ATZAF - Aritzia: Mid-Luxury Powerhouse With Huge Potential

2023-03-16 12:28:20 ET

Summary

- Aritzia has demonstrated a superior strategy and business model through strong growth and fundamentals.

- The company is led by capable management with greater industry experience than peers.

- The combination of these factors and the current valuation create a highly asymmetric risk-return profile to the upside for ATZAF. I expect annual returns greater than 15% for the next.

Introduction & Investment Thesis

Aritzia (ATZAF) is a Canada-based women's apparel retailer operating in the mid-luxury market. The company has spent nearly 40 years building a reputable brand around high-quality, fashionable products. Since the company's IPO in 2016, ATZAF stock has returned investors over 200%. Still, Aritzia remains a small-cap company valued at $3.4 billion, with a long-runway for growth.

My long-term bullish investment thesis for ATZAF hinges on three main factors:

- A superior strategy and business model - driven in large part by an experienced management team.

- Strong and improving fundamentals vs peers.

- An attractive risk-return profile given the company's current valuation and growth potential.

Competitive Strategy and Business Model

The backbone of Aritzia's historical success is its leadership. Aritzia was started by the Hill family as a part of their 70-year-old department store, but the first stand-alone boutique (and official company) was founded in 1984 by Brian Hill. The mission of delivering "everyday luxury" has changed little as Brian Hill remained CEO up until 2022, a total tenure of 38 years. Hill remains part of the executive team as Chair Executive. Hill was proceeded by current CEO Jennifer Wong, who began as a Sales Associate in 1987 (tenure of 35 years). The overall average tenure of Aritzia's executive team is 18 years, compared to an average of 4.8 years within the Consumer businesses sector. The combination of Aritzia's mission and managerial experience sets the company apart from competitors.

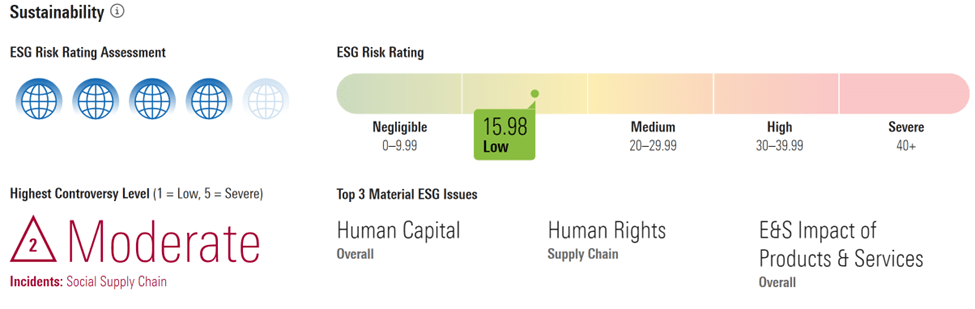

The mission of delivering "everyday luxury" has enabled Aritzia to run in an attractive segment of the fashion market: Mid-Luxury. Mid-luxury apparel retailers aim to produce products with luxury quality but at a more reasonable price. Thus capturing a wider consumer base than traditional luxury brands. Mid-luxury retailers also separate themselves from 'Fast-fashion' companies by sourcing higher-quality materials while keeping ESG factors like sustainability and human rights in mind. McKinsey found that a quarter of younger generations (Millennials and Gen Z) already shop with sustainability in mind. The survey also found almost all of those who are strongly motivated to shop sustainably earned higher than average incomes and would be willing to pay at least 15% more for sustainably sourced goods. Many Fast Fashion companies have already come under fire for ESG issues, including several greenwashing incidents. Mid-luxury stands to benefit from these ESG related consumer trends. Aritzia specifically has a focus on sustainability initiatives and is highly rated on Morningstar's ESG assessment.

{kind=link}

Another benefit of Mid-luxury is durability against macroeconomic factors like inflation and slowing consumer demand. McKinsey found that luxury brands are able to protect profitability as higher income customers rarely change spending habits, even in difficult economies. It would seem Mid-luxury companies, including Aritzia, are able to capture some of this macro durability. CEO Wong highlighted this fact in Aritzia's most recent earnings call :

…what we're seeing is, a tremendous amount of consistency between who's shopping with us, what they're buying, their average basket size have not changed, the average selling price has not changed, the number of units has not changed.

This mid-market strategy allows Aritzia to create considerable brand affinity and customer loyalty.

