ASAN - Asana: The Stock Deserves A Substantial Premium

2023-12-01 02:54:10 ET

Summary

- Asana's stock might look overvalued, but its premium is well-deserved due to the exceptional business execution.

- ASAN has a strong balance sheet with high gross margins allowing for continued innovation and revenue growth.

- Potential investors should be prepared for volatility and hold the stock for multiple years, but the company's consistent beating of consensus estimates suggests positive surprises in upcoming earnings releases.

Investment thesis

Asana ( ASAN ) was one of the hottest stocks during the 2021 stock market mania, but now it trades more than seven times below all-time highs. My valuation analysis suggests the stock is still overvalued, but I believe that the premium is well-deserved. The company's stellar revenue growth is backed by the superiority of its solutions which add vast value to customers. Asana's business model demonstrates exceptional land-and-expand capacity, which I see from stellar dollar-based retention metrics. The company is well-positioned to continue innovating and driving revenue growth, given the strong balance sheet and unmatched 90% gross margin. Potential investors should be ready to hold this stock for multiple years and stomach substantial volatility if they finally decide to opt in. I assign the stock a "Strong Buy" rating.

Company information

Asana is a work management platform that helps organizations orchestrate work, from daily tasks to cross-functional strategic initiatives. According to the latest 10-K report , as of the FY2023 year-end, the company had more than 2.5 million paid customers.

The company's fiscal year ends on January 31 with a sole operating segment. In FY 2023, the company generated almost 40% of the total sales outside the U.S.

{kind=link}

Financials

Asana went public relatively recently, in late 2020. Therefore, the earnings history is not very long. Still, we can see several important points from the multiple years of financial trend analysis.

{kind=link}

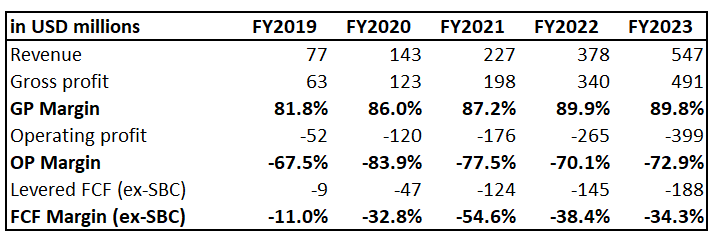

Revenue increased more than sevenfold over the last five fiscal years, representing a staggering 63% CAGR. However, it is essential to highlight that the base year revenue was relatively low. I like the fact that ASAN demonstrated strong gross margin expansion as the business scaled up and achieved almost 90% level, which is nothing but stellar. A wide gross margin allows the company to reinvest a large portion of revenue in R&D and marketing, which ASAN actually does. The company allocates half of its sales to R&D, which demonstrates a solid commitment to innovation and building long-term value for shareholders. However, it is significant to point out that the SG&A to revenue ratio is also very high and is still not very far from a hundred percent despite rapid revenue growth.

ASAN has more than half a billion dollars in outstanding cash, which makes the company well-positioned to continue investing aggressively in growth and innovation. The company's cash position is almost twice the total debt, underscoring strong liquidity. The TTM levered free cash flow [FCF] is positive, meaning the company's cash burn is decelerating. However, I would like to emphasize a couple of important points. First, the TTM stock-based compensation [SBC] is substantial, representing almost one-third of the company's TTM revenue. Second, ASAN issued almost $370 million worth of stock in the trailing twelve-month period.

Seeking Alpha

The latest quarterly earnings were released on September 5, when the company topped consensus estimates. Revenue grew by 20% YoY, which allowed ASAN to continue improving profitability metrics. The gross margin was at a stellar 90%, and the operating margin improved YoY from -82.5% to -45.2%. The operating margin expansion was due to the significantly improved SG&A to revenue proportion, while R&D investments still represented more than half of the company's quarterly sales.

