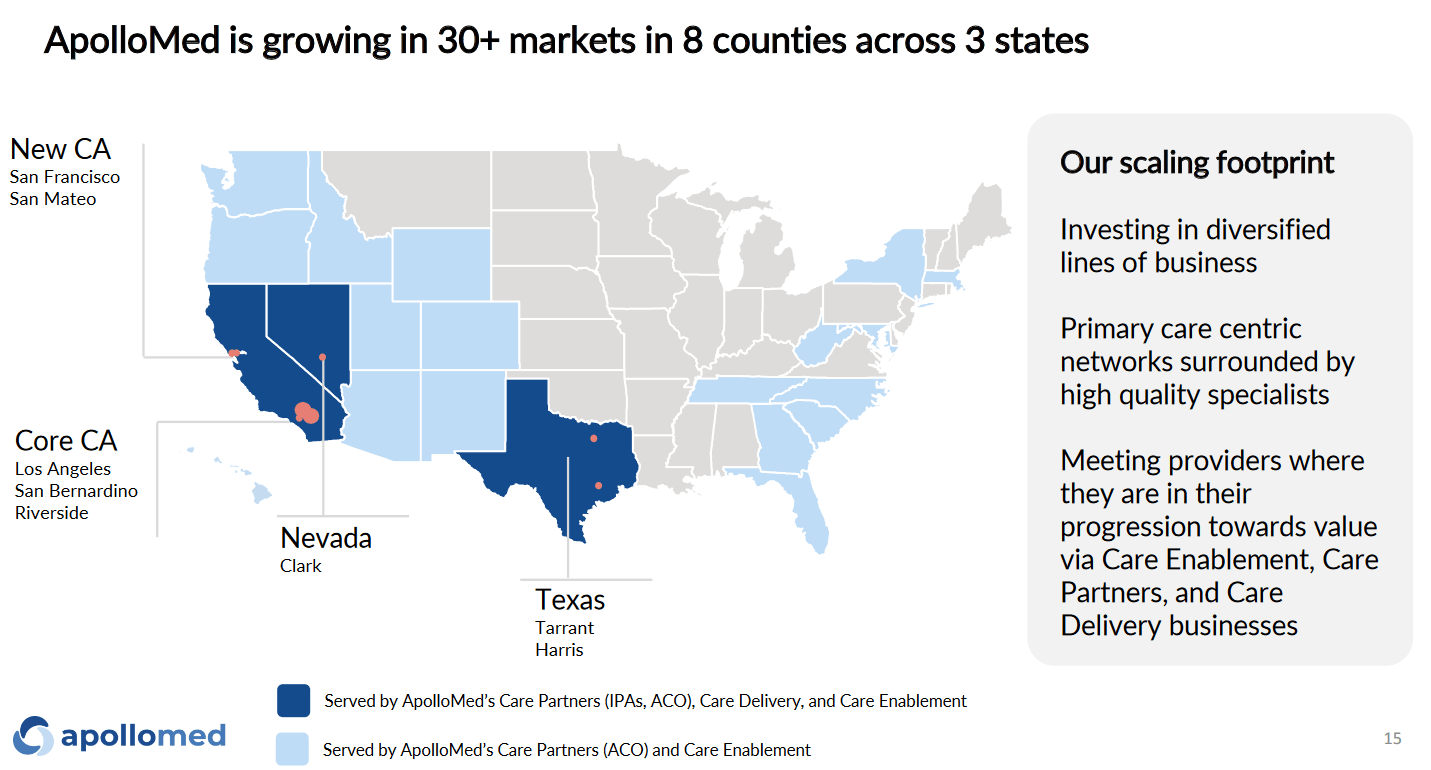

In recent news, AMEH announced on July 12 that they have signed a definitive agreement to acquire assets of Texas independent providers. This move is expanding the operations for AMEH into Houston and will in the long run bring in additional revenues for the business. The Co-CEO Brandon Sim of AMEH said the following about the news, "We are thrilled to begin partnering with some of Houston's most esteemed providers in providing value-based care services for their patients. Partnering with TIP's high-quality, community-focused providers accelerates our expansion in Houston and represents the continued execution of our strategy to empower providers in this key new geographic market to deliver equitable, patient-focused care to their communities".

I think the comment highlights that AMEH is not standing still whilst competitors are making moves. Strategic investments like this efficiently broaden the services and offerings of AMEH.

