CA - Argonaut Gold: First Gold Pour At Magino Now Imminent

2023-06-11 01:55:49 ET

Summary

- Argonaut did in early May report its Q1-23 result, which was mostly in line with guidance, and the consolidated figures will improve drastically with Magino coming online.

- First gold pour is now due to be announced in the next couple of weeks and commercial production is expected in Q3-23.

- Argonaut stock still trades with an attractive valuation, despite a relatively strong stock price performance in 2023.

Investment Thesis

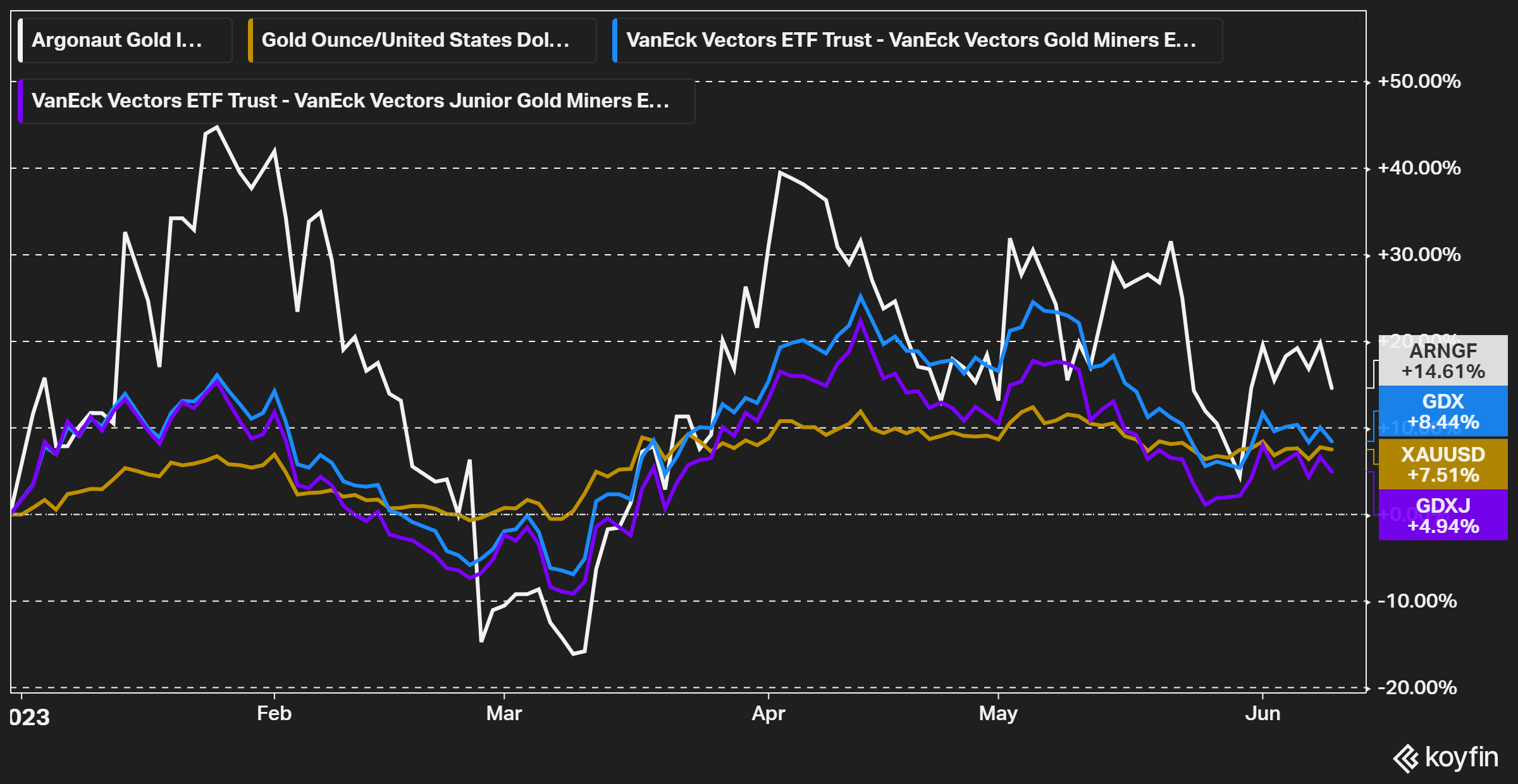

Argonaut Gold ( OTCPK:ARNGF ) has had a relatively good stock price performance this year, where it has so far in 2023 outperformed both (GDX) and (GDXJ). Given that Argonaut is a higher cost producer, it is natural that it has a higher leverage to a rising gold prices, even if that hasn't been the case for all mining companies lately.

