ATZAF - Aritzia Inc. Q3 Review: Momentum Stalls

Summary

- Aritzia Inc. announced Q3 earnings on Jan. 12, 2023 that beat on the top line, but saw inventory soar and margins fall.

- Management was grilled about the inventory jump, but stressed that inventory levels were extremely low last year, and that discounts won't materially rise.

- While the stock fell sharply today, I still think ATZ:CA has value - I re-iterate Buy with a C$61 price target (down $2 from Oct. 2022) over an 18-month term.

Introduction

On Jan. 12, 2023, Aritzia Inc. ( ATZ:CA , OTCPK:ATZAF ) reported Q3 earnings that exceeded analysts' revenue expectations, but saw gross margins slide and inventory rise. The stock fell 10%, as the headlines highlighted the 188% jump in inventory year over year. Nonetheless, the company's brands continued to impress throughout the quarter, and their U.S. sales now account for half of geographic sales, a monumental shift in a short period of time. My recent Q2 article showcased a bull view, and these results still show that many key tailwinds remain intact. While the global economy and the retail apparel sector as a whole may remain challenged, ATZ:CA remains one of a select few super growth stocks in apparel. I re-iterate my Buy rating with a C$61 ($45 USD) price target over an 18-month period. All numbers in CAD unless otherwise noted.

Q3 Review

While ATZ:CA stock sold off immediately following the earnings release, the results were mixed in nature. Net revenue reached $625MM , up 37% and a new all-time high, capping off a strong fall season. The company's profit rose 9% to $70.7MM, sporting an 11.3% net income margin. The revenue bump was fueled by continued retail expansion, notably in the U.S., and e-commerce growth. The company saw e-commerce sales grow by 36% to $201.4MM from last year. However, some concerns were also raised; gross margins dropped 3% due to higher warehousing costs and SG&A rose to 26% of sales, a 2% increase from last year. Inventory jumped 188% to $508.4MM, which was shocking, considering that last quarter, executives emphasized that inventory was booked earlier in order to mitigate the risk of supply chain disruptions. The $53MM increase quarter over quarter is something of a concern, given the warehousing costs for this inventory played a material part in the margin deterioration. ATZ:CA reported $0.61 of net earnings per share, outpacing last year's mark of $0.56 earnings per share.

Jennifer Wong, CEO of ATZ:CA, highlighted on the Q3 analyst call that client demand continued to exceed expectations, and that their customer base continues to grow. Adjusted EBITDA increased by 9.5% from Q3 2022, while retail store revenue increased by 38.6% from last year to $423.4MM. ATZ:CA had a "Black Fiveday Event", to increase Black Friday sales, and delivered record-breaking results with retail sales hitting an all-time high on Black Friday. ATZ:CA surpassed 2 billion views on TikTok and the company has seen views grow at a rate of nearly 100MM every month, thanks to their impressive influencer outreach efforts. The company also revamped 4 boutiques in the quarter, setting the stage for more organic growth.

The company yet again raised guidance for year-end revenue expectations. ATZ:CA now anticipates $2.14Bn-$2.16Bn in FY2023, which would represent a jump of ~44% from FY2022, and up from the previous outlook of $2.0Bn-$2.05Bn. ATZ:CA noted that these increases are being led by continued outperformance in the United States across both retail and e-commerce channels, and improved performance in Canada within e-commerce sell-through. The company also mentioned that profit margins would shrink throughout the year given the supply chain woes and high inflation, and expect gross margins to dip about 200-225 basis points compared to the prior year, a downgrade from previous estimates of a 100-150 basis point drop. ATZ:CA also re-iterated that CAPEX would be $110MM-120MM this year, and that SG&A would increase ~125 basis points from last year - that would be an improvement from this quarter, which saw SG&A tick up 170 basis points. If ATZ:CA can hit on their top line estimates, and ensure costs and inventory hit their guided forecasts, this market reaction can be reversed quickly.

{kind=link}

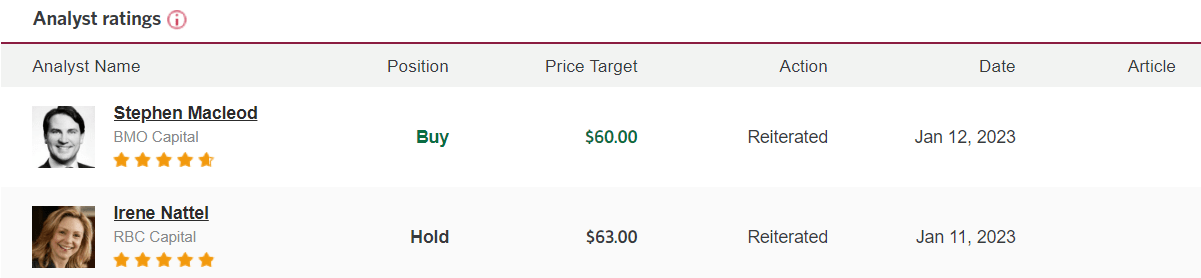

On the negative side, the company also announced sky-high inventory of $508.4MM at the end of the quarter. Management emphasized that inventory was booked earlier in order to mitigate the risk of supply chain disruptions, similar to last quarter. The company emphasized that they are comfortable with its inventory position and expect normalized markdowns to be no greater than pre-pandemic levels. Todd Ingledew, CFO of ATZ:CA, also told BMO's Stephen MacLeod that inventory peaked in Q3. These developments are a bit worrisome, but given ATZ:CA's consistently strong results, I'll take management's word heading into Q4 given such strong growth. Bay St. seems to agree, as evidenced by multiple analysts re-iterating their price targets above C$60. Mark Petrie, CIBC analyst, mentioned to clients that "Though near-term margin pressure and elevated inventory are front and centre, we believe the robust brand momentum outweighs cost concerns".

