TRIN - Ares Capital: Assessing The Recent Results For 10% Yield

2023-08-29 07:58:57 ET

Summary

- One of the largest mistakes that investors make is focusing on historical dividend coverage instead of projected dividend coverage.

- This article discusses ARCC's dividend coverage comparing the recently reported results to my base, best, and worst projections which were provided in the previous article.

- If you're not getting this level of detail for each of your BDC investments, please consider taking a more detailed approach to due diligence each quarter.

- Also discussed are ARCC's recently issued investment grade ("IG") bonds which currently have yield-to-maturities near 7% as shown below.

This article discusses Ares Capital ( ARCC ) , mostly focused on dividend coverage, comparing the recently reported results to my base, best, and worst projections which were provided in the following article from last month:

Also, please see the previous article which discussed ARCC's portfolio credit quality:

As discussed in " Introduction To BDC Google Sheets ", many BDCs have investment grade ("IG") bonds/notes for lower-risk investors building a balanced 60/40 portfolio (composed of 60% to 70% stocks/equities and 30% to 40% bonds or other fixed-income offerings). Last month, ARCC issued $600 million of unsecured notes (upsized from $500 million) with a yield-to-maturity of 7.249% which was a 265 basis points spread to the benchmark treasury rate. Please note that this is a higher spread than many of the previous notes which were most recently around 125 to 180 basis points but lower than the 330 to 370 basis points from the notes issued in mid-2020. ARCC had $11.4 billion of borrowings of which $3.6 billion is credit facilities at SOFR+1.75% to 2.80% and the proceeds from the new notes will be used to pay down the higher rate facilities which are around 8% given the recent increase in interest rates. Clearly, management knows higher for longer is very likely and these notes will NOT have a material impact on borrowing rates .

ARCC now has 9 tradeable bonds with investment-grade ratings by S&P, Moody's, and Fitch most of which currently have yield-to-maturities near 7% as shown below from the BDC Google Sheets:

{kind=link}

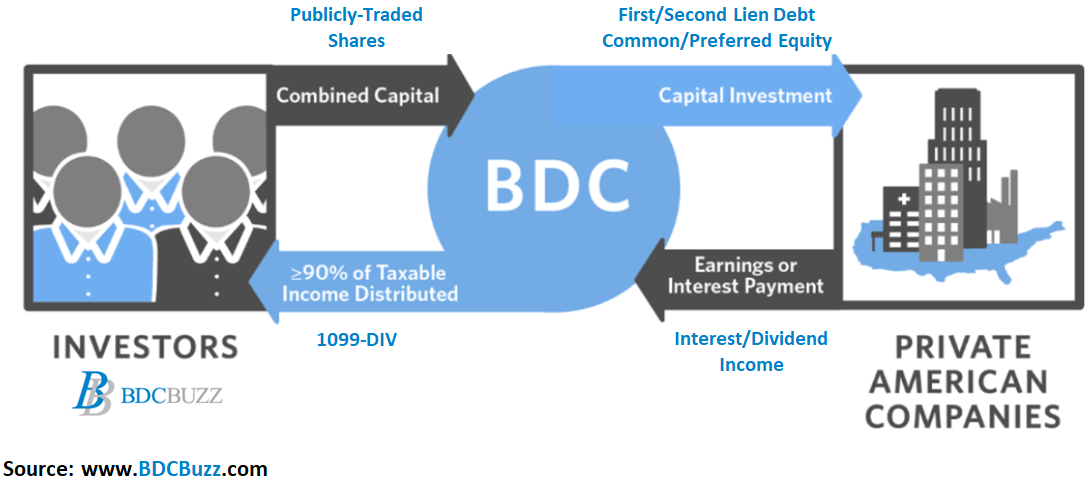

Business development companies ("BDCs") invest shareholder capital in privately-owned, small- and medium-sized U.S. companies generating income from secured loans and capital gains from equity positions, much like venture capital or private equity funds.