The company's valuation remains attractive despite the good stock price performance, provided Magino comes close to its full year guidance. Argonaut did on the 1st of June communicate that the commissioning is ongoing at Magino and first gold pour is now expected by mid-June. Commercial production is still expected in Q3-23. So, everything appears to be going well, even if we have seen a few of months delay from the original plan.

{kind=link}

Figure 1 - Source: Koyfin

Q1-23 Result

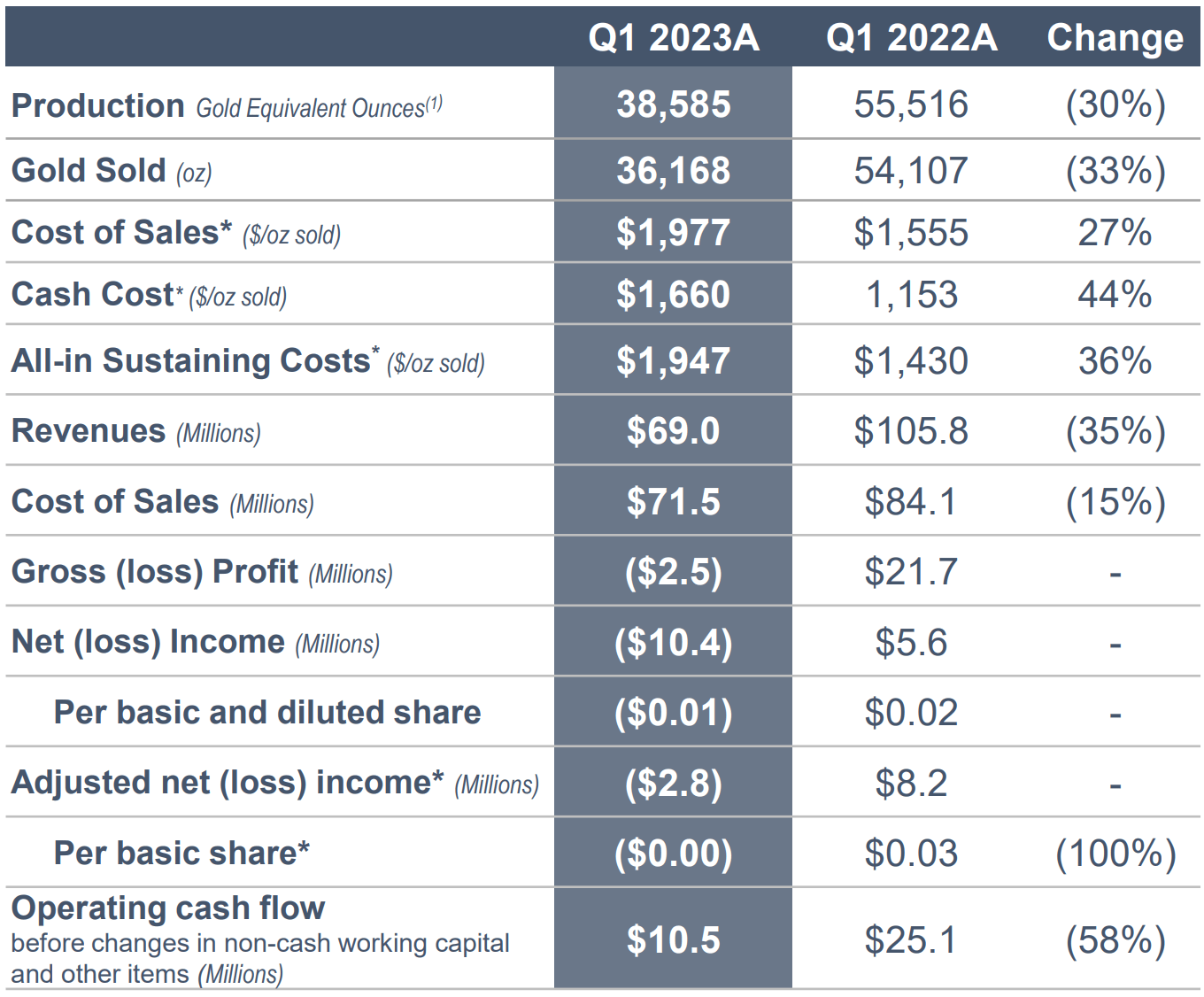

Argonaut Gold did in early May report its Q1-23 result. If we focus on the consolidated figures, it looked far from good, but the company confirmed that the results were mostly in-line with guidance and will improve throughout the year with the addition of Magino and mining higher grades at La Colorada in the next few quarters.

In the first quarter, Argonaut reported $69.0M in revenues, $10.5M in adjusted operating cash flow, and a net income of $-10.4M.

