CA - Argonaut Gold: Tight Labor Market And Rising Energy Prices Could Impact H2

2023-09-04 04:04:32 ET

Summary

- Argonaut Gold released its Q2 results last month, reporting a near 30% decline in GEO production at all-in sustaining costs of $1,594/oz.

- And while bringing the lower-cost Magino Mine online will help, Argonaut has back-end weighted sustaining capital spend, is dealing with labor tightness, and now rising energy prices.

- In this update, we'll look at the Q2 earnings, the H2 2023 outlook, and whether these headwinds (labor tightness, sector-wide contractor inflation, rising energy prices) are priced into the stock.

Just over three months ago, I wrote on Argonaut Gold ( ARNGF ), noting that further weakness in the stock would provide a buying opportunity. This is because its new Magino Mine was nearing completion, and while the mine was a month behind schedule and over ~100% above its initial budget, Magino would transform the company with a lower cost profile and a shift to being a mostly Tier-1 jurisdiction producer. Jus as importantly, the previous management has been replaced with a highly successful leader in Richard Young (former Teranga). Since then, Argonaut has easily outperformed the Gold Juniors Index ( GDXJ ) with a 30% plus excess return vs. its benchmark, and with a solid asset in a Tier-1 jurisdiction barely a month away from commercial production, the future is much brighter for the company. However, as I'll detail in this update, some of this has been priced into the stock after its ~130% rally and headwinds remain in place, resulting in a more mixed outlook short-term.

In this update, we'll dig into the Q2 results, what has changed, and why it might be time to consider taking some profits above US$0.54.

