X - ArcelorMittal Should Rebound Post Destocking Cycle Peak

Summary

- ArcelorMittal S.A.’s financial results in Q3 were affected by spread compression and capacity curtailments.

- Optimization in production should support free cash flow generation in a subdued demand environment.

- ArcelorMittal S.A. is currently valued at a significant discount compared to U.S. peers, which opens substantial potential upwards.

ArcelorMittal S.A. ( MT ) is positioned to successfully overcome the peak of the destocking cycle due to the prudent adaption and allocation of production capacity to addressable demand, working capital, and effective cost management. I am bullish on MT, as I believe the company could capture more growth opportunities amid secular trends in the automotive sector and construction recovery once the headwinds weaken their grip and inventory restocking takes place.

ArcelorMittal is the world’s second-largest steel producer. Overall, the prospects for steel markets have deteriorated significantly as a result of the global economic slowdown, acceleration of inflation, high energy prices, and war-related disruptions. These led to a collapse in steel production and widespread production capacity idling and stoppages, especially in Europe. For reference, world crude steel production decreased by 3.7% YoY (1 691M mt) in the Jan-Nov 2022 period, with the most prominent decline in UE output, down by 10.1% YoY (127M mt) and CIS region, -19.6% YoY (79M mt; including Ukraine).

Steel sector’s activity and outlook

Apparently, prospects for steel companies remain gloomy in Europe due to high and volatile energy costs, the looming recession, and waning consumer confidence. However, the steel-using sectors are set to gain momentum in the second half of 2023.

Steel-using index (Eurofer)

Following the aggressive rebound in steel-using sectors since the removal of lockdown measures, total production activity is increasingly impacted by rising energy costs and supply chain issues starting from the second half of 2021.

Russia’s invasion of Ukraine initially affected output only to a limited extent until the second quarter of 2022. However, the landscape for the rest of 2022 deteriorated significantly over the summer as energy prices and production costs surged to unsustainable levels.

The rapid deterioration of the global economic indicators, combined with the war-related disruptions is expected to roll over the first half of this year, exhibiting a downside pressure to the steel sectors. The outlook is expected to improve only from the Q2 of 2023 onwards, driven mainly by the automotive and construction sectors.

The demand for steel in the automotive industry will be associated with the advance of high-strength steels ((AHSS)) implementation, as the use of advanced alloys ensures lightweighting, optimization of the vehicles’ design, improvement of safety and fuel efficiency. ArcelorMittal produces advanced high-strength steels to supply automotive companies. I believe MT will be able to maintain the above cyclical growth in automotive, as the AHSS segment is fast-growing, and the company has a leading position in it. Additionally, the alloy steel value added products are priced at a premium, which will underpin MT’s profit margins.

Infrastructure investments owing to government measures will provide support for steel demand by the construction industry going forward. Following the alleviation of the strict Covid measures in China, the government efforts to boost the real estate market could lead to a turnaround in the world’s largest steel consumer, and exhibit upward pressure on steel prices.

Financial results

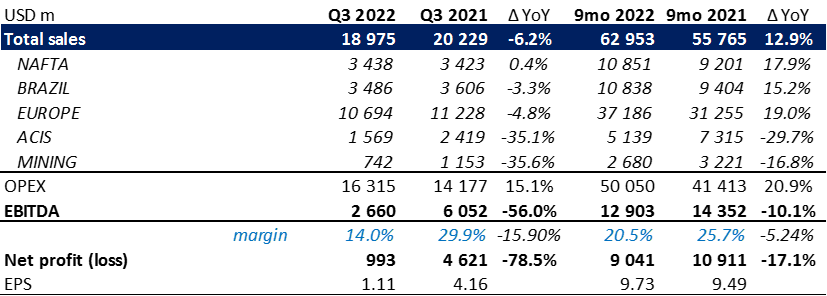

ArcelorMittal reported a 6.2% YoY decrease in total sales to $19 billion in Q3 2022. The decrease was due to the lower overall steel shipments by 7.1% YoY (13.6k mt) and lower iron ore reference price by 36.5% YoY. Segment-wise, all segments except NAFTA (+0.4% YoY) registered sales drop, reflecting weaker demand in Europe (-4.8% YoY) and suppressed ACIS segment (-35.1% YoY).

{kind=link}

The weak quarterly performance was amplified by higher operating costs (+15.1% YoY) and led to a 56% YoY slump in EBITDA to $2.7 billion. This corresponds to $1.11 per share, compared to $4.16 per share in Q3 2021.

9mo 2022 total sales were up 12.9% YoY to $63 billion following the strong growth in first two quarters. However, input costs pressure brought EBITDA 10.1% short YoY and resulted in a 17.1% YoY decrease in net earnings for the period.