Seeking Alpha

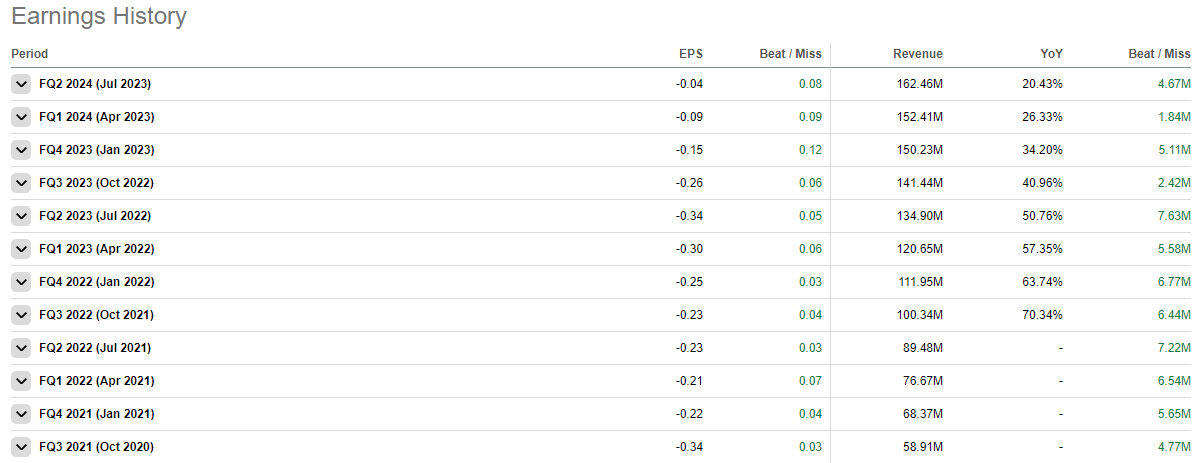

I will not dig into much deeper details because the new earnings release is approaching, and I would like to be more forward-looking. The earnings for the upcoming quarter are scheduled for release on December 5. Quarterly revenue is projected by consensus at $164 million, which means a 16% YoY growth. The adjusted EPS is expected to follow the top line and improve from -$0.26 to -$0.11. The solid bullish sign is that there were twelve upward EPS revisions over the last 90 days.

Seeking Alpha

The fascinating fact about Asana is that the company has never missed consensus estimates, though the earnings history is relatively short. Consistency in beating revenue and EPS projections suggests sound planning and the predictability of financial performance. Past performance is not a guarantee of future success, but the fact that ASAN consistently beats consensus estimates increases the probability that the upcoming earnings release will also deliver positive surprises.

{kind=link}

Aggressive recent ASAN stock buying by CEO Dustin Moskovitz also makes me more optimistic about the upcoming earnings release. The company continues demonstrating a firm commitment to innovation by adding new artificial intelligence capabilities to its offerings. This is crucial because innovation looks like ASAN's key strength, which fuels strong revenue growth and profitability improvement.

