CA - Argonaut Gold: Now Heavily Dependent On Successful Ramp Up Of Magino

Summary

- Argonaut Gold reported a very poor Q4-22 result, impacted by higher costs, an inventory write-down, and impairments of several assets.

- We are looking at another smaller cost overrun at Magino, which I am not overly concerned about.

- The company is presently planning to stop producing from all the Mexican assets by the end of 2023, due to a combination of higher costs and permitting challenges.

Investment Thesis

Argonaut Gold ( OTCPK:ARNGF ) reported its Q4-22 result earlier this week and the numbers were poor due to higher than anticipated operating costs, an inventory write down, and yet another impairment of the operating assets.

Figure 1 - Source: YCharts

This caused the stock to sell off substantially and the market cap of the company is now low compared to the NPV of Magino alone, using the current gold price.

Q4-22 Results

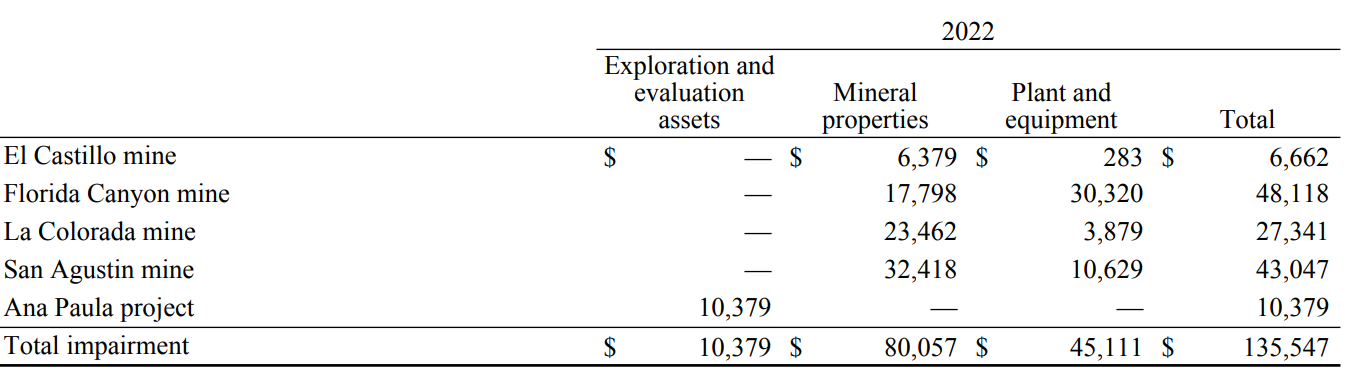

Net income during Q4-22 was $-175M and $-152M for 2022. The numbers were to a large degree impacted by the impairment of several assets. Adjusted net income was $-22M in 2022.

