ARCC - Ares Capital: Consistent Dividend Income To Help Fund Your Retirement

2023-12-20 15:34:54 ET

Summary

- ARCC currently offers a dividend yield of 9.7% and has a healthy payout ratio of 83%.

- The fund typically invests between $20 million and $200 million in companies with an EBITDA ranging from $10 million to $250 million.

- Lower rates could enhance net interest margins, reduce borrowing costs, and stimulate economic activity among portfolio companies.

Overview

I believe that some high yielding assets have a place in any investors portfolio, old or young. There are few gems out there that match ARCC in terms of income, total return, and consistency. ARCC has slowly crept its way to a top 3 position in my portfolio and the high levels of income I've received from its distributions over the last 4 years, makes it easy for me to stick by it. ARCC has the setup to thrive in a range of economic conditions and has a proven track record of providing consistently reliable income.

Ares Capital Corporation ( ARCC ) specializes in various financial transactions within the middle market, including acquisition, recapitalization, restructurings, and leveraged buyouts. The company focuses on investing in businesses operating in sectors such as basic and growth manufacturing, consumer products, healthcare, and technology.

The fund typically invests between $20 million and $200 million, with a maximum of $400 million, in companies with an EBITDA ranging from $10 million to $250 million. So the target audience are middle market companies. As part of its strategy, the fund actively seeks to lead and/or act as an agent in the transactions it engages in. Board representation in portfolio companies is also a priority. Additionally, ARCC selectively considers third-party-led senior and subordinated debt financings, and it opportunistically explores the purchase of stressed and discounted debt positions. Let us dig into their portfolio and see if it deserves a spot in your portfolio.

Portfolio

{kind=link}

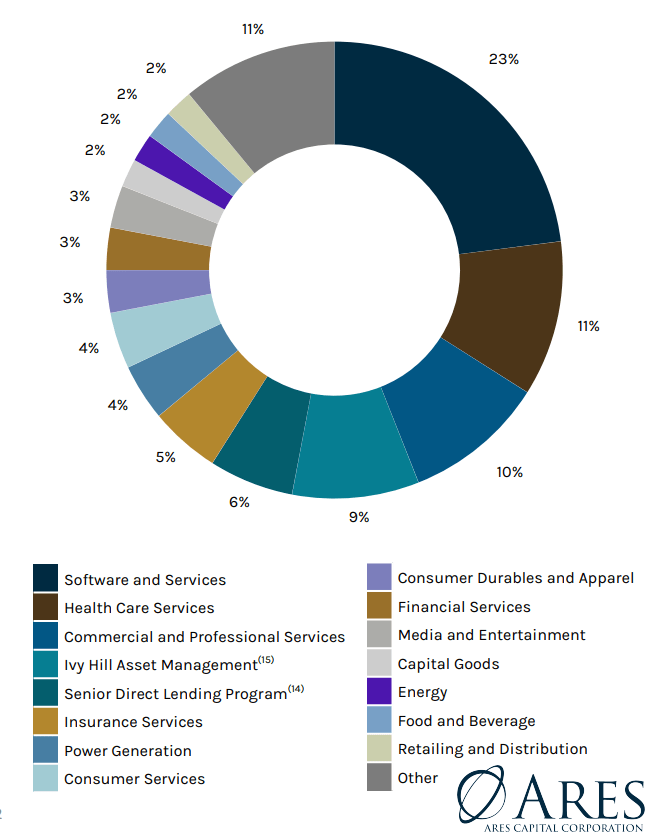

We can see that a majority of ARCC's portfolio is tech leaning with software and services making up 23%. This is closely followed by healthcare services coming in at 11% and commercial and professional services at 10%. Interestingly, ARCC's top 15 investments account for 30% of their total portfolio. I think this is pretty concentrated considering the total portfolio consists of 475 companies in all.

Over the last earnings call it was revealed that ARCC is expanding their portfolio with new commitments. They have accumulated approximately $410 million in commitments. Notably, 97% of these commitments were allocated to first lien senior secured loans, while 2% were designated for preferred equity and 1% for other equity. The majority, accounting for 97%, were floating rate investments, 2% were fixed rate.

Simultaneously, ARCC executed exits totaling around $158 million in investment commitments. The weighted average yield of debt and other income-producing securities exited or repaid at amortized cost was notable at 11.6%, aligning with the weighted average yield on total investments exited or repaid at amortized cost. There was a realized total net gains of approximately $1 million during this exit phase.