{kind=link}

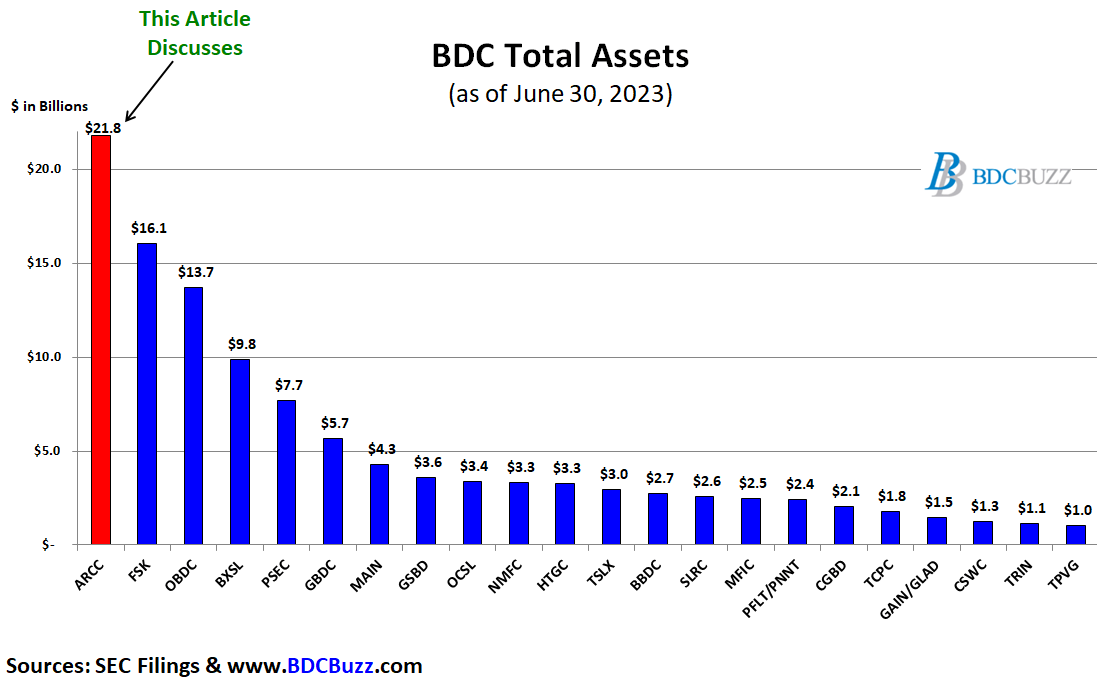

The BDCs in the chart below account for around 90% of the total assets and market capitalization for the sector. Over the two months, we discussed the portfolio credit quality and/or dividend coverage for most of them including FS KKR Capital ( FSK ), Blue Owl Capital ( OBDC ), Prospect Capital ( PSEC ), Golub Capital ( GBDC ), Goldman Sachs BDC ( GSBD ), Oaktree Specialty Lending ( OCSL ), New Mountain Finance ( NMFC ), Hercules Capital ( HTGC ), Sixth Street Specialty Lending ( TSLX ), PennantPark Floating Rate Capital ( PFLT ), PennantPark Investment ( PNNT ), BlackRock TCP Capital ( TCPC ), Gladstone Investment ( GAIN ), Gladstone Capital ( GLAD ), Monroe Capital ( MRCC ), Trinity Capital ( TRIN ), and TriplePoint Venture Growth ( TPVG ) in the following articles:

- Lower Fees Driving Higher Dividends: GBDC

- Solid 10% Yield From OBDC or TSLX?

- TRIN: Initiating Coverage Of This 14% Yielding BDC

- Solid 10% Yield From GAIN & GLAD

- OCSL or NMFC For Solid 11% Yield?

- Better High-Yield Buy: FSK or PSEC?

- PNNT: Big Win From Dominion/Fox Settlement

- Venture Debt Opportunity Yielding 13% To 14%: HTGC or TPVG?

- TCPC or PFLT For Solid 12% Yield?

- Safer 12% Yield: GSBD or MRCC

{kind=link}

The following chart shows the average dividend coverage over the last 10 years with the last 4 quarters averaging over 120% even after taking into account the previous dividend increases. For Q2 2023, the average coverage was 132% but with a wide range of results from the lowest being SLRC at 101% (not covered by BDC Buzz) to PNNT at 185% partially due to the dividend income from Dominion, as predicted in the article linked above.

Many BDCs have opted to take a conservative approach when setting their regular dividends (just in case rates head lower) and using supplemental/special dividends to pay out excess earnings. This means that if portfolio yields decline, we will see lower amounts of supplemental/special dividends but the regular dividends will be maintained especially 'Level 1' dividend coverage BDCs.

{kind=link}

Even if the underlying interest rates eventually go lower, there is a good chance that most BDCs will continue to over-earn their regular dividends. For example, the Fed funds target range declined by 2.25% (225 basis points) starting in Q3 2019 through Q1 2020 resulting in a decline in average dividend coverage from 109% to 102%.

Also, many BDCs decreased their leverage (debt-to-equity) with plenty of dry powder to invest in new loans at higher rates with floors, which might continue even if interest rates head lower given the current market conditions including a "lender-friendly environment" with "higher overall yields", better terms, and stronger covenants (safer investments) which will be taken into account with the updated best-case projections.