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Sales

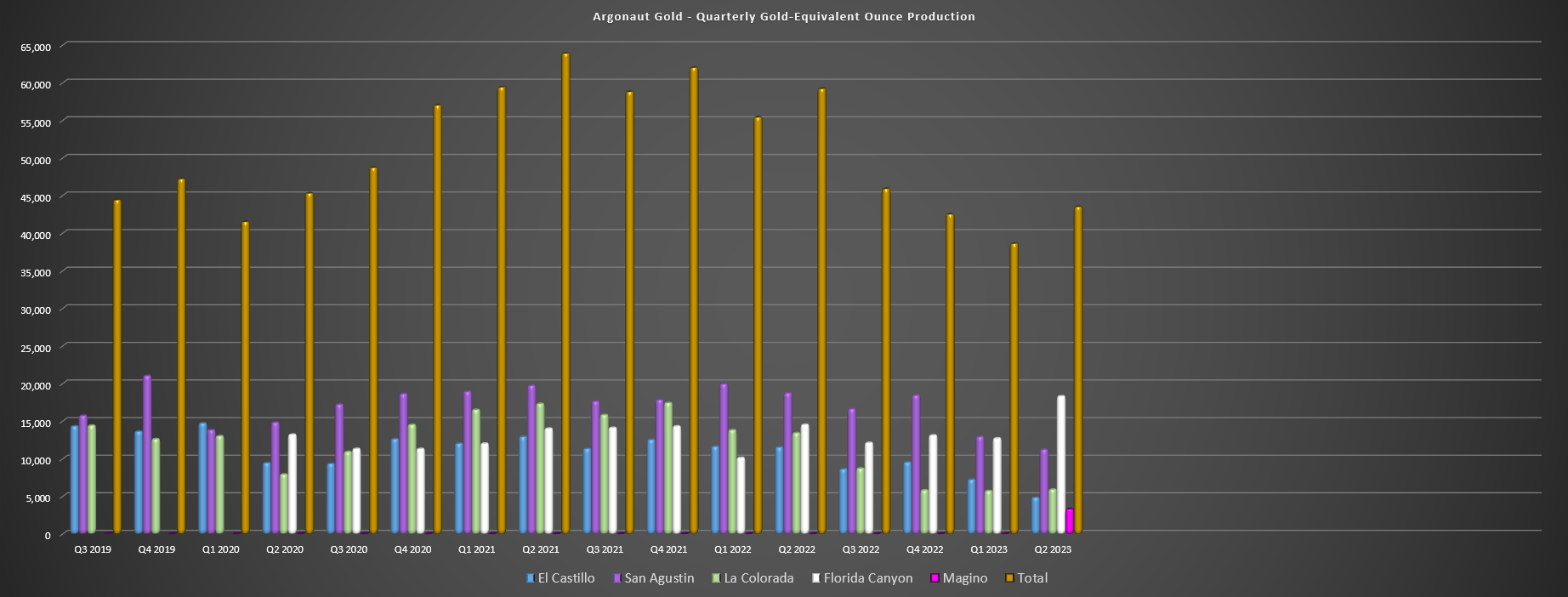

Argonaut Gold released its Q2 results last month, reporting quarterly production of ~43,500 gold-equivalent ounces [GEOs], a 27% decline from the year-ago period. Argonaut's sharp decline in consolidated production was related to lower output from its Mexican operations with no production at the El Creston pit (La Colorada), fewer tonnes of ore mined and processed at San Agustin, and re-leaching of pads taking place at El Castillo following suspension of mining in December. This was offset by a better quarter at Florida Canyon and initial contribution from the company's new Magino Mine in Ontario, Canada. While this headline production figure may appear disappointing, this was largely in line with plans, and year-to-date production is tracking with the FY2023 guidance of 215,000 ounces with a stronger H2 on deck (La Colorada, steady ramp-up at Magino with commercial production expected by October).

Argonaut Gold - Quarterly GEO Production - Company Filings, Author's Chart

{kind=link}

Digging into the results a little closer, we can see that Magino produced ~3,300 ounces of gold in June (72 ounces sold), and the company noted that the ramp-up is progressing well, with $730 million of the $755 million estimated cost to completion spent at Magino. That said, Argonaut noted that sourcing remaining labor has been a challenge and that vacant roles are being filled by contract personnel, a negative development that will put pressure on mining costs until resolved. This is consistent with what we're seeing sector-wide, with several producers in prolific jurisdictions commenting on turnover and even large ones like Gold Fields ( GFI ), with Gold Fields noting that mining costs continue to trend higher as salaries increase and it has stuck with its ~6% inflation estimate in 2023 despite a tailwind from a weaker Australian Dollar. So, with Argonaut also operating in prolific jurisdictions (Nevada and Ontario), this could put further pressure on operating costs at both its assets, the $907/oz cash cost at Magino doesn't look conservative enough.