{kind=link}

Figure 2 - Source: Argonaut Gold Corporate Presentation

The production volume in Q1-23 was 38,585 gold equivalent ounces and costs remain relatively high but were also impacted by some inventory write-downs. The company reported a cash cost of $1,660/oz and an AISC of $1,947/oz.

{kind=link}

Figure 3 - Source: Quarterly Reports

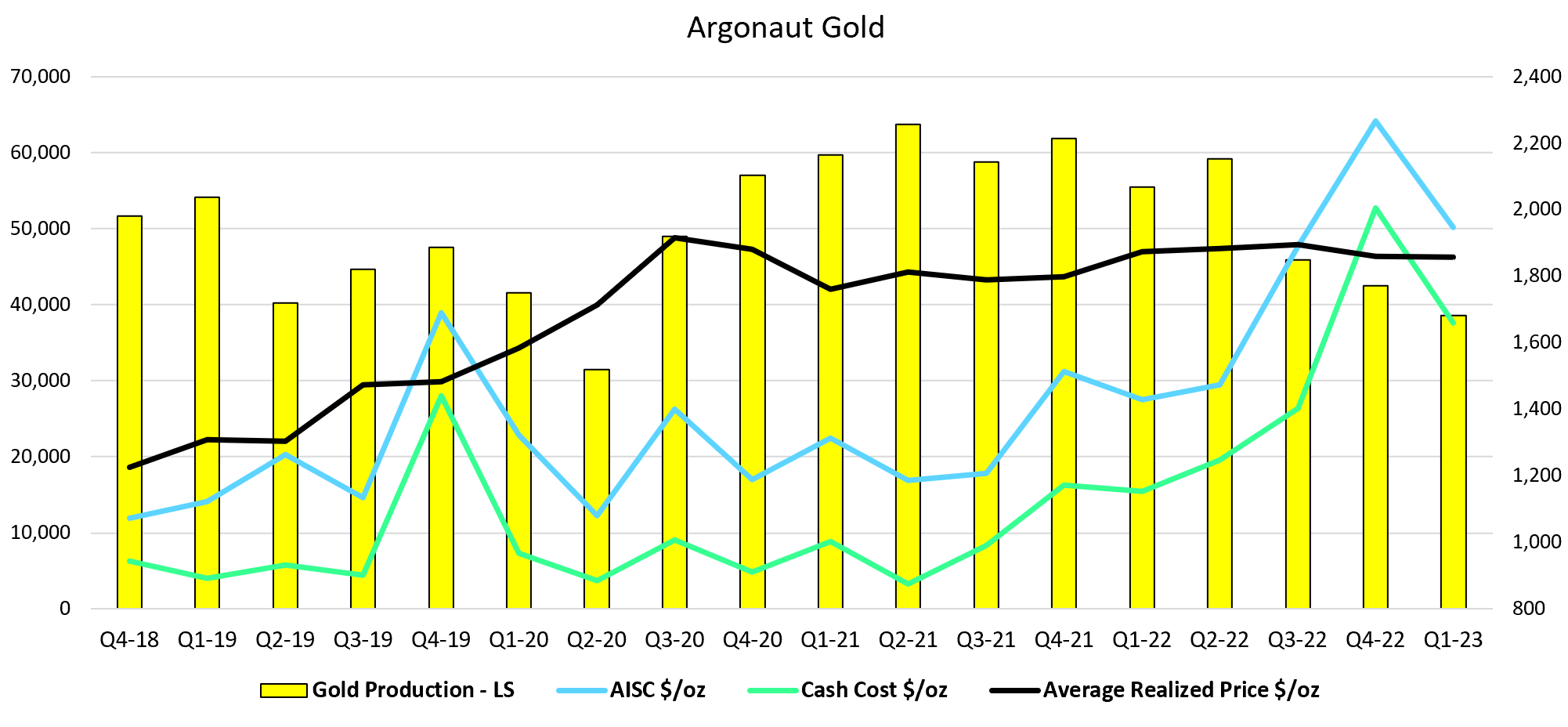

It is difficult to judge the production volume of the Mexican operations, given the current plan to stop mining late 2023.

Mining and stacking stopped at El Castillo in December last year and the asset is currently going through residual leaching. It has already in Q1-23 produced more than half of the upper end of the full year guidance. So, even with a high decline rate, I would be very surprised if that mine didn’t meet the guided production volume.