{kind=link}

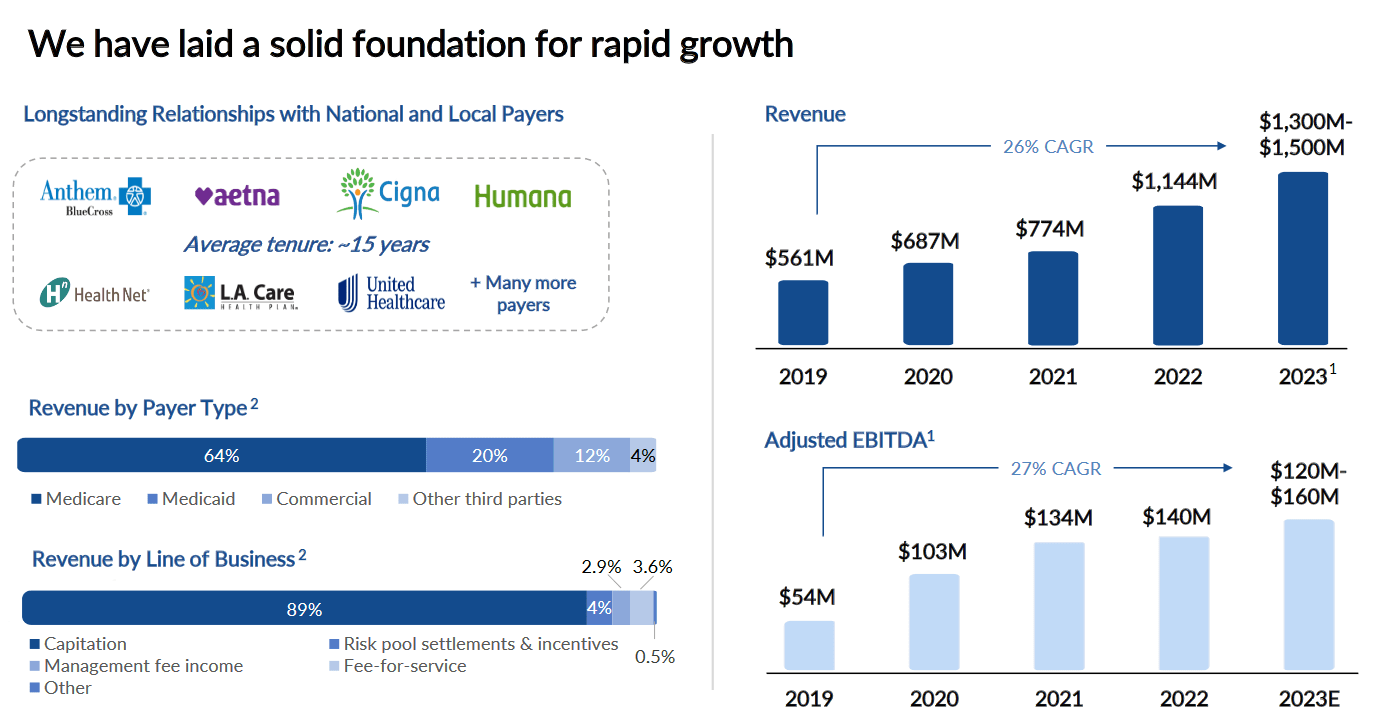

AMEH has been very focused on laying the support for long-term growth and providing investors with solid investment returns as a result. The company has strong partnerships and relationships with some leading companies in the healthcare sector. The revenue mix for AMEH is also quite diverse but Medicare is still making up the majority of payer types at 64%. What I think is very reassuring about AMEH compared to other healthcare companies is the fact they have been able to grow revenues not only because of stronger demand during Covid-19 but also afterward.