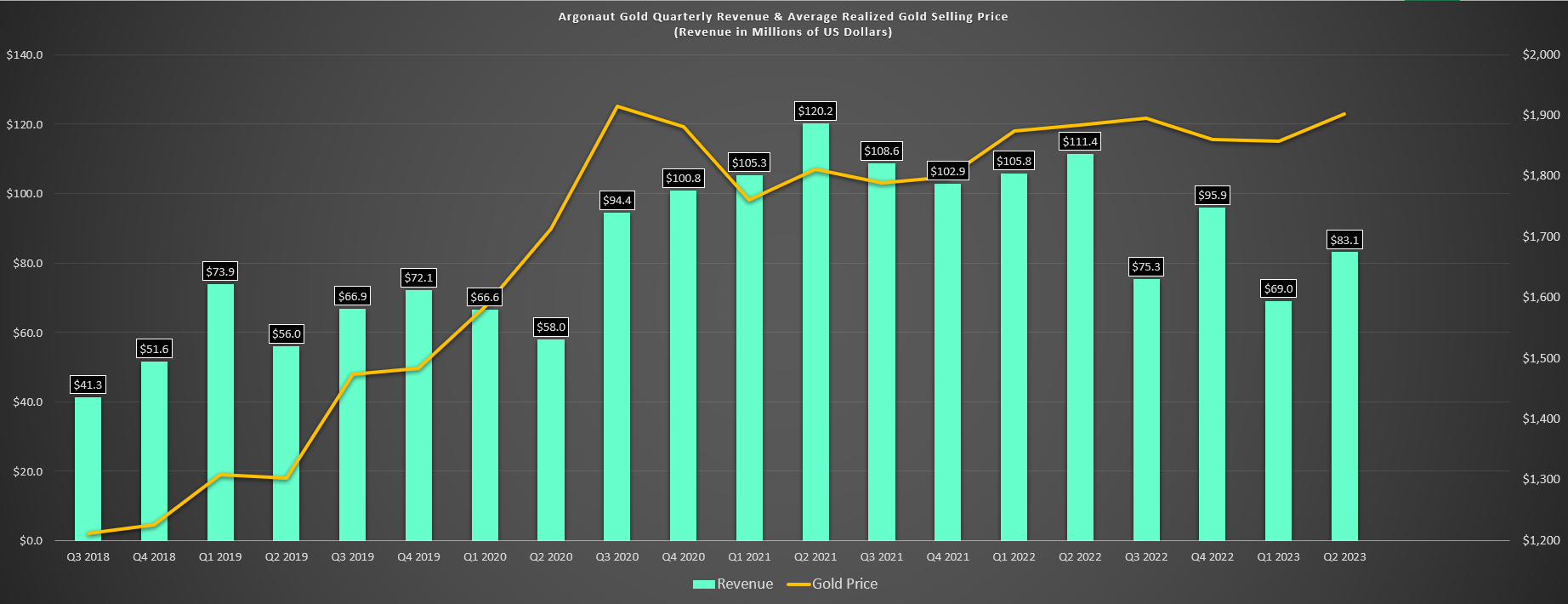

Argonaut Gold - Quarterly Revenue & Average Realized Gold Price - Company Filings, Author's Chart

{kind=link}

Meanwhile, at Florida Canyon, the company increased production levels to ~18,300 ounces vs. ~14,500 ounces in Q2 2022, with the increase driven by more run of mine ore being placed on its heap leach pads. However, while costs were down year-over-year because of being up against easy comps ($2,063/oz), they remained elevated at $1,662/oz in the period, and given the low grades and lack of economies of scale here, it's tough to envision this asset consistently producing gold at sub $1,500/oz all-in sustaining costs, suggesting it will struggle to generate any meaningful free cash flow. The result of the lower production and higher costs year-over-year was that Argonaut generated $17.4 million in operating cash flow (down 25% year-over-year), and finished the quarter with $72 million in cash and ~$152 million in net debt. Meanwhile, revenue sunk to $83.1 million despite a near-record average realized gold price (lower sales and deliveries into gold forward contracts at $1,888/oz).

