ARCC - Ares Capital: Consider This ~10% Yield Whether Rates Remain High Or Come Down In 2024

2023-12-20 16:45:05 ET

Summary

- Ares is a high-yielding stock that has an impressive track record of delivering value to investors.

- Ares benefits from the high interest rate environment, but could suffer if rates are lowered - although lower rates could see capital moving back into dividend stocks, driving multiple expansions.

- In this analysis, I look into the sustainability of the dividend going forward.

Rising interest rates: Why dividend investors have been hurt - and why rates are now in the sweet spot for Ares

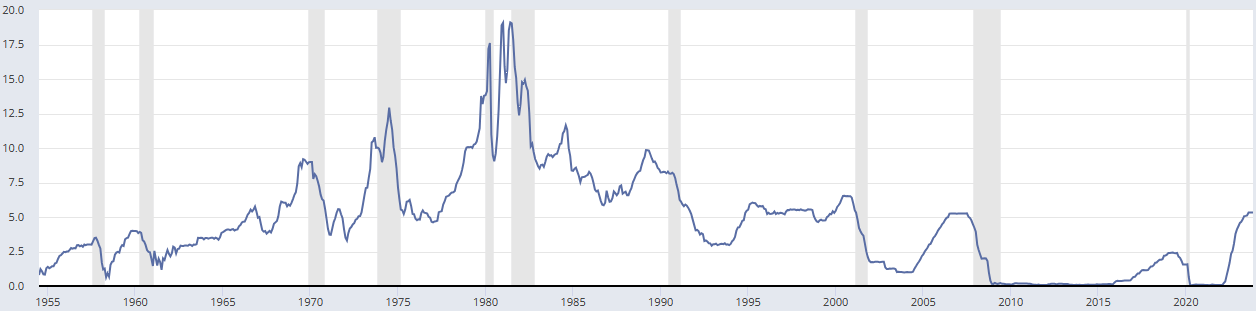

In the past couple of years, we've seen sharp rises in interest rates in response to widespread inflation. The US Federal Reserve raised rates several times in 2022 and 2023. While rates are still fairly low historically speaking (see the chart below), the hikes were substantial enough to suddenly make the otherwise "forgotten art" of fixed-rate investing mainstream again.

Federal Reserve Bank of St. Louis

{kind=link}

Several dividend stocks have been hurt by the rise in interest rates, and that's important to remember when considering a high-yielder like Ares Capital ( ARCC ) for investment.

The poor performance of many dividend stocks in the rising interest rate environment has a pretty simple explanation: Before rates started going up, they were at record lows. Just look at the chart above. During the COVID pandemic, rates were virtually zero. Between the years of the financial crisis and 2015, rates were virtually zero as well. In those years, investors shunned the fixed-income instruments. Instead, investors seeking income would buy dividend stocks as a proxy for high-yielding fixed-income investments. As interest rates have come up, we've seen this trend reverse: Investors are turning to bonds, including high-yield bonds, seeking the safety of principal that bonds may provide now that you can easily find coupons on bonds matching many high-yield stocks. The rate on a 10-year US treasury bond is ~4%. When you can make a respectable "dividend" at that level taking virtually no risk at all, why risk buying an equity with a comparable dividend knowing that you can lose the principal, and the dividend may get cut? At least that seems to be the thinking of many investors.

Well, on a macro level, you might want to get ready for yet another change. Federal Reserve officials now expect rate cuts in 2024. If rates come down again, we might see the trends described above change direction again. We may see a comeback for dividend stocks. That in and of itself is good for buyers of Ares, because if we see lots of capital moving out of fixed-income back into equities and especially those carrying a dividend, we could see multiple expansions in such issues. With Ares trading at an earnings multiple of just ~8, there's a lot of multiple expansion potential right there. That's one macro driver that I see working for Ares going forward.

Now you can't rely on macro factors alone, of course. Since Ares is a business development company ((BDC)) that operates as a direct lender to middle-market companies - that means it finances other companies, typically companies that are developing or in distress - its core business benefits from a rising interest rate environment. At least to a certain extent. In a higher interest rate environment and as lending terms become more restrictive, specialty credit such as that offered by Ares becomes more attractive. So on a micro level, Ares benefits at least to some extent from rising interest rates. I say "to some extent" because Ares makes money in part by using borrowed money to provide financing to other companies at higher rates, thereby making a profit on the interest margin. If rates are too high, the financing that Ares offers could become simply too expensive, thereby limiting Ares' ability to efficiently deploy capital, or it would lead to Ares having to work with a lower interest margin, thereby limiting Ares' profit margins.

In other words, interest rates coming down would, in my opinion, hurt the core business of Ares in that it would make its specialty credit business less attractive, but again it could actually benefit what earnings multiple the market is ready to pay for a high yield - because the alternatives in fixed-income would be so much poorer in a lower rate environment. An investor's alternatives are always important to consider in a valuation.

A lot suggests that right now, with rates around 4%, we're in a bit of a sweet spot for Ares. Rates are high enough that Ares' capital services are attractive, but low enough that the system still works. And even with fluctuating interest rates, Ares reports having seen a growing demand for direct lending over time:

Ares Capital investor presentation

And since its IPO in 2004, Ares has generated impressive performance:

Ares Capital investor presentation

The question of course is whether (or for how long) Ares can keep up its current business model and impressive performance. This directly ties into the discussion of the sustainability of its dividend, which I'll look into later in this analysis.