Figure 2 - Source: Q4-22 Financial Statement

{kind=link}

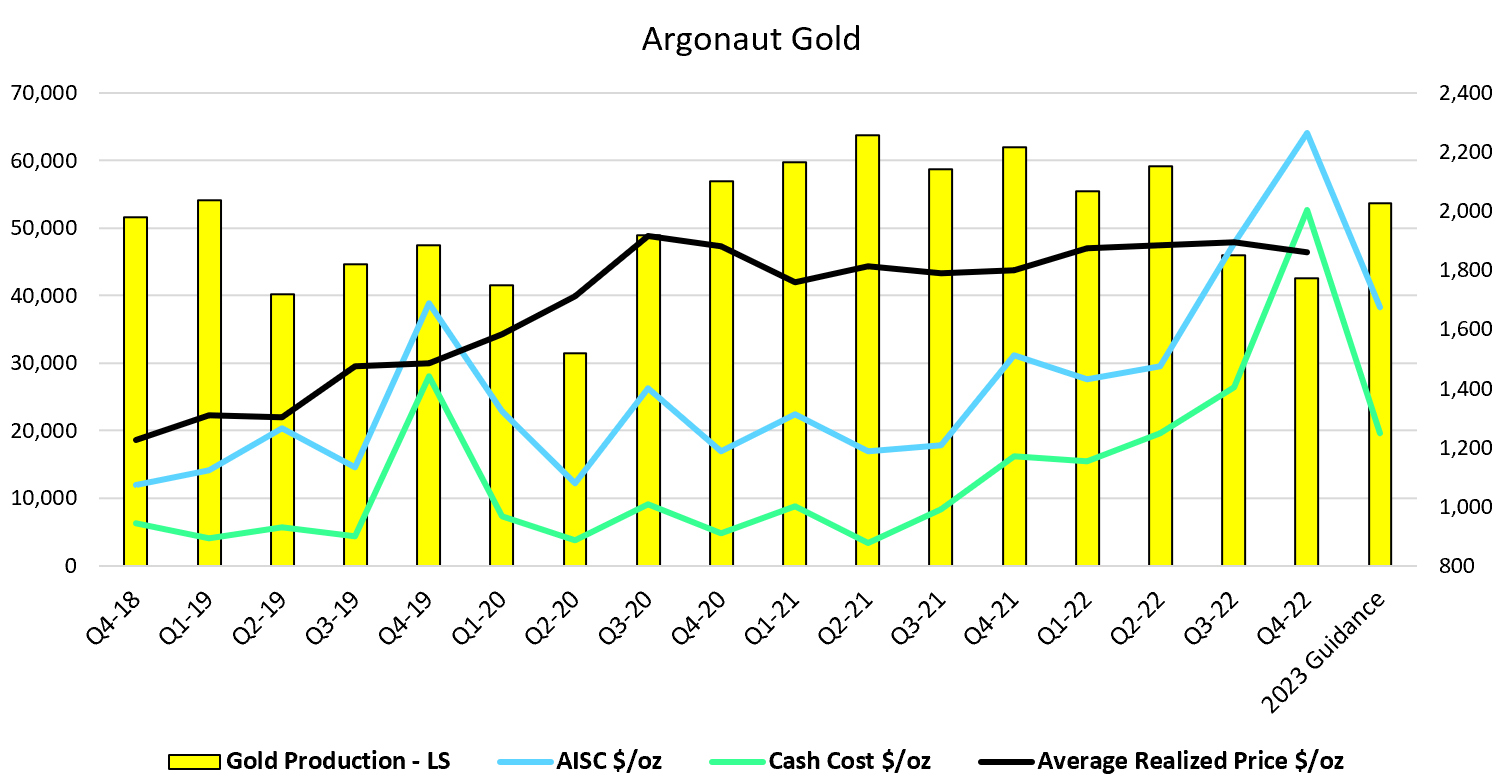

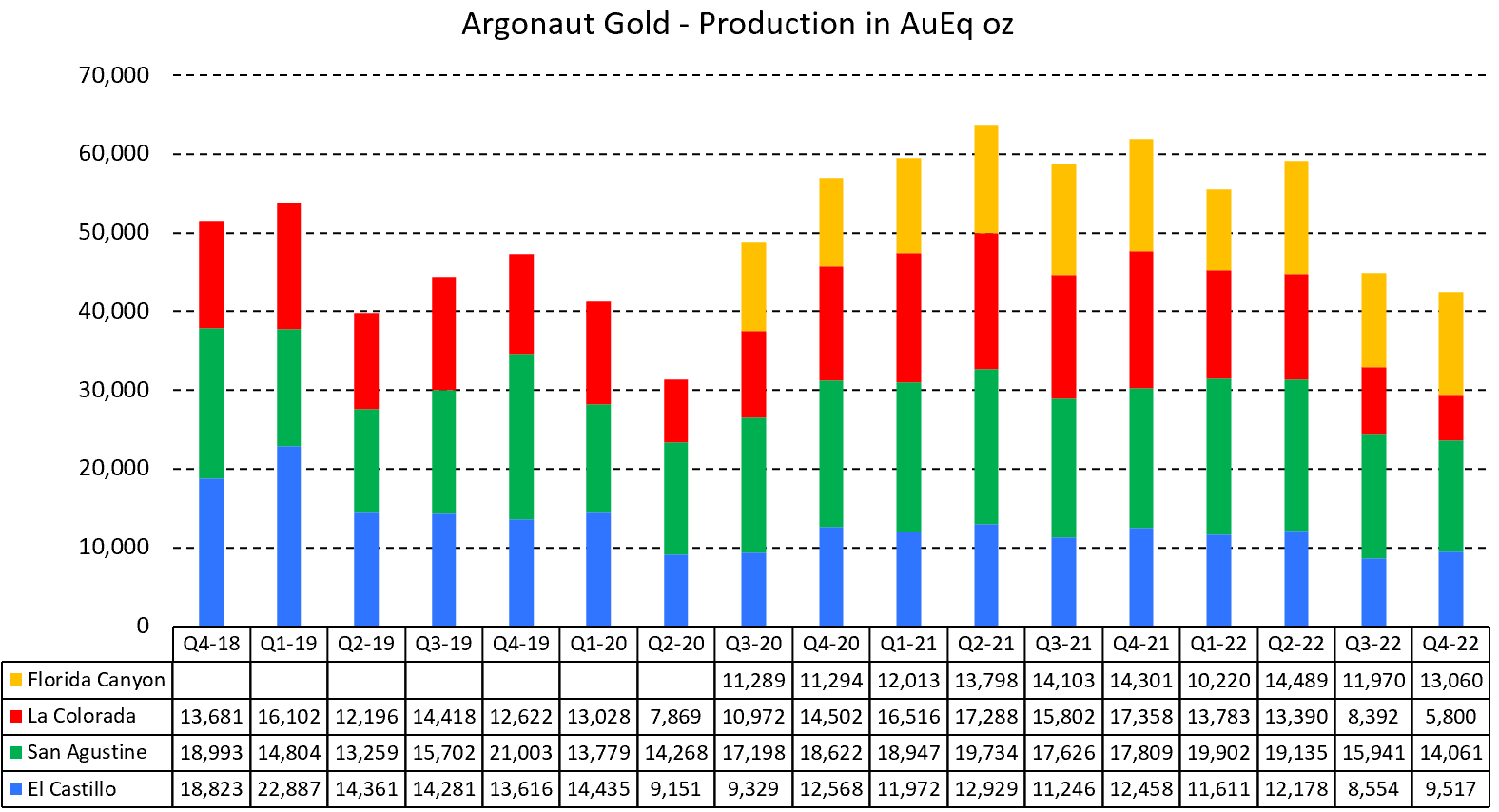

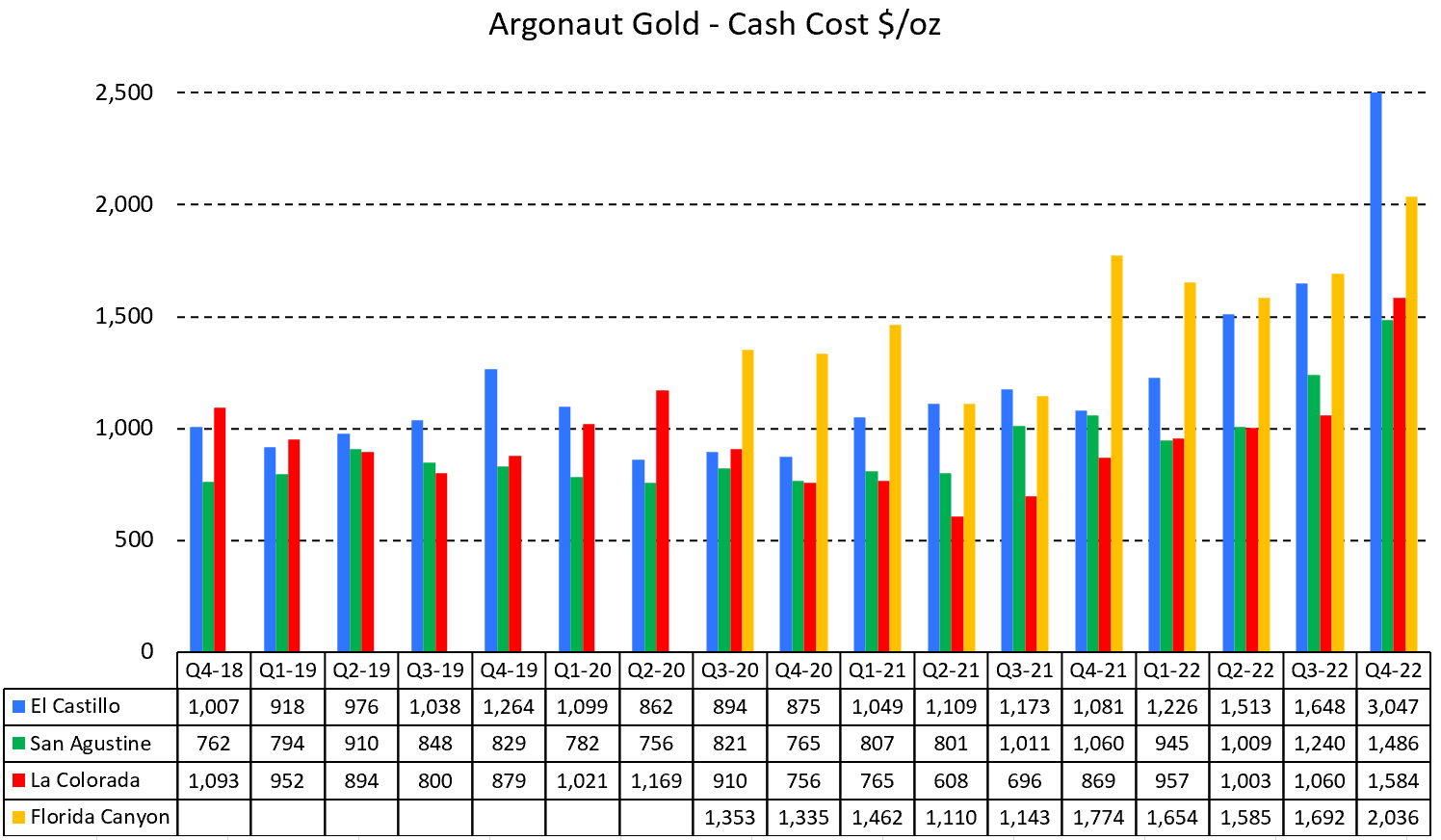

As the below figure highlights, both cash cost and AISC were extremely elevated during Q4-22, above the realized gold price. However, much of that was due to an inventory write down, which boosted cash cost & AISC by about $450/oz in Q4-22. The cost guidance for 2023 is substantially better even if it is dependent on a successful ramp up of Magino in H2-23. Argonaut's costs are in 2023 still above the industry average.

Figure 3 - Source: Quarterly Reports

{kind=link}

Magino

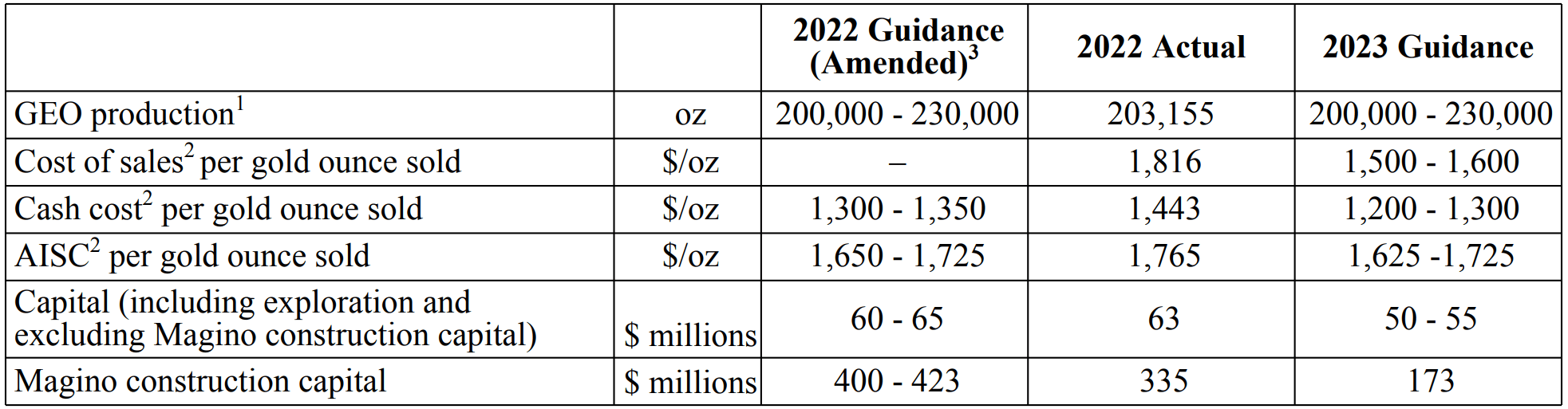

Magino is on track for its first gold pour in May of 2023 and commercial production in Q3-23. The project is running about 45 days behind schedule, but a slight delay was flagged early, and is partly due to the labor strike in Ontario a while back.

We are also looking at another increase in the total capital cost, partly due to the delay and other factors. However, we are talking about an additional $25M, which is not a massive concern in my view given the current liquidity position of about $245M, while total CAPEX for 2023 is according to guidance around $225M. Keep in mind that the cash cost guidance for 2023 is $1,250/oz, which means the company is unlikely to need additional capital to get Magino into production.