Costs & Margins

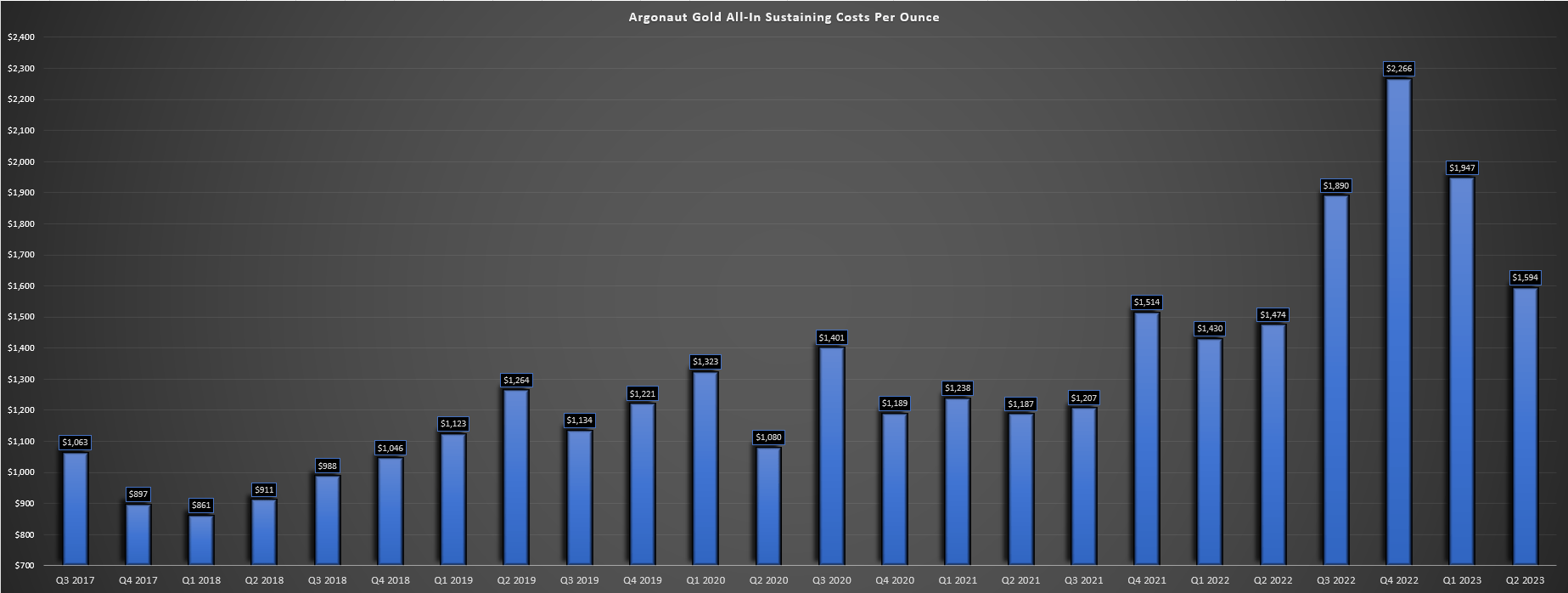

Moving over to costs and margins, Argonaut reported all-in sustaining costs of $1,594/oz in Q2 2023, just over a 2% increase from $1,553/oz in the year-ago period. The company's all-in sustaining costs benefited from lower sustaining capital, which is tracking at less than 20% of annual guidance ($50 - $55 million) which suggests major catch-up in H2, but this will fortunately be offset by much higher production from its Magino Mine, which is expected to produce at least 70,000 ounces of gold in the second half of this year. Unfortunately, the record average realized gold price didn't help from a margin standpoint given that ~32,400 ounces were delivered at prices well below spot ($1,888/oz), resulting in AISC margins of $309/oz in Q2 2023, down from $331/oz in Q2 2022 despite a higher average realized gold price ($1,903/oz vs. $1,884/oz). And this underperformance from a realized price standpoint will continue, with considerable gold forward contracts locked in between now and 2027.