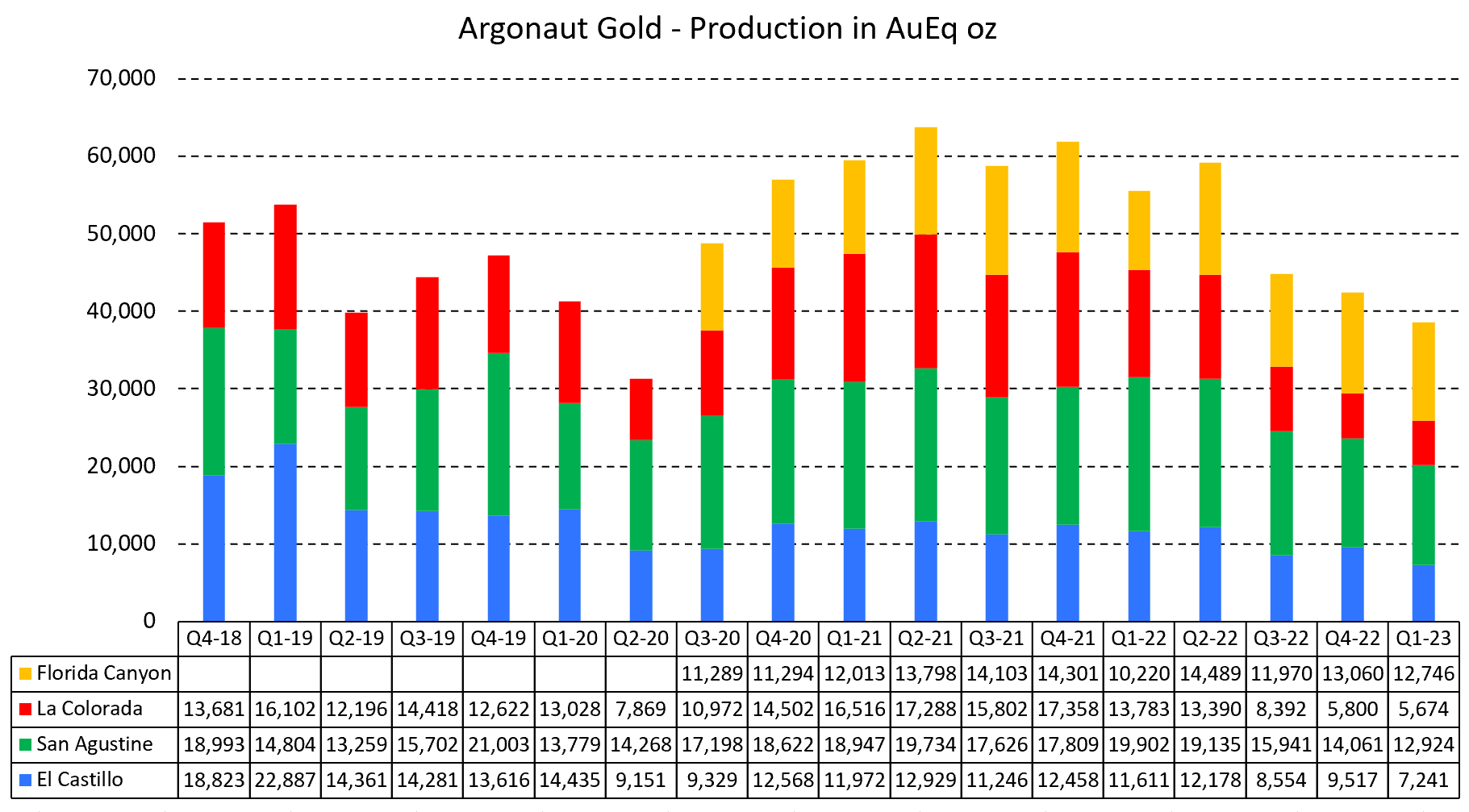

San Agustin is after Q1-23 tracking above guidance, while Florida Canyon and La Colorada are slightly below the production guidance.