Valuation

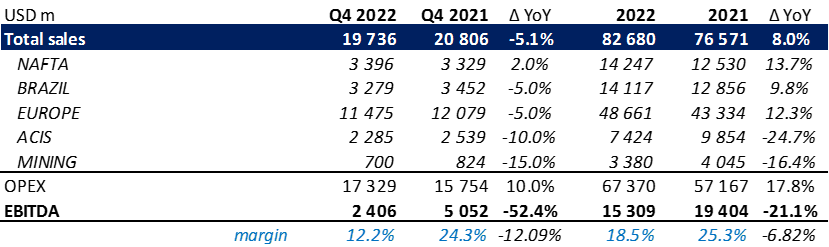

I addressed the valuation of ArcelorMittal by using peer selection. The following table presents my forecasts regarding MT’s total sales and EBITDA for the Q4 and 2022 full year.

{kind=link}

The company announced operating curtailments in the fourth quarter in order to optimize energy consumption and bring production in line with lower apparent demand. Thus, for Q4 2022, I assumed a 5.1% YoY decrease in total sales as a result of suppressed macro environmental in Europe, steel spread compression and rapid supply chain destocking. However, I expect NAFTA segment to remain on the positive side, as a result of resilient automotive production output in the region, driven by strong demand for new vehicles in the U.S.

With the above assumptions, I estimate the company’s 2022 full-year revenue to grow by 8% YoY and reach $82.7 billion with EBITDA of $15.3 billion, down 21.1% YoY on a margin of 18.5% (-6.8 pp), as a result of input cost pressure.

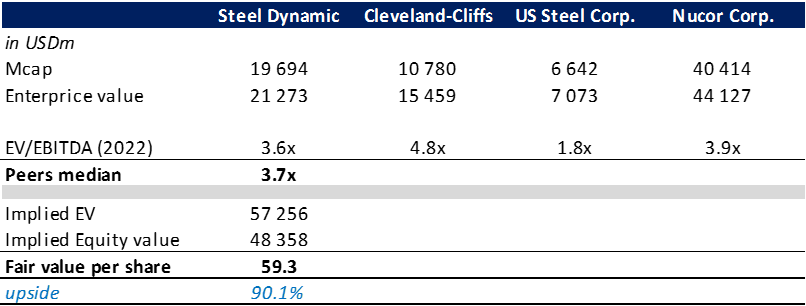

I selected Steel Dynamics ( STLD ), Cleveland-Cliffs ( CLF ), U.S. Steel Corporation ( X ) and Nucor ( NUE ) as a peer group in order to derive the sector EV/EBITDA forward trading multiple.

Comparable valuation (seekingalpha data; author’s estimates )

{kind=link}

ArcelorMittal is currently trading at EV/EBITDA forward multiple of 2.3x, which represents a significant discount of around 60% to the sector’s median of 3.7x, derived from the main comps. When applying my estimate of EBITDA to the peers median multiple, the calculations should yield an enterprise value of $57.3 billion. Subtracting interest-bearing and pension-related liabilities, we should arrive at an equity value of 48.4 billion, which corresponds to $59.3 per share and implies 90% upside potential. The upside would be supported by the strong management’s commitment of returning capital to shareholders. The ongoing 60 million share buyback program was 50% completed in Q3 and is set to last till May 2023. Additionally, the working capital unwind will reinforce FCF generation consistency and support future dividend distribution flows and higher Capex.

Risk factors

Operational disruptions, especially at a major production facility, represent a significant challenge for such capital-intensive companies as MT, and could restrain the company’s financial results. Despite the announced adapting of production capacity down by circa 6M mt in order to reduce fixed costs, the aggravation of energy prices and inflationary pressure may lead to further production curtailments. Additionally, stagnation in the automotive and construction industries due to recession fears could worsen the supply-demand balance for steel producers.

Conclusion

The ongoing disruptions linked to the geopolitical tension, severe rises in energy prices, and input costs weigh poorly on the demand outlook and erodes ArcelorMittal S.A.’s profitability as a result of spread compression and production curtailments. The headwinds are expected to weigh on the steel-using sectors at least until mid-2023. However, once the current destocking cycle completes, the inventory buildup will make a positive contribution to steel demand rollout in end-markets and support overall economic recovery.

ArcelorMittal is navigating well in a difficult market environment due to a resilient business model, balance sheet and flexibility in responding prudently to the subdued demand. I believe ArcelorMittal is an attractive investment opportunity, as current low valuation to its U.S. competitors opens up a significant upside gap.

For further details see:

ArcelorMittal Should Rebound Post Destocking Cycle Peak