Argonaut Gold - Quarterly AISC - Company Filings, Author's Chart

{kind=link}

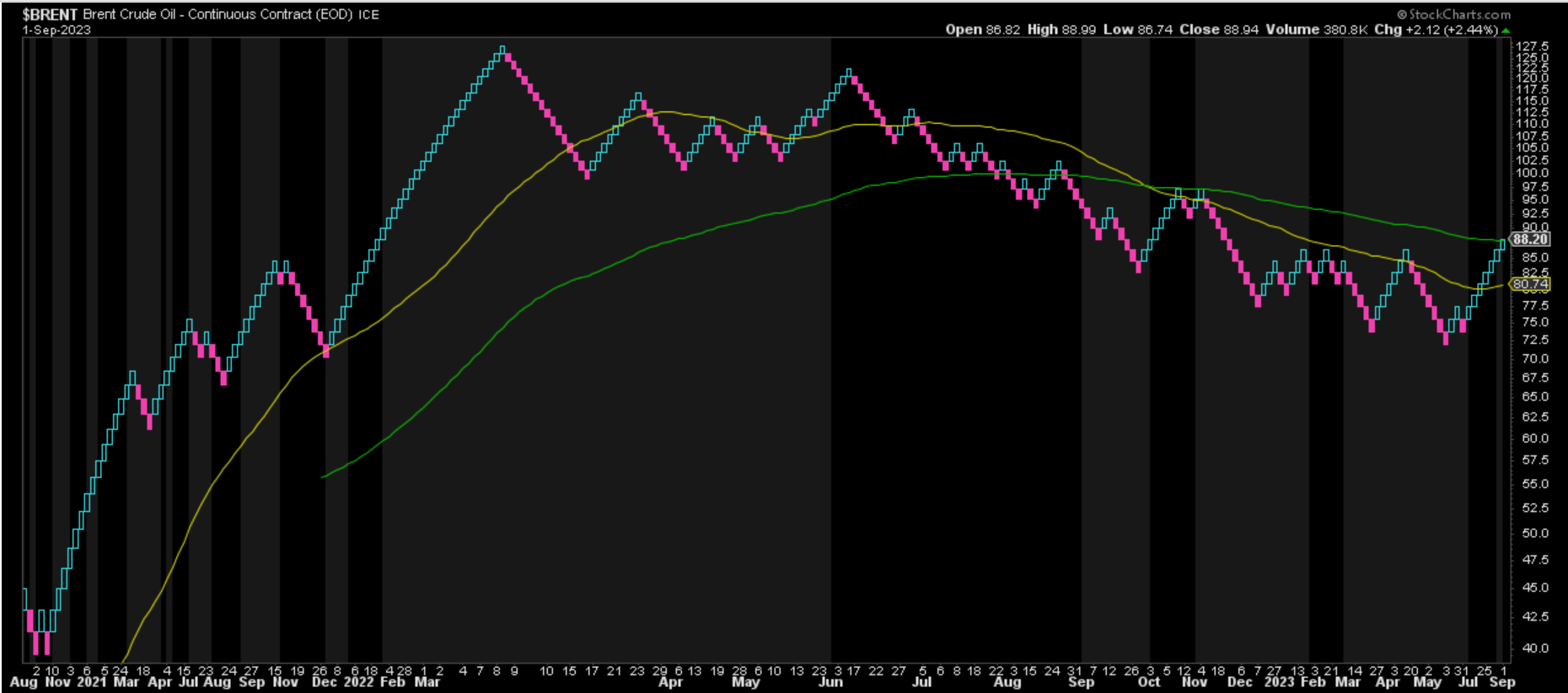

As for inflationary pressures, Argonaut operates several high-volume and low-grade operations, meaning that the lower fuel prices were a nice tailwind in H1 of this year with a dip in oil prices. However, this has not been the case thus far in H2, with energy prices rebounding off their June lows in a near straight line off their May lows. This is not ideal, nor is the company's disclosure that mining costs will be higher than planned due to delays in expanding and staffing the mobile equipment fleet, with rental equipment and contract operators set to be used for the remainder of 2023. In addition, mobile equipment maintennace is above plan partially related to a shortage of experienced operators and personnel. So, with a rebound in energy prices, back-end loaded sustaining capital spend, short-term headwinds due to a tight labor situation and limited exposure to the higher gold prices as an offset, I'm not sure that the H2 results will be nearly as robust as some investors might be expecting from a margin standpoint.

Brent Crude Prices - StockCharts.com

{kind=link}

On a positive note, Magino is expected to produce over 140,000 ounces of gold next year at sub $870/oz cash costs, but with another year of inflationary pressures (many majors are seeing mid to single-digit inflation), I'm less confident in this cost profile being realized. And while even a ~$950/oz cost profile is exceptional compared to the company's current cost profile ex-Magino, the labor situation and energy prices will be important to watch at Magino as it's not ideal to see a combination of a lack of experienced operators during a mine start-up and rising fuel prices as a headwind. Plus, a similar negative dynamic will be in place at Florida Canyon, where labor is also tight in Nevada and fuel prices could hurt margins at this ultra low-grade operation (~0.33 gram per tonne reserve grade).