{kind=link}

Figure 4 - Source: Quarterly Reports

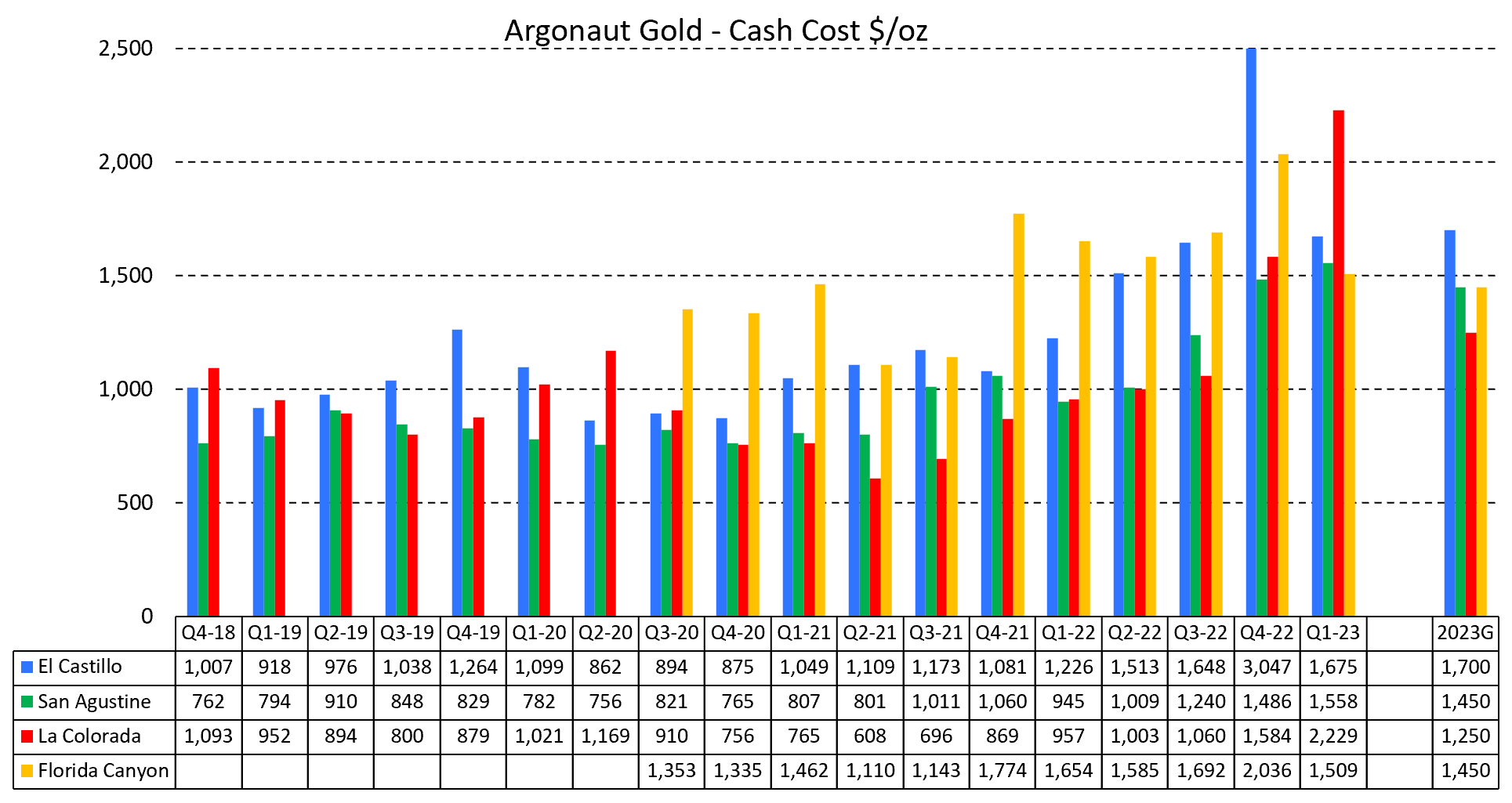

In the chart below, you can see the cash costs over time and the mid-point of what the company has guided for in 2023 furthest to the right. Where El Castillo, San Agustin, and Florida Canyon are roughly tracking guidance. It is especially noticeable that Florida Canyon was the lowest cost mine in the quarter, after some optimization work, even if costs are still high at the mine.