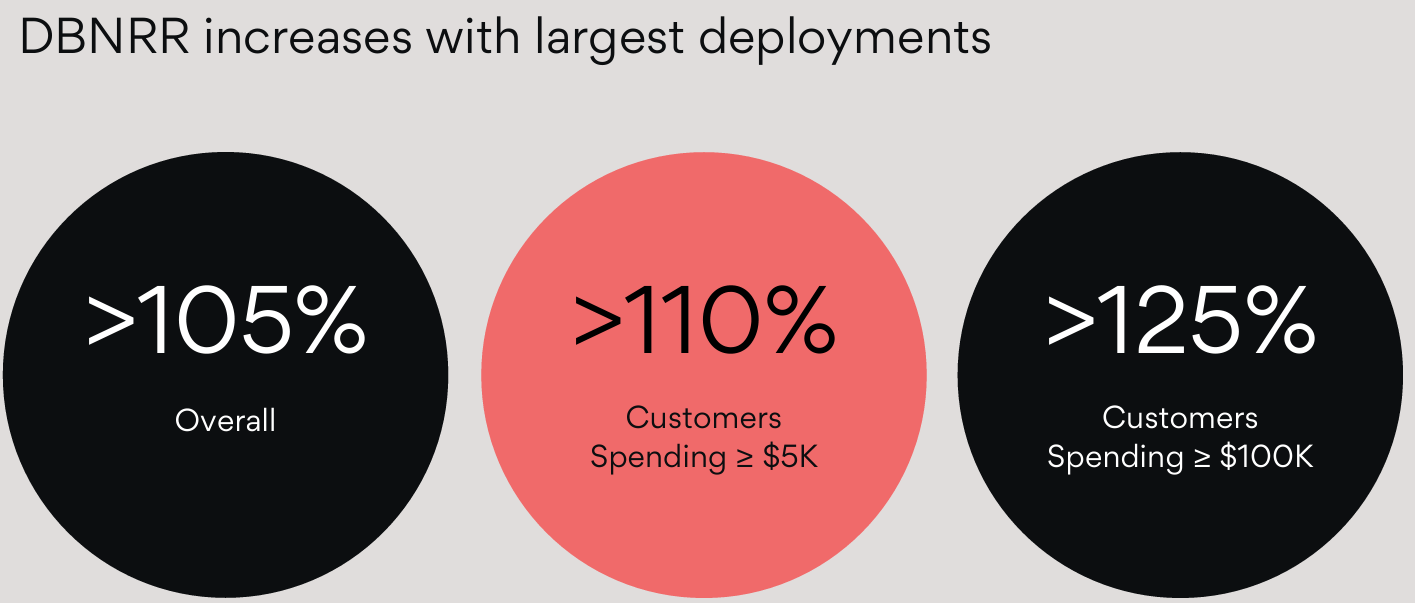

The company's key metrics suggest that ASAN will highly likely deliver another stellar quarter. Having a 90% gross margin and far beyond 100% Dollar-Based Net Retention Rate [DBNRR] from the largest customers clearly indicates the company's product superiority compared to competitors. High gross margin indicates strong pricing power and stellar DBNRR means the company is exceptionally absorbing all the upselling and cross-selling opportunities. Strong DBNRR also means that Asana is succeeding in building an ecosystem that apparently will increase customer switching costs, which is also good for business. The ability to land and expand is a critical success factor in the SaaS industry, and Asana looks like a rockstar from this perspective.

{kind=link}

Consistent double-digit revenue growth and a 90% gross margin underscore the business model's scalability and high efficiency. The fact that the relatively young company is already present in more than 200 countries and generates almost 40% of sales outside the U.S. also emphasizes the strength of Asana's business approach.

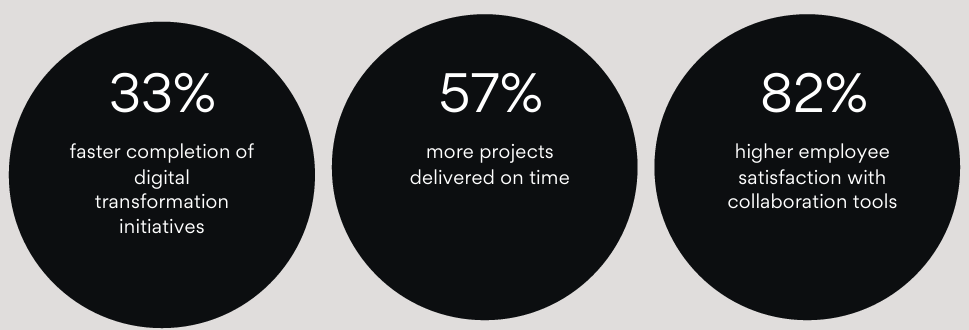

I do not expect guidance downgrades from the management even despite the challenging macro environment when businesses are keen on cutting costs. From the IDC's research quoted in the latest Asana earnings presentation , it looks like the company's solutions actually help to cut costs. The current challenging environment likely is more of a tailwind for Asana as businesses seek more cost efficiency, which can apparently be achieved by streamlining internal processes.