Valuation

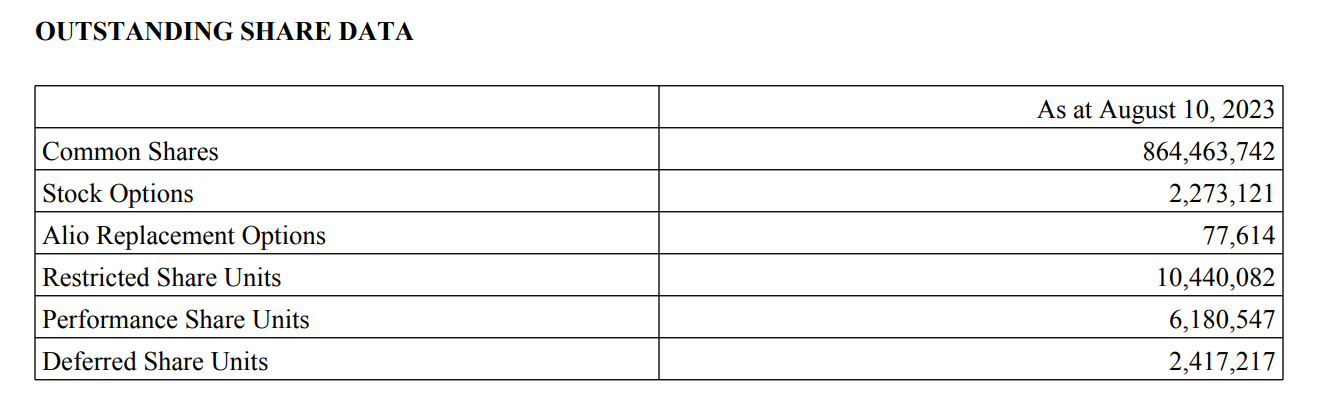

Based on ~886 million fully diluted shares and a share price of US$0.53, Argonaut Gold trades at a market cap of ~$470 million and an enterprise value of ~$620 million. This compares favorably to other junior producers, especially given Argonaut's 300,000+ ounce production profile in 2024, with other 150,000 to 200,000 ounce producers trading at similar or higher valuation figures, like Karora Resources ( KRRGF ) and Wesdome Gold Mines ( WDOFF ). That said, Argonaut's true production profile looks to be closer to ~200,000 ounces (given its plan to wind down its Mexican operations) and one-fourth of this production profile is relatively high-cost, with Florida Canyon still unable to prove that it can consistently operate at sub $1,500/oz all-in sustaining costs. So, if we adjust for the normalized production profile (exclude Mexican operations), Argonaut trades more in line with its peer group following its recent outperformance.