{kind=link}

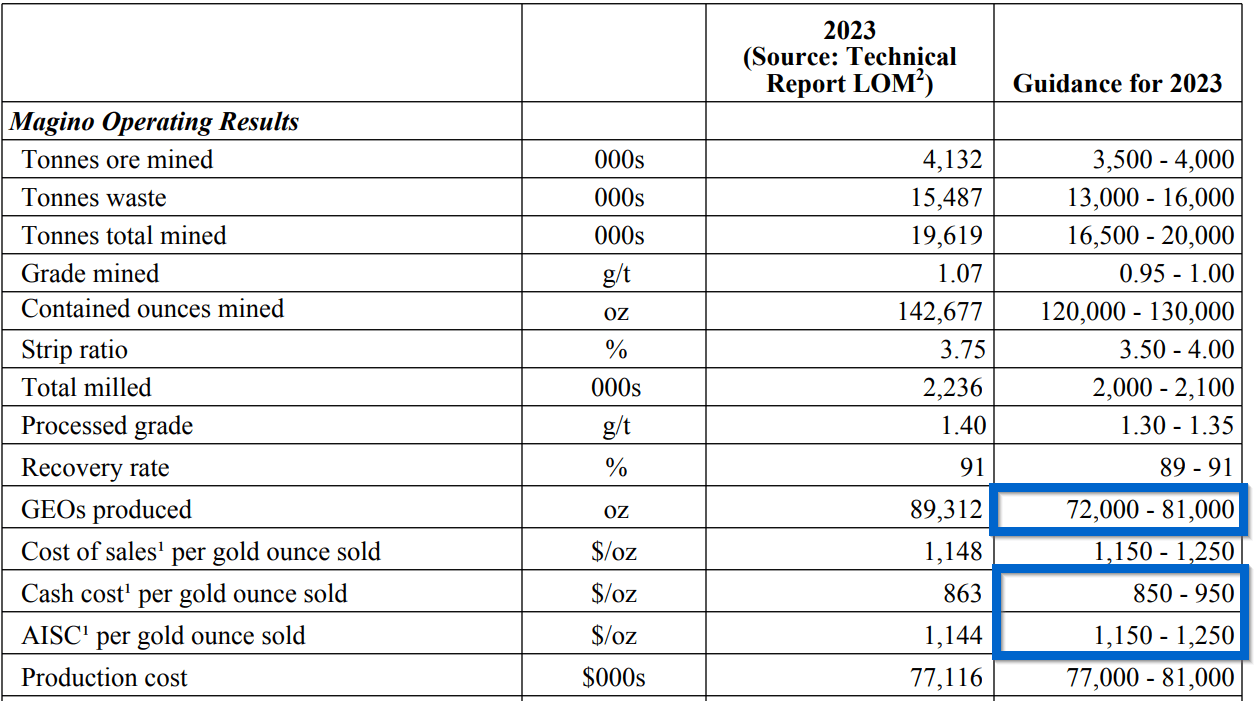

Magino is less of a concern to me at this stage, with the financing in place, and construction about 80% complete. The below figures highlight 2023 guidance for Magino, where we are looking at around 76,500 gold ounces being produced, with a cash cost around $900/oz and an AISC around $1,200/oz.

{kind=link}

Producing Assets

Argonaut Gold did in the Q4-22 result announce that El Castillo has stopped mining in December of 2022, one quarter ahead of schedule, due to cost inflation and lower recoveries. The impact from this is not that material as the asset was barely profitable before Q4-22.