{kind=link}

Figure 5 - Source: Quarterly Reports

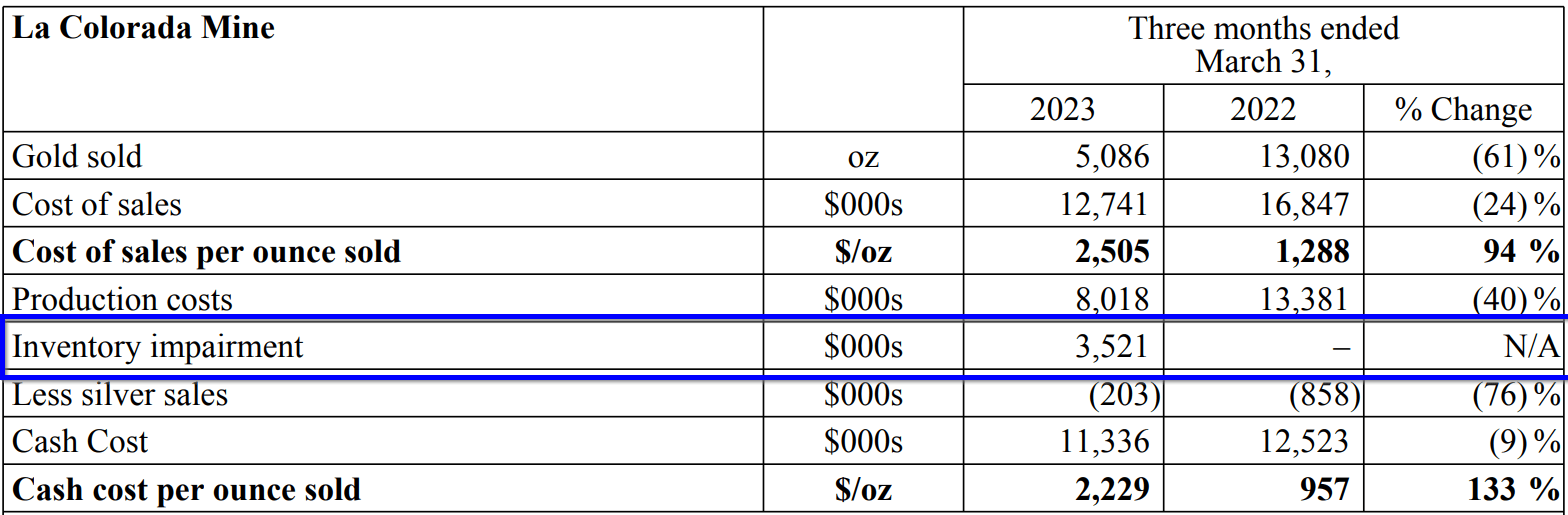

La Colorada is a different story, where the cash cost is substantially above guidance at $2,229/oz. However, the grade is expected to increase during the remaining three quarters of the year due to sequencing, which should boost production and decrease costs. The operation was also impacted by an inventory write-down, which added almost $700/oz to La Colorada's cash cost in Q1-23.

{kind=link}

Figure 6 - Source: Argonaut Q1-23 MDA

With Magino now close to production and given that the company did on the 31st of March have about $103M left to spend on Magino and somewhere around $160M in cash and debt capacity. There should not be any liquidity concerns for Argonaut Gold at this point. Especially as we have seen a relatively high gold price in 2023 as well, which will have allowed Argonaut to generate positive cash flows in Q2, even with the other high-cost operations.

Valuation & Conclusion

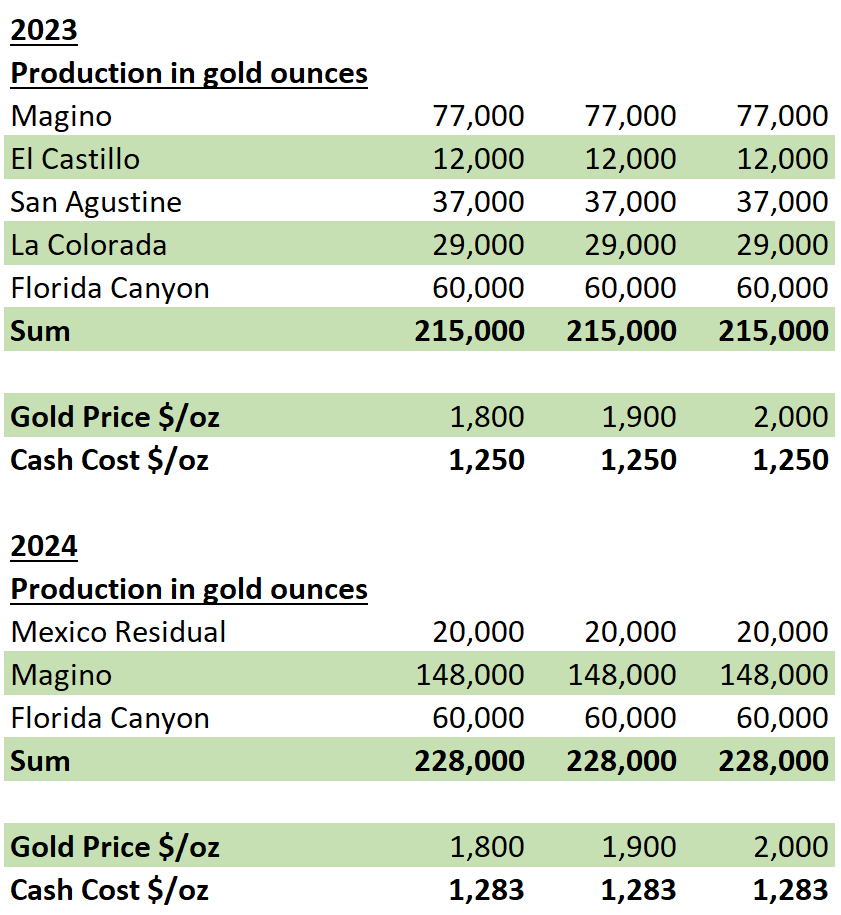

The below tables highlight the assumptions I used to arrive at my free cash flow estimates for Argonaut in 2023 and 2024. Where I have relied on the latest technical report for Magino, 2023 guidance, historical financial statements, and my best judgement having covered Argonaut Gold for over three years now.