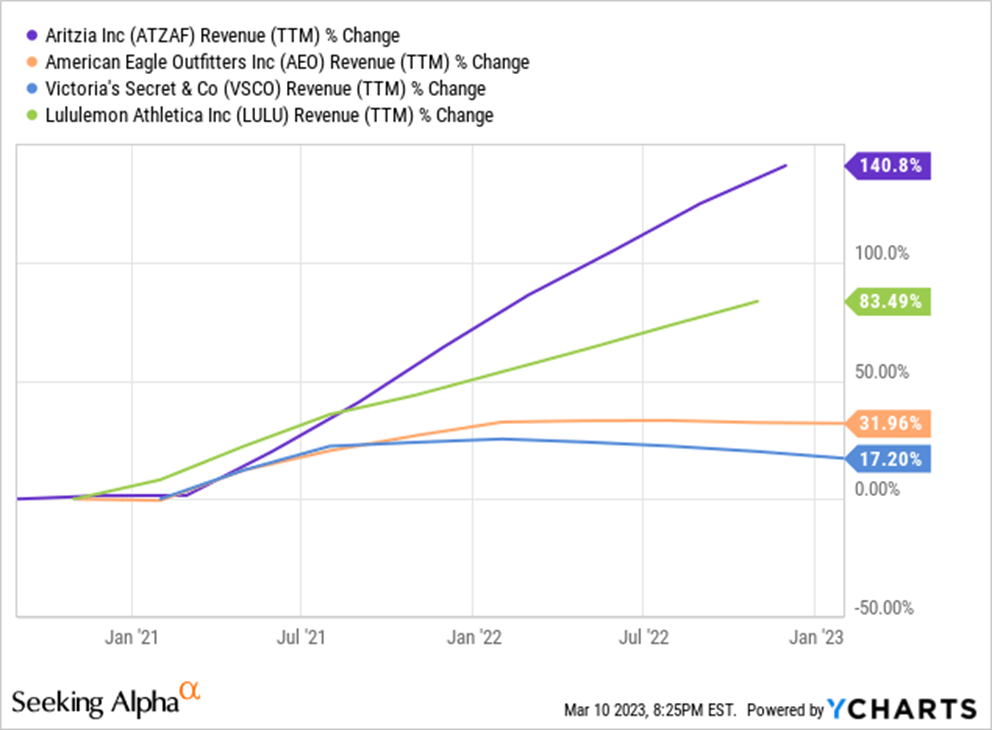

With decades of industry experience, Aritzia has developed core competencies for innovative product development, merchandise planning, manufacturing, and value-chain integration. The company uses a multi-brand approach for broader appeal to different climates and lifestyle activities. The aim of product expansion and development is to capture more "closet share" and increase category cross-sell. 40 years in the industry has allowed Aritzia to build strong relationships high-quality suppliers, thus bolstering their supply chain. Supply chain durability and effective inventory management enabled Aritzia to more effectively capture demand and outperform peers:

{kind=link}

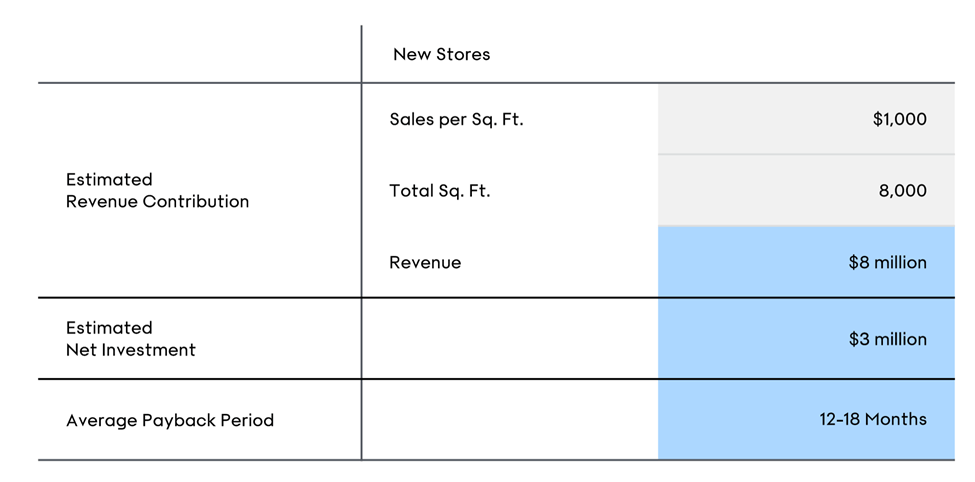

The last piece of Aritzia's differentiated business model is their real estate. Aritzia considers their boutiques as an integral part of their business offering and source of brand awareness. Aritzia takes an extremely measured approach to real estate, choosing quality over quantity. They search for prime locations, focus heavily on shopper experience, and invest in the expansion of well-performing boutiques. Aritzia plans to open only 8-10 stores annually through FY27. This strategy has paid off with impressive store economics.