Figure 6 - Source: Quarterly Reports Figure 7 - Source: Quarterly Reports

{kind=link}

{kind=link}

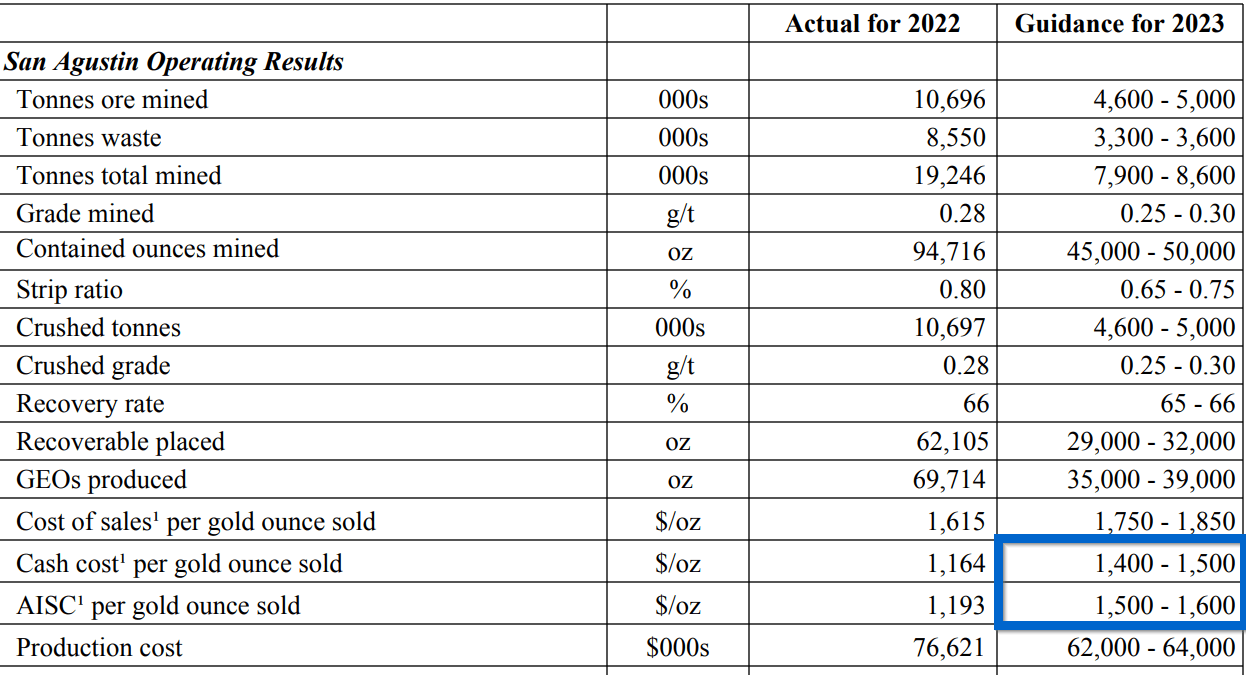

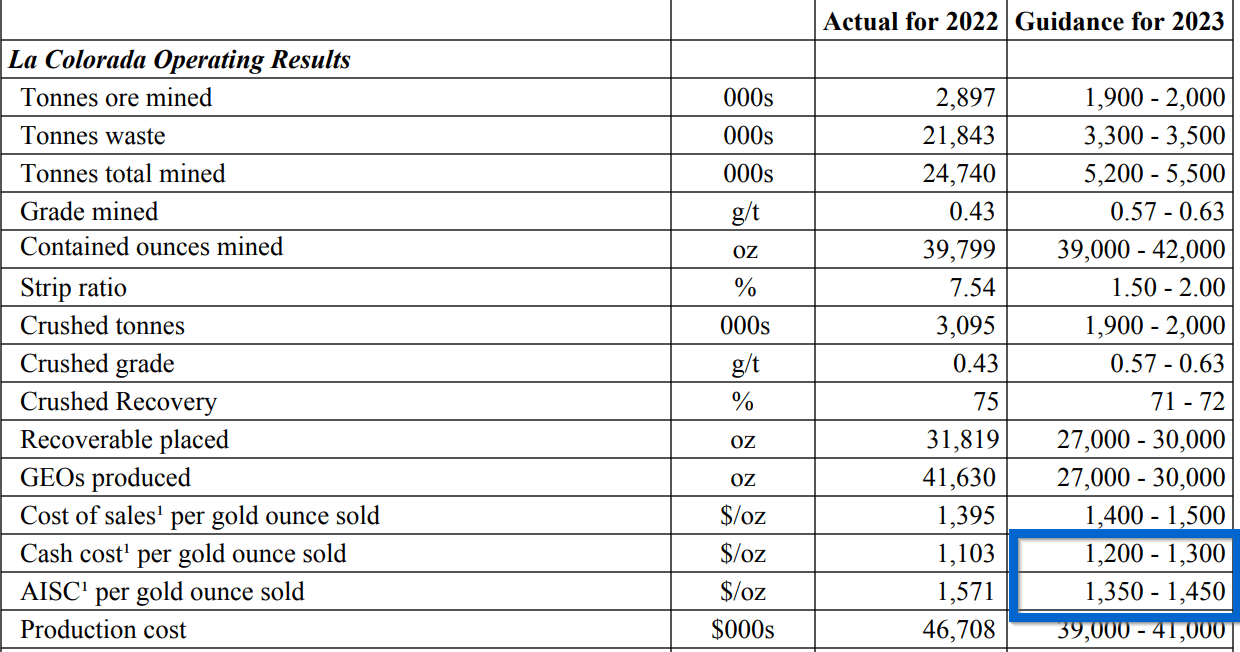

The impairment and announcement to halt production in the end of 2023 at San Agustin and La Colorada is more concerning. This is due to a combination of higher costs and permitting challenges in Mexico. If we disregard Q4-22, where the inventory write down skews the numbers, these assets have operated with decent cost levels historically, and guidance for 2023 is not terrible under the circumstances either.

This is an impairment and temporary mining halt, which will drop roughly 110Koz of gold production per year for Argonaut Gold, from the 2022 figures. However, it is not clear to me if the base case is to stop mining, or if it is partly a tactic to put some pressure on the Mexican government to issue the permits. Regardless, I do expect the high-grade ounces at La Colorada will be mined relatively soon, where a trade-off study is being conducted during 2023.