{kind=link}

Figure 7 - Source: My Assumptions

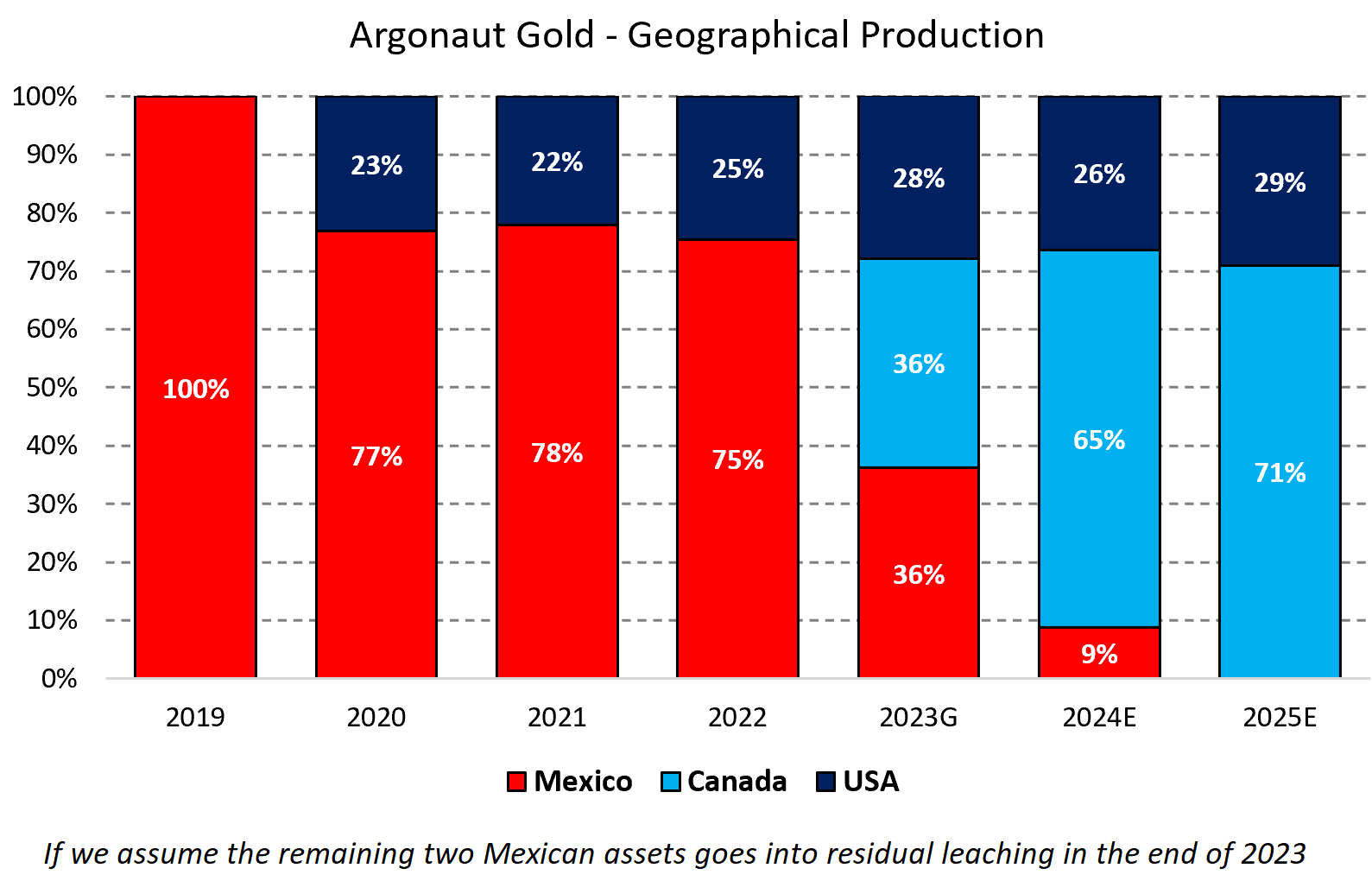

We can see that production is expected to marginally increase in 2024 compared to 2023 and the consolidate costs are also expected to increase some. This is because the Mexican assets will move into residual leaching towards the end of this year. This is a rather conservative assumption, where at least I think the high-grade ounces at La Colorada have a very good chance of being mined in the near future. So, the 2024 figures could turn out to be overly conservative.