{kind=link}

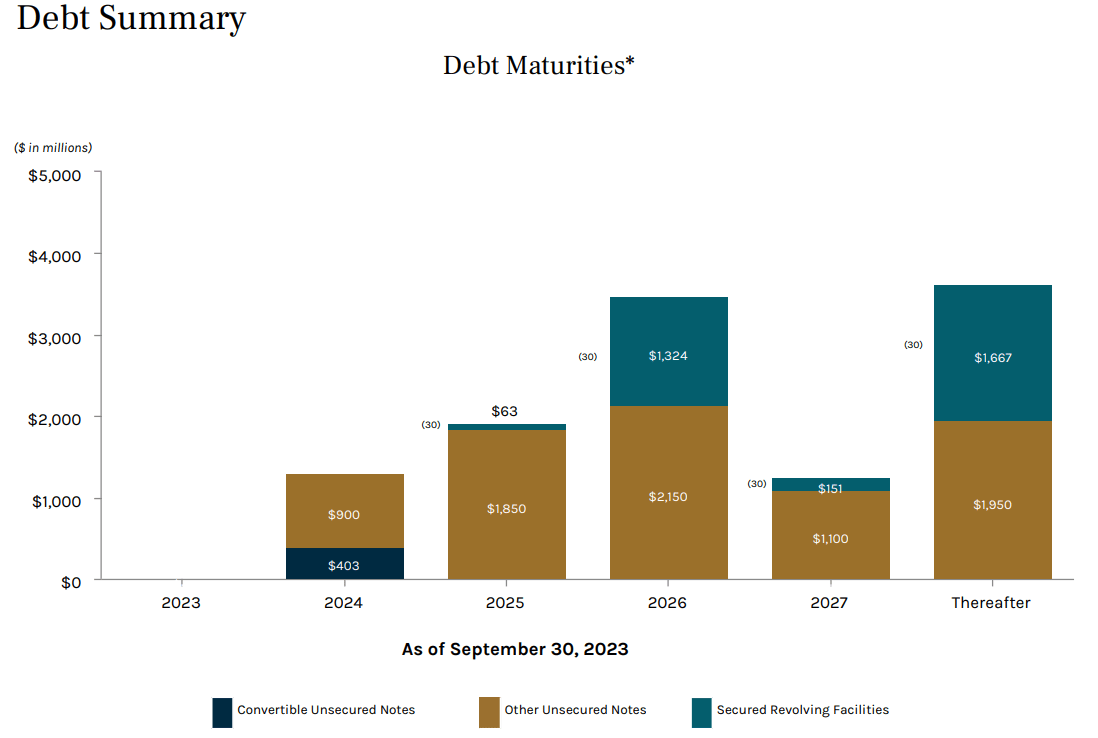

In general, their liquidity position demonstrates strength, boasting approximately $5.3 billion in total available liquidity. Closing the third quarter with a debt-to-equity ratio net of available cash at 1.03 times, a slight improvement from 1.07 times in the previous quarter, underscores their financial resilience. Lastly, this robust liquidity stance ensures there is no refinancing risk concerning next year's term debt maturities.

Risk Profile

I think that ARCC is top tier because a majority of ARCC's portfolio is exposed to first lien and second lien secured loans. First lien loans take priority in the repayment hierarchy, holding the primary claim on a company's assets in the event of default. This priority status enhances the likelihood of repayment and reduces default risk. Second lien loans still maintain a higher claim on assets compared to unsecured debt, providing an intermediate level of security.

ARCC Q3 Earnings Presentation

This is already an attractive setup because the steady income and cash flow generated by these loans contribute to a more predictable revenue stream for BDCs like ARCC. The strategy also involves seeking a balance between risk and reward. While first lien loans provide a more stable but lower return, second lien loans generally offer a slightly higher return.

Recent Earnings

ARCC announced its third-quarter earnings and it's clear they are benefiting from higher interest rates during the quarter. The Q3 EPS (earnings per share) came in at $0.59, slightly exceeding the average analyst estimate of $0.58. This marked an increase from $0.58 in Q2 and $0.50 in the same period last year.

In Q3 they raised $800 million of new capital which further strengthens ARCC's liquidity profile. The balance sheet remains a source of strength with ample low leverage at 1.03x net debt to equity. Net investment income for the quarter was $289 million, showing a decrease from $314 million in the prior quarter but an increase from $288 million in the same quarter the previous year.

Examining portfolio and investment activity, Ares made gross commitments of $1.60 billion, up from $1.22 billion in Q2 but down from $2.24 billion a year ago. Exits of commitments stood at $1.28 billion compared with $1.14 billion in Q2 and $1.98 billion in Q3 of the previous year.

Dividend & Superior Performance

As of the latest declared dividend of $0.48/share, the dividend yield comes in at 9.72% after the price rise shortly after announcement. ARCC's payout ratio sits at a comfortable 83%. This suggests that the company's dividend is well-supported by its earnings and allows room for expansion. Since the start of the pandemic, the NII payout ratio has consistently remained below 100%. Therefore, I see no threat to the dividend going forward.

The dividend story here has been impressive for such a high yielding asset. A $10,000 investment in 2010 would have provided roughly $1,200 in dividend income. As per Portfolio Visualizer, with dividends reinvested and no additional capital deployed, your dividend income would have grown to over $4,000 and your position value would be worth approximately $60,000. The five year dividend CAGR comes in at 4.51% while your yield on cost would have grown to 12.5% if you were holding over the same five year period.