Figure 8 - Source: Q4-22 MDA Figure 9 - Source: Q4-22 MDA

{kind=link}

{kind=link}

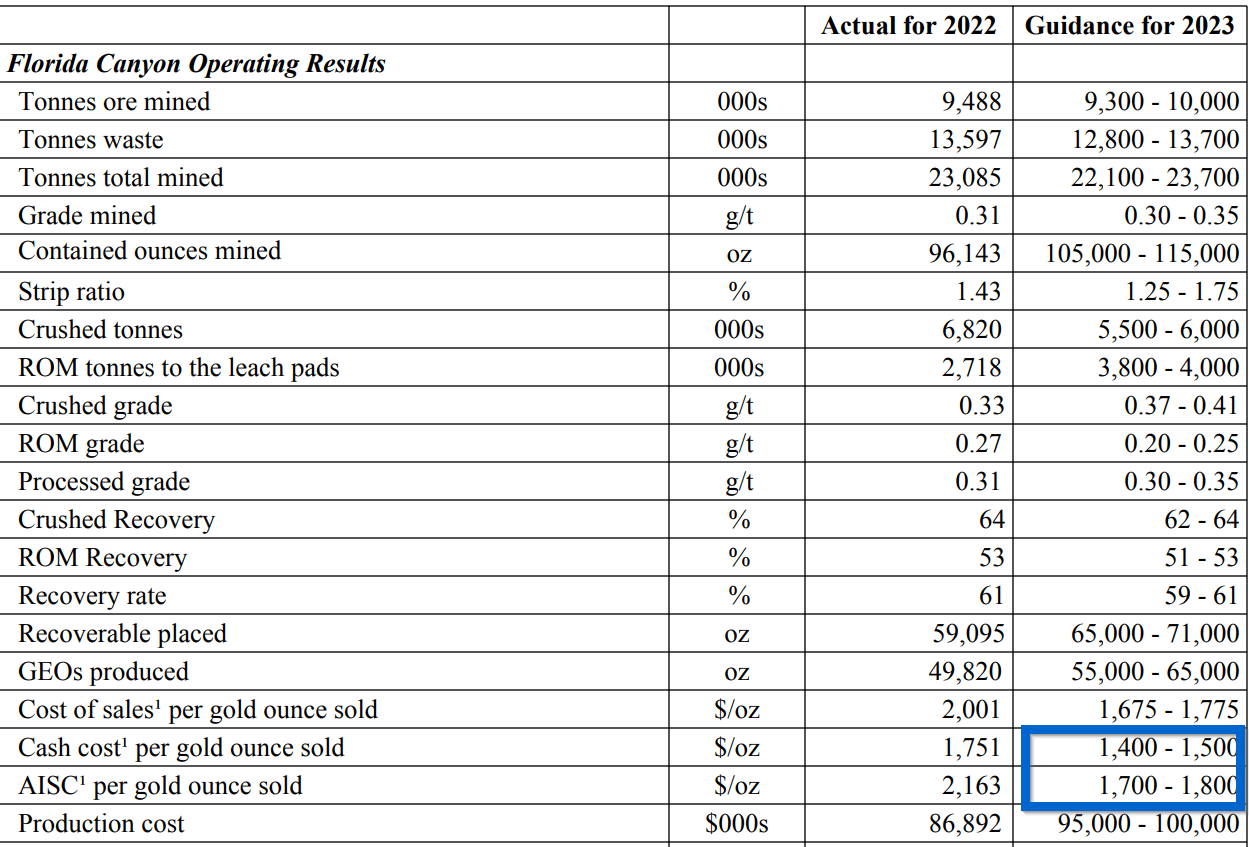

Florida Canyon will continue to operate, and the company hopes to optimize operations and potentially mine sulfide resources more profitably, but I continue to be skeptical about the viability of this asset. Where 2023 guidance for AISC is around $1,750/oz, even if that is an improvement over 2022.

{kind=link}

Conclusion

Following the changes to the mine plans, the company is guiding for about 215,000 gold ounces of production in 2023. If the Mexican assets do in fact stop producing in late 2023, we will unfortunately not see much production growth in 2024, and costs should not decrease much either. A larger portion of production will in 2024 come from Magino, which has lower costs, but the remaining portion will also come from Florida Canyon, which is likely to have higher costs than the Mexican producing assets in 2023.

The stock price of Argonaut is now to an even larger degree dependent on the successful ramp up of Magino, with the Mexican assets looking to stop producing soon. Having said that, with a market cap around $270M, this is still a very cheap stock given that Magino alone has an NPV well above that level.

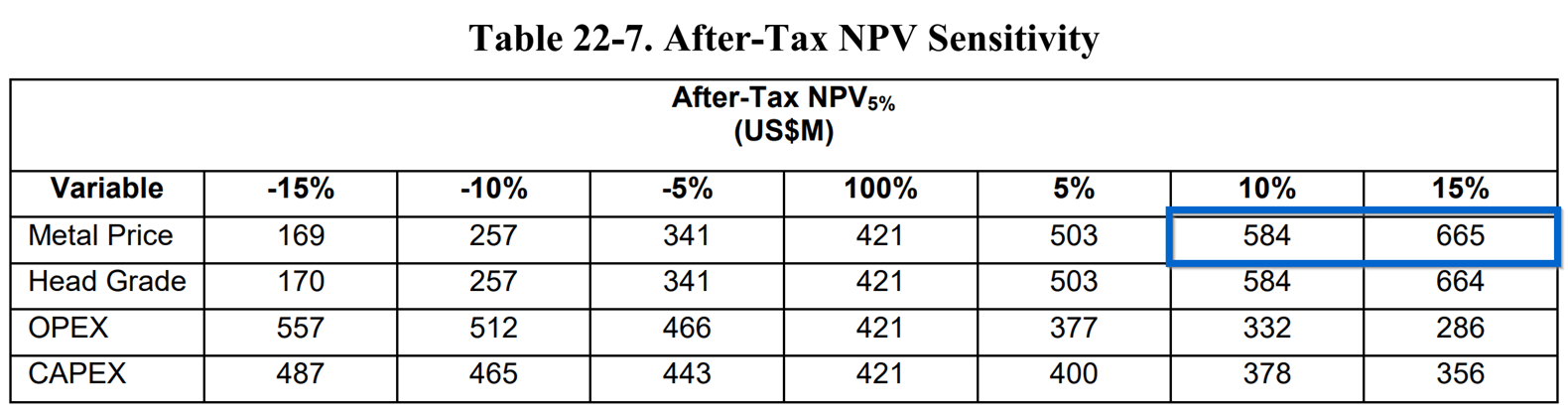

Argonaut did in early 2022 update its feasibility study, but the capital costs are unfortunately already somewhat obsolete due to the cost overruns. The after-tax NPV was around $625M in the updated feasibility study at the current gold price.

