ASAN - Asana Q3 Preview: Not Worth The Risk

2023-11-23 23:59:32 ET

Summary

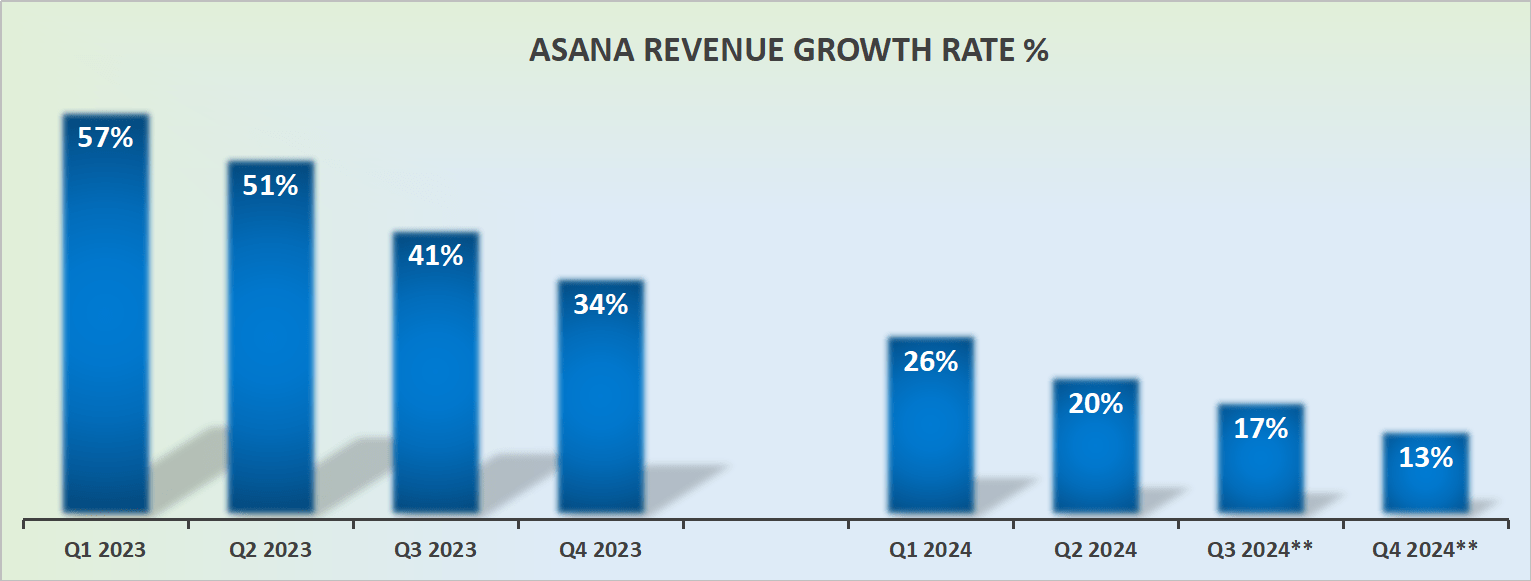

- Rapidly moderating growth rates highlight the urgency of addressing long-term financial sustainability.

- The absence of meaningful guidance raises doubts about Asana's visibility and future trajectory.

- Ultimately, the extended timeline to profitability and slowing customer adoption curve make Asana a less compelling investment option for me.

Investment Thesis

Asana ( ASAN ) is a work management platform designed to help teams organize and coordinate their tasks and projects effectively. It provides a collaborative space where team members can create and track tasks, fostering improved communication and productivity within organizations.

Asana stresses that it can serve the nuanced needs of organizations to foster collaboration in the evolving landscape of work management solutions.

There's a lot to like about Asana as it heads into its fiscal Q3 2024 earnings results in two weeks (not calendar year), for instance, Asana's very strong balance sheet being amongst its top considerations.

But I don't believe the positive elements are sufficiently alluring to detract from the overall reality that its growth rates are rapidly moderating down towards the mid-teens, while the business is still more than 18 months away from being profitable, at the very minimum.

Rapid Recap,

I concluded my previous neutral analysis by saying,

While its robust balance sheet provides stability, the challenge is to justify investors paying 7x forward sales for a company still reporting losses.

Author's work on ASAN

Since I penned that analysis back in August, the stock has gone nowhere fast. And today, I stand by that succinct argument, that there's not enough to entice investors to this name.