ARCC

Quick Update

One of the largest mistakes that BDC investors make is focusing on historical dividend coverage instead of projected dividend coverage which is heavily reliant on portfolio credit quality. Each quarter I update the financial projections for each BDC with base, best, and worst-case scenarios to test the sustainability and/or changes to the current dividends. In the previous article, I discussed many of the drivers used for projecting dividend coverage including my base, best, and worst-case projections for ARCC. If you're not getting this level of detail for each of your BDC investments, please consider taking a more detailed approach to due diligence each quarter.

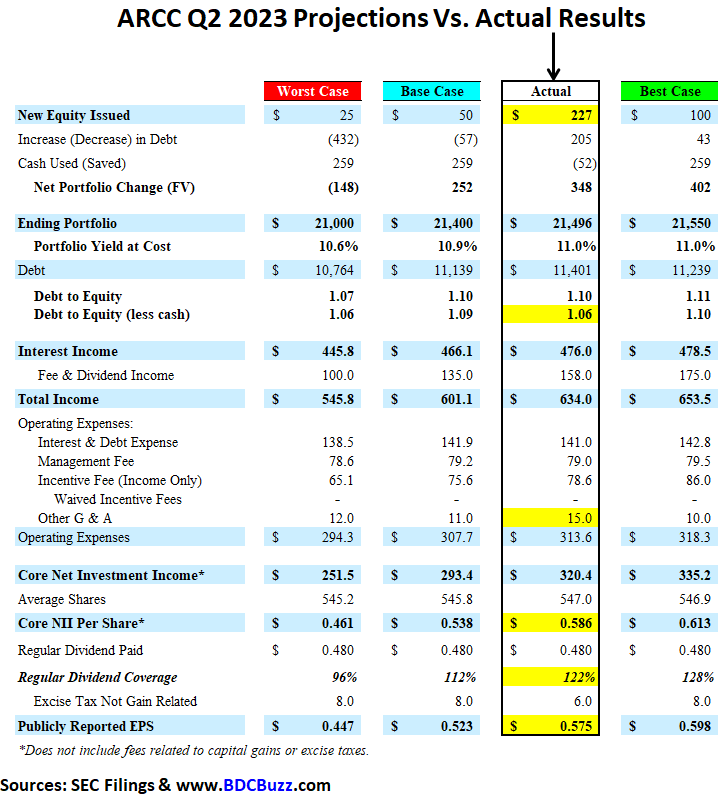

For Q2 2023, ARCC reported between its base and best-case projections, mostly due to much higher-than-expected dividend income and slightly higher portfolio growth, partially offset by higher 'other G & A', covering its regular dividend by 122% (excluding excise tax). The company reaffirmed its regular dividend of $0.48 per share, which was predicted in the previous base case projections. The amount of payment-in-kind ("PIK") interest income declined from 6.6% to 6.3% of total income or 8.4% of interest income.

The following table shows the actual results compared to my previous projections provided in the article linked above. The portfolio growth and yields came in mostly as expected. One of the largest differences was the issuance of 12.1 million shares (accretive to NAV) through its "at the market" ATM equity program raising a total of $227 million in net proceeds. This had a meaningful impact on leverage and slightly lower-than-expected interest expense (as shown below).

{kind=link}

There was another decline in leverage with its debt-to-equity ratio declining from 1.08 to 1.06 (net of cash) due to the issuance of 12.1 million shares.

Kipp deVeer , CEO : We reported another strong quarter with year-over-year growth in our GAAP and Core earnings per share driven by rising portfolio yields, increased investment activity and continued stable credit quality. We believe that our scale, relationships and deep sourcing capabilities leave us well-positioned to capitalize on the growing demand for flexible capital from the middle market.

Our strong balance sheet and liquidity enable us to take advantage of the compelling investment opportunities currently available and to further build upon our strong track record of performance. To illustrate the consistency of our performance, this quarter marks our 56th consecutive quarter where we have declared a steady or increased regular quarterly dividend for our shareholders.

It is important to point out that its regular dividend of $0.48 per share is adequately covered, especially given that the company has earned an average of over $0.54 per share over the last two years. As mentioned in the weekly BDC sector updates, I am expecting fewer (and smaller) increases in the regular dividends but larger supplemental dividends over the coming quarters, as BDCs prepare for potentially lower rates. ARCC management discussed this on the previous call and is "cautious about raising the dividend" and "chose not to raise the dividend this quarter because we'd like a stronger view on where we see rates normalizing in the future". This is another example of higher-quality management and was also discussed on the recent call :

I think the discussion that we had when we raised the dividend, obviously, was, the earnings are well in excess of given the raised dividend level, what's prudent, right? And the discussion that was much more about the direction of interest rates than it was about portfolio credit quality, right? So if we pull a couple of the different levers that could allow us to have a higher dividend or a lower dividend, the one that's the most impactful would be a significant decrease in base rates. You'd have to model non-accruals up a lot to have it to have any real impact on how we thought about the dividend today.