Figure 11 - Source: Magino 2022 FS

{kind=link}

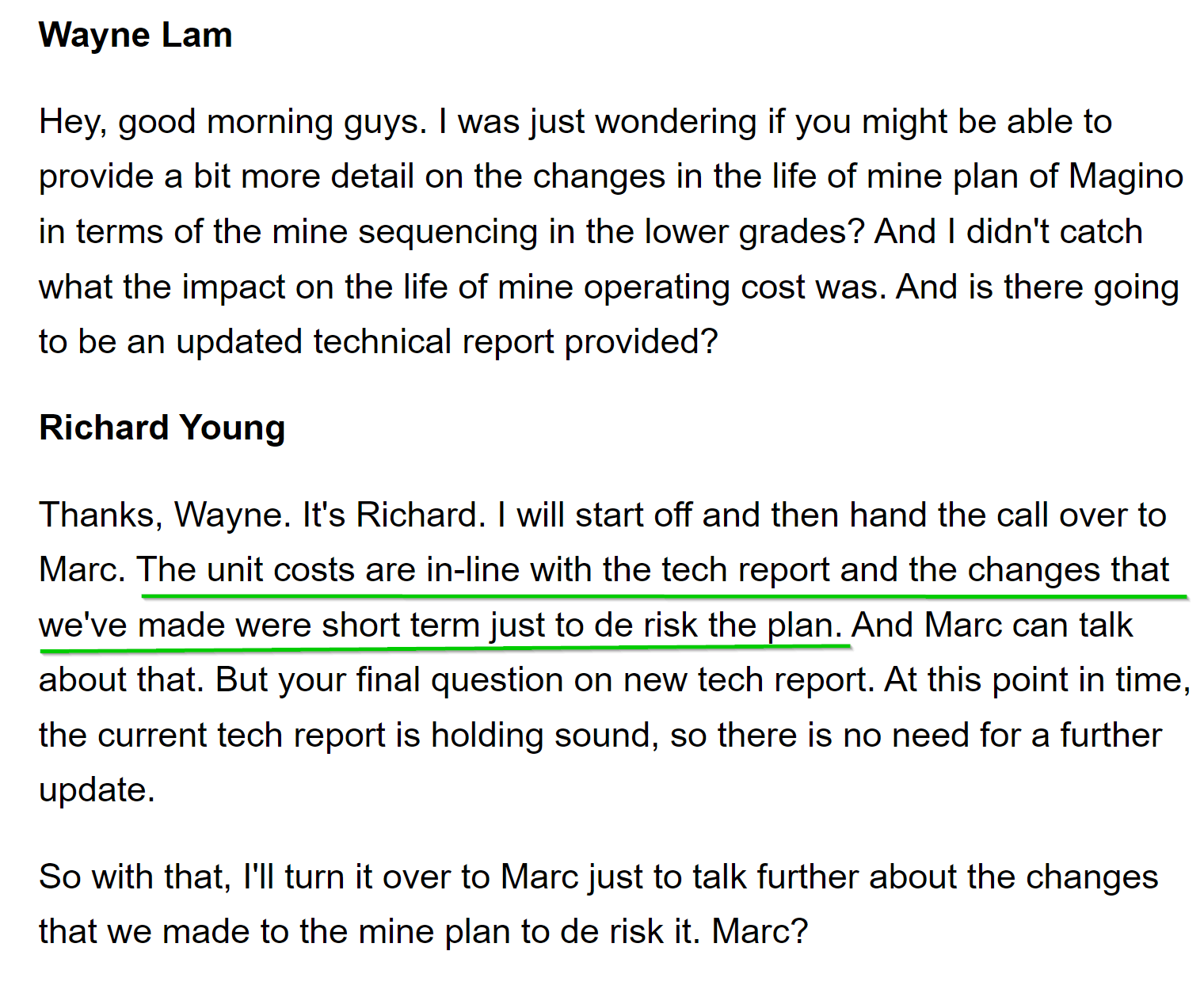

While the cost overruns have been far from beneficial to existing shareholders over the last couple of years, I would argue the NPV is actually higher at this point given that even more of the initial capital cost can today be viewed as a sunk cost, while operating costs are still tracking the feasibility study according to the CEO on the Q4-22 conference call .