Margins declined ~310 basis points, with a large portion of the decline attributed to elevated warehousing costs for the inventory. While there's some solace in the fact that management was adamant that the inventory is still high demand items, back to back quarters of inventory approaching the revenue total sparks some concerns.

{kind=link}

Overall, aside from high inventory levels, ATZ:CA is still chugging along and generating standout growth. The company showcased several positives in the quarterly update, even amidst margin deterioration and elevated inventory. If ATZ:CA can prove that inventory peaked in Q3, which I believe they will, and that revenue remains robust, investors should cheer the stock.

Model Forecasts Upside

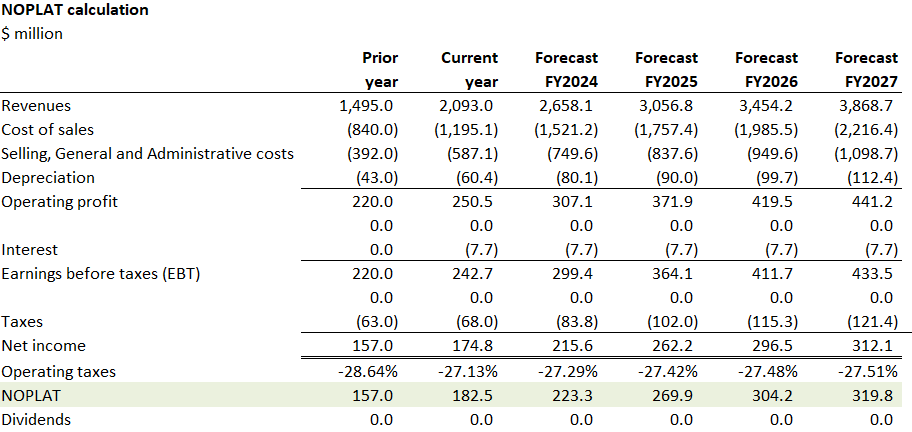

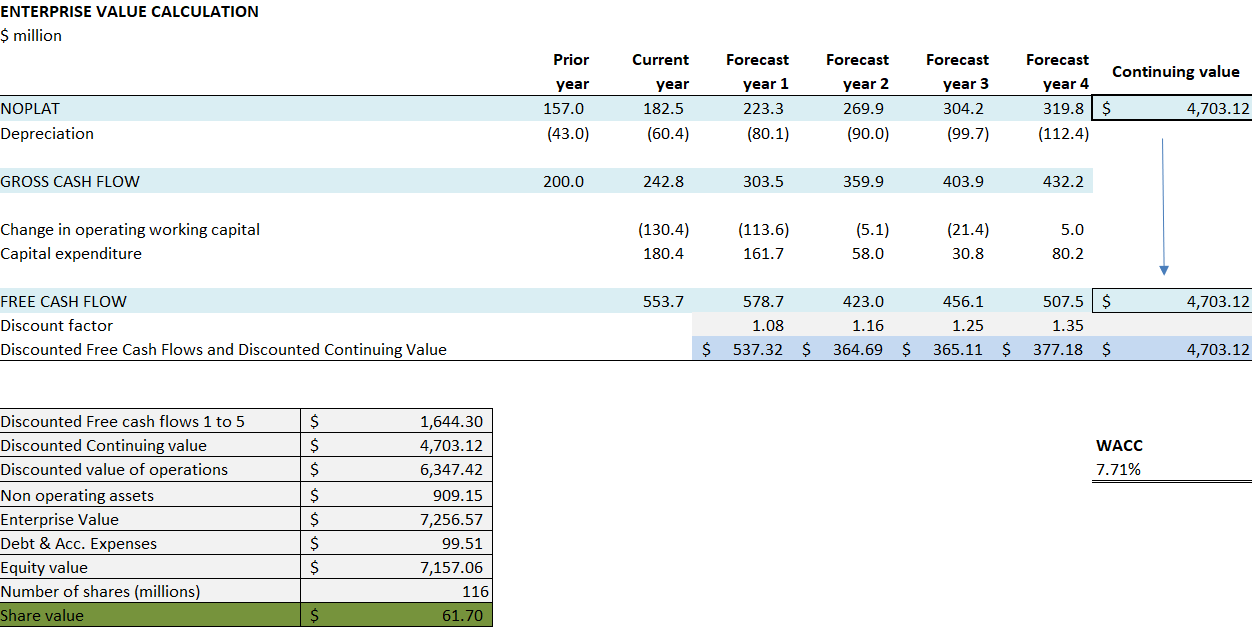

ATZ:CA continues to post impressive results, and the stock price weathered the storm in 2022, even in a rising rate environment. The stock tumbled post-results, but I believe the fundamentals showcase potential to recover. I don't change much in the model from my prior analysis other than some small adjustments given the company's refreshed forecast (notably SG&A increases and margin reductions). This leads to a WACC of 7.7%, a terminal value of almost $5Bn and a FY2023 EV/EBITDA of 18.7.

Author WACC Forecast

{kind=link}

{kind=link}

Conclusion

ATZ:CA continues to impress with outsized growth that's unmatched with most peers. The company delivered strong revenue and profit numbers, and continued to impressively increase sales in the U.S. While margin deterioration and high inventory are things to watch, ATZ:CA remains one of just a few high-growth stories in apparel. In the next earnings report, I hope to see that inventory peaked, as management emphasized on the Q3 call. I re-iterate my previous Buy recommendation, but reduce my price target to C$61 ($46 USD) to account for the increased warehousing costs and the risk that sell-through on these items disappoint.

For further details see:

Aritzia Inc. Q3 Review: Momentum Stalls