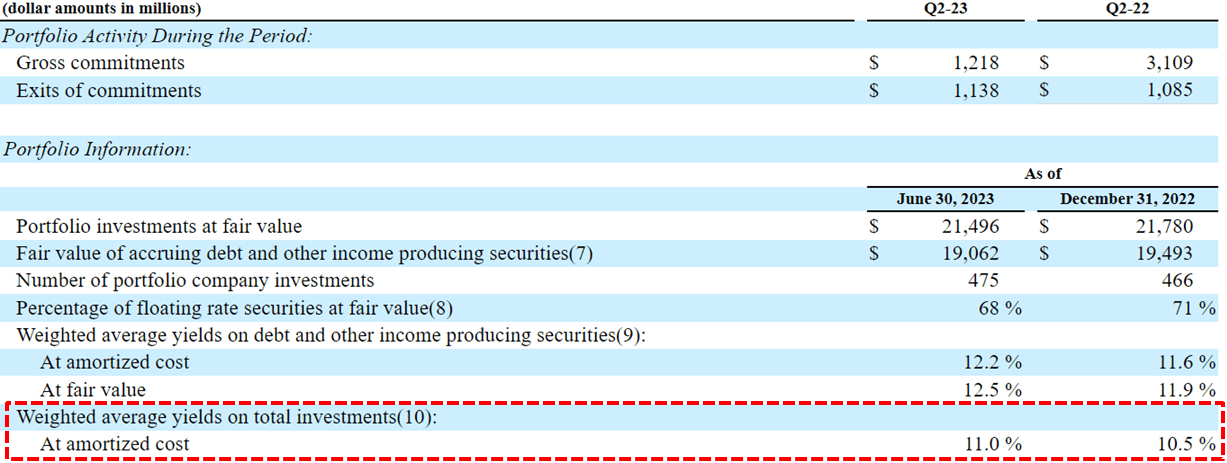

During Q2 2023, ARCC sold another $39 million of loans to IHAM that should continue to drive higher dividend income over the coming quarters and the overall portfolio yield has increased from 10.5% to 11.0% over the last two quarters:

{kind=link}

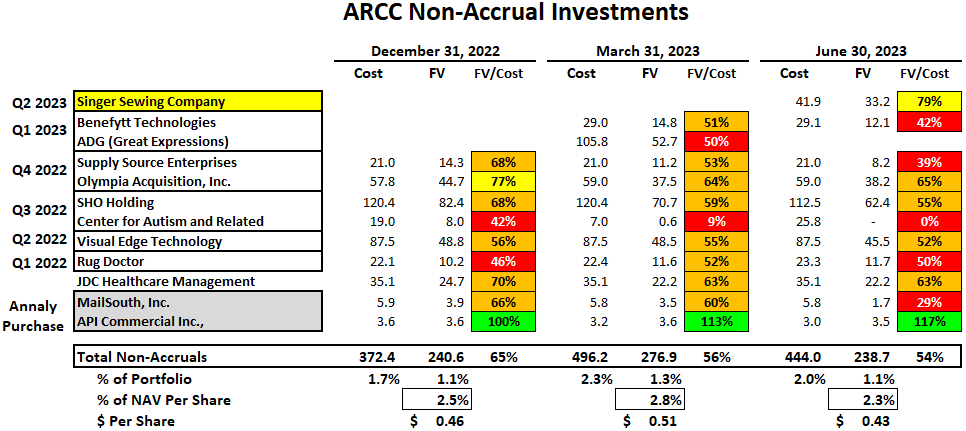

Non-accrual investments decreased slightly from 1.3% to 1.1% of the total portfolio fair value due to restructuring ADG (Great Expressions) partially offset by adding its watch list investment in Singer Sewing Company . Also, there were additional loans to Center for Autism and Related Disorders ("CARD") added to non-accrual status which was predicted in the previous report. Please note that ARCC has a very large portfolio with 475 portfolio companies valued at over $21 billion, so there will always be a certain amount of non-accruals.

{kind=link}

As mentioned in previous articles, CARD is an autism treatment and services provider specializing in applied behavior analysis therapy which was added to non-accrual during Q3 2022. In June 2023, the company filed for Chapter 11 bankruptcy due to a $82 million net loss in the 12 months ending April 2023, largely as a result of the long-term impacts of the COVID-19 pandemic. The center entered bankruptcy with just $2 million in cash on hand, and it intends to fund its bankruptcy with an $18 million loan from its primary lender, ARCC.