Figure 12 - Source: Q4-22 Conference Call

{kind=link}

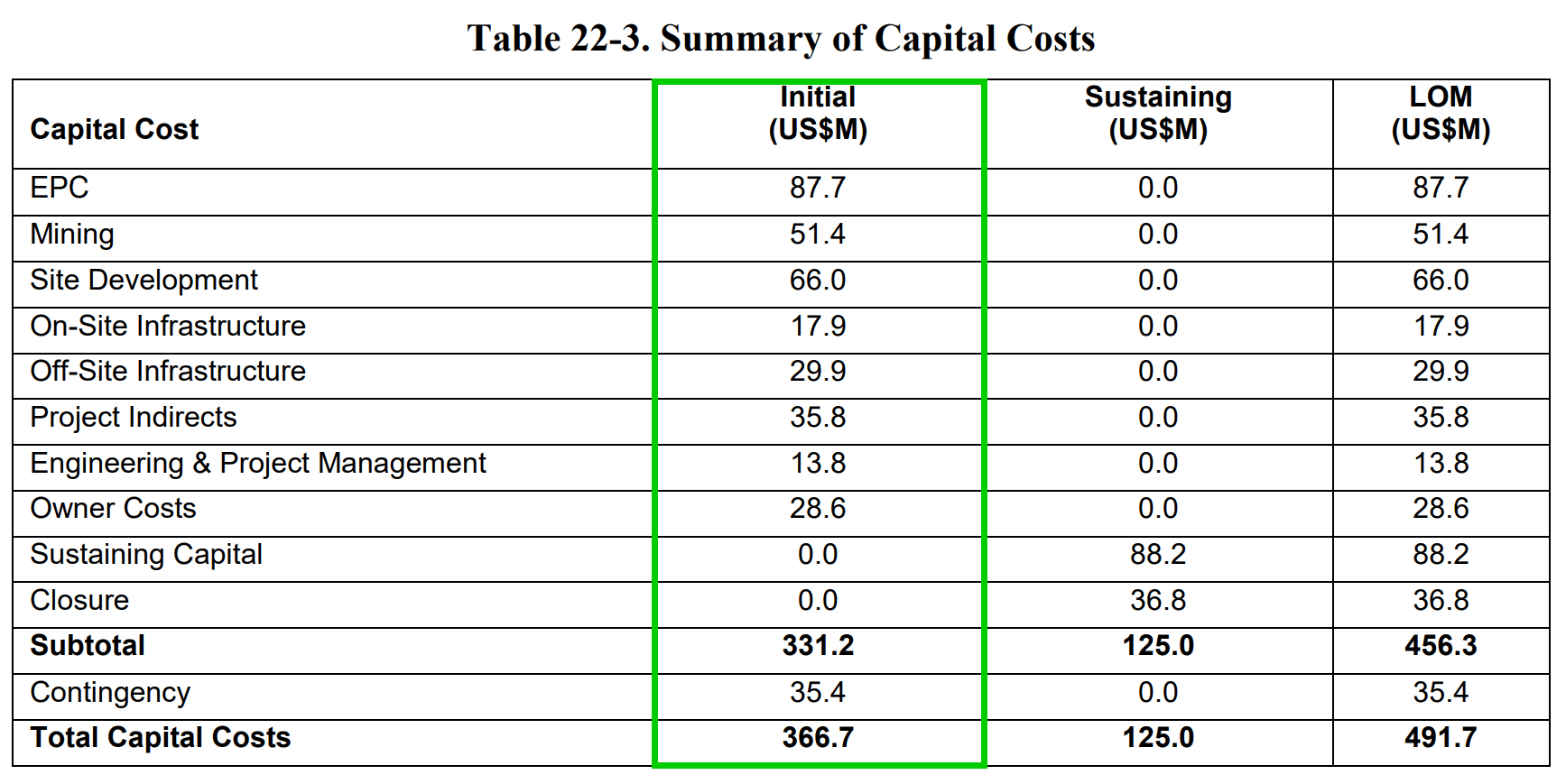

The 2022 feasibility study had $366.7M in initial capital cost for 2022-2023, but the company has confirmed that there is only $173M construction costs left to spend on Magino in 2023, see guidance in figure 4 earlier in the article. Another point not reflected in the feasibility study is that Argonaut sold a 2% net smelter return royalty for $52.5M on the asset. So, after adjusting for the remaining initial capital cost and new royalty, I would argue the NPV for Magino is somewhere around $736M today ($625M+$336.7M-$173M-$52.5M).

Note that these adjustments do not take into account the lower tax payments for the project, which will naturally follow the higher capital investments & depreciations, and will further boost the actual NPV.

Figure 13 - Source: Magino 2022 FS

{kind=link}

Also, even though the cashflows from the Mexican assets would have been very welcomed for a few more years, note that the overall political risk will drastically decrease for the company once the Mexican assets have gone through residual leaching.

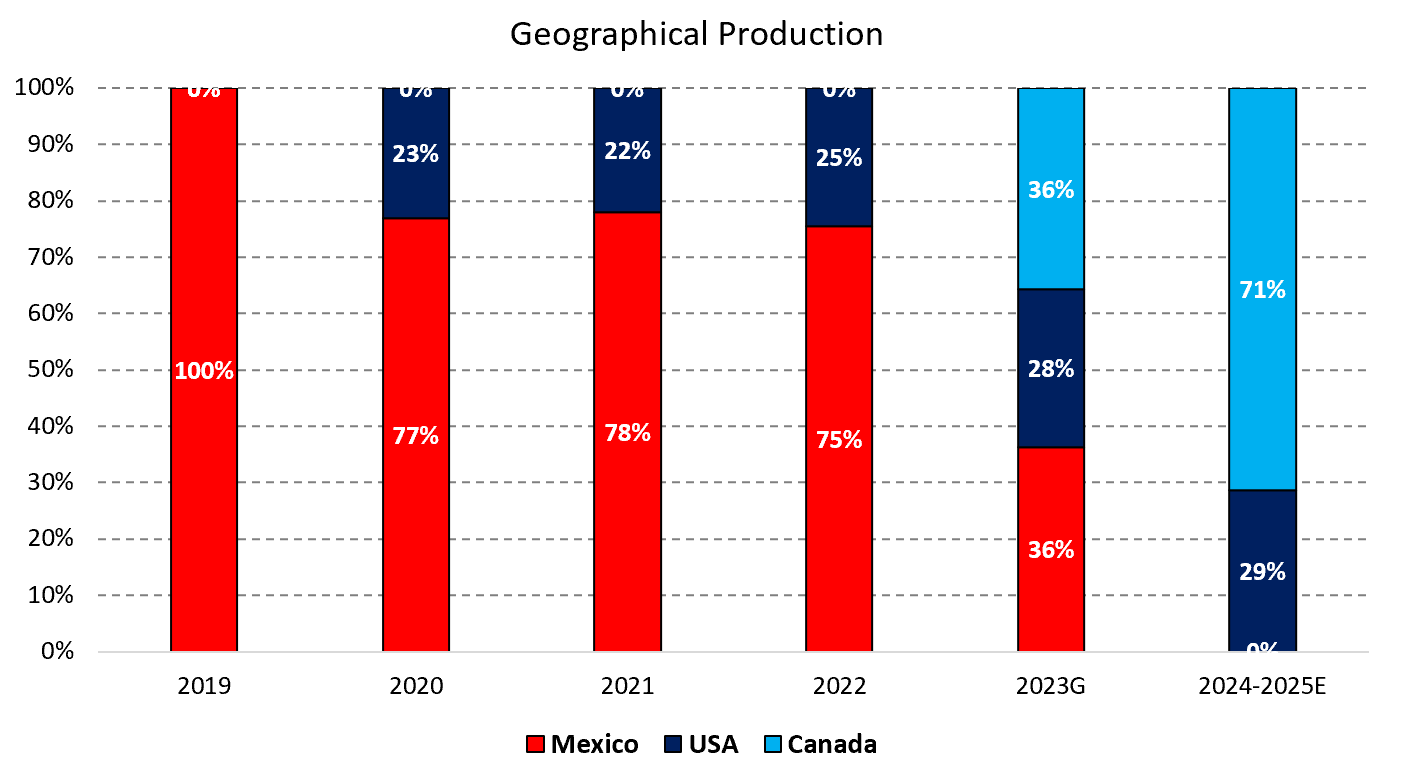

Figure 14 - Source: Annual Reports, Guidance, & My Estimates

{kind=link}

For further details see:

Argonaut Gold: Now Heavily Dependent On Successful Ramp Up Of Magino