{kind=link}

Valuation

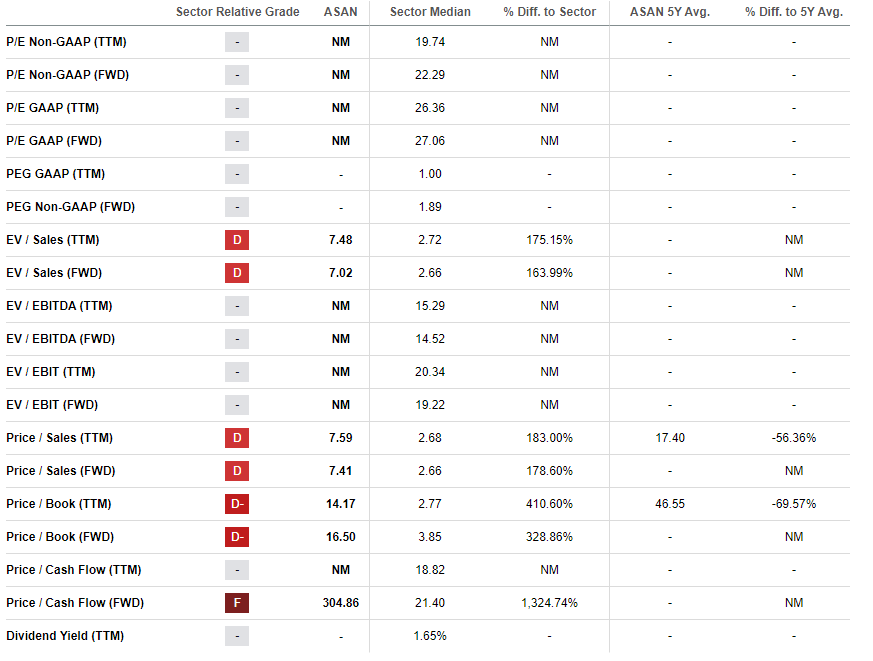

ASAN rallied by a massive 59% year-to-date, significantly outperforming the broader U.S. stock market. As an aggressive growth company, ASAN has sky-high valuation ratios . However, if compared to the historical averages, multiples have moderated.

{kind=link}

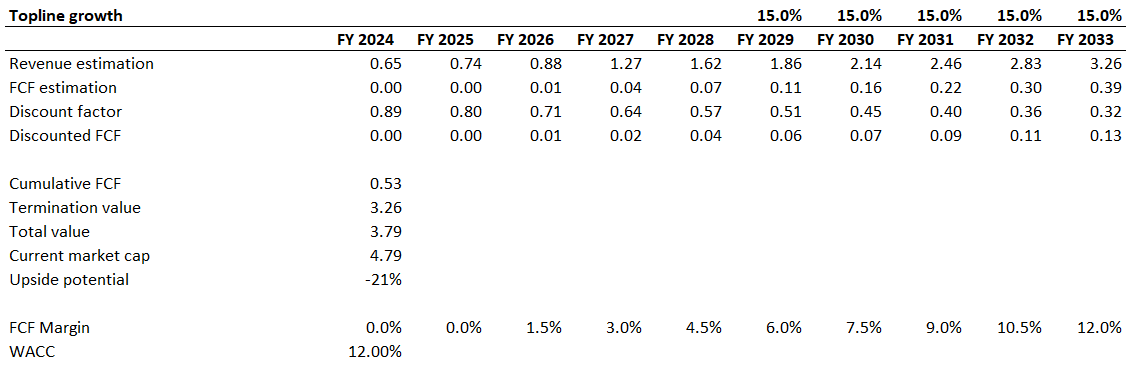

I want to proceed with the discounted cash flow [DCF] simulation. I use an elevated 12% WACC since ASAN is a young company with uncertain breakeven timing. Consensus revenue estimates expect revenue to almost triple between FY 2024 and FY 2028, which I incorporate into my DCF. For the years beyond, I expect revenue growth to moderate and project a 15% CAGR. I expect ASAN to generate a positive FCF ex-SBC margin starting from FY 2026 with a 150 basis points yearly expansion. I do not consider the net cash position for my fair value calculation because I expect ASAN to burn this cash in 2024-2025.

{kind=link}

My simulation shows the business's fair value is approximately $3.8 billion. This is around 21% higher than the current market cap, which indicates substantial overvaluation. However, ASAN is a high-quality business demonstrating strong revenue growth and unmatched profitability dynamics. Thus, the premium looks well-deserved.

Risks to consider

The valuation is high even under generous assumptions, significantly increasing investor risks. Any indications of revenue growth decelerating or profitability expansion lagging behind the estimated trajectory will likely lead to investors' disappointment and potential stock sell-off. The stock trades seven times lower than its all-time high of late 2021, underscoring high volatility. ASAN is apparently a long-term bet for investors seeking a potential moonshot and ready to hold the stock over decades. Dollar-averaging looks like a sound approach to building up the position in ASAN, considering substantial volatility.

The technological landscape is rapidly evolving, which poses substantial risks to Asana's ability to sustain rapid revenue growth and vast pricing power. As technological advancements shape the future of work management solutions, Asana's agility and strategic responses to industry shifts will play a pivotal role in ensuring sustained success. It is crucial to understand that Asana's past stellar performance does not guarantee that the company will be able to deliver staggering results over the long term.

Bottom line

To conclude, Asana's looks like a "Strong Buy" for long-term investors. The stock looks overvalued from the calculations perspective, but the premium looks well-deserved considering the company's exceptional performance and growth prospects.

For further details see:

Asana: The Stock Deserves A Substantial Premium