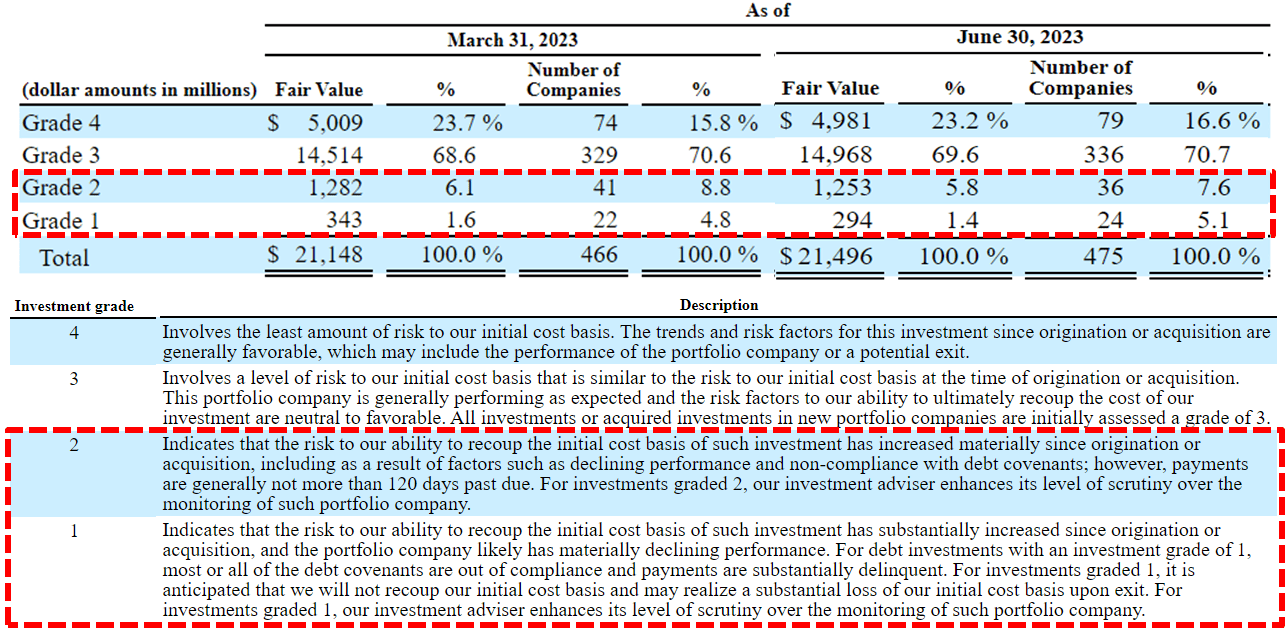

There was a decrease in the amount of higher-risk Grade 1 and Grade 2 credit-rated investments, from 7.7% to 7.2% of the portfolio fair value, and likely includes many of the previously discussed watch list investments. The weighted average grade of the portfolio at fair value remains 3.1 and will be discussed in an upcoming article.

{kind=link}

During Q2 2023, there were net realized losses of $68 million or $0.12 per share mostly related to restructuring its non-accrual investment in ADG (Great Expressions) :

{kind=link}

Summary and Returns

- ARCC reported another solid quarter between its base and best-case projections due to higher-than-expected dividend income, slightly higher portfolio growth, partially offset by higher 'other G&A'.

- ARCC covered its dividend by 122% (excluding excise tax), NAV per share increased by 0.7%, debt-to-equity declined to 1.06, PIK declined to 6.3% of income, and non-accruals declined to 1.1%.

- ADG (Great Expressions) was restructured and removed from non-accruals partially offset by adding Singer (discussed in previous reports) and additional loans to Center for Autism and Related Disorder (as expected).

- There were net realized losses of $68 million or $0.12 per share mostly related to restructuring its non-accrual investment in ADG and a decrease in the amount of higher-risk (Grade 1 and Grade 2), from 7.7% to 7.2% of the portfolio fair value (the previously discussed watch list investments).

- As expected in the base case, ARCC maintained its regular dividend of $0.48 per share which is well covered given that the company has earned an average of over $0.54 per share over the last 8 quarters.

- ARCC recently issued another $600 million of unsecured notes that will not have a meaningful impact on earnings.

The "annualized" return shown below shows the actual compounding of annual returns :

{kind=link}

For further details see:

Ares Capital: Assessing The Recent Results For 10% Yield