Asana's Near-Term Prospects

Here I'll describe some bullish and bearish aspects to help readers think through this opportunity.

Asana recently had its Investor Day here they discussed their success in securing significant land deals reflecting demand for its collaborative work management platform.

Notably, a key win involved a customer seeking a long-term partnership with a focus on reducing technology sprawl by replacing multiple existing applications with Asana, often described as platformization.

Asana describes its ability to accommodate complexities and facilitate collaboration across various departments positioning it as a strategic partner for companies looking to enhance efficiency and standardization.

What's more, Asana notes that as AI becomes increasingly integral to organizational strategies, Asana's vision to assist clients in navigating this landscape and deploying AI effectively demonstrates its forward-thinking approach.

Asana's focus on addressing nuanced organizational needs, fostering collaboration, and embracing emerging technologies positions it as a dynamic player with substantial growth prospects in the evolving landscape of work management solutions.

Despite its notable successes, Asana acknowledges that it is facing headwinds, particularly within the tech sector, where budget scrutiny and layoffs in tech companies have prompted a reevaluation of spending.

Moreover, the strategic shift toward larger enterprise deals and the realignment of corporate and enterprise teams in regions such as EMEA pose challenges. While focusing on substantial deals can be strategic, there is a risk of neglecting the lower end of the market, leaving room for competitors to gain traction.

Given this context, let's now turn to focus on its financials.

Revenue Growth Rates Moderate

{kind=link}

Asana's growth rates are moderating, and of that there can be no doubt. The big question facing investors is how will fiscal 2025 look from this lower comparable base?

Given that Asana recently had its Investors Day and failed to provide any sort of meaningful guidance, this reinforces my theory that Asana hasn't got much visibility either.

So, on the one hand, Asana's comparables do ease up. And it should be relatively easy for it to deliver mid-teens CAGR, perhaps even high teens CAGR . On the other hand, given that its customer adoption curve appears to be slowing down, this will mean that Asana will be left with only price hikes to support its growth prospects.

Case in point, in Q2 2023 (the prior year), customers spending more than $5K were up 41% y/y to 18,040. And for its most recently published quarter?

ASAN Q2 2024

Ultimately, you can only take price hikes up for so long before you end up pushing your customers away from your platform towards that of your competitors.

The Bear Case: Profitability Profile

Asana will most likely exit fiscal 2024 with its underlying profit margin at approximately negative 12%. This means that over the past 12 months, Asana has dramatically improved its profitability profile from negative 25% to negative 12%.

However, this still leaves Asana with a long path toward breakeven profitability. Indeed, I suspect that Asana took the low-hanging fruit in the first instance, meaning that the climb from negative 12% to breakeven could take a further 18 months. At the very least.

To be more specific, I don't imagine that Asana will exit fiscal 2025 with better than negative 5% operating margins.

Consequently, how long will investors continue to be cheerleaders for this stock, when there are so many other similar businesses that have very similar growth rates and are already profitable?

Allow me to compare and contrast two businesses very briefly. Asana and monday.com ( MNDY ) are both popular project management tools designed to enhance team collaboration, but they differ in their approach and features.

Asana is known for its intuitive interface and flexibility, offering a wide range of project views such as Kanban boards, timelines, and lists. It excels in task management and integrates seamlessly with various third-party applications. On the other hand, monday.com is recognized for its visually appealing and customizable workspaces, providing a centralized hub for project tracking. While Asana leans towards simplicity and ease of use, monday.com leans towards adaptability in project organization. Note, I've recently discussed why I'm bullish on monday.com here .

Yes, I recognize that Asana's CEO is a strong advocate for buying Asana's stock. And yes, I recognize that Asana has nearly $500 million of net cash on its balance sheet. And while those two considerations are ''nice to have'' they are a distraction from the underlying value proposition that Asana offers investors.

The Bottom Line

Despite Asana's notable successes and strategic positioning in the collaborative work management landscape, the glaring challenges on the horizon render it a less-than-enticing investment opportunity.

The significant distance from achieving profitability, coupled with the evident deceleration in growth rates, raises substantial concerns about the company's long-term viability.

While Asana's emphasis on addressing organizational complexities and embracing emerging technologies is commendable, the current financial trajectory, marked by moderating growth and a prolonged path to profitability, renders the stock unattractive for investors seeking a more robust return on investment.

For further details see:

Asana Q3 Preview: Not Worth The Risk