{kind=link}

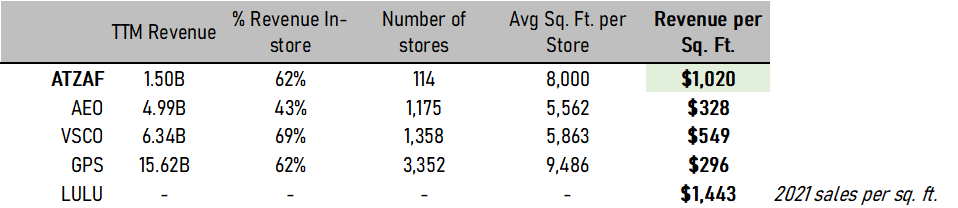

The 'quantity-based' strategy of many competitors like Gap and American Eagle has actually forced them to close and consolidate many stores, highlighting Aritzia's superior strategy. High ROI boutiques coupled with a focus on the customer's experience generates greater brand affinity and demand for Aritzia stores in retail locations. Aritzia has leverage to negotiate terms with landlords with brand strength and greater sales per square foot than competitors - almost in the likes of apparel giant Lululemon (LULU).

{kind=link}

Fundamental Strength and Quality

Aritzia's competitive strengths are made apparent through solid operational performance and growth. Here is a breakdown of how Aritzia fares versus peers financially:

{kind=link}

Topline growth has been the most impressive metric for the company. This is in spite of a tough macro environment as made evident by peers' depressed YoY growth. Even more, the company outperforms industry leader LULU on annual growth the past 3 years (28% vs 26%) and forward growth (38% vs 28%). Aritzia has maintained a leading gross margin for firms its size (excludes LULU), which may exhibit the company's leverage with suppliers and superior product. It's profitability and relative margin strength is evidence of operational excellence and effective inventory planning-further shown by a high inventory turnover ratio.

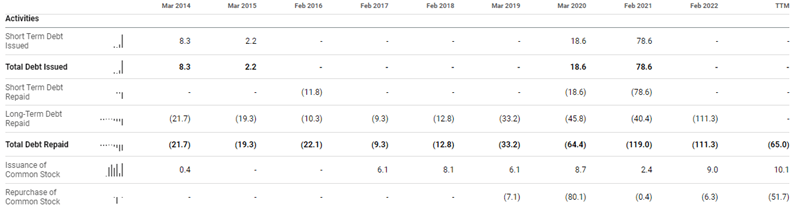

Most of Aritzia's operating performance was driven by internally generated funds. This ties back to the quality of Aritzia's management and their capital allocation ability. Management tends to repay debt frequently and has repurchased more shares than they've issued since their IPO in 2016.

{kind=link}

Additionally, Aritzia leadership has aligned incentives with shareholders, owning nearly 19% of outstanding shares.

Risk-Reward Profile

In tandem with Aritzia's healthy fundamentals, the company's growth potential creates an asymmetric risk-return profile to the upside in my view. The two main pillars of future growth are geographic and omnichannel expansion. Aritzia has relatively low penetration in the massive U.S. apparel market, expected to reach nearly $345B in 2023. The company has only 46 U.S. boutiques out of 114 total, which would equate to $605M of TTM revenue or 0.2% penetration of the overall U.S. apparel market. Given their deliberate approach to boutique selection and compelling store economics, continued U.S. expansion should propel growth for the next 5-10 years. Aritzia has already identified 100+ prime U.S. locations meeting their strict criteria for boutiques. Omnichannel is the second vertical fueling Aritzia's forward growth. Since 2016, e-commerce revenue has grown over 30% annually, now making up almost 40% of total revenue. Aritzia.com serves over 200 countries, allowing Aritzia to tap into the $580B global apparel market .

The primary risk Aritzia faces is macroeconomic uncertainty. Though we saw earlier that mid-upper luxury companies may hold some macro durability, this risk is never completely neutralized. Rising interest rates and elevated inflation make investment in growth difficult. Expanding and acquiring boutiques is not ideal in such an environment as cash carries less pricing power and debt is more expensive. Apparel retail is also heavily dependent on consumer behavior, specifically consumer demand and shopping trends. Though I believe Aritzia has shown relative strength in these areas, given their market positioning and product development expertise. Despite these real risks, Aritzia's risk-return profile is highly attractive for long-term investors in my view, especially considering the current valuation.