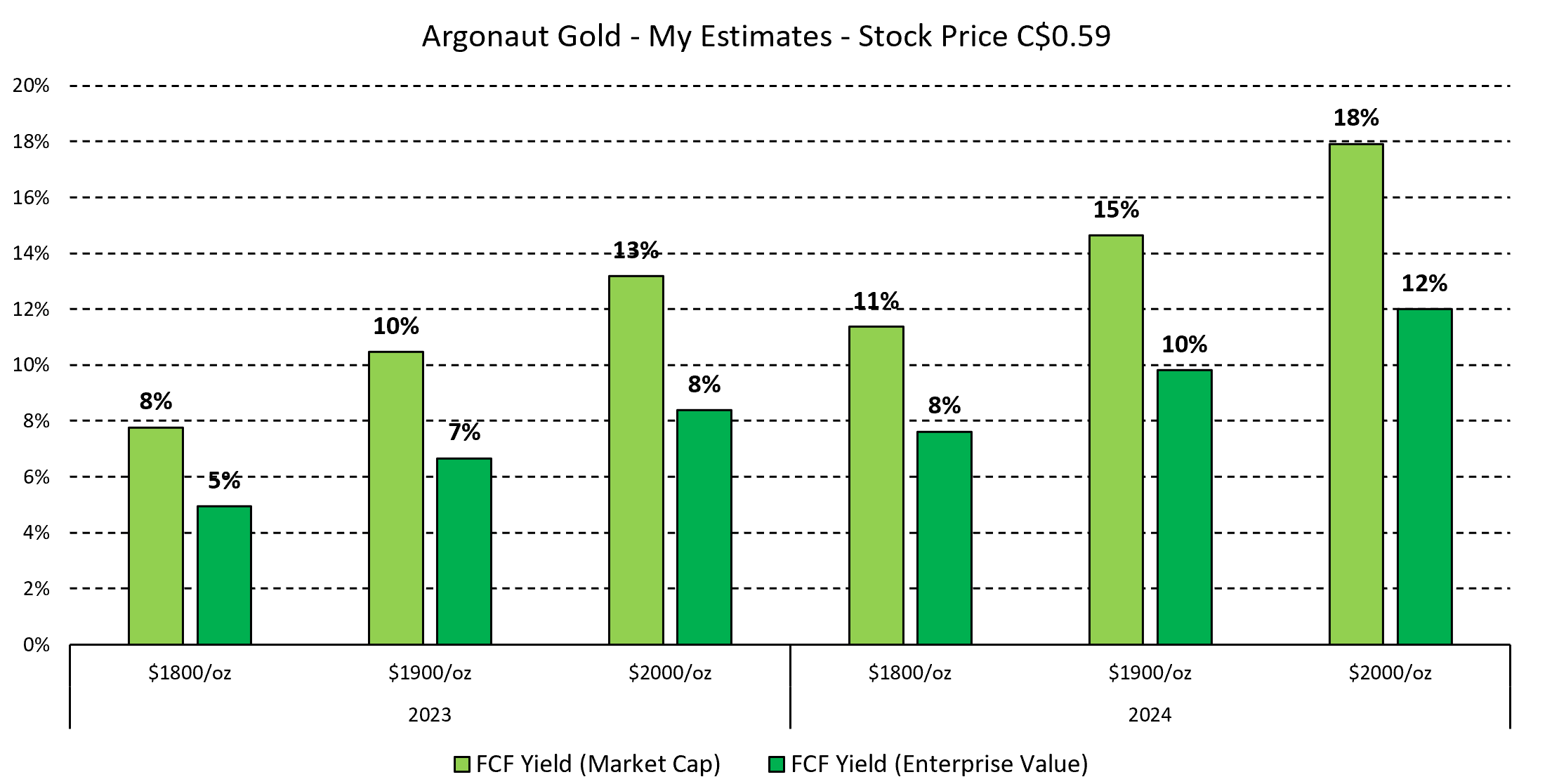

In the chart below, we can see that the FCF yield is attractive, despite a positive stock price performance lately. We are talking about a FCF yield in the 10-15% range for the next couple of years, using a $1,900/oz gold price.

Note that the gold hedges, interest expenses, and other line items from the income & cash flow statements are included in these figures. However, the Magino construction capex has been excluded in 2023.

{kind=link}

Figure 8 - Source: My Estimates

Do keep in mind that the figures are extremely dependent on Magino scaling up as planned and reaching commercial production in Q3-23, where it is relatively common to see delays for new mines reaching the design capacity. So, while the valuation is very attractive, there is still some execution risk remaining, even if much will at this point in time be behind us.

I like the risk-reward for Argonaut Gold here and I am long the stock, but would need at least a slight pullback to add to my position. The company will be generating solid cash flows and will have much or possibly all of its production coming from the U.S. and Canada going forward. That is no doubt a welcomed characteristic given the increased political risk we have seen in several South and Central American countries lately.

{kind=link}

Figure 9 - Source: Quarterly Reports, Guidance, and My Estimates

For further details see:

Argonaut Gold: First Gold Pour At Magino Now Imminent