Argonaut Gold Share Count - Company Filings

{kind=link}

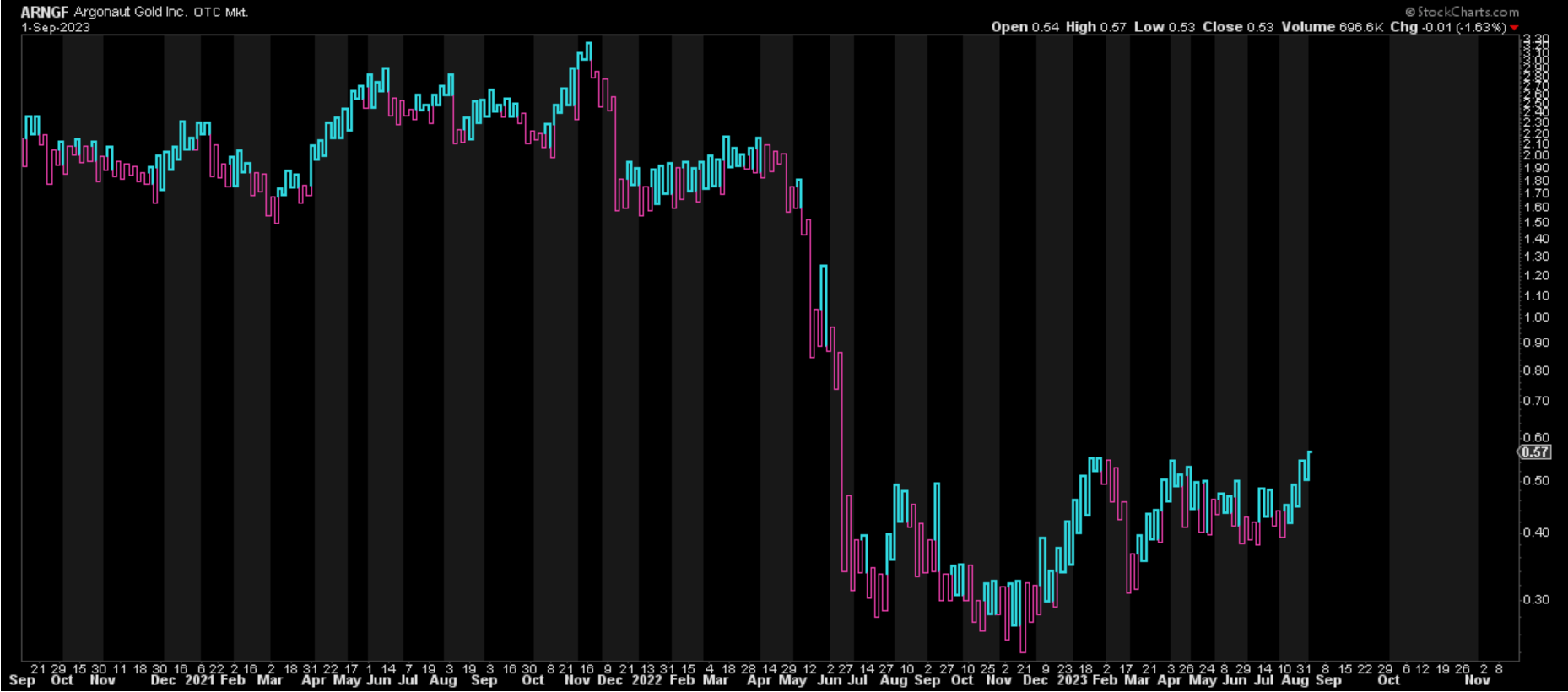

Using what I believe to be a conservative net asset value estimate of ~$640 million (Magino + Florida Canyon at 5% discount rate [-] $330 million in combined corporate G&A and net debt) and applying a 1.0x P/NAV multiple, I see a fair value for Argonaut Gold of $640 million. If we divide this figure by ~886 million fully diluted shares, this translates to a fair value of US$0.72 per share, pointing to a 36% upside from current levels. However, while this is a solid upside, I believe it makes sense to demand a significant margin of safety when investing in small-cap gold producers and especially single-asset producers, and I require a 40% discount to estimated fair value. After applying this required discount, ARNGF's updated buy zone comes in at US$0.43 or lower, suggesting that the stock is ~23% outside of its low-risk buy zone following its recent rally. The technical picture corroborates this view, with the stock reversing sharply on high volume after testing resistance last week, and getting short-term overbought above US$0.55.

ARNGF 3-Year Chart - StockCharts.com

{kind=link}

Obviously, I could be wrong, and the stock could continue its rally and outperformance vs. its peer group. However, while the stock was dirt-cheap and worth accumulating below US$0.27 earlier this year after many investors had thrown in the towel after a ~90% decline, I don't see nearly the same reward/risk setup following its ~70% rally. Plus, in the same period that Argonaut has outperformed followed the appointment of its new CEO, Richard Young, we've seen several other high-quality names continue to sell-off, with many higher-quality and more diversified producers down 15-30%. So, from a relative value standpoint, I see far more attractive bets elsewhere in the sector, and I would view any rallies above US$0.54 on Argonaut Gold as an opportunity to book some profits, hence my neutral rating as the stock approaches a potential resistance area in the US$0.55 - US$0.60 range.

Argonaut Gold - December 2022 Update - Seeking Alpha Premium/PRO

{kind=link}

Finally, it's important to note that if one is bullish on gold which I imagine is the case for most investors reading this as they are looking for leverage to the metal using producers, Argonaut does not provide the same leverage that many expected 18 months ago when they invested for Magino's eventual first gold pour. This is because the company has over 40% of 2024-2026 gold production sold forward at an average price of ~$1,830/oz, meaning it's not benefiting nearly as much from the higher gold prices as some of its peers. This isn't a deal-breaker, but with nearly half of 205 and 2026 gold sales locked in at $1,821/oz, this could be a significant drag on profits if a new bull market in gold emerges, and this could actually lead to underperformance relative to peers given that Argonaut is now one of the most hedged names sector-wide.

Summary

Argonaut Gold has finally crossed the much-awaited finish line at Magino, and the company strategy is solid, with a plan to look at optimizing its two Tier-1 jurisdiction operations while simultaneously looking at moving away from Mexico, a jurisdiction with a declining investment attractiveness profile. However, the stock is now up ~130% off its recent lows; it's far more hedged than its peer group, which reduces its leverage (the primary reason one would own a gold producer) and while Magino is working towards commercial production, labor continues to be an issue sector-wide and especially in prolific mining jurisdictions (Ontario, Nevada, Canada) and energy prices are back on the rise, placing downside risk on margins with Argonaut less able to benefit from higher gold exposures which could offset energy and labor inflation (a negative attribute relative to peers). So, while Argonaut is substantially de-risked relative to nine months ago, I see the reward/risk as more balanced currently, suggesting the best course of action is taking some profits into strength.

For further details see:

Argonaut Gold: Tight Labor Market And Rising Energy Prices Could Impact H2