Valuation & Summary

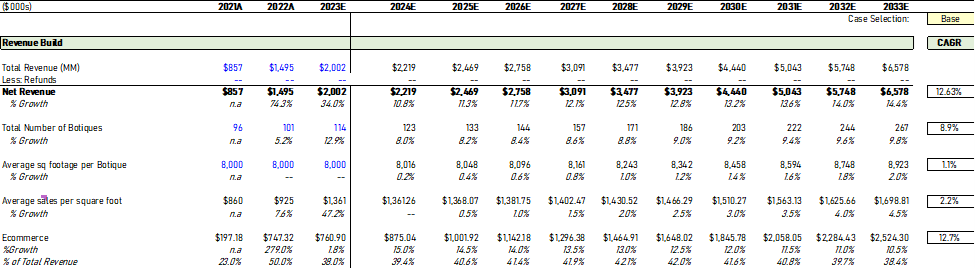

Below is a 10-year bottom-up revenue build for Aritzia using forecasted boutique acquisitions and expansions (sq ft), e-commerce growth, and average sales per square foot. I used management's estimate of 8-10 new boutiques annually, per store square foot growth of 0.2% annually, average sales per square foot growth of 0.5% annually, and e-commerce growth of 12.7% annually through 2033. This resulted in total annual revenue growth of 12.6% through 2033. My forecast period is longer, but closely aligns with management guidance of 15-17% through FY27.

{kind=link}

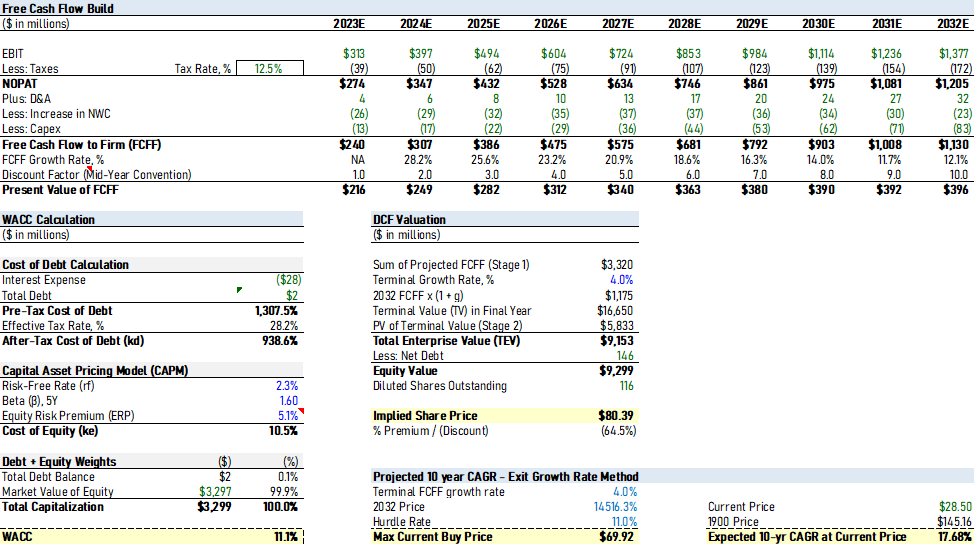

Moving down the income statement, I expect gross margins to slowly expand to 43% in year 10 driven by continued competitive pricing power. I also see Aritzia reducing SG&A margins over my forecast to 25% of revenues (currently 27%) as they realize scale advantages with their disciplined operating approach. This results in EBIT margins climbing to the mid-teens by 2032. I expect change in net working capital, depreciation & amortization, and capex to remain relatively consistent with historical numbers as a percentage of incremental revenue. My estimate of fair value per share for ATZAF based on these assumptions is $80.61 per share, representing a discount of 64.5% from the current price. In addition, I projected the expected 10-year share price CAGR. At the stock's current price, I expect a 17.58% annual return through 2032.

{kind=link}

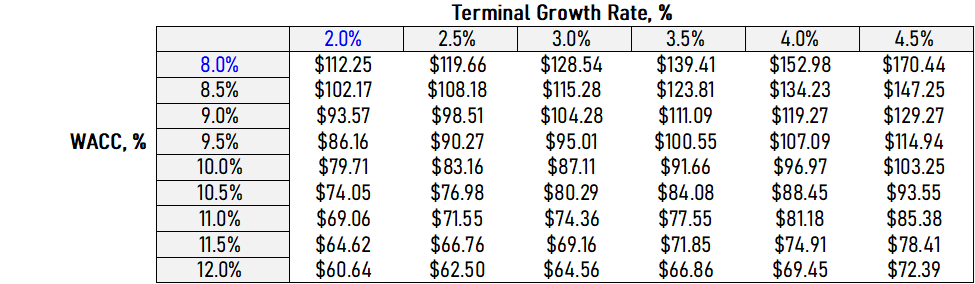

Because DCFs are heavily dependent on the WACC and terminal growth assumptions, below is a sensitivity analysis of changes in these assumptions on the calculated intrinsic value.

{kind=link}

In summary, Aritzia has a proven track record of success within the Mid-luxury apparel industry, bolstered by a superior managerial strategy and business model. The company's competitive advantages are made evident through comparative fundamental strength and operational excellence. ATZAF is an attractive long-term buy in my view, with an asymmetric risk-return profile, wide margin of safety (60%+), and expected 10-year annual return above 17%.

For further details see:

Aritzia: Mid-Luxury Powerhouse With Huge Potential