First, let's have a quick look at where the quant system says we are in terms of timing an entry into Ares.

Quant rating: A little mixed in terms of timing, but great dividend scores

On Seeking Alpha, Ares was recently downgraded by the quant system to "Hold", but still has a "Buy" rating among Seeking Alpha analysts and Wall Street analysts:

Seeking Alpha

In fact, Wall Street likes Ares so much that it's nearing a "Strong Buy" rating, with most analysts following the company currently having issued that rating:

Seeking Alpha

The Dividend Grades on Seeking Alpha are rated as follows:

Seeking Alpha

As seen, the dividend grades are quite good - perhaps except for the safety score - and have been improving over the last 6 months. Investing with an eye to the quantitative scores could help you make investment decisions that are less prone to biases and human misjudgment. Or it could help you confirm whether your qualitative reasoning has support in the data.

As for the safety score, I will look into the safety of Ares' dividend just below.

Why I think the dividend is safe

First of all, let's acknowledge the track record: Ares has 14+ years of stable or increasing quarterly dividends. While that's not nearly enough to challenge the Dividend Aristocrats, and while the dividend has not been raised all years, it's been at least kept stable.

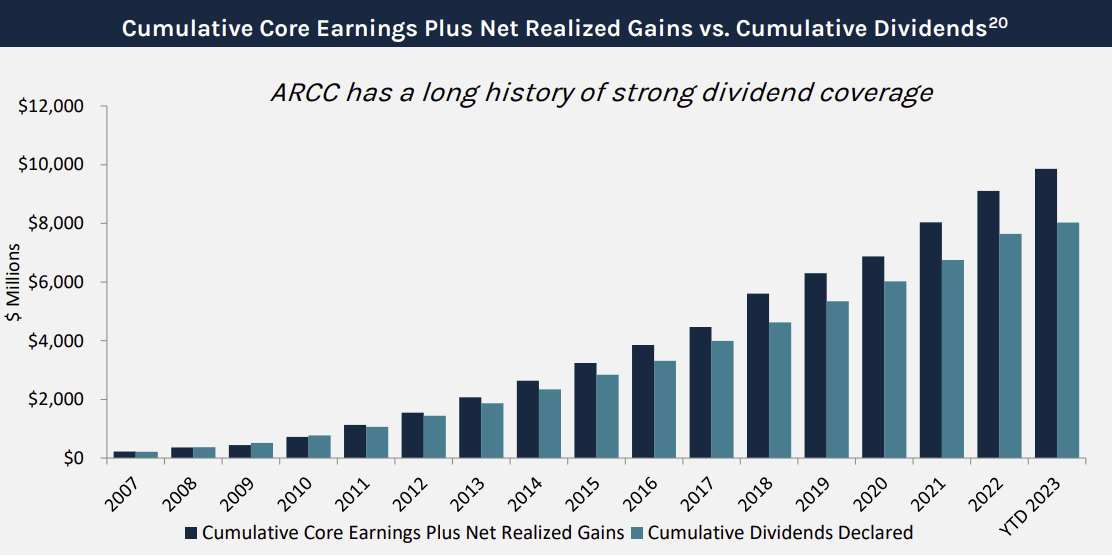

If we turn to the fundamentals that allow for the growing or maintaining of the dividend at Ares (core earnings and realized gains), we see that the dividend is well covered:

Ares Capital investor presentation

{kind=link}

The dividend coverage is positive and has been for more than a decade - supporting the dividend and the growth. This gives Ares a cushion to maintain its dividend even if things turn somewhat against the company on a macro level.

Further, the diversification in Ares' underlying assets should be noted. Ares has most of its investments within non-cyclical industries. These include healthcare, consumer durables, enterprise services, and software. Overall, Ares is very diversified among different industries:

Ares Capital investor presentation

With diversification in place, a healthy track record of improving or maintaining the dividend, good dividend coverage, and interest rates currently at attractive levels, I think the healthy dividend is safe for now.

Risks

If interest rates come down very quickly and substantially, it'll hurt specialty credit as it becomes less attractive compared to alternatives. By extension, Ares would not do as well as it has been recently in the higher rate environment. With some signals pointing to lower rates in 2024 and other signals to the contrary, I believe there's a fair chance - although there's no way of accurately predicting it - that rates will remain in a "sweet spot" that is still attractive to Ares for at least a while to come. In other words, while substantial drops in rates would hurt Ares' business, some lowering of rates is manageable for Ares. But the question of where interest rates are going will remain the biggest concern for potential investors in Ares.

Other risks apply too, of course. One such risk is that of the general credit risk assumed from financing Ares' portfolio companies. With several of Ares' customers being either developing or distressed entities, there's a higher risk of default in each individual company than would be had the customers been mature companies. I believe the main thing protecting Ares in this regard is its wide diversification.

Key takeaways

Ares is the world's largest "BDC" and a blue-chip in its field. It offers investors a healthy dividend which is supported by good dividend coverage and a well-diversified portfolio of financial engagements.

The current interest rate environment holds both opportunities and challenges for Ares: Rates are high enough to make its specialty credit offerings attractive, but low enough that financing conditions are not too restrictive to dry opportunities out. Currently, I think Ares will remain in a "sweet spot" for a while to come. That should even out the risks of the investment for now.

For the reasons stated above, I rate Ares a Buy.

For further details see:

Ares Capital: Consider This ~10% Yield Whether Rates Remain High Or Come Down In 2024