{kind=link}

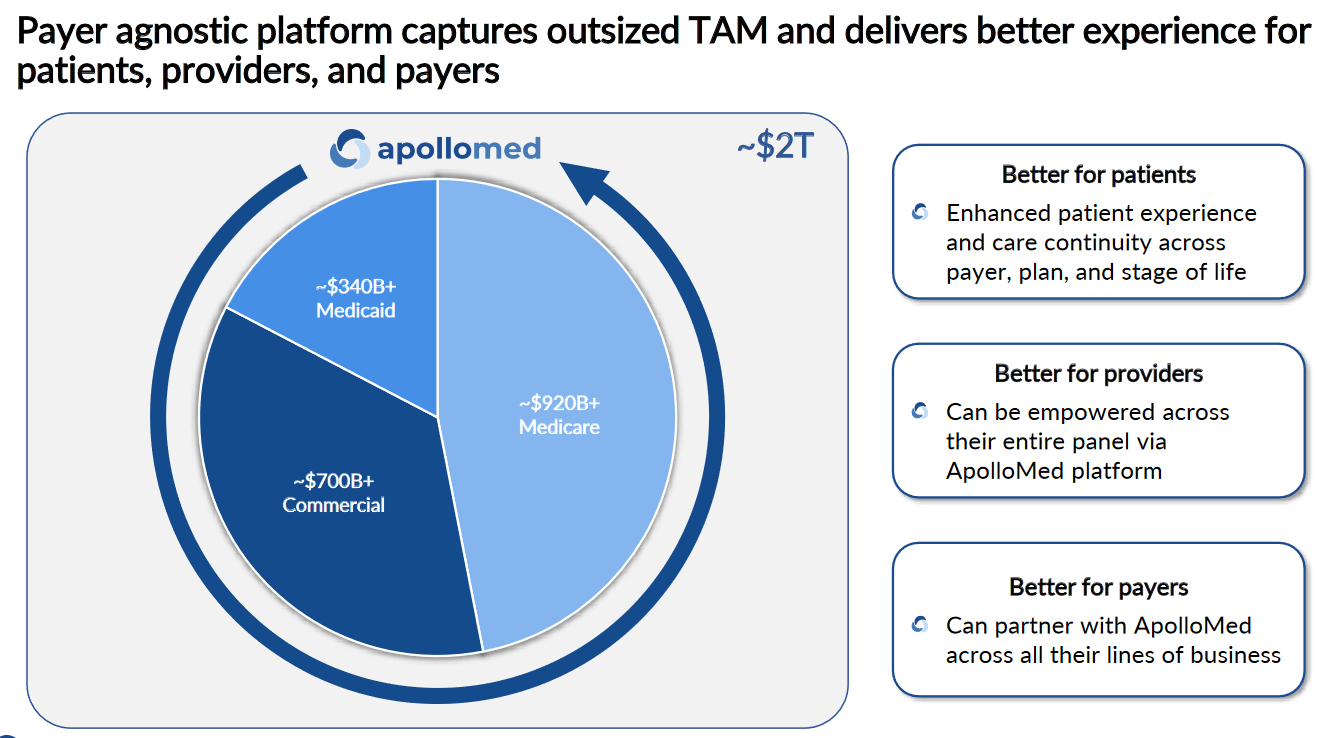

With a superior product offering AMEH can capture market share and deliver a better patient experience in the end. The combined TAM that AMEH is massive at a valuation of $2 trillion. With the acquisition that we just discussed it's lending AMEH to capture new market opportunities and broaden the stake of the TAM, they estimate there to be.

Margins

Margin Profile (Seeking Alpha)

The margin profile of AMEH right now leaves some things to be desired. The gross margins have seen some of their lowest levels in the last couple of years at 16.8%. This is 21% lower than its 5-year average and far below the sector's average of 55%.

But a shining light is the FCF margin of the company which is reducing the necessity to be diluting shares. Over the last few years, dilution has significantly haltered as the FCF has improved and I am confident about the future of AMEH because of that, at least in terms of an investor's gain from a stake in the company. As AMEH continues to leverage its assets the ROA remains strong at nearly 5%. I think this will eventually translate into AMEH being able to buy back shares, but that still seems to be years out.

Valuation

DCF Model (My Own Model)

Looking at the DCF model above it further highlights the fact that the share price of AMEH is too high to invest. The intrinsic value lands at $11 per share which is significantly under the share price of today. These estimates are also quite optimistic with a terminal FCF growth rate of 15%. This is under the 3-year average for AMEH but still enough to make a realistic assumption I think. The cash and debt position however are quite strong. AMEH is in a position where it could pay off all the long-term debts without using up all the cash funds.

Risks

Being a holdings company, AMEH generates a substantial portion of its revenues through strategic acquisitions and expanding its existing platform in collaboration with larger companies. This approach has been instrumental in fueling AMEH's growth trajectory and expanding its market presence. However, it also exposes the company to certain risks inherent in the business model.

{kind=link}

One key risk for AMEH lies in its acquisition strategy. While acquiring companies can provide access to new markets, technologies, and customer bases, it also involves integrating diverse businesses and managing potential cultural differences. The success of these acquisitions depends on effective post-merger integration and synergies realization, which may not always be smooth or immediate. Delays or difficulties in integrating acquired companies could impact AMEH's financial performance and operational efficiency.

Moreover, AMEH's current trading at a significant premium to its sector raises concerns about its valuation. An unjustified premium could make the stock vulnerable to corrections or price adjustments, especially if market sentiment shifts or investor expectations change. This could lead to potential downside risk for the share price, as investors may reassess their positions to align with a more realistic valuation.

Investor Takeaway

AMEH has not been a company that was a one-hit wonder because of the Covid-19 pandemic and the demand and capital that entered the healthcare market because of it. Instead, the revenues have been steadily climbing for the company.

But the valuation of the company is still quite high and the DCF model of the company highlights the fact that the share price needs to drop a fair bit before a buy case could be thought about. The performance so far from AMEH in terms of revenue growth has me optimistic enough to rate AMEH a hold for investors.

For further details see:

Apollo Medical Holdings: Rich Premium But Returning To Its Former Self