ARCC's performance has been superior when compared against other top tier BDCs and even the S&P 500 ( SPY ). When including distributions, the total return has been superb amongst the competition. Some other well-performing BDCs that competes with ARCC are the following:

Since the start of the pandemic crash, ARCC has provided a superior return to the competition while maintaining their high distribution. Even against the S&P, ARCC outperforms in total return as well.

Valuation & Catalyst

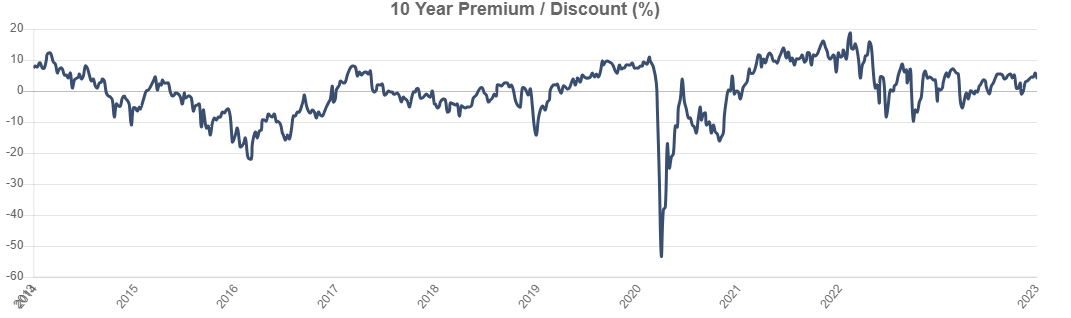

ARCC trades at a slight premium to NAV of only 4%. This is pretty much on par with the 3 year average premium of 5.72% We saw the premium rise as high as 19% in 2022 and the largest discount we received over the last 3 year period was only -10%. So in my opinion, even though ARCC trades near fair value range, I think the income it provides here is more important.

{kind=link}

Ideally, we all wish we bought in heavily during the crash in 2020. However, I do think the current price level still makes for an attractive entry point for ARCC because of a catalyst we have going into the new year. ARCC is poised to benefit from anticipated interest rate cuts. Lower interest rates can lead to reduced borrowing costs for ARCC, enhancing their net interest margin and bolstering profitability.

ARCC Q3 Earnings Presentation

The company's emphasis on floating-rate investments, positions it favorably to adapt in a declining interest rate environment. Similarly to how ARCC was able to maintain high profitability during a higher interest rate period where yields on their instruments stayed stable or increased, they will be just fine in a lower rate environment for a few reasons. Lower interest rates can further enhance ARCC's cost of capital, making it more cost-effective for the company to raise funds through debt issuance and other financing channels. This improved cost of capital, coupled with lower interest rates, may present favorable opportunities for ARCC to refinance existing debt, potentially reducing overall interest expenses and improving cash flow. For reference, when interest rates were close to zero after the GFC, ARCC still provided great value.

The middle-market companies in ARCC's portfolio may benefit from a stimulated economic environment as well. This positive economic climate can contribute to improved performance among portfolio companies, potentially leading to increased cash flows and reduced default risk. While ARCC does not typically hold a lot of weight in equity stakes, the company may indirectly benefit from an overall healthier economic landscape, which could positively influence the credit quality of its debt investments.

Moreover, lower interest rates may encourage middle-market businesses to pursue expansion initiatives. ARCC, as a provider of financing for growth projects, acquisitions, and strategic endeavors, could find opportunities to support the expansion plans of its portfolio companies. In navigating these potential benefits, ARCC will need to adapt to changing market dynamics and undertake a comprehensive assessment of the broader economic landscape to make informed decisions in response to future interest rate movements.

Takeaway

Ares Capital Corporation maintains a resilient position in the middle-market sector. The Q3 2023 earnings report showcases ARCC's adaptability and strategy on maintaining superior returns for shareholders. With a concentrated yet diversified portfolio, recent commitments of $410 million underscore the company's proactive expansion. Notably, a focus on first lien senior secured loans mitigates risk.

ARCC's strong liquidity of $5.3 billion, coupled with a debt-to-equity ratio improvement to 1.03 times, reflects financial resilience. The preference for secured loans reinforces a solid risk profile. Q3 earnings exceeded expectations, benefiting from higher interest rates. A robust dividend yield of 9.72% and a comfortable payout ratio of 83% contribute to ARCC's shareholder value proposition.

The slight premium to NAV at 4% aligns with consistent income generation. ARCC's strategic positioning for potential interest rate cuts serves as a compelling catalyst. Lower rates could enhance net interest margins, reduce borrowing costs, and stimulate economic activity among portfolio companies. In conclusion, ARCC's prudent risk management, diversified investments, and income generation model position it for continued success in navigating evolving market conditions.

For further details see:

Ares Capital: Consistent Dividend Income To